Dialysis Market Outlook:

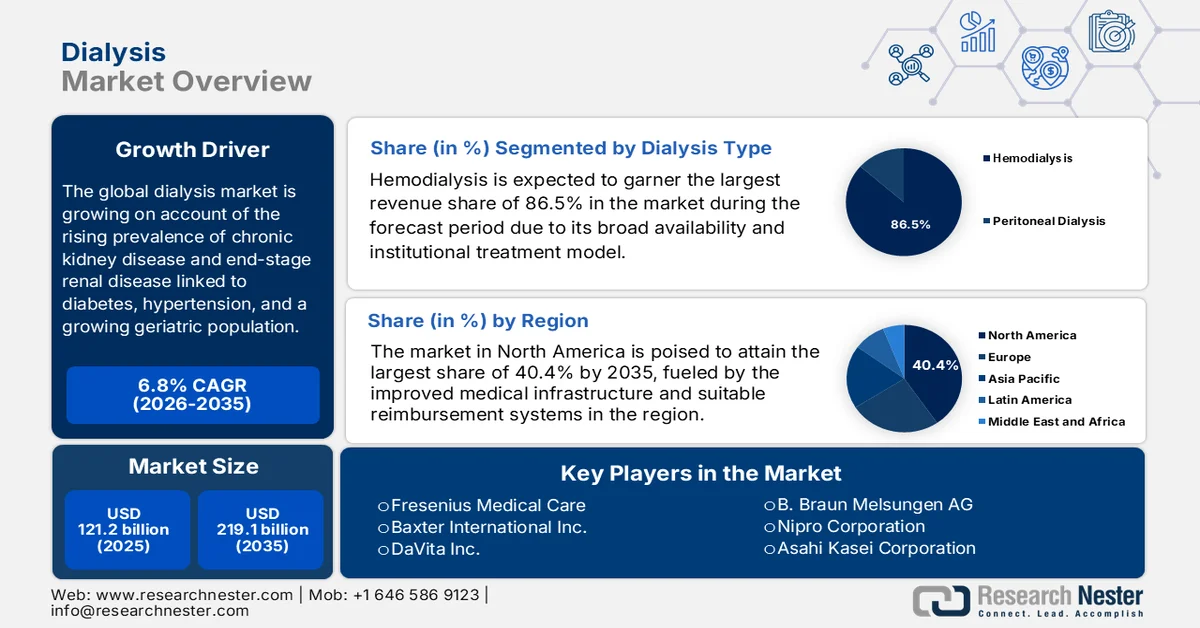

Dialysis Market size was valued at USD 121.2 billion in 2025 and is projected to reach USD 219.1 billion by the end of 2035, rising at a CAGR of 6.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of dialysis is evaluated at USD 129.4 billion.

The global dialysis market is experiencing robust, sustained growth, which is propelled by the rising prevalence of chronic kidney disease and end-stage renal disease linked to diabetes, hypertension, and a growing geriatric population. According to the article published by the Institute for Health Metrics and Evaluation in November 2025, chronic kidney disease affected 788 million adults worldwide in 2023, which is double from the past three decades. CKD is now the ninth leading cause of death and a major contributor to disability, with impaired kidney function responsible for more than 11% of cardiovascular deaths. Besides, the study highlights the urgent need for better screening, prevention, and treatment strategies to address this growing global health challenge, and hence indicates an encouraging opportunity for the dialysis industry in the upcoming years.

Furthermore, the dialysis market is witnessing strong growth stimulated by suitable payers' reimbursement structures. Competitive pricing and supportive payment policies are facilitating higher adoption of dialysis services. The U.S. Centers for Medicare & Medicaid Services in January 2025, implemented the inclusion of oral-only renal dialysis drugs and biological products into the ESRD prospective payment system bundled payment. This particular policy also expanded the transitional add-on payment adjustment for new and innovative equipment and supplies to cover home dialysis machines, providing temporary reimbursement incentives for advanced technologies. On the other hand, CMS corrected prior claim errors that were related to TPNIES capital-related assets, thereby ensuring proper payment adjustments. Overall, the ESRD PPS continued to deliver bundled, patient-level payments for dialysis services, including drugs, labs, supplies, and training, with add-ons for innovation and high-cost outliers, hence increasing adoption in this sector.

Global and Regional Dialysis Costs and Modalities: HD, PD, Home HD, and Transplant (2023-2024)

|

Country/Region |

Hemodialysis (HD) Annual Cost (USD) |

Peritoneal Dialysis (PD) Annual Cost (USD) |

Home HD Annual Cost (USD) |

Kidney Transplant Cost (USD) |

|

Global Average |

57,334 |

49,490 |

- |

First year: 75,326; Subsequent years: 16,672 |

|

Australia (2022) |

- |

- |

7% of HD patients |

- |

|

Canada (2021) |

In-center HD: higher than PD |

Lower than in-center HD |

Home HD: higher than PD |

- |

|

Taiwan (2022-2027) |

- |

- |

- |

Dialysis is fully reimbursed; kidney care is USD 19 billion/year. |

|

U.S. |

57,334 |

49,490 |

- |

First year: 75,326; Subsequent years: 16,672 |

Source: IACN

Key Dialysis Market Insights Summary:

Regional Highlights:

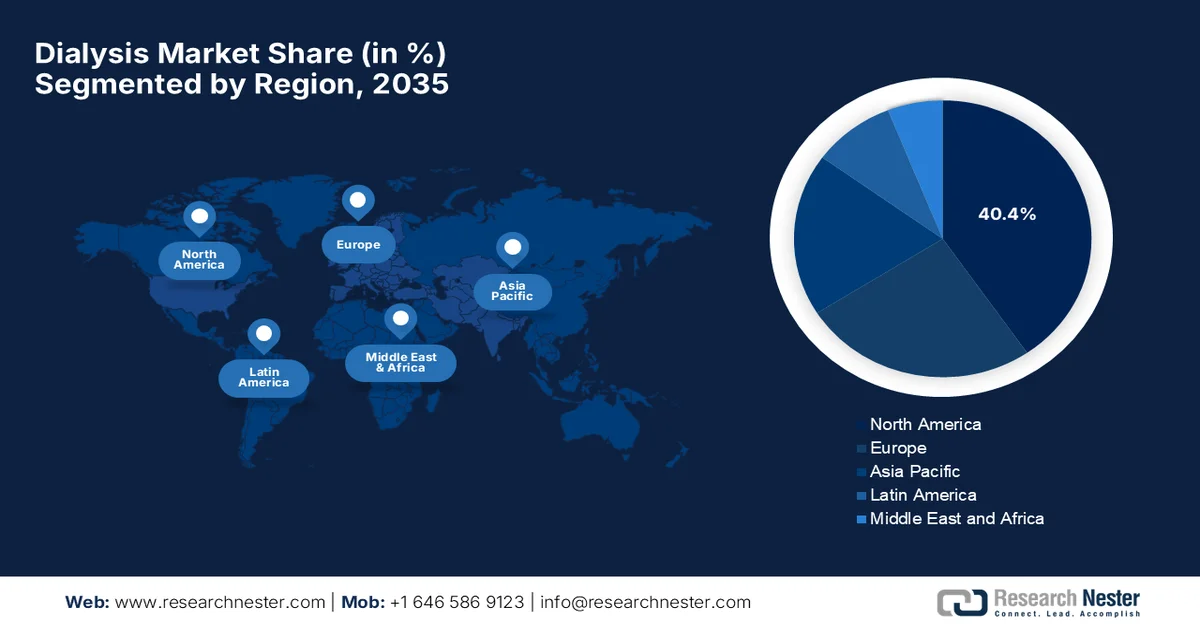

- North America dialysis market is projected to hold a dominant 40.4% share by 2035, owing to advanced healthcare infrastructure and strong reimbursement systems

- Asia Pacific is anticipated to witness the fastest growth by 2035, attributed to rising affected population and expanding medical access

Segment Insights:

- Hemodialysis segment in the dialysis market is projected to account for an 86.5% revenue share by 2035, propelled by its broad availability, clinical effectiveness for ESRD, and institutional treatment model

- Service segment is expected to secure a significant share by 2035, impelled by increasing demand for frequent treatments generating recurring service fees

Key Growth Trends:

- Technological advancements

- Increasing adoption of home‑based dialysis

Major Challenges:

- High treatment costs

- Limited access to dialysis centers

Key Players: Fresenius Medical Care, Baxter International Inc., DaVita Inc., B. Braun Melsungen AG, Nipro Corporation, Asahi Kasei Corporation, Nikkiso Co. Ltd., Diaverum, NxStage Medical Inc., Toray Industries Inc., Medtronic plc, Rockwell Medical Technologies Inc., JMS Co. Ltd., Satellite Healthcare Inc., AllMed Medical GmbH, Outset Medical Inc., Alebund Pharmaceuticals, R1 Therapeutics, Bayer, Quanta Dialysis Technologies, Innovative Renal Care, Advin Health Care, Diaverum Deutschland GmbH, Biosun Corporation, Renalyx Health Systems Private Limited, IHH Healthcare Berhad.

Global Dialysis Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 121.2 billion

- 2026 Market Size: USD 129.4 billion

- Projected Market Size: USD 219.1 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, Brazil, South Korea, Mexico, Indonesia

Last updated on : 26 March, 2026

Dialysis Market - Growth Drivers and Challenges

Growth Drivers

- Technological advancements: The dialysis market is currently accelerating with continued developments of advanced dialysis equipment. The innovations in terms of portable and wearable dialysis devices, improved dialyzers, and biocompatible consumables improve the overall treatment outcomes and accessibility. In October 2024, Vivance announced the successful completion of the pre-pivotal trial of its wearable peritoneal dialysis device, which is Viva Kompact, at Singapore General Hospital. The U.S. Food & Drug Administration (FDA) designated breakthrough device was tested for safety and performance in home use, with 10 patients completing at least one week of dialysis independently without serious adverse events. Hence, with consistent efforts from global pioneers, the dialysis market will propagate at a rapid pace.

- Increasing adoption of home‑based dialysis: Remarkable improvements in home dialysis technologies, such as peritoneal dialysis and automated home hemodialysis, are empowering patients to receive treatment other than in clinics and lowering long‑term costs. As per an article published by Home Dialysis Central in December 2025, the home dialysis rates reached their highest levels in a decade. Data from 2023 revealed that the incidence of peritoneal dialysis rose from 9.1% a decade earlier to 14.5%, whereas the prevalent cases increased from 9.3% to 12.1%. Besides, home hemodialysis also saw modest growth, with incident rates rising from 0.3% to 0.4% and prevalent rates from 1.5% to 2.5%. Therefore, these findings highlight a growing shift toward home-based dialysis options within one decade, thus reflecting improved patient access and interest in flexible treatment modalities, hence suitable for bolstering dialysis market growth.

- Expanded healthcare infrastructure & policies: The existence of consistent efforts to increase healthcare access through expanded dialysis center networks is rearranging the growth dynamics of the dialysis market. According to the article published by the Press Information Bureau (PIB) in August 2025, the Pradhan Mantri National Dialysis Program (PMNDP) has been rolled out across all 36 states and Union Territories by covering almost 751 districts with 1,704 operational centers as of June 2025. The initiative is largely focused on establishing hemodialysis centers in district hospitals and gradually expanding to community health centers based on demand. In addition, it is supported by the National Health Mission, whereas states and UTs receive financial assistance to provide both hemodialysis and peritoneal dialysis services, ensuring access even in remote and tribal areas, hence strengthening the dialysis market’s exposure.

Challenges

- High treatment costs: Dialysis treatments, mostly hemodialysis, consist of expensive machinery, consumables, and recurring sessions, which makes the entire process financially challenging for patients and healthcare systems. Patients typically require treatment three times a week, which in turn leads to significant ongoing expenses hindering adoption in the dialysis market. Meanwhile, in terms of low- and middle-income countries, limited insurance coverage or public funding exacerbates the problem, by reducing access and contributing to higher mortality rates. On the other hand, the aspect of high costs also discourages providers from adopting advanced technologies such as wearable or portable dialysis devices. In addition, hospitals from price-sensitive regions face budget constraints when scaling dialysis programs, creating hurdles between quality care and affordability.

- Limited access to dialysis centers: The existence of geographic disparities is considered to be yet another major bottleneck for the dialysis market since it directly impacts treatment availability. Not all rural and remote areas have dialysis centers, requiring patients to travel long distances multiple times a week, which is physically and financially exhausting. On the other hand, infrastructure limitations, such as insufficient water purification systems, power supply issues, and a lack of trained staff, in turn reduce accessibility. These factors result in delayed treatments, negatively impacting patient outcomes, and increasing hospitalization rates. Dialysis market expansion in underserved regions is costly as well as logistically complex. Without proper accessibility, large portions of the population remain untreated, representing both a public health concern and a missed market opportunity.

Dialysis Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 121.2 billion |

|

Forecast Year Market Size (2035) |

USD 219.1 billion |

|

Regional Scope |

|

Dialysis Market Segmentation:

Dialysis Type Segment Analysis

In the dialysis type segment, hemodialysis is expected to garner the largest revenue share of 86.5% in the dialysis market during the forecast period. Its broad availability, clinical effectiveness for ESRD, and institutional treatment model are the key drivers behind the sub-segment’s dominance. As per an article published by the National Institute of Health (NIH) in February 2022, hemodialysis is the most common form of kidney replacement therapy worldwide, accounting for nearly 69% of all kidney replacement therapy and almost 89% of dialysis. Besides, standardizing outcome measures, improving registries, and addressing inequities are highly essential to enhancing HD care and reducing the global burden of kidney failure. Therefore, with evidence-based strategies and continued investment in infrastructure, hemodialysis is expected to maintain its leading position in the global market, driving revenue growth.

Type Segment Analysis

Under the type segment, service is anticipated to garner a significant revenue share in the dialysis market over the forecasted years. The growth of the segment is mainly propelled by patients requiring frequent treatment, driving recurring service fees. In March 2024, DaVita Inc. announced strategic agreements to expand operations in Brazil and Colombia, while also entering Chile and Ecuador through acquisitions from Fresenius Medical Care worth USD 300 million. With these transactions, DaVita will operate more than 270 clinics serving over 60,000 patients, making it the largest dialysis services provider in Latin America. Hence, from a strategic perspective, such instances demonstrate the prominence of targeted acquisitions and regional expansion, allowing leading dialysis service providers to capture high-volume patient bases. The service segment allows for securing recurring revenue streams, especially in areas where demand for hemodialysis services is growing rapidly.

Disease Indication Segment Analysis

By the conclusion of the forecast period, the end-stage renal disease (ESRD), which is under the disease indication segment, is predicted to grow at a considerable rate in the dialysis market. The ESRD is considered to be the primary driver of dialysis demand globally, influenced by the chronic nature of the condition and regular treatment requirements. As per the article published by NIH in June 2025, the incidence of end-stage renal disease in the U.S. rose by over 31% in the last two decades, reflecting the growing burden of kidney failure. The report outlines that age is a major factor, with CKD prevalence reaching 38% among those 65 and older, whereas men have about a 50% higher cumulative incidence of ESRD when compared to women. Therefore, these trends highlight the complex interplay of demographics and access in shaping kidney disease outcomes, denoting a huge growth opportunity for pioneers in this field.

Our in-depth analysis of the dialysis market includes the following segments:

|

Segment |

Subsegments |

|

Dialysis Type |

|

|

Type |

|

|

Disease Indication |

|

|

End user |

|

|

Treatment Setting |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Dialysis Market - Regional Analysis

North America Market Insights

The North America dialysis market is predicted to account for the highest revenue share of 40.4% by the end of the forecast period. The advanced healthcare infrastructure and strong reimbursement systems are the key drivers fueling the region’s leadership. The region hosts major service providers and medical technology firms. As per an article published by Home Dialysis Central in January 2025, there has been a steady growth in home dialysis use over the decade leading up to 2022. Incident patients starting home dialysis rose from 8.5% to 14.5%, whereas PD increased more than home HD. Prevalent patients also saw gains, with PD rising to 12.1% and home HD to 2.4%. Younger, rural, and lower-SDI patients were more likely to use home dialysis. On the other hand, patients with job-based plans and Medicare as a secondary payer had the highest home dialysis rates, hence suitable for bolstering market growth in the region.

U.S. Home Dialysis Facility Distribution by Patient Volume and Modality: 2022 Data

|

Number of Patients per Facility |

Home Dialysis (%) |

Peritoneal Dialysis (PD) (%) |

Home Hemodialysis (HHD) (%) |

|

0 |

21.23 |

22.24 |

40.76 |

|

1-10 |

26.79 |

30.85 |

43.91 |

|

11-20 |

22.31 |

22.50 |

9.79 |

|

21-30 |

12.20 |

11.22 |

2.94 |

|

31-40 |

6.50 |

5.82 |

1.05 |

|

41-50 |

4.00 |

2.69 |

0.55 |

|

51+ |

6.96 |

4.68 |

1.01 |

Source: Home Dialysis Central

The higher disease prevalence rates of chronic kidney disease and diabetes, along with a heavy reliance on federal reimbursement programs, are rearranging the growth dynamics of the dialysis market in the U.S. The industry is undergoing a significant transition toward home-based therapies and remote patient monitoring to reduce long-term healthcare costs. According to the report published by the Centers for Disease Control and Prevention in May 2024, about 35.5 million adults in the country, which is 14%, or more than 1 in 7, were affected with CKD in 2023. The report underscored that CKD prevalence increases significantly with age, which affected 34% of adults aged 65 and above, compared to 12% among people aged 45-64 years and 6% in 18-44 years. Therefore, these findings highlight the urgent need for management strategies, i.e., dialysis, to prevent complications such as heart disease and stroke.

The publicly funded healthcare framework, where provincial health authorities manage the majority of renal care services, is responsible for uplifting the dialysis market in Canada. The market is reshaped by a strong focus on enhancing remote patient monitoring and expanding access to care for indigenous communities through telehealth integration. In May 2023, the Government of Saskatchewan and the Saskatchewan Health Authority inaugurated a six-bed satellite hemodialysis unit at the Northwest Health Facility in Meadow Lake. The government invested a total amount of USD 2.6 million in construction and committed USD 700,000 annually for operations, with additional support from the Meadow Lake Tribal Council and Indigenous Services Canada. Hence, such instances in the country indicate the prominence of government-led investments and collaborations in strengthening dialysis infrastructure and accessibility across Canada.

APAC Market Insights

The dialysis market in the Asia Pacific is identified as the fastest-growing sector in the global landscape. The region’s market is primarily propelled by a rising number of affected population and expanding medical access. The countries across the region are making generous investments in terms of dialysis equipment, and local manufacturing initiatives are reducing reliance on foreign-based imports. As stated by the government of Australia in June 2023, Hornsby Ku-ring-gai Hospital introduced renal dialysis services for the first time in its 90-year history as part of a USD 265 million redevelopment. The new 10-chair unit, which has been operational since February 2023, has already delivered over 1,150 treatments and provides care six days a week in just three months. Hence, such satellite units reflect the region’s focus on expanding dialysis infrastructure and improving accessibility, thus supporting the growth potential of the dialysis market.

A structural shift toward domestic manufacturing and increased government-led healthcare coverage are driving dialysis market expansion in China. Growth is primarily fueled by a strategic national push toward peritoneal dialysis to improve access for patients in rural and underserved regions. In addition, market dynamics are also propelled by Buy China policies that support local medical device companies, as well as a centralized procurement system, which is designed to lower the cost of consumables. According to the January 2025 government data, the country’s health authorities have prioritized expanding hemodialysis services nationwide, and as of the end of 2024, more than 90% of county-level hospitals already offer hemodialysis, reflecting a 20-percentage-point increase when compared to the past decade, hence denoting a positive dialysis market outlook.

India dialysis market is solidifying its presence in the global dynamics owing to the government healthcare schemes, expanding dialysis infrastructure, and technological advancements in renal care. The sector is characterized by a heavy reliance on private providers, along with a gradual push for peritoneal dialysis to overcome the challenges of limited clinical facilities and high travel costs for patients. In February 2024, Odisha Chief Minister dedicated dialysis centers at 16 sub-district hospitals, thereby expanding access to kidney care under the state’s 5T initiative. A total of 32 dialysis centers have been established at the sub-district level, building on the SAHAY scheme, which has provided free, life-saving dialysis services without a heavy financial burden. Hence, such initiatives reflect the prominence of state-led infrastructure expansion and supportive policies, which are strengthening the dialysis ecosystem in India.

Europe Market Insights

The Europe dialysis market is emerging as a mature and highly regulated landscape that benefits from a strong presence of established medical technology firms and a mix of public and private healthcare delivery models. Market dynamics are efficiently fueled by an aging population and a strong R&D ecosystem. For instance, in May 2024, Fresenius Medical Care presented nearly 40 company-affiliated research abstracts at the 61st Renal Association Congress Europe in Stockholm, thereby highlighting innovations in kidney care with real-world evidence. It also mentions the key findings, including a 23% reduction in mortality with high-volume hemodiafiltration in the CONVINCE study and the use of AI and machine learning to improve hemodialysis outcomes, including predicting hospitalization risk and classifying arteriovenous access aneurysms. Hence, the consistent efforts from domestic pioneers reflect the region’s leadership in advancing dialysis care and its focus on improving patient outcomes.

Germany dialysis market is highly focused on improving a dense network of specialized centers operated by both non-profit organizations and global companies. Value-based care for long-term patient health and efforts on fewer hospital visits are also responsible for uplifting the market. In December, 2024, as per the official press release, the funding for dialysis has been improved to strengthen local access and promote home dialysis under new agreements between the KBV and GKV-Spitzenverband. Reimbursement rates for pediatric dialysis rose by 3.85%, whereas adult dialysis fees increased by 3.0%, with added surcharges to support home-based treatments. New flat-rate fees were introduced, including USD 114 per week for the first year of home dialysis, along with surcharges for peritoneal dialysis, home hemodialysis, and night dialysis. In total, about USD 70.8 million was allocated, with USD 54.5 million directed toward fee increases and the remainder used for structural adjustments, hence denoting a positive market outlook.

A strategic emphasis on cost-efficiency and patient autonomy is responsible for uplifting the UK dialysis market. The country operates as a highly centralized, single-payer system wherein the National Health Service (NHS) serves as the primary provider and purchaser of renal care. In July 2025, the Welsh Kidney Network released an updated home dialysis utility reimbursement toolkit, which helps patients manage rising costs. The toolkit was developed with UKKA, ANN UK, and the Association of Renal Technologists, and it includes a new reimbursement calculator, patient forms, and practice guidelines. Besides, in August, 2024, NHS England issued guidance on a universal dialysis transport support offer to improve patient access. It states that dialysis patients typically require transport three times per week, and the framework allows them to choose flexible options such as public transport, self-driving, or support from relatives, with reimbursement at locally agreed rates, hence suitable for bolstering the market’s development in the country.

Key Dialysis Market Players:

- Fresenius Medical Care (Germany)

- Baxter International Inc. (U.S.)

- DaVita Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Nipro Corporation (Japan)

- Asahi Kasei Corporation (Japan)

- Nikkiso Co., Ltd. (Japan)

- Diaverum (Sweden)

- NxStage Medical, Inc. (U.S.)

- Toray Industries, Inc. (Japan)

- Medtronic plc (Ireland)

- Rockwell Medical Technologies, Inc. (U.S.)

- JMS Co., Ltd. (Japan)

- Satellite Healthcare, Inc. (U.S.)

- AllMed Medical GmbH (Germany)

- Outset Medical, Inc. (U.S.)

- Alebund Pharmaceuticals (U.S.)

- R1 Therapeutics (U.S.)

- Bayer (Germany)

- Quanta Dialysis Technologies (UK)

- Innovative Renal Care (U.S.)

- Advin Health Care (India)

- Diaverum Deutschland GmbH (Germany)

- Biosun Corporation (South Korea)

- Renalyx Health Systems Private Limited (India)

- IHH Healthcare Berhad (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Fresenius Medical Care is one of the world’s largest dialysis providers and manufacturers, which is offering a full portfolio of hemodialysis machines, dialyzers, consumables, and services. The company benefits from a vertically integrated model combining equipment manufacturing with a vast global clinic network, allowing it to maintain a leading position in this field.

- Baxter International Inc. is yet another dominant force in this sector, which has a strong focus on renal care, particularly peritoneal dialysis systems and consumables. The firm emphasizes automated and home‑based therapies and has undertaken organizational restructuring to accelerate R&D in wearable, portable, and patient‑centric dialysis solutions.

- DaVita Inc. is also a major global dialysis service provider with one of the largest outpatient dialysis networks, primarily in the U.S., and it is expanding internationally. The company’s competitive strength lies in care delivery, operational scale, and data analytics to enhance patient outcomes and optimize clinic utilization.

- B. Braun Melsungen AG is a well‑established global healthcare firm that is best known for high‑quality hemodialysis systems, consumables, and water treatment solutions. Besides, the firm’s strategy focuses on product innovation, clinical safety, and strong regional presence, especially in Europe.

- Nipro Corporation is a prominent medical device company from Japan that has a solid global footprint in dialysis consumables and equipment. The firm competes on cost‑effective, high‑quality products which are suitable for both emerging markets and established regions.

Below is the list of some prominent players operating in the global dialysis market:

The global dialysis market is dominated by large, diversified medical device and healthcare companies. The pioneers, such as Fresenius Medical Care and Baxter International Inc., are leading in terms of equipment, consumables, and care delivery across both developed and emerging regions. These players focus on innovation and strategic expansion through acquisitions and partnerships. Meanwhile, service providers such as DaVita Inc. and Diaverum strengthen global clinical networks, whereas regional players such as Advin Health Care and Renalyx are focused on localized, cost‑competitive technology. In March 2025, Diaverum Germany announced the acquisition of two new clinics in Neubrandenburg and Neustrelitz to deliver enhanced renal care through dialysis, bringing its total presence to a total of 18 clinics in the country, hence positively impacting the market’s expansion and exposure.

Corporate Landscape of the Dialysis Market:

Recent Developments

- In March 2026, Alebund Pharmaceuticals announced a collaboration with R1 Therapeutics for AP306, which is a first-in-class pan-phosphate transporter inhibitor aimed at treating hyperphosphatemia in CKD patients on dialysis.

- In March 2026, Bayer announced that Finerenone met the primary endpoint with the Phase III FIND-CKD study, showing significant benefits in slowing kidney disease progression among patients with non-diabetic chronic kidney disease.

- In September 2025, Quanta Dialysis Technologies entered into an alliance with Innovative Renal Care in a multi-year agreement to expand access to the Quanta dialysis system across the U.S., following a successful pilot in Iowa.

- Report ID: 4643

- Published Date: Mar 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.