Medical Microcontrollers Market Outlook:

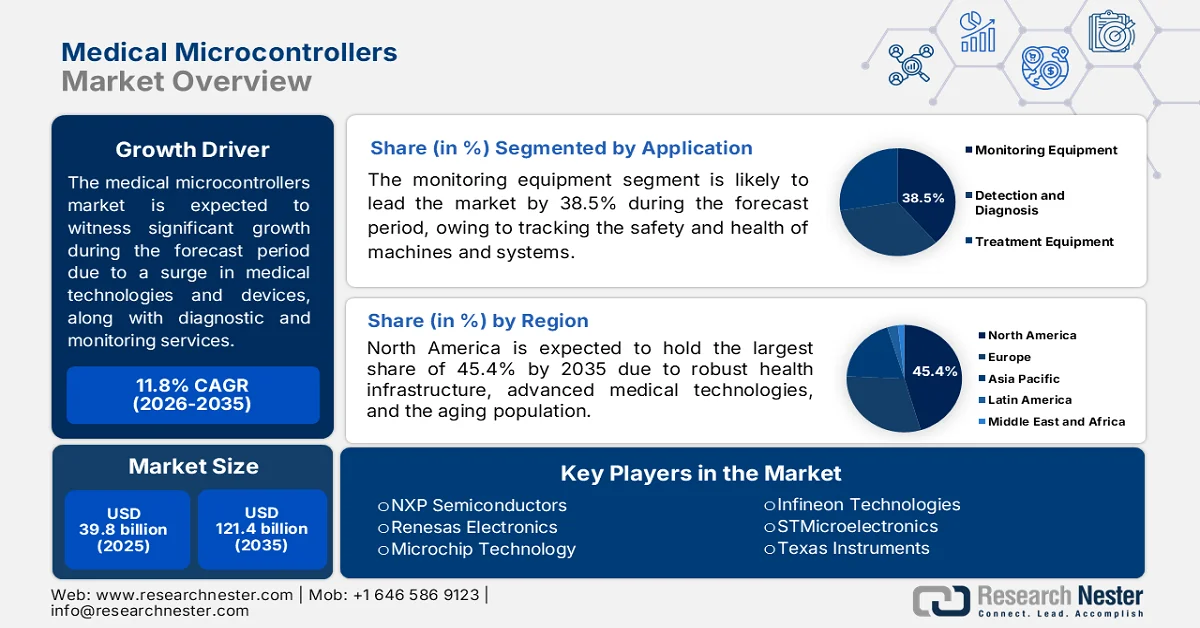

Medical Microcontrollers Market size was valued at USD 39.8 billion in 2025 and is projected to exceed USD 121.4 billion by the end of 2035, expanding at over 11.8% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of medical microcontrollers is estimated at USD 44.5 billion.

The worldwide medical microcontrollers market is witnessing a significant transformation, which is underpinned by the widened healthcare technology infrastructure, trade dynamics for appliances and instruments utilized in medical settings for treatment, monitoring, and diagnostics, and the expansion in the growth of medical devices. According to a data report published by the Government of Canada in July 2025, the global medical device industry was worth USD 555.7 billion, excluding in vitro diagnostics. Additionally, it is predicted that this industry will be valued at USD 725.1 billion and grow at a 5.5% rate by the end of 2029. Besides, the number of instruments and appliances utilized in the industry is equally proliferating the market’s growth and demand globally due to continuous import facilities.

Global Shipment of Medical Instruments and Appliances Import, 2023

|

Countries |

Trade Valuation (1,000 USD) |

Production Quantity in Items |

|

U.S. |

19,524,852.4 |

2,377,630,000 |

|

Europe |

11,498,576.3 |

764,181,000 |

|

Singapore |

1,047,377.1 |

448,089,000 |

|

India |

1,024,496.8 |

1,342,460,000 |

|

Brazil |

652,320.8 |

942,484,000 |

|

South Africa |

409,816.2 |

170,085,000 |

|

Malaysia |

390,260.2 |

71,207,500 |

|

Thailand |

200,494.3 |

79,891,200 |

|

Colombia |

275,664.1 |

277,253,000 |

|

Chile |

271,992.6 |

97,830,500 |

Source: WITS

Furthermore, the adoption of wireless communication, energy efficiency and miniaturization, innovative data security features, the integration of machine learning and artificial intelligence (AI), and the development of multi-functional technologies are certain trends that are bolstering the medical microcontrollers market. As stated in an article published by iScience in May 2025, the International Telecommunication Union (ITU) noted that the need for data traffic is anticipated to increase by a factor of 100 in comparison to current levels by the end of 2030. Besides, to combat the disruptive technological shifting, there is a requirement for developing enhanced functionalities to boost network performance. Therefore, 6G can elevate coverage and sensing accuracy from 70% to 99%, along with boosting reliability from 99.9% to 99.999%, thereby positively fueling the market development.

