Liver Cancer Therapeutics Market Outlook:

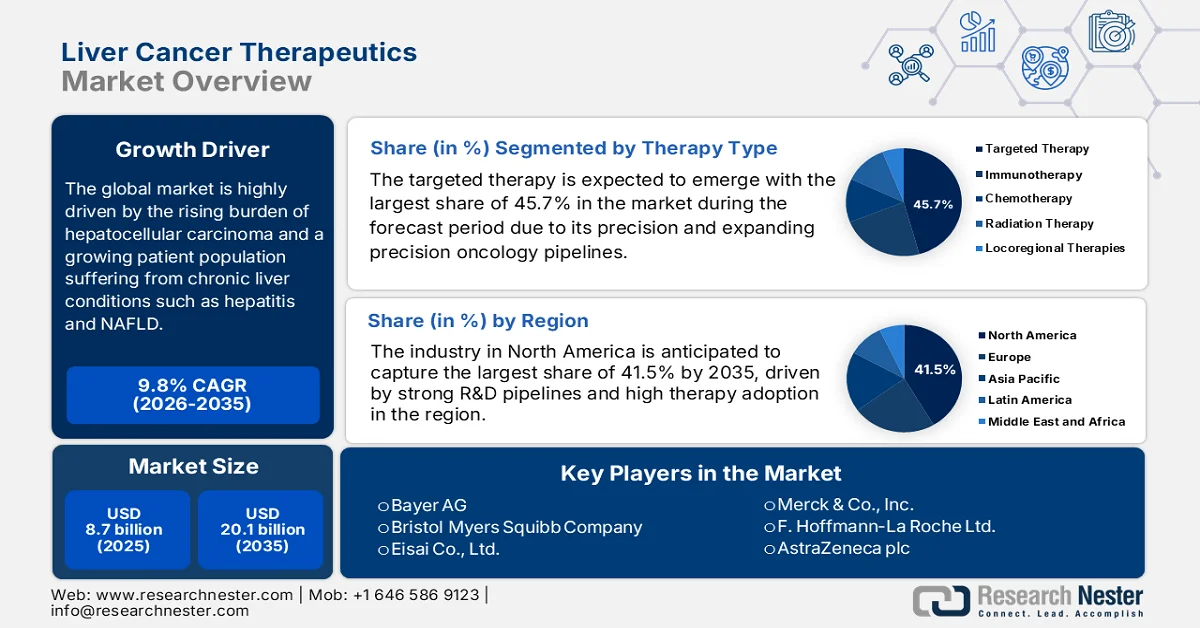

Liver Cancer Therapeutics Market size was valued at USD 8.7 billion in 2025 and is projected to reach USD 20.1 billion by the end of 2035, rising at a CAGR of 9.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of liver cancer therapeutics is estimated at USD 9.5 billion.

The global liver cancer therapeutics market is positively influenced by the increasing incidence of hepatocellular carcinoma (HCC) and a growing patient population suffering from chronic liver conditions such as hepatitis and non-alcoholic fatty liver disease. According to the official statistics published by the Gastrojournal Organization in April 2023, Asia Pacific accounted for over half of the global hepatocellular carcinoma burden in a year, with about 530,000 cases, largely driven by hepatitis B virus and hepatitis C virus. Besides, China alone had 290,000 new cases and 188,000 deaths, whereas Japan reported 34,000 HCC deaths, with rising non-alcoholic steatohepatitis (NASH) and alcohol-related liver disease cases, and Australia’s HCC prevalence grew from 400 to 2,300 in a decade. North America witnessed a total of 41,260 new HCC cases, 30,520 deaths in 2022, whereas Latin America had 18,000 cases and 20,000 deaths, and Europe reported 85,000 to 90,000 cases, denoting an insatiable demand for efficacious therapeutics.

