Medical Device Coatings Market Outlook:

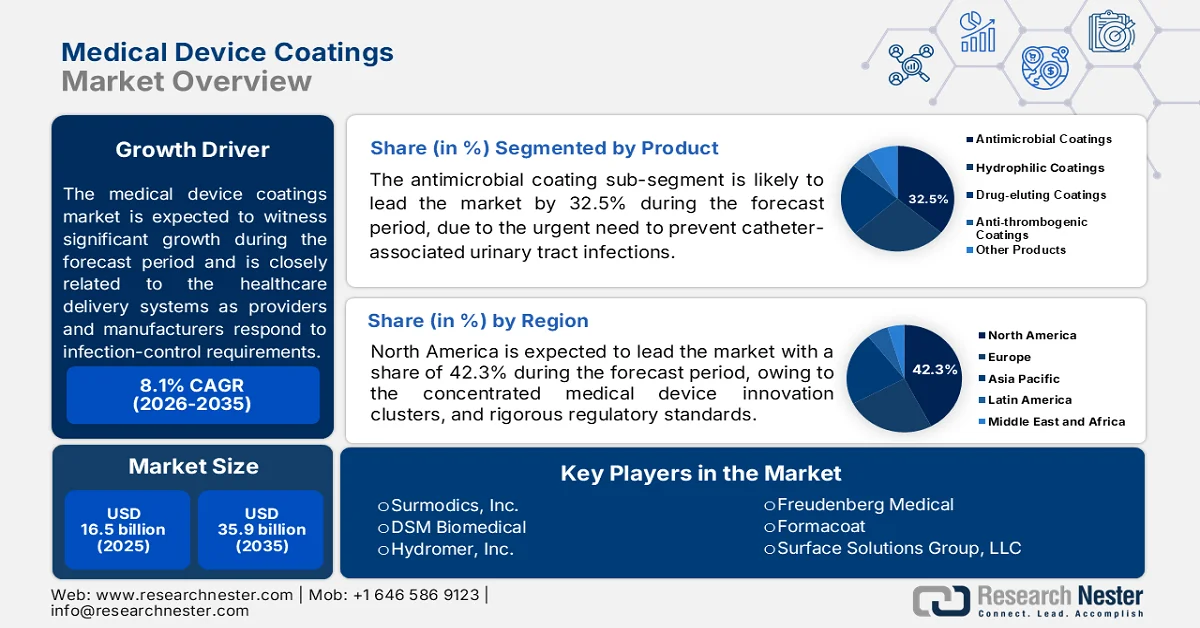

Medical Device Coatings Market size was valued at USD 16.5 billion in 2025 and is projected to exceed USD 35.9 billion by the end of 2035, expanding at over 8.1% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of medical device coatings is estimated at USD 17.8 billion.

Medical device coatings are gaining importance across healthcare delivery systems as providers and manufacturers respond to infection-control requirements, longer device utilization periods, and increasing procedural volumes. The U.S. Centers for Disease Control and Prevention (CDC) January 2026 data estimates that on any given day, approximately 1 in 31 hospitalized patients has at least one healthcare-associated infection (HAI), sustaining demand for technologies that help reduce microbial contamination and improve device performance in clinical settings. At the same time, the CDC reports that millions of patients are affected by HAIs annually, creating ongoing pressure on hospitals to adopt devices designed to support infection-prevention protocols.

Long-term market expansion is also supported by demographic and healthcare utilization trends. According to the NLM July 2023 study, the global population aged 60 years and older will increase from 1 billion in 2020 to 1.4 billion by 2030, significantly expanding the patient population requiring chronic disease management, surgical interventions, and implantable medical devices. Rising procedure volumes, increasing emphasis on patient outcomes, and continued regulatory focus on safety and effectiveness are encouraging manufacturers to expand coating integration across both reusable and single-use devices. The combination of aging populations, higher healthcare spending, and infection-prevention priorities is expected to maintain steady demand for coating-enabled medical devices across developed and emerging healthcare markets.

Key Medical Device Coatings Market Insights Summary:

Regional Highlights:

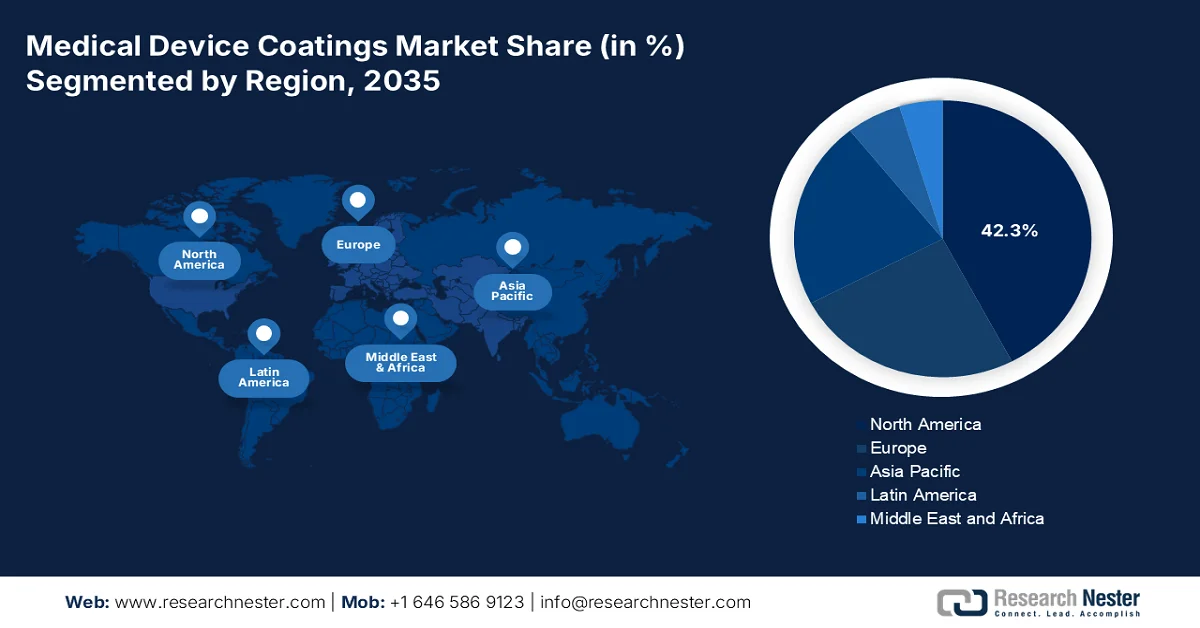

- North America is anticipated to capture 42.3% of the medical device coatings market revenue by 2035, reinforced by a mature healthcare ecosystem, concentrated medical device innovation clusters, and rigorous regulatory standards mandating high-performance surface engineering

- Asia Pacific is expected to witness the fastest expansion in the forecast period 2026-2035, fueled by rapid healthcare infrastructure modernization, expanding middle-class populations, and rising procedural volumes across cardiovascular and orthopedic specialties

Segment Insights:

- The antimicrobial coating segment is projected to account for 32.5% of the medical device coatings market by 2035, supported by the growing need to prevent catheter-associated urinary tract infections (CAUTIs) and surgical site infections

- Synthetic polymers are expected to maintain a dominant position in the material segment through 2035, benefiting from the increasing adoption of bacteria-resistant platforms such as PEG, POZ, and zwitterionic polymers for infection-prone medical devices

Key Growth Trends:

- Expansion of cardiovascular disease treatment programs

- Increasing prevalence of diabetes and long-term catheter utilization

Major Challenges:

- Stringent regulatory approvals

- High R&D & validation costs

Key Players: Surmodics, Inc. (U.S.),DSM Biomedical (Netherlands),Hydromer, Inc. (U.S.),Freudenberg Medical (Germany),Formacoat (U.S.),Surface Solutions Group, LLC (U.S.),PPG Industries, Inc. (U.S.).

Global Medical Device Coatings Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 16.5 billion

- 2026 Market Size: USD 17.8 billion

- Projected Market Size: USD 35.9 billion by 2035

- Growth Forecasts: 8.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: China, India, South Korea, Singapore, Australia

Last updated on : 24 June, 2026

Medical Device Coatings Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of cardiovascular disease treatment programs: Cardiovascular disease remains the leading cause of mortality globally, increasing demand for coated guidewires, angioplasty balloons, stents, catheters, and electrophysiology devices. The WHO 2026 data estimates that 17.9 million people die annually from cardiovascular diseases. Governments continue allocating substantial resources toward cardiovascular screening, intervention, and treatment programs. Hydrophilic and anti-thrombotic coatings improve device maneuverability and reduce complications during vascular procedures, making them increasingly important in modern interventional cardiology. As healthcare systems seek to improve patient outcomes while reducing procedural risks, demand for advanced coating technologies is expected to remain strong across developed and emerging healthcare markets.

- Increasing prevalence of diabetes and long-term catheter utilization: The global rise in diabetes is increasing demand for coated medical devices used in vascular access, insulin delivery, wound care, and chronic disease management. According to the World Health Organization November 2024 data, approximately 830 million people worldwide were living with diabetes in 2022. Governments are expanding diabetes screening and treatment programs, resulting in greater use of infusion systems, diagnostic devices, and long-term catheter-based therapies. Medical device coatings help improve device durability, reduce friction, and minimize infection risks associated with repeated or prolonged use. Suppliers are increasingly developing biocompatible coating platforms optimized for chronic disease applications. As diabetes prevalence continues rising, demand for coated devices supporting long-term patient management is expected to strengthen.

Challenges

- Stringent regulatory approvals: Navigating complex FDA 510(k), PMA, and EU-MDR requirements demands substantial time and financial investment. Biocompatibility testing per ISO 10993, clinical evidence generation, and post-market surveillance create high barriers for new entrants. Small manufacturers often lack regulatory expertise, delaying product launches. Companies like Surmodics have dedicated regulatory teams to streamline submissions.

- High R&D & validation costs: Developing novel coating formulations requires extensive investment in polymer chemistry, stability testing, and accelerated aging studies. Validation against mechanical wear, leaching, and sterilization compatibility adds further expense. DSM Biomedical invests heavily in proprietary biomaterials research to maintain competitive differentiation in hydrophilic and drug-eluting platforms.

Medical Device Coatings Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.1% |

|

Base Year Market Size (2025) |

USD 16.5 billion |

|

Forecast Year Market Size (2035) |

USD 35.9 billion |

|

Regional Scope |

|

Medical Device Coatings Market Segmentation:

Product Segment Analysis

Under the product segment, the antimicrobial coating is leading in the medical device coating market and is poised to hold the share value of 32.5% by the end of 2035. The segment is driven due to the urgent need to prevent catheter-associated urinary tract infections (CAUTIs) and surgical site infections. Innovative formulations, such as the triclosan-based 23EV and 28SC coatings developed by a Kaohsiung-based steel plate manufacturer, demonstrate the technology transfer potential from industrial to medical applications—though medical grades increasingly favor silver-ion and iodine-based actives over triclosan due to regulatory shifts, as per NLM December 2024 study. These formulations, compliant with EU RoHS and REACH directives and validated by SGS, TÜV SÜD PSB, and the Food Industry Research and Development Institute, highlight the rigorous third-party efficacy testing required for market acceptance.

Material Segment Analysis

Synthetic polymers dominate the medical device coatings material segment, with polyethylene glycol (PEG), poly(oxazoline) (POZ), and zwitterionic polymers emerging as the most effective bacteria-resistant platforms. Among these, zwitterionic polymers demonstrate exceptional performance, achieving up to 99% reduction in bacterial adhesion over uncoated controls, making them highly attractive for infection-prone devices like urinary catheters, central venous lines, and orthopedic implants, as per NLM June 2025 study. PEG remains widely adopted due to its established biocompatibility and antifouling properties, while POZ offers superior thermal and chemical stability for long-term implantable applications. Manufacturers are actively investing in cross-linked and grafted polymer architectures to enhance coating robustness.

Application Segment Analysis

Dip coating remains the most widely adopted application method in the medical device coatings market, prized for its operational simplicity, cost-efficiency, and exceptional uniformity across complex device geometries. The process involves immersing substrates—such as guidewires, catheters, and stent struts—into a coating solution and withdrawing them at a controlled speed, with film thickness governed by viscosity, withdrawal rate, and evaporation dynamics. Its scalability from laboratory-scale prototyping to high-volume production lines makes it indispensable for both OEMs and contract coating service providers. Dip coating's adaptability to diverse chemistries—hydrophilic, hydrophobic, antimicrobial, and drug-eluting—and its compatibility with metal, polymer, and ceramic substrates.

Our in-depth analysis of the medical device coatings includes the following segments:

|

Segment |

Subsegments |

|

Product |

|

|

Material |

|

|

Substrate |

|

|

Application |

|

|

End user |

|

|

Functionality |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Medical Device Coatings Market - Regional Analysis

North America Market Insights

North America is dominating the medical devices coating market and is poised to hold the regional revenue share 42.3% by the end of 2035. The region is driven by the mature healthcare ecosystem, concentrated medical device innovation clusters, and rigorous regulatory standards that mandate high-performance surface engineering. The region's device manufacturers—particularly in cardiovascular, orthopedic, and neurovascular specialties—consistently demand advanced hydrophilic, antimicrobial, and drug-eluting coatings to enhance procedural success and patient safety. Regulatory bodies enforce stringent biocompatibility and durability requirements, compelling OEMs to partner with specialized coating suppliers offering validated formulation expertise. Strategic collaborations between coating manufacturers and academic research institutions drive continuous innovation, ensuring North America maintains its leadership position through technological superiority and application excellence.

The strong healthcare spending, high procedural volumes, and continued investment in advanced medical technologies is driving the medical device coatings market in the U.S. According to the AMA April 2025 data, U.S. national health expenditures reached USD 4.9 trillion in 2023, creating substantial demand for coated catheters, implants, guidewires, and surgical devices used across healthcare settings. In addition, the U.S. Food and Drug Administration (FDA) reported receiving more than 3,000 medical device submissions through its Breakthrough Devices Program by 2025, reflecting ongoing innovation in device development where specialized coatings improve safety and performance, as per the NLM August 2024 study. Rising adoption of minimally invasive procedures and infection-prevention initiatives continues to strengthen demand for advanced coating technologies across the U.S. healthcare sector.

The expanding medical device production and export activity is driving the market in Canada. According to OEC 2024 data, exports under HS 9018 (Medical Instruments and Appliances) reached approximately USD 1.4 billion, highlighting Canada’s role in supplying medical and surgical devices to global markets. Many products within this category, including catheters, surgical instruments, and diagnostic devices, incorporate specialized coatings to improve biocompatibility, infection resistance, and device performance. Combined with growing healthcare expenditures and an aging population, Canada’s strong medical device export sector continues to create opportunities for coating manufacturers and contract coating service providers.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the medical device coating market. The region is driven by the rapid healthcare infrastructure modernization, expanding middle-class populations, and rising procedural volumes across cardiovascular and orthopedic specialties. Domestic manufacturing is gaining traction, with local coaters developing hydrophilic and antimicrobial formulations tailored to regional cost sensitivities. Government-led universal health coverage schemes are expanding access to interventional procedures, indirectly boosting coating demand. Multinational coating suppliers are establishing regional application centers and R&D facilities to serve local OEMs, offering technical support and faster turnaround. Sustainability trends, including solvent-free and bio-based polymer coatings, are gradually emerging in mature markets like Japan and Australia.

The rapid expansion of the country’s MedTech industry and government-backed manufacturing programs is fueling the medical device coatings market in India. According to the Invest India May 2025 data, the domestic medical devices sector is valued at approximately USD 14 billion and is projected to reach USD 30 billion by 2030. India’s medical device exports have also surpassed USD 4 billion, reflecting growing production of devices that require antimicrobial, hydrophilic, anti-thrombogenic, and wear-resistant coatings. Government support through the ₹3,420 crore Production-Linked Incentive (PLI) Scheme for Medical Devices and the National Medical Devices Policy 2023 is encouraging local manufacturing, reducing import dependence, and creating opportunities for coating suppliers serving cardiovascular, orthopedic, diagnostic, and surgical device manufacturers.

The expansion of the country’s broader medical technology sector and sustained demand for advanced imported devices is driving the medical device coatings market in China. According to the U.S. International Trade Administration (ITA) September 2025 data, China’s medical device market is projected to reach USD 55.2 billion by 2029, with a forecast CAGR of 8.9% between 2024 and 2029. The ITA also reports that medical device imports accounted for approximately 12% of China’s market in 2023, while U.S. suppliers exported USD 5.4 billion worth of medical devices to China. Strong demand for orthopedic implants, diagnostic equipment, in-vitro diagnostics, and imaging systems is expected to support increasing adoption of antimicrobial, hydrophilic, and wear-resistant coating technologies across the Chinese healthcare sector.

Europe Market Insights

Europe represents a mature and highly regulated market, characterized by stringent EU-MDR compliance, strong emphasis on biocompatibility, and a robust medical device manufacturing base concentrated in Germany, France, Italy, Switzerland, and the UK. The region's coating demand is driven by advanced cardiovascular, orthopedic, and neurovascular procedures, with a pronounced preference for hemocompatible, antimicrobial, and drug-eluting platforms. Sustainability is a key differentiator, with European regulators pushing for solvent-free, bio-based, and fully biodegradable coating chemistries under REACH and Green Deal directives. Manufacturers increasingly adopt parylene and diamond-like carbon coatings for implantable electronics and wear-resistant orthopedic applications. The region hosts world-class coating R&D centers and contract coating service providers, fostering innovation in plasma-enhanced and UV-curable technologies.

The substantial imports of advanced medical technologies is shaping the medical device coatings market in Germany. According to OEC 2024 data under HS 9018 (Medical Instruments and Appliances), Germany imported approximately USD 12.7 billion worth of medical instruments, highlighting the country’s position as one of Europe’s largest healthcare technology markets. The high volume of imported diagnostic equipment, surgical instruments, cardiovascular devices, and minimally invasive medical products creates significant demand for specialized coating solutions that improve device performance, durability, and patient safety. Combined with Germany’s aging population and strong healthcare expenditure, continued imports of sophisticated medical devices are expected to support growth opportunities for medical device coating manufacturers and service providers.

The medical device coatings market in the UK is supported by strong imports of advanced medical technologies. According to OEC 2024 data under HS 9018 (Medical Instruments and Appliances), the United Kingdom imported approximately USD 4.81 billion worth of medical instruments, reflecting substantial demand from hospitals, diagnostic centers, and surgical facilities. A significant share of these imports includes cardiovascular devices, minimally invasive surgical instruments, diagnostic equipment, and patient monitoring products where specialized coatings enhance durability, biocompatibility, lubricity, and infection resistance. The continued reliance on imported medical technologies, coupled with ongoing healthcare investment and growing demand for advanced treatment solutions, is expected to sustain opportunities for medical device coating manufacturers in the UK.

Key Medical Device Coatings Market Players:

- Surmodics, Inc. (U.S.)

- DSM Biomedical (Netherlands)

- Hydromer, Inc. (U.S.)

- Freudenberg Medical (Germany)

- Formacoat (U.S.)

- Surface Solutions Group, LLC (U.S.)

- PPG Industries, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Surmodics, Inc. is a leading pure-play innovator in the medical device coatings market, renowned for its proprietary hydrophilic, hemocompatible, and drug-delivery coating platforms. The company’s flagship Serene® and Velocity® coating families are benchmark standards for vascular guidewires, catheters, and stents, enabling ultra-low friction and sustained thrombus resistance.

- DSM Biomedical, a division of Royal DSM, is a global material science powerhouse in the market, leveraging over 30 years of polymer expertise. Its Bioskin® and Bionate® polycarbonate-urethane families, along with hydrophilic Tecophilic® coatings, are widely adopted for implantable and temporary devices requiring biostability and lubricity.

- Hydromer, Inc. is a specialized U.S. manufacturer firmly established in the market, focusing almost exclusively on hydrophilic polymer coatings for temporary interventional devices. Its patented Hydromer® and Aquavene® coating systems are applied to guidewires, balloon catheters, and introducer sheaths, delivering exceptional wet lubricity and particulate resistance—critical for reducing vessel trauma during complex angioplasty procedures.

- Freudenberg Medical, part of the global Freudenberg Group, is a vertically integrated contract manufacturing giant with a strong foothold in the market. Through its coating division (including the acquisition of Specialty Coating Systems assets), it offers hydrophilic, silicone, parylene, and antimicrobial coatings for minimally invasive tools, catheters, and implantable leads.

- Formacoat is a Houston-based, ISO 13485-certified pure-play coater that has carved a distinct niche in the medical device coatings market by offering highly customized hydrophilic, hydrophobic, and drug-eluting coatings for vascular, urological, and gastrointestinal devices.

Here is a list of key players operating in the global market:

The medical device coatings market is moderately fragmented, with U.S., Europe and Japan firms. Competition centers on biocompatibility, durability, and infection prevention. Key players are pursuing strategic partnerships with OEMs for co-developed hydrophilic and drug-eluting coatings, alongside capacity expansions in Asia-Pacific to reduce supply chain risks. Acquisitions are rampant e.g., larger chemical groups buying niche coating specialists to build integrated portfolios. Sustainability is emerging as a differentiator, with firms investing in solvent-free, UV-curable and biodegradable polymer platforms. Simultaneously, AI-driven high-throughput screening accelerates formulation timelines, while stringent FDA/MDR regulations force continuous quality upgrades, creating barriers for new entrants.

Corporate Landscape of the Market:

Recent Developments

- In February 2026, Freudenberg Medical announced the launch of LUBRITEQ™, which is a new high-performance hydrophilic coating solution, with a comprehensive suite of associated development and manufacturing services.

- In January 2026, Formacoat announced the launch of HydroMark™, which is its proprietary platform of hydrophilic coatings, marking a major milestone evolution from contract coating application to full-service coating service innovator.

- In January 2026, Surface Solutions Group, LLC (SSG) announced its arrival in Costa Rica with the establishment of a new operation dedicated to advanced and high‑precision manufacturing processes for the international medical industry.

- Report ID: 8627

- Published Date: Jun 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.