IoT Integration Market Outlook:

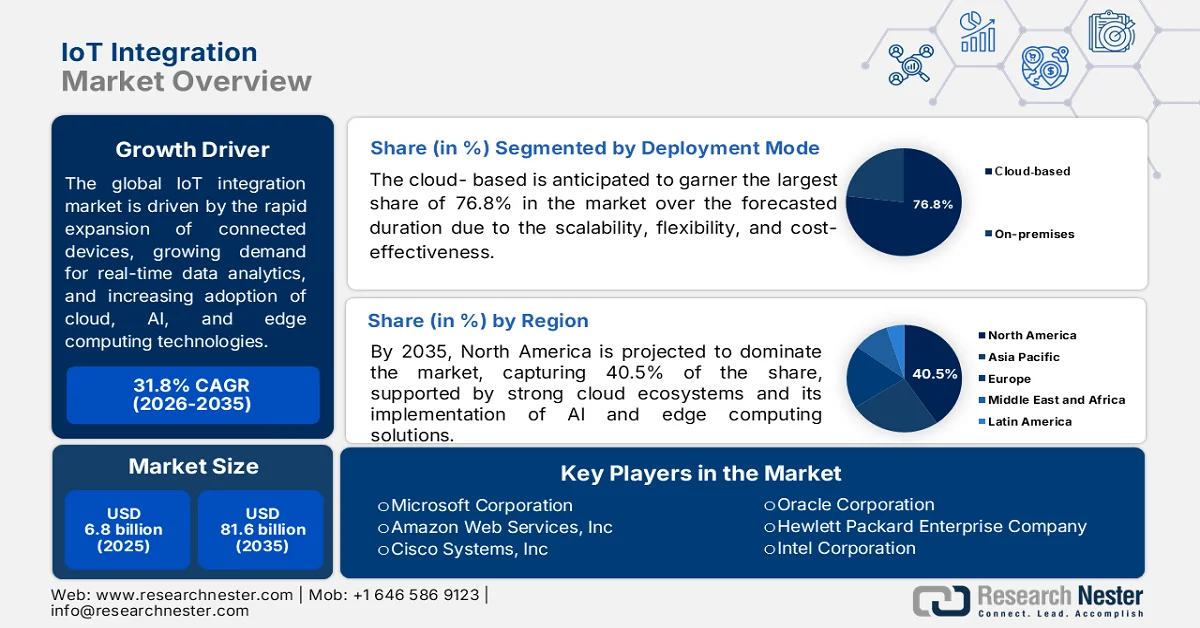

IoT Integration Market size was valued at USD 6.8 billion in 2025 and is projected to reach USD 81.6 billion by the end of 2035, expanding at a CAGR of 31.8% during the forecast period, 2026-2035. In 2026, the industry size of IoT integration is assessed at USD 8.9 billion.

The global IoT integration market is projected to experience exceptional growth owing to the continued digital transformation of industries such as manufacturing, healthcare, and retail. This growth is fueled by the increasing necessity to connect disparate systems and legacy infrastructure into unified, data-driven ecosystems. In this context, the report published by IoT M2M Council (IMC) in May 2024 stated that the worldwide IoT connections are forecast to grow from 16.1 billion in 2023 to 39.9 billion by 2033, with a CAGR of almost 10%, wherein the annual device sales are rising from 4.1 billion to 8.7 billion. The report also underscored that short‑range technologies will dominate at 73% of connections, whereas cellular will expand to 7.5 billion, including 5.5 billion 5G (mostly mMTC). The IoT industry value is expected to reach a surging value of USD 934 billion in 2033, led by consumer use and enterprise sectors such as utilities, retail, and logistics.

Furthermore, organizations across different nations prioritize real-time operational visibility and automated decision-making, due to which the demand for middleware and professional services such as system design, device management, and platform integration is surging at an extensive pace. According to an article published by the National Institute of Health (NIH) in August 2023, the IoT adoption is accelerating owing