Key Medical Microcontrollers Market Insights Summary:

Regional Highlights:

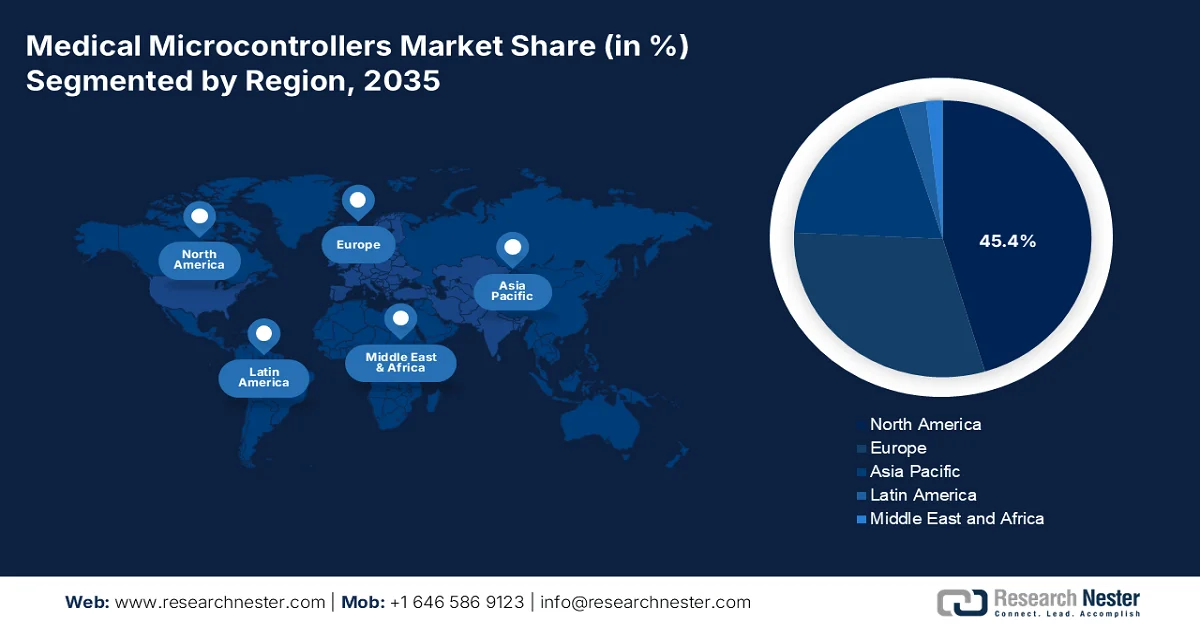

- North America medical microcontrollers market is projected to command 45.4% of the market share by 2035, reinforced by the presence of advanced healthcare infrastructure, growing adoption of innovative medical technologies, and rising demand for implantable, monitoring, and diagnostic devices

- Asia Pacific is anticipated to capture a 19.5% share in the market during the forecast period, stimulated by expanding wearable technology adoption, accelerating healthcare digitalization, and increasing automotive demand

Segment Insights:

- The monitoring equipment segment is expected to secure 38.5% of the medical microcontrollers market by 2035, supported by its critical function in real-time tracking of system safety, health, and operational performance

- The 32-bit microcontrollers segment is forecast to account for 29.5% of the market during the forecast period, fueled by its capability to process complex computations, enable rapid device control, and support advanced smart features

Key Growth Trends:

- Growth in telemedicine

- Innovations in wearable health technology

Major Challenges:

- Stringent regulatory compliance and certification hurdles

- Rapid Technological Obsolescence and Design Complexity

Key Players: NXP Semiconductors (Netherlands),Renesas Electronics (Japan),Microchip Technology (U.S.),Infineon Technologies (Germany),STMicroelectronics (Switzerland),Texas Instruments (U.S.),Silicon Laboratories (U.S.),Analog Devices (U.S.),Ambiq Micro (U.S.),Hangzhou SDIC Microelectronics (China),Intricon (U.S.),Minnetronix Medical (U.S.),Neways Electronics (Netherlands).

