Lateral Flow Assays Market Outlook:

Lateral Flow Assays Market size was valued at USD 8.9 billion in 2025 and is projected to reach USD 19.7 billion by the end of 2035, rising at a CAGR of 8.3% during the forecast period, i.e., 2026-2035. In 2026, the industry size of lateral flow assays is estimated at USD 9.6 billion.

The global market is mainly driven by the sustained public sector investment in infectious disease surveillance, decentralized diagnostics, and emergency preparedness programs. The government agencies continue to prioritize rapid testing to strengthen the outbreak response and routine screening capacity. According to the NLM study in January 2026, nearly 37 cases in nonpoultry mammals and birds and 31 cases of Avian influenza in poultry occurred in the U.S., Africa, Asia, and Europe. Further, this results in the killing or culling of more than 907,222 poultry. Moreover, the African swine fever has reported in many regions across 68 countries and has affected more than 1,079,278 pigs and 39,161 wild boars, resulting in more than 2,255,137 animal losses. These data indicate the growing frequency and spread of the animal disease and the need for rapid and scalable lateral flow assays for early detection and continuous surveillance across both human and veterinary health systems.

Moreover, the rising incidence of infectious diseases is the major driver for the market growth. According to the CDC, September 2024 data, there are currently 120 infectious diseases nationally requiring continuous reporting and rapid diagnostic confirmation. This regulatory mandate significantly increases the routine testing volumes across hospitals, community screening programs, and public health laboratories. The lateral flow assays play a vital role by enabling fast decentralized detection during early-stage outbreaks. Further, the demand is amplified by their cost-effectiveness, ease of deployment, and suitability for large-scale surveillance initiatives. This sustained surveillance requirement ensures consistent government procurement and long-term adoption of lateral flow assays as a frontline diagnostic tool in national infectious disease control strategies.

Key Lateral Flow Assays (LFA) Market Insights Summary:

Regional Highlights:

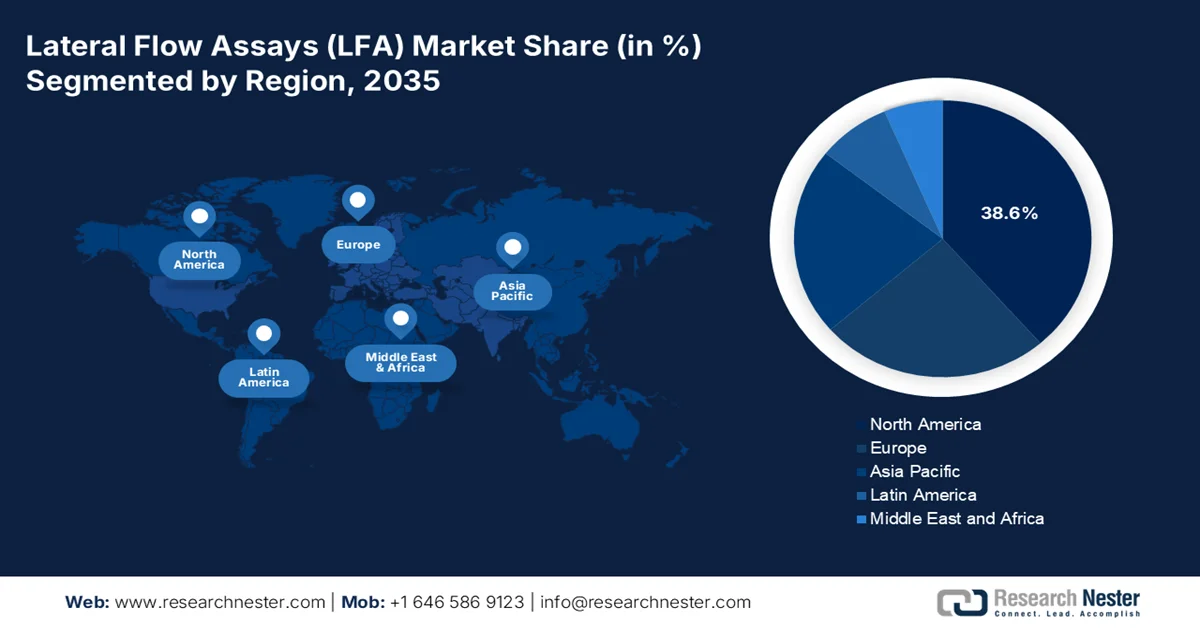

- North America lateral flow assays market is projected to capture a 38.6% revenue share by 2035, underpinned by advanced healthcare infrastructure, strong regulatory backing, and sustained public health preparedness investments.

- Asia Pacific is forecast to expand at a CAGR of 7.7% through 2035, stimulated by rising healthcare expenditure, expanding diagnostic access in rural care, and strengthening domestic manufacturing initiatives.

Segment Insights:

- In the lateral flow assays market, the kits & reagents segment is projected to command a 78.4% share by 2035, fueled by sustained high-volume demand across healthcare, home testing, and public health screening programs.

- Clinical testing is anticipated to witness robust expansion during 2026–2035, accelerated by the global shift toward decentralized healthcare and integration of lateral flow assays into routine diagnostic pathways.

Key Growth Trends:

- Government backed HIV TB and malaria control programs

- Sustained government spending on infectious disease surveillance

Major Challenges:

- High R&D and regulatory costs

- Technological advancements and keeping pace

Key Players: Abbott Laboratories (U.S.), QuidelOrtho (U.S.), Siemens Healthineers (Germany), Roche (Switzerland), Danaher Corporation (Beckman Coulter, etc.) (U.S.), BD (Becton, Dickinson and Company) (U.S.), Thermo Fisher Scientific (U.S.), bioMérieux (France), PerkinElmer (U.S.), Merck KGaA (Germany), Hologic, Inc. (U.S.), bioLytical Laboratories (Canada), OraSure Technologies (U.S.), Sekisui Diagnostics (U.S.), Boditech Med Inc. (South Korea), SD Biosensor (South Korea), Atomo Diagnostics (Australia), Mylab Discovery Solutions (India), BTNX Inc. (Canada), ACON Laboratories (U.S.)

Global Lateral Flow Assays (LFA) Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 8.9 billion

- 2026 Market Size: USD 9.6 billion

- Projected Market Size: USD 19.7 billion by 2035

- Growth Forecasts: 8.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, United Kingdom, China, Japan

- Emerging Countries: India, Brazil, South Korea, Singapore, Australia

Last updated on : 12 February, 2026

Lateral Flow Assays Market - Growth Drivers and Challenges

Growth Drivers

- Sustained government spending on infectious disease surveillance: The national governments continue to allocate a significant budget to the infectious disease surveillance, directly supporting the demand for rapid diagnostic formats such as the lateral flow assays. According to the CDC 2025 budget, the request exceeded USD 9.683 billion with a substantial share directed toward surveillance laboratory capacity and outbreak preparedness. The rapid antigen and antibody tests are explicitly referenced as tools for decentralized screening in community and outpatient settings. Besides, the WHO indicates rapid diagnostics to close detection gaps, mainly in low-resource regions. These policies translate into predictable procurement cycles through public tenders, benefiting the market manufacturers supplying high-volume screening tests.