Furthermore, the payers' pricing is yet another major trend that is impacting the growth of the market globally. This, in turn, drives strong competition among drugmakers to demonstrate cost-effectiveness and value, thereby impacting innovation and market growth. As per an article published by the National Institute of Health (NIH) in November 2025, advanced hepatocellular carcinoma treatments, including immune checkpoint inhibitors (ICI) and targeted therapies, have imposed a severe financial burden in low- and middle-income countries, in which only about 1.6% of eligible patients receive ICIs. The article also mentioned that out-of-pocket expenditures in LMICs averaged 35.25% of total healthcare spending, reaching 79.3% in Afghanistan, 64% in Cambodia, and 63% in Egypt. In this context, cost-reduction strategies such as dose rounding, vial sharing, extended dosing intervals, and shorter treatment courses show promising benefits, encouraging players to adopt innovative pricing models and optimize treatment protocols to encourage adoption.

Hepatocellular Carcinoma Immune Checkpoint Inhibitors: Wholesale Pricing Trends and Treatment Cost Analysis (2022)

|

Drug Name |

Dose |

Place of Use in HCC |

Available Strength (mg) |

Average Wholesale Price (USD) |

Average Direct Cost per Cycle (USD) |

|

Atezolizumab |

1200 mg |

1st line |

840, 1200 |

8,272.86 (840 mg), 11,818.37 (1200 mg) |

11,818.37 |

|

Durvalumab |

1500 mg |

1st line |

120, 500 |

1,103.74 (120 mg), 4,598.90 (500 mg) |

13,796.70 |

|

Tremelimumab |

300 mg |

1st line |

300 |

40,000 |

40,000 |

|

Nivolumab |

1 mg/kg |

2nd line |

40, 100, 240, 480 |

1,410.65 (40 mg), 3,526.61 (100 mg), 4,231.9 (240 mg), 8,463.88 (480 mg) |

2,821.3 (40 mg), 4,231.9 (240 mg), 8,463.88 (480 mg) |

|

Ipilimumab |

3 mg/kg |

2nd line |

50, 200 |

9,648.43 (50 mg), 38,593.61 (200 mg) |

38,593.61 |

|

Pembrolizumab |

200 mg |

2nd line or 3rd line |

100, 400 |

6,410.11 (100 mg), 25,640.44 (400 mg) |

12,820.22 (100 mg), 25,640.44 (400 mg) |

Source: NIH

Key Liver Cancer Therapeutics Market Insights Summary:

Regional Highlights:

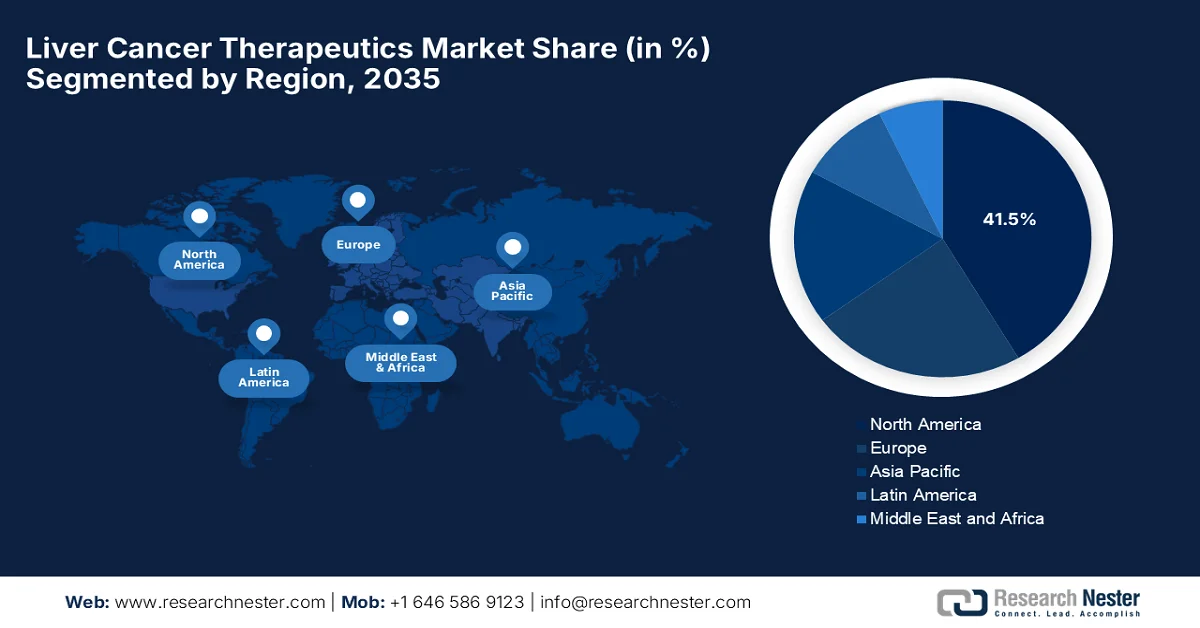

- North America is projected to account for 41.5% share by 2035 in the liver cancer therapeutics market, supported by advanced oncology infrastructure, strong R&D pipelines, and high therapy adoption