Global Medical Microcontrollers Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 39.8 billion

- 2026 Market Size: USD 44.5 billion

- Projected Market Size: USD 121.4 billion by 2035

- Growth Forecasts: 11.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: China, India, South Korea, Singapore, Australia

Last updated on : 29 June, 2026

Medical Microcontrollers Market - Growth Drivers and Challenges

Growth Drivers

- Growth in telemedicine: The expansion in telehealth services has created a suitable growth demand for the medical microcontrollers market with strong connectivity features. According to an article published by NLM in July 2024, a clinical study was conducted on 242,848 Kaiser Permanente patients, which demonstrated that early exposure to initial telemedicine care is related to high rates of HbA1c measurement. This includes 90.5% of telephone and 91% for video, in comparison to 86.7% without physical visits. In addition, the exposure is also associated with low levels of HbA1c, accounting for 67.3% of telephone, 68.5% of video, compared to 66.6% without visits. Therefore, with this increased participation of patients in telehealth services, there is a huge growth opportunity for the market.

- Innovations in wearable health technology: The increased proliferation of wearable medical devices, such as ECG patches, continuous glucose monitors, and smartwatches with health monitoring, is driving the medical microcontrollers market globally. As stated in an article published by JMIR Organizations in February 2025, a clinical study was conducted on 5,591 adults, particularly in the U.S., denoting that since the pandemic, there was an increase in wearable device adoption to 36.3% as of 2022. In addition, the willingness to share medical data with healthcare professionals accounted for 78.4% of adults, and 26.5% of adults accomplished in sharing medical data. Besides, female adults were considered to highly utilize wearables with increased incomes ranging from USD 50,000 to USD 75,000, thus proliferating the market’s upliftment.

Challenges

- Stringent regulatory compliance and certification hurdles: The medical microcontrollers market tends to navigate complex regulatory landscapes across multiple jurisdictions, each with unique requirements. Compliance with IEC 60601 for medical electrical equipment safety, IEC 62304 for software lifecycle processes, and ISO 14971 for risk management demands significant engineering resources and documentation. The transition to new functional safety standards like IEC 61508 and ISO 26262 for critical medical applications adds further complexity. Besides, regulatory bodies require extensive verification and validation data, including failure mode and effects analysis, electromagnetic compatibility testing, and environmental stress screening.

- Rapid Technological Obsolescence and Design Complexity: The breakneck pace of semiconductor technology evolution creates significant challenges for medical device manufacturers in the medical microcontrollers market. Besides, architectures evolve rapidly, with new instruction sets, memory technologies, and peripheral integrations emerging frequently. Medical device development cycles typically span 3 to 5 years, which means that products launched with microcontrollers are already considered legacy. Furthermore, manufacturers must balance the desire for advanced features against the need for long-term product stability and availability. The increasing complexity of medical devices requires integration of multiple functions, such as sensor interfacing, wireless connectivity, cryptography, and real-time control, onto single microcontrollers, pushing thermal and power budgets.

Medical Microcontrollers Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

11.8% |

|

Base Year Market Size (2025) |

USD 39.8 billion |

|

Forecast Year Market Size (2035) |

USD 121.4 billion |

|

Regional Scope |

|

Medical Microcontrollers Market Segmentation:

Application Segment Analysis

Based on the application segment, the monitoring equipment sub-segment, which is part of the application segment, is projected to grab the largest share of 38.5% in the medical microcontrollers market by the end of 2035. The sub-segment’s upliftment is primarily attributed to its importance in tracking the safety, health, and performance of systems or machines in real time. According to an article published by the NCBI in April 2026, in a type 1 diabetes clinical study, the utilization of either or both controlled glucose monitoring and insulin pump surged from 19.7% to 77.4% as of 2023. Additionally, there was an increase in the utilization of glucose monitoring devices when Medicare coverage services broadened. Besides, the technology adherence has been optimized due to usability, accuracy, and wide-ranging coverage, thereby making it suitable for the sub-segment’s growth.