CDC 2025 President’s Budget

|

Budget Allocation Category |

Funding Amount (USD Million) |

Share of Total (%) |

|

Protecting Americans from Infectious Diseases |

3,134 |

32% |

|

Preventing the Leading Causes of Disease, Disability, and Death |

2,708 |

28% |

|

Protecting Americans from Natural and Bioterrorism Threats |

943 |

10% |

|

Monitoring Health and Ensuring Laboratory Excellence |

804 |

8% |

|

Cross-cutting Services |

764 |

8% |

|

Ensuring Global Disease Protection |

693 |

7% |

|

Keeping Americans Safe from Environmental and Work-related Hazards |

630 |

7% |

|

Total |

9,683 |

100% |

Source: CDC 2025

- Government backed HIV TB and malaria control programs: In the lateral flow assays (LFA) market, the LFA’s remain a core diagnostic tool in the global HIV, tuberculosis, and malaria programs funded by governments and multilateral organizations. According to the UNICEF February 2023 data, nearly 5 to 18 million rapid diagnostic tests for malaria are conducted every year, largely financed via public and donor funding. Moreover, the parasites caused 247 million cases of malaria and 619 thousand deaths in 2021. These programs require WHO prequalified rapid tests, creating sustained institutional demand. Further, the continued scale-up of national elimination programs and donor-backed procurement framework ensures long-term high-volume purchasing of lateral flow assays, reinforcing their role as an essential cost-effective diagnostic solution in low and middle-income countries.

- Regulatory support for rapid diagnostic approvals: The regulatory agencies continues to support the expedited pathways for diagnostics, addressing the public health needs. Further, the U.S. FDA maintains emergency use authorization and streamlined 510(k) pathways enabling the faster market entry for the lateral flow assays during outbreaks. The FDA authorized hundreds of rapid tests, demonstrating regulatory willingness to scale LFA access when public health impact is high. This regulatory posture lowers commercialization risk for manufacturers supplying government buyers. Moreover, the regulatory readiness enhances supplier responsiveness to sudden demand spikes driven by public sector needs.

Challenges

- High R&D and regulatory costs: Developing and obtaining regulatory clearance for a new lateral flow assay is capital and time-intensive. The FDA’s 510(k) or De Novo pathways require extensive clinical validation. For example, the novel multiplex cardiac panel can cost over a million dollars and take years from concept to commercialization. Further startups invest heavily to develop their novel microfluidic immunoassay platform, facing significant pre-revenue R&D expenditure before market entry.

- Technological advancements and keeping pace: The shift from simple qualitative strips to quantitative reader-based and multiplex assays demands continuous innovation. New entrants in the lateral flow assays market must compete with the advanced systems that offer high-throughput automated lateral flow-like testing. Falling behind in the digital integration or sensitivity can render a product obsolete. Investment in R&D for features such as smartphone connectivity is now a necessity, not a differentiator.

Lateral Flow Assays Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.3% |

|

Base Year Market Size (2025) |

USD 8.9 billion |

|

Forecast Year Market Size (2035) |

USD 19.7 billion |

|

Regional Scope |

|

Lateral Flow Assays Market Segmentation:

Product Segment Analysis

The kits & reagents are leading the segment and are poised to hold the share value of 78.4% by 2035 in the market. The segment is driven by the continuous high-volume demand from the healthcare, home testing, and public health screening programs, creating a recurring revenue stream far exceeding that of durable readers. The importance of rapid, accessible testing was highlighted by massive government procurement, with the U.S. government alone investing heavily to distribute tests nationwide. As per the National Institute of Allergy and Infectious Disease 2025 data, allergy and infectious disease research funding accounted for USD 6.581 billion in 2025, mainly assigned for test kits and reagents to sustain the national response and surveillance capabilities. Further, the technological improvements are surging the repeat purchases and broadening the applicability of kits across infectious, chronic, and preventive care testing settings.

Application Segment Analysis

Clinical testing is leading due to rapid diagnostics for infectious diseases, cardiology, pregnancy, and chronic conditions in the market. The growth of the segment is propelled by the global push for decentralized healthcare and the integration of the lateral flow assays into standard clinical pathways for triage and management. The expansion beyond pandemic-related tests to routine screenings ensures sustained growth. A key statistical driver from this period is the scale of clinical trial settings. Moreover, the clinical trials are rising in the cancer field, and the data from the NLM January 2024 study indicates that nearly 7747 clinical trials were involved in the study to define the clinical trial enrollment disparities in common cancers. The data indicate the entrenched role of rapid clinical testing.

Technology Segment Analysis

The technology segment is driven by the sandwich assays, the most widely employed format, mainly for detecting larger analytes such as proteins and pathogens. Their dominance stems from a high specificity, user-friendly design, and well-established manufacturing process. This format is the foundation for most infectious disease and pregnancy tests. The government validation and utilization statistics highlight its prevalence. For example, in evaluating rapid diagnostics tests, organizations such as the FDA and the WHO rely heavily on sandwich assay-based test. Moreover, the WHO has included numerous sandwich-format LFAs, with one report noting that a single manufacturer’s WHO-prequalified malaria RDT accounted for millions of tests procured annually for global health programs.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Product |

|

|

Technology |

|

|

Application |

|

|

Test Type |

|

|

Sample Type |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Lateral Flow Assays Market - Regional Analysis

North America Market Insights

The North America lateral flow assays (LFA) market is dominating and is expected to hold the regional revenue share of 38.6% by 2035. The market is driven by the advanced healthcare infrastructure, high healthcare expenditure, and strong regulatory frameworks from the FDA and Health Canada. A primary trend is the strategic integration of rapid diagnostics into value-based care and decentralized testing models supported by reimbursement pathways from the CMS. Moreover, the government spending focuses on public health preparedness with agencies such as BARDA funding next-gen assays for pandemic response and biological threats. The shift toward managing chronic diseases at the point of care and the expansion of retail clinics and home testing further propel the demand. Besides, the collaborative initiatives between public health bodies and manufacturers ensure a pipeline for advanced tests, sustaining the region's leadership through a combination of procurement stability and continuous product evolution.

The U.S. market continues to expand and is driven by the high clinical burden of infectious and parasitic diseases and the integration of rapid testing into routine care. According to the CDC December 2024 data, physician offices recorded 10.2 million visits with these conditions as the primary diagnostics including 790,000 admissions resulting in hospitalization. This sustained patient volume creates a consistent demand for rapid diagnostic tools at the point of care and in emergency settings. Regulatory authorization of lateral flow-based OTC products further supports the market growth. The FDA authorized Abbott Diagnostics in February 2025, BinaxNOW COVID-19 Antigen Self-Test and BinaxNOW Ag Card, both lateral flow assays designed for visual read and decentralized testing. These approvals enabled large-scale deployment beyond hospitals into homes, pharmacies, and public screening programs. Collectively, these data indicate an active market growth in the U.S.

FDA Authorized Molecular Diagnostic Tests

|

Manufacturer |

Device Name |

Attributes |

Data of Authorization |

|

Abbott Diagnostics Scarborough, Inc. |

ID NOW COVID-19 2.0 |

RT, Isothermal amplification, Single Target |

08/10/2023 |

|

Abbott Molecular Inc. |

Alinity m Resp-4-Plex |

Real-time RT-PCR, Multi-analyte, Multiple Targets |

|

|

BD Integrated Diagnostic Solutions/Becton, Dickinson & Company |

BD Respiratory Viral Panel for BD MAX System 445215; BD Respiratory Viral Panel-SCV2 for BD MAX System 445361 |

Real-time RT-PCR, Multi-analyte, Multiple Targets |

|

|

BioFire Defense, LLC |

Biofire Covid-19 Test 2 |

RT, Nested multiplex PCR, Multiple Targets |

07/25/2022 |

|

Cepheid |

Xpert Xpress CoV-2/Flu/RSV plus |

Real-time RT-PCR, Multi-analyte, Multiple Targets |

08/17/2023 |

Source: FDA January 2026

The ongoing highly pathogenic avian influenza outbreaks in Canada are strengthening the demand for rapid field-deployable diagnostic solutions, directly supporting the growth of the market. According to the Government of Canada, January 2025, the Canadian Food Inspection Agency has managed widespread outbreaks that resulted in significant economic impact, including 32.3% decline in chicken exports and an 8.7% decline in turkey exports in 2022 compared to 2021, highlighting the urgency for faster disease containment. While current diagnostics rely on centralized rRT PCR testing at CFIA laboratories, result turnaround times exceed 4 hours, and logistical delays limit real-time decision-making at farms. As a result, the CFIA and federal partners are identifying the need for a rapid, affordable lateral flow-based test capable of detecting influenza A, including H5 and H7 subtypes, at sensitivity levels comparable to molecular assays. Hence, the market in Canada has strategic growth, and the demand is expected to accelerate the adoption of advanced LFAs in veterinary surveillance, outbreak response, and biosecurity programs.

APAC Market Insights

The Asia Pacific lateral flow assays market is the fastest-growing and is poised to grow at a CAGR of 7.7% by 2035. The market is driven by the vast population bases, increasing healthcare expenditure, and strong governmental focus on expanding diagnostic access in primary and rural care settings. The key drivers include the rising prevalence of infectious and chronic diseases, substantial public health investments in pandemic preparedness, and a growing local manufacturing ecosystem aiming for self-sufficiency. A significant trend is the health initiatives which prioritize the domestic production of medical devices including the rapid tests. Further, the regulatory harmonization efforts, such as those by the Asia Pacific Medical Technology Association, aim to streamline market access, while digital health integration is enhancing the utility of point-of-care testing in decentralized healthcare models across the region.

The China lateral flow assays (LFA) market growth is closely linked to the persistent and rising incidence of notifiable infectious diseases reported nationwide. According to the NLM January 2025 study, official surveillance data show that the reported Class A and B infectious disease cases increased from 2.43 million in 2022 to 3.51 million in 2023, while the incidence rate rose from 172.2 to 248.8 per 100,00 population, indicating renewed pressure on disease monitoring systems. Further, the high-volume diseases such as viral hepatitis, pulmonary tuberculosis, syphilis, and gonorrhea consistently accounted for over 92% reported cases between 2018 and 2023, creating a sustained demand for frequent screening and early detection tools in hospitals and public health clinics. The adoption of lateral flow assays across China’s public health and primary care systems is contributing to steady market growth alongside regulatory support from national health authorities.

Incidence and Mortality of Class A and B Public Infectious Diseases in China

|

Project/year |

Number of cases in million |

Number of deaths |

Population in million |

Incidence rate/100,000 |

Death rate/100,000 |

|

2018 |

3.063 |

23,174 |

1395.38 |

219.51 |

1.66 |

|

2019 |

3.072 |

24,981 |

1400.05 |

219.44 |

1.78 |

|

2020 |

2.58 |

21,655 |

1411.77 |

183.19 |

1.53 |

|

2021 |

2.712 |

22,177 |

1412.60 |

191.98 |

1.57 |

|

2022 |

2.431 |

21,834 |

1411.75 |

172.22 |

1.55 |

|

2023 |

3.5078 |

25,525 |

1409.67 |

248.83 |

1.81 |

Source: NLM January 2025

The lateral flow assays (LFA) market in India is growing steadily and is supported by the high infectious disease burden, expanding public healthcare expenditure, and the government-led screening programs. According to the IIJMR data in February 2024, India recorded 4 billion outpatient visits annually across public health facilities, creating a sustained demand for rapid point-of-care diagnostics in primary and community settings. Further, the national health mission finances large-scale screening programs for tuberculosis, HIV, malaria, and viral hepatitis, with diagnostics representing a core expenditure line item. Moreover, the IBEF April 2023 data shows that the health expenditure increased to 2.1% of GDP by 2023, reflecting a rising allocation toward preventive care and disease surveillance. Collectively, high patient volumes, expanding publicly funded screening initiatives, and regulatory support for rapid diagnostics underpin the sustained growth of the lateral flow assays market across India’s public health system and decentralized care environments.

Europe Market Insights

The Europe lateral flow assays market is defined by the stringent regulatory oversight under the in vitro diagnostic regulation and a strong push toward integrated decentralized healthcare models. The primary driver is the strategic EU level initative to strengthen the health system resilience that promotes the stockpiling of critical medical countermeasures, including rapid diagnostics. Aging demographics and the rising burden of antimicrobial-resistant infections are increasing the clinical demand for point-of-care testing across community and hospital settings. The market is transitioning toward higher value quantitative and digitally connected assays, moving beyond simple qualitative strips. Further, the market is experiencing a stable environment focused demand on preparedness rather than reactive purchasing.

The UK market is growing steadily and is supported by the sustained government spending on diagnostics, infectious disease surveillance, and emergency preparedness. According to the Government of the UK, April 2022 data, the government invested over 5.9 billion euros in testing and diagnostics primarily to maintain national infectious disease monitoring and rapid response capacity. Further, the NLM study in March 2025 depicts that 80 million PCR and lateral flow assay device tests were reported, with ongoing procurement to support outbreak readiness and seasonal respiratory surveillance. Moreover, the Office for National Statistics data in May 2024 shows that the UK healthcare expenditure exceeded £292 billion in 2023, with diagnostics and laboratory services embedded within NHS preventive and community care budgets. Overall UK experiences a steady demand for lateral flow assays across hospitals, community healthcare settings, and public health programs in the UK.

The lateral flow assays (LFA) market in Germany is supported by the sustained public healthcare expenditure, statutory health insurance reimbursement, and government-led infectious disease surveillance. According to the Debatis April 2023 data, Germany’s total health expenditure exceeded €501 billion in 2023, representing 12.0% of GDP, with diagnostics funded under the statutory health insurance system. Moreover, the EU Health Preparedness July 2023 report shows multiple antigen tests have been evaluated to meet the criteria and definitions by the Health Security Committee. Additionally, the Infection Protection Act continues to mandate the testing and surveillance measures for notifiable infectious diseases, sustaining government procurement and reimbursement of rapid diagnostic tests beyond the pandemic period. These data reinforce Germany’s position as a stable growth market within Europe.

COVID-19 Antigen Tests in Germany

|

Device ID |

REF number |

Name of submitting company |

Commercial name of the device |

Date |

|

1232 |

41FK10 |

Abbott Rapid Diagnostics |

Panbio COVID-19 Ag Rapid Test |

17/02/2021 |

|

1457 |

L031-118 {…}, L031-125A5, L031-129 {…} |

Acon Biotech (Hangzhou) Co., Ltd |

Flowflex SARS-CoV-2 Antigen Rapid Test |

14/07/2021 |

|

2108 |

REF 840001, REF 840003, REF 840005, REF 840007 |

AESKU.Diagnostics GmbH & Co KG |

AESKU.RAPID SARSCoV-2 |

14/10/2022 |

|

2277 |

COV-S35002 |

Assure Tech. (Hangzhou) Co., Ltd. |

COVID-19 Antigen Nasal Test Kit |

09/12/2022 |

|

3966 |

RC-HM02 |

Chastru Biotech Limited |

COVID-19 Antigen Rapid Test Cassette |

15/03/2023 |

Source: EU Health Preparedness July 2023

Key Lateral Flow Assays Market Players:

- Abbott Laboratories (U.S.)

- QuidelOrtho (U.S.)

- Siemens Healthineers (Germany)

- Roche (Switzerland)

- Danaher Corporation (Beckman Coulter, etc.) (U.S.)

- BD (Becton, Dickinson and Company) (U.S.)

- Thermo Fisher Scientific (U.S.)

- bioMérieux (France)

- PerkinElmer (U.S.)

- Merck KGaA (Germany)

- Hologic, Inc. (U.S.)

- bioLytical Laboratories (Canada)

- OraSure Technologies (U.S.)

- Sekisui Diagnostics (U.S.)

- Boditech Med Inc. (South Korea)

- SD Biosensor (South Korea)

- Atomo Diagnostics (Australia)

- Mylab Discovery Solutions (India)

- BTNX Inc. (Canada)

- ACON Laboratories (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Abbott Laboratories is a dominant player in the lateral flow assays market, mainly via its Alere acquisition. Abbott strategically uses its massive manufacturing scale and global distribution to lead in rapid infectious disease and cardiometabolic testing. Its key initiative is the integration of these rapid tests with a digital health platform to enhance data utility and user engagement. In 2024, the company has made annual sale of USD 42 billion.

- QuidelOrtho, formed by a major merger, is a top player in the market. Its strategy focuses on creating a comprehensive diagnostic ecosystem, pairing its high-volume rapid assays with its advanced laboratory instrumentation. This synergy allows for a one-stop diagnostic solution for customers, from rapid screening to confirmatory testing, strengthening customer retention and driving growth. According to the 2024 annual report, the company has made a revenue of USD 2.78 billion.

- Siemens Healthineers applies its expertise in high-throughput laboratory automation to the lateral flow assays (LFA) market via its Atellica Solution. A key strategic initiative is the development of advanced quantitative lateral flow assays that can be run on automated immunoassay analyzers. This blurs the line between central lab and point of care, offering hospitals the speed of lateral flow with the precision workflow integration and data management of a fully automated platform.

- Roche competes in the lateral flow assays market via its point-of-care division. Roche’s strategy emphasizes connectivity and high clinical utility. Its cobas Liat PCR system represents a strategic pivot, but for lateral flow, it focuses on professional use of rapid tests seamlessly connected via the cobas IT infrastructure. This ensures reliable, traceable results within the electronic medical record, catering to the stringent data management needs of institutional healthcare settings.

- Danaher Corporation operates in the lateral flow assays market primarily via its subsidiary Beckman Coulter. Danaher’s strategic approach is underpinned by its renowned Danaher Business System, driving continuous operational improvement and quality in assay manufacturing. A core initiative is expanding its rapid test menu for critical care and triage settings within hospitals, ensuring these assays deliver central lab quality performance at the point of need, thereby improving patient throughput and clinical decision speed.

Here is a list of key players operating in the global market:

The global lateral flow assays market is highly competitive and fragmented, defined by a mix of established diagnostic giants and specialized rapid test developers. The key players are aggressively pursuing strategic initiatives to consolidate market share, including acquisitions to expand product portfolios and geographic reach, significant R&D investments in multiplexing and digital readers technologies, and forging partnerships with government bodies and distributors, mainly highlighted during the pandemic. For example, in July 2024, Roche closes acquisition of LumiraDx’s Point of Care technology to expand access to diagnostic testing in primary care. The competitive edge is increasingly defined by the ability to offer high complexity quantitative tests alongside traditional qualitative strips, pushing the market toward more advanced point of care diagnostics.

Corporate Landscape of the Lateral Flow Assays (LFA) Market:

Recent Developments

- In November 2025, Sapphiros announced a strategic agreement with Roche, providing Roche access to 1 billion lateral flow tests and access to future molecular point-of-care tests. The reel-to-reel manufacturing capability of Sapphiros can produce up to 5 billion diagnostics per year.

- In July 2025, VolitionRx Limited, a multi-national epigenetics company, today announces it has demonstrated quantification of nucleosomes in whole venous blood in minutes utilizing a simple lateral flow device.

- In May 2024, Surmodics, Inc., announced that it has entered into a definitive agreement to be acquired by GTCR, a leading private equity firm with a long track record of investment expertise across healthcare and healthcare technology.

- Report ID: 4871

- Published Date: Feb 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.