- Asia Pacific is anticipated to witness the fastest growth over 2026–2035, propelled by rising healthcare spending and improved diagnostic screening

Segment Insights:

- In the liver cancer therapeutics market, the targeted therapy segment is expected to capture 45.7% share by 2035, driven by precision and expanding oncology pipelines alongside improved tolerability and survival benefits

- The small molecule drugs segment is projected to secure a considerable revenue share by 2035, owing to oral bioavailability, ease of manufacturing, and cost efficiency

Key Growth Trends:

- Shift toward advanced therapies

- Pharmaceutical industry investments

Major Challenges:

- Inequitable global access to therapies

- Stringent regulatory hurdles

Key Players: Bayer AG (Germany), Bristol Myers Squibb Company (U.S.), Eisai Co., Ltd. (Japan), Merck & Co., Inc. (U.S.), F. Hoffmann La Roche Ltd. (Switzerland), AstraZeneca plc (UK), Novartis AG (Switzerland), Pfizer Inc. (U.S.), Eli Lilly and Company (U.S.), Johnson & Johnson (U.S.), Sanofi S.A. (France), Eureka Therapeutics (U.S.), Gilead Sciences, Inc. (U.S.), AbbVie Inc. (U.S.), Mirum Pharmaceuticals (U.S.), AstraZeneca Pharma India (India), Takeda Pharmaceutical Company Limited (Japan), Ipsen S.A. (France), Exelixis, Inc. (U.S.), Bluejay Therapeutics (U.S.), Amgen Inc. (U.S.), Incyte Corporation (U.S.), BeiGene, Ltd. (China).

Global Liver Cancer Therapeutics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 8.7 billion

- 2026 Market Size: USD 9.5 billion

- Projected Market Size: USD 20.1 billion by 2035

- Growth Forecasts: 9.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (41.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Singapore, Australia

Last updated on : 26 March, 2026

Liver Cancer Therapeutics Market - Growth Drivers and Challenges

Growth Drivers

- Shift toward advanced therapies: The liver cancer treatment category is making a transition from chemotherapy to checkpoint inhibitors and targeted therapies, driving demand in the liver cancer therapeutics market. As per the article published by NIH in April 2025, atezolizumab plus bevacizumab has become a highly preferred first-line therapy for unresectable hepatocellular carcinoma, which reflects a structural shift from earlier tyrosine kinase inhibitors to immunotherapy-based treatment procedures. In a real-world cohort of 374 patients from the U.S. oncology network, median overall survival was 13.2 months, increasing to 16.5 months in trial-like patients. Besides, the median progression-free survival reached 6.4 months overall and 9.4 months in the subgroup, demonstrating meaningful clinical benefit, hence positively impacting overall market growth.

- Pharmaceutical industry investments: Major pharma companies are making heavy investments in terms of oncology pipelines. High revenues from blockbuster drugs are sustaining both innovation and competition in the market. In April 2023, Roche announced that the Tecentriq plus Avastin Phase III IMbrave050 study showed reduced recurrence risk in adjuvant hepatocellular carcinoma by 28% when compared to surveillance. It outlined that with up to 80% of patients facing recurrence post-surgery, this marks the first positive trial in the adjuvant HCC setting. Therefore, from a strategic perspective, such instances efficiently enhance the market’s exposure and attract more players to establish their footprint in the country.

- Heightened awareness & screening: The consistent efforts with awareness programs and the development of improved diagnostic tools are leading to earlier interventions. The aspect of better screening is eventually changing the therapeutic mix, sustaining high demand for intervention and ongoing clinical management. As per an article published by the Medical Journal of Australia in October 2025, the 2023 HCC surveillance guidelines recommend six‑monthly ultrasound, with or without α‑fetoprotein testing, for people at high risk of hepatocellular carcinoma. Besides, it states that routine surveillance is advised for those with cirrhosis, and for chronic hepatitis B patients without cirrhosis but with a family history or specific ethnic backgrounds. In addition, it is endorsed by the NHMRC, and these guidelines aim to improve early detection and survival outcomes, hence suitable for bolstering market growth.

Challenges

- Inequitable global access to therapies: The stark disparities in access to therapeutics are a major obstacle hindering the expansion of the market. Most of the affected population in low‑ and middle‑income countries face delayed drug availability influenced by the limited healthcare budgets, weaker reimbursement policies, and slower regulatory approvals. In some regions, innovative treatments approved in other major nations may take years to become available. In addition, the aspect of out‑of‑pocket costs is prohibitive for many patients without insurance support, leading to underutilization and widening outcome gaps. Hence, these disparities reduce overall market potential and challenge global manufacturers who are looking to scale uptake across various healthcare systems.

- Stringent regulatory hurdles: Developing liver cancer drugs requires lengthy, expensive clinical trials to demonstrate safety and survival benefits in populations with complex liver dysfunction. In this context, regulatory authorities across different nations maintain rigorous approval standards, which necessitate large trials with challenging endpoints. Therefore, the differences in regulatory requirements across regions add complexity and extend time‑to‑market timelines, making it challenging for small-scale firms to operate in the market. Negotiating different clinical protocols and safety considerations for cirrhotic patients increases R&D costs and delays access to innovative therapies. Further, these bureaucratic hurdles ultimately cause delays to product launches and make it harder for companies to bring new treatments to patients, hindering market expansion.

Liver Cancer Therapeutics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.8% |

|

Base Year Market Size (2025) |

USD 8.7 billion |

|

Forecast Year Market Size (2035) |

USD 20.1 billion |

|

Regional Scope |

|

Liver Cancer Therapeutics Market Segmentation:

Therapy Type Segment Analysis

The targeted therapy subtype is expected to emerge with the largest share of 45.7% in the liver cancer therapeutics market during the forecast period. Their precision and expanding precision oncology pipelines make this sub-segment the revenue leader. On the other hand, clinical adoption has been rising due to better tolerability and survival benefits when compared with traditional chemotherapies. In June 2023, Eureka Therapeutics was allocated a total of USD 10.6 million grant from the California Institute for Regenerative Medicine to support its ARYA‑2 Phase I trial of ET140203 ARTEMIS T‑cell therapy in pediatric liver cancers. The company notes that ET140203 is engineered to target AFP‑positive liver cancer cells, and it offers a breakthrough for rare, hard‑to‑treat malignancies such as hepatoblastoma and HCC, hence denoting a positive outlook for the segment’s dominance.

Top Government-Registered Liver Cancer Therapeutics Clinical Trials (2023-2026) - Phase 2 Studies and Interventions

|

Trial Name |

ID |

Intervention |

Phase |

Year (Updated) |

|

HCC-SIGHT: Platform Trial for Personalized Adaptive Therapies |

NCT07328009 |

Multi-arm: Lenvatinib, Regorafenib, Tislelizumab+TKI, HAIC+TKI, QL1706+TKI, Camrelizumab+TKI, XELOX combos |

Phase 2 |

2026-2029 |

|

HAIC With Lipiodol Embolization in Advanced HCC |

NCT06632717 |

Cisplatin + 5-fluorouracil + Lipiodol embolization |

Phase 2 |

2024 -2027 |

|

Perioperative Sintilimab + Bevacizumab Biosimilar + TACE-HAIC for HCC with PVTT |

NCT06031285 |

Sintilimab + Bevacizumab biosimilar + TACE-HAIC |

Phase 2 |

2023-2026 |

Source: ClinicalTrials.gov

Drug Type Segment Analysis

Under the drug type, the small molecule drugs segment is anticipated to grow with a considerable revenue share in the liver cancer therapeutics market by 2035. The growth of the segment is largely attributable to its oral bioavailability, ease of manufacturing, and cost efficiency, serving as the foundation for many treatment procedures. In January 2025, Tempest Therapeutics received the U.S. Food & Drug Administration (FDA) orphan drug designation for amezalpat (TPST‑1120), which is a selective PPAR⍺ antagonist, for hepatocellular carcinoma. The designation follows promising phase 1b/2 trial results showing improved overall survival and response rates when combined with atezolizumab and bevacizumab. Hence, such instances show that small molecule therapies with oral bioavailability are actively being advanced through regulatory pathways in the liver cancer space, reflecting real investment and focus on these drugs.

Treatment Line Segment Analysis

In the liver cancer therapeutics market, the first-line therapies segment is predicted to attain a significant revenue share by the conclusion of the forecast period. The segment benefits from earlier interventions and broader patient eligibility at diagnosis. Besides, the first-line therapies segment is expanding due to the shift towards personalized medicine and combination treatments that enhance patient outcomes. Moreover, growing awareness among healthcare providers about the benefits of initiating treatment at diagnosis is increasing the uptake of early treatment procedures. In addition, improvements in diagnostic tools are enabling more accurate patient stratification for first-line treatments. Furthermore, regulatory approvals of new drugs with broader indications are also contributing to the segment’s strong revenue growth and exposure in the industry.

Our in-depth analysis of the liver cancer therapeutics market includes the following segments:

|

Segment |

Subsegments |

|

Therapy Type |

|

|

Drug Type |

|

|

Treatment Line |

|

|

Cancer Type |

|

|

Drug Class |

|

|

Route of Administration |

|

|

Distribution Channel |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Liver Cancer Therapeutics Market - Regional Analysis

North America Market Insights

North America liver cancer therapeutics market is forecasted to hold the largest share, contributing 41.5% of total revenue by the end of 2035. The advanced oncology infrastructure, strong R&D pipelines, and high therapy adoption are the key factors driving the region’s leadership in this sector. As of July 2025, NIH data show that funding for liver cancer research by the National Cancer Institute (NCI) has steadily increased over recent years, rising from USD 72.7 million six years ago to USD 114.2 million in 2023. These funds support a variety of research areas, including basic science, clinical trials, and disease-specific studies. Besides, in 2023, the total NCI budget reached USD 7.2 billion, including USD 216 million from the Cures Act, representing a 5.7% increase from the prior year. This consistent investment reflects the prioritization of liver cancer research within the NCI portfolio, with a main goal to advance understanding, treatment, and patient outcomes, hence denoting an optimistic market outlook.

The regulatory support for fast-track approvals and the rising disease burden are responsible for uplifting the U.S. market. Technological breakthroughs in biomarker research and personalized medicine, with the presence of major pharmaceutical players, are reorganizing the growth dynamics of the sector. According to the article published by NIH in January 2024, in a span of two decades, the U.S. recorded 467,346 cases of hepatocellular carcinoma, which is 26% in women. Incidence in men increased from 7.32 to 9.82 per 100,000, and in women from 2.38 to 3.09 per 100,000, whereas older adults showed higher rates, i.e., men: 25.28, 40.38, and women: 8.94, 12.29. Therefore, these trends reveal marked age and sex specific differences, underscoring the urgent need for targeted early detection and intervention strategies to address the long-term complications.

The universal healthcare mandates that facilitate the uptake of approved treatments are driving the liver cancer therapeutics market in Canada. The improvements in provincial reimbursement are efficiently enabling market access for patients in the country. In January 2026, the government of Ontario launched the FAST program to accelerate access to breakthrough cancer drugs. Besides, it stated that since October 2025, six therapies, including treatments for lung, prostate, leukemia, lymphoma, colorectal, and liver cancers, have been fast-tracked. The initiative reduces patient wait times by nearly a year when compared to traditional approval processes. In addition, Health Canada, in August 2025, approved the dual immunotherapy OPDIVO plus YERVOY for first‑line treatment of unresectable or advanced hepatocellular carcinoma and MSI‑H/dMMR colorectal cancer, supported by pivotal Phase 3 trials, hence denoting a positive market outlook.

APAC Market Insights

Asia Pacific liver cancer therapeutics market is likely to exhibit the fastest growth rate from 2026 to 2035. The region’s growth in this sector is largely driven by increased healthcare spending and improved diagnostic screening in countries such as China, Japan, and South Korea. Rising disease burden, coupled with robust clinical trials, is also fueling market growth. As per the NIH article published in June 2025, HCC results in almost 85% to 90% of primary liver cancers and disproportionately affects the region, which carries 73% of the global burden. Besides, in 2022, more than 80% of the cases in this region were diagnosed at advanced stages. Japan’s model demonstrates success with the presence of initiatives such as the USD 108 million 2024 investment in early detection, treatment subsidies, and public awareness, along with universal HBV vaccination and biomarker surveillance. The economic burden from this illness is projected to rise in China to USD 34.0 billion by 2030.

A massive patient population primarily affected by chronic hepatitis B is driving the market in China. The landscape is supported by aggressive government reforms, which are aimed at accelerating drug approvals and expanding national reimbursement coverage. Based on the government data published in July 2025, the National Healthcare Security Administration, together with the National Health Commission, introduced several measures to support the high-quality development of innovative drugs. These measures accelerate inclusion of new drugs in the national medical insurance catalog, reduce the overall approval-to-reimbursement timelines, and provide preferential policies, negotiation support, and value-based purchasing to boost innovation and sales. Furthermore, optimized renewal rules, confidential pricing, and strategic purchasing have stabilized expectations for new drugs, increased approved Class 1 drugs from 9 to 48 in a span of six years, and improved public drug security and patient outcomes.

In India, the market is witnessing noteworthy growth, which is driven by a rising incidence of non-alcoholic fatty liver disease and a trend toward affordable, innovative liver cancer treatments. The market is also sustained on account of affordable generic versions of global blockbuster drugs and government-led disease control programs. As stated by ClinicalTrials.gov in March 2026, a phase I multicentric study was initiated in 2026 at PGIMER Chandigarh and later included AIIMS New Delhi and TMH Mumbai. It will enroll 18 patients, 12 in the 188Re arm, 6 in the 90Y arm, using a 3+3 dose-escalation design across three tumor absorbed-dose cohorts. In this context, patients will undergo detailed pre-therapy dosimetry, targeted infusion of radiolabeled microspheres, and monitoring for dose-limiting toxicities during a 28-day post-SIRT window. The study is estimated to finish by October 2028, and it mainly aims to develop a cost-effective and accessible selective internal radiation therapy option for patients with inoperable hepatocellular carcinoma, thereby reducing financial barriers and improving treatment outcomes.

Europe Market Insights

In Europe, the liver cancer therapeutics market is effectively fueled by a well-organized regulatory environment and the rapid adoption of combination immunotherapies as the standard of care. Major pharmaceutical players in the region are focused on precision medicine and biomarker-driven treatments to navigate the continent's stringent pricing regulations and improve long-term patient survival. In January 2024, the European Union launched the THRIVE project, which is a USD 13 million initiative to improve outcomes for children and adults with liver cancer. The initiative is coordinated by a researcher at the University of Barcelona, and it unites 13 organizations from eight countries under the region’s Mission on Cancer. Its mission is to identify at-risk populations, develop biomarkers for immunotherapies, create affordable new treatments, and maximize societal impact through accessible data and integration with social sciences.

Germany liver cancer therapeutics market has gained enhanced exposure, which is facilitated by its statutory health insurance system. The country is identified as a major hub for clinical research and early-access programs, thereby allowing patients to benefit from innovative combination therapies within a short time after regulatory approval. LiSyM-Cancer is a multidisciplinary research network in Germany that is funded by the Federal Ministry of Research, Technology, and Space (BMFTR) from July 2024 to June 2027 under the National Decade Against Cancer. The research is highly focused on clinical applications for liver cancer prevention and early detection. The mission is to translate systems medicine insights into strategies that diagnose, prevent, or delay liver cancer at its earliest stages, hence suitable for bolstering the country’s market growth.

The awareness of liver diseases and improvements in early disease detection technologies are responsible for uplifting the market in the UK. In addition, the availability of both branded and affordable generic drugs, combined with ongoing clinical research and collaboration, is fostering a supportive landscape focused on improving accessibility of liver cancer care. The Rare Cancers Bill passed its third reading in the UK House of Commons in July 2025, which marks a major step toward becoming law. The bill is focused on boosting research, innovation, and clinical trial access for rare cancers such as liver cancer, which has only a 13% five-year survival rate. Besides, it aims to appoint a government lead, strengthen drug regulations, and incentivize new treatments. Hence, such instances in the country and policy measures are creating a supportive environment for the development and adoption of effective liver cancer therapies.

Key Liver Cancer Therapeutics Market Players:

- Bayer AG (Germany)

- Bristol‑Myers Squibb Company (U.S.)

- Eisai Co., Ltd. (Japan)

- Merck & Co., Inc. (U.S.)

- F. Hoffmann‑La Roche Ltd. (Switzerland)

- AstraZeneca plc (UK)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Johnson & Johnson (U.S.)

- Sanofi S.A. (France)

- Eureka Therapeutics (U.S.)

- Gilead Sciences, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Mirum Pharmaceuticals (U.S.)

- AstraZeneca Pharma India (India)

- Takeda Pharmaceutical Company Limited (Japan)

- Ipsen S.A. (France)

- Exelixis, Inc. (U.S.)

- Bluejay Therapeutics (U.S.)

- Amgen Inc. (U.S.)

- Incyte Corporation (U.S.)

- BeiGene, Ltd. (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Bayer AG is considered to be a major leader in terms of liver cancer therapeutics, which leverages define systemic therapy for advanced hepatocellular carcinoma. Besides, the company benefits from its global commercial footprint and robust R&D investment to sustain market leadership, with ongoing trials that are exploring targeted and combination regimens.

- Bristol‑Myers Squibb Company is also identified as a dominant force in immunotherapy for liver cancer, along with other combination approaches for advanced HCC. The firm proactively participates in expanding indications for immuno‑oncology agents, advancing combination regimens, and engaging in strategic partnerships and trials.

- Merck & Co., Inc. has bolstered its position through its immunotherapy portfolio, which is extensively used across multiple cancers, including liver cancer. The company makes heavy investments in clinical trial programs and collaborations designed to extend the therapeutic footprint of its immuno‑oncology agents in liver cancer and other tumors.

- F. Hoffmann‑La Roche Ltd is maintaining a strong position in this sector. The company’s competitive edge lies in deep expertise in biologics, extensive clinical evidence, and global commercialization capabilities.

- AstraZeneca plc has gained immense prominence with its immunotherapy, which is providing an alternative frontline option for HCC patients. The company invests heavily in innovative immuno‑oncology combinations and global expansion of its oncology franchises.

Below is the list of some prominent players operating in the global market:

The liver cancer therapeutics market hosts both multinational pharmaceutical leaders and rising biotech innovators. Major companies such as Bayer, Bristol‑Myers Squibb, Merck & Co., Roche, and AstraZeneca lead the sector through broad oncology portfolios, tactical collaborations, and late‑stage clinical programs to address the hepatocellular carcinoma and combination regimens. Firms are also focused on R&D investments and collaboration deals with a main goal to enhance pipelines and expand geographic reach, whereas acquisitions and co‑development agreements strengthen market positions. In January 2026, Mirum Pharmaceuticals acquired Bluejay Therapeutics to add brelovitug, a late-stage monoclonal antibody for chronic hepatitis delta virus, to its rare disease portfolio. The deal was funded through USD 268.5 million in private placement financing, thus denoting a positive outlook for the market’s growth and exposure.

Corporate Landscape of the Liver Cancer Therapeutics Market:

Recent Developments

- In March 2026, AstraZeneca Pharma India received CDSCO approval for durvalumab monotherapy in patients with unresectable hepatocellular carcinoma who have not received prior systemic therapy.

- In January 2026, Eureka Therapeutics received the U.S. FDA RMAT designation for ECT204, which is its ARTEMIS CAR T-cell therapy targeting GPC3 in advanced hepatocellular carcinoma. This recognition was based on promising Phase I/II trial data, and it allows closer FDA collaboration and potential accelerated approval pathways.

- Report ID: 4114

- Published Date: Mar 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.