Type Segment Analysis

During the forecast period, the 32-bit microcontrollers type is predicted to account for the second-largest share of 29.5% in the medical microcontrollers market. The segment’s growth is effectively driven by its role as the brain of devices, suitable enough for processing 32 pieces of data at a time. It connects with integrated circuits, permitting the administration of complicated math, controlling different parts at a rapid speed, and running smart features. As stated in a data report published by the IEEE Organization in February 2026, a secured 32-bit RISC-V microcontroller was integrated with a fast and lightweight post-quantum NTRU-HPS cryptosystem for the Internet of Things (IoT), resulting in 2,040 cycles for KeyGen, along with 2,039 cycles for standard encryption, and 3,058 cycles for decryption. In addition, this led to the achievement of more than 300 and 540 times of encryption and decryption, thereby bolstering the segment’s demand.

Global Integrated Circuits Export and Import, 2024

|

Countries/Components |

Export (USD Billion) |

Import (USD Billion) |

|

Chinese Taipei |

223 |

- |

|

South Korea |

139 |

- |

|

China |

171 |

174 |

|

Hong Kong |

- |

217 |

|

Singapore |

- |

81.8 |

|

Global Trade Value |

928 |

|

|

Global Trade Share |

4.0% |

|

|

Product Complexity |

1.2 |

|

|

Export Growth |

16.9% |

|

Source: OEC

Connectivity Segment Analysis

The Bluetooth sub-segment under the connectivity segment is expected to garner a suitable share in the medical microcontrollers market by the end of the stipulated timeline. The sub-segment’s development is highly fueled by its crucial role as the wireless standard for personal and portable medical devices. Its dominance in the medical microcontroller market is driven by an intrinsic alignment with the industry's core requirements: ultra-low power consumption, adequate bandwidth for physiological data, and ubiquitous smartphone integration. Unlike Wi-Fi, which demands robust power supplies and heavy protocol stacks, BLE enables medical devices to operate continuously on tiny coin-cell batteries for months or even years. This makes it the natural choice for wearable monitoring devices like continuous glucose monitors, cardiac patch recorders, and pulse oximeters, where patient mobility and comfort are paramount.

Our in-depth analysis of the medical microcontrollers market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Type |

|

|

Connectivity |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Medical Microcontrollers Market - Regional Analysis

North America Market Insights

The North America medical microcontrollers market is anticipated to account for the highest share of 45.4% by the end of 2035. The market’s upliftment in the region is effectively driven by the existence of a strong healthcare facility, an increase in the adoption of innovative medical technologies, the largest medical device economy, the patient population, and the demand for implantable and monitoring devices, along with diagnostic equipment. According to an article published by Advamed Organization in 2026, the U.S. is considered the largest medical device industry globally, comprising more than 40% of the overall medtech sector. Likewise, medtech exports have outpaced imports, including an increase of over USD 1.1 billion, while there has been a decrease by 38% in the number of patient-days accommodation in hospitals due to advanced medical technologies and devices, thereby bolstering the market exposure in the region.

The medical microcontrollers market in the U.S. is growing significantly, owing to aging demographics, the high adoption of AI and digital technologies, the presence of innovation and R&D culture, and the need for wearable devices and home healthcare services. As stated in an article published by the NIH in June 2023, nearly 1 in 3 people utilized a wearable device, such as a smart band or watch, for tracking their fitness and health. In addition, more than 80% of users tend to share information from their respective wearable devices with healthcare professionals to support health monitoring. Besides, researchers demonstrated that 38% of adults with cardiovascular disease utilize such devices regularly, while adults aged from 18 to 49 years also wear these devices, thereby making it suitable for driving the market growth and expansion in the overall country.

The innovation center, rebound and investment in health technology, the integration of digital health, and robust export facilities are certain factors for driving the medical microcontrollers market in Canada. Based on government estimates published by the Government of Canada in July 2025, the medical devices industry in the country, excluding in-vitro diagnostics, accounted for an approximate valuation of USD 10 billion as of 2024, which is almost 2.5% of the global economy. Besides, in terms of trade dynamics, there was an increase in medical device exports from USD 3 billion (CAN4.3 billion) to USD 3.9 billion (CAN5.5 billion), along with a surge in imports from USD 6.8 billion (CAN9.4 billion) to USD 9.8 billion (CAN14 billion). Moreover, the U.S. is considered the country’s largest trading partner for these devices, accounting for 42% of domestic device imports and 73% of exports, thus enhancing the market growth.

Key Business Segments of Canada Medical Devices Industry, 2024

|

Segments |

Share % |

|

Diagnostic Imaging |

19.5 |

|

Consumables |

14.8 |

|

Patients Aids |

15.2 |

|

Orthopaedic and Prosthetic |

11.6 |

|

Dental Products |

8.3 |

|

Others, including Hospital Furniture, Endoscopy Apparatus, Blood Pressure Monitors, Dialysis Apparatus, Anesthesia Apparatus, Ophthalmic Instruments, and Wheelchairs |

30.6 |

Source: Government of Canada

APAC Market Insights

The Asia Pacific in the medical microcontrollers market is expected to emerge as the fastest-growing region, with a share of 19.5% during the forecast period. The market’s development in the region is highly propelled by a rise in wearable technology, particularly in Japan, an increase in healthcare digitalization, and an increase in automotive demand, especially in China. According to a report published by the Asia House Organization in 2023, the region accounts for a fast-growing population of almost 4.7 billion people, witnessing an upsurge in the burden of healthcare demands. Besides, the pandemic resulted in over 1 million people losing their lives in the overall region, which is equivalent to 17.5% of the global population. Therefore, this particular aspect has readily focused the government to ensure the requirement for resilience in the regional healthcare industry, thus positively fueling the market’s development.

The aspects of the elderly population, robust government semiconductor support, the demand for innovative devices, technological innovation, and the surging need for healthcare automation are a few trends that are responsible for bolstering the medical microcontrollers market in Japan. As stated in a report published by the ITA in September 2022, the telemedicine industry in the country was worth USD 243 million as of 2020, which later on increased to USD 404.5 million by the end of 2025. Simultaneously, the country’s healthcare IT sector, service systems, and wearable healthcare equipment significantly reached USD 16 billion as of 2025. Moreover, the domestic healthtech segment also grew by USD 2 billion within the same timeline, particularly in areas, including baby-tech and sleep-tech, suitable for improving sleep support services, such as bed sensors and sleep diagnostic testing, thus denoting an optimistic outlook for the market exposure.

The medical microcontrollers market in China is gaining increased traction, owing to the massive automotive electronics demand, an increase in vehicle production and sales, the semiconductor manufacturing ecosystem, and the increased need for healthcare monitoring systems. As per an article published by Sustainable Futures in June 2026, the automotive industry is continuously booming by producing and selling more than 10 million units as of 2025. Additionally, this corresponds to a 10.8% and 12.9% surge in both sales and manufacturing, respectively. In this regard, electric vehicles tend to utilize microcontrollers to monitor the cell health, which is equivalent to medical devices tracking biological signals, to ensure suitable management of battery systems, thereby denoting a huge growth opportunity for the market in the overall country.

Europe Market Insights

The Europe medical microcontrollers market is projected to witness a considerable share of 30.3% by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by strict regulatory frameworks, innovation in medical technology, an increase in healthcare spending, and the adoption of IoT and AI capabilities into medical devices. According to an article published by NLM in March 2026, there are variations in healthcare expenditure across the overall region as of 2023, with medical payers’ pricing amounting to USD 6,724.2 per person. In addition, Switzerland is considered the highest spender in the region, which is followed by USD 6,446.8 in Norway and USD 6,147.3 in Germany. Besides, the expenditure level in Finland, Denmark, Luxembourg, France, Belgium, Ireland, the Netherlands, Sweden, and Austria was above the regional average of USD 3,720.5, thus enhancing the market’s expansion.

Europe Healthcare Spending Analysis, 2023

|

Countries |

USD PPP Million |

USD PPP Per Capita |

GDP% |

|

Austria |

48,331 |

5,293 |

11.2 |

|

Belgium |

58,139 |

4,936 |

10.8 |

|

Bulgaria |

14,513 |

2,252 |

7.9 |

|

Croatia |

8,464 |

2,195 |

7.1 |

|

Cyprus |

2,891P |

3,019P |

8.1 |

|

Czechia |

34,322 |

3,159 |

8.4 |

|

Denmark |

26,805 |

4,507 |

9.5 |

|

Estonia |

3,174 |

2,317 |

7.5 |

|

Finland |

24,095 |

4,315 |

10.5 |

|

France |

321,942 |

4,709 |

11.5 |

Source: NLM

The medical microcontrollers market in Germany is gaining increased exposure, owing to the presence of a robust manufacturing base, standard research institutions, generous medical spending, leadership in healthcare digitalization, and energy-efficient medical devices. As per an article published by NCBI in April 2025, the European Health Data Space (EHDS) effectively covered 449 million regional citizens, while the country’s upcoming Health Data Lab provided accessibility to data from 75 million insured individuals, which accounts for 90% of the national population. Additionally, this particular initiative offered unprecedented opportunities for advancing digital health innovation and reach with an international impact. Besides, accessibility to 7.9 million data sets tends to represent 2 million patients, and enables the domestic secondary utilization of emergency medicine records, thus uplifting the medical microcontrollers market growth.

An increase in the chronic disease burden, technological investment, digital transformation, and regulatory modernization are certain factors that are responsible for bolstering the medical microcontrollers market in the UK. As stated in an article published by the Health Foundation in July 2023, 9.1 million people residing in England are expected to be impacted by severe illness by the end of 2040. This demonstrates an increase by 37%, which is 9 times the rate at which the working population, aged between 20 and 69 years, is predicted to grow by 4% by the same year. Besides, 80% or 2 million people of the expected increase in critical illness are poised to impact people aged more than 70 years, thereby making it suitable for driving the market's exposure in the overall nation.

Key Medical Microcontrollers Market Players:

- NXP Semiconductors (Netherlands)

- Renesas Electronics (Japan)

- Microchip Technology (U.S.)

- Infineon Technologies (Germany)

- STMicroelectronics (Switzerland)

- Texas Instruments (U.S.)

- Silicon Laboratories (U.S.)

- Analog Devices (U.S.)

- Ambiq Micro (U.S.)

- Hangzhou SDIC Microelectronics (China)

- Intricon (U.S.)

- Minnetronix Medical (U.S.)

- Neways Electronics (Netherlands)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- NXP Semiconductors is a global semiconductor leader that designs purpose-built, rigorously tested technologies enabling devices to sense, think, connect, and act intelligently, serving automotive, industrial, and IoT applications.

- Renesas Electronics is a notable embedded semiconductor solution provider driven by the purpose of making lives easier, delivering scalable solutions for automotive, industrial, infrastructure, and IoT industries with unmatched quality and system-level know-how.

- Microchip Technology is a broadline semiconductor supplier focused on embedded control applications, offering comprehensive solutions including microcontrollers, FPGAs, analog, power, and connectivity products for industrial, automotive, consumer, and aerospace markets.

- Infineon Technologies is considered a global semiconductor manufacturer known for its expertise in power systems, security, and IoT, delivering solutions for automotive, industrial, and medical applications with a focus on efficiency, safety, and connectivity.

- STMicroelectronics is an integrated device manufacturer offering one of the industry's broadest product portfolios, including general-purpose MCUs, wireless solutions, secure MCUs, and MEMS sensors for automotive, industrial, and consumer applications.

Here is a list of key players operating in the global medical microcontrollers market:

The global medical microcontrollers market is characterized by a consolidated competitive landscape dominated by a handful of established semiconductor manufacturers with broad geographic footprints. Key players compete on product quality, R&D investments, and technological innovation, with differentiation centered on energy efficiency, wireless integration, security features, and miniaturization. The medical microcontrollers market features a mix of global leaders offering comprehensive microcontroller portfolios and niche players specializing in ultra-low-power or application-specific solutions for medical devices. Besides, in October 2025, Intricon and Minnetronix Medical partnered and jointly formed Forj Medical, and catered to providing end-to-end capabilities for advanced manufacturing, precision molding, microelectronics, and system design through commercial sale, thereby positively contributing to the medical microcontrollers industry.

Corporate Landscape of the Medical Microcontrollers Market:

Recent Developments

- In March 2026, Neways Electronics successfully acquired Philips Micro Devices, which added industry-based consumers under long-lasting partnerships to the existing growing and robust customer portfolio.

- In March 2023, Silicon Labs introduced two latest integrated circuit families that are designed for the small-scale factor IoT devices, including the xG27 family of Bluetooth systems on chips (SoCs) and the BB50 microcontroller unit.

- In April 2022, Microchip Technology Inc. unveiled 5 newest 8-bit PIC® and AVR® microcontroller products and more than 60 medical devices that provide embedded designers with suitable solutions for the majority of their challenges.

- Report ID: 8642

- Published Date: Jun 29, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Medical Microcontrollers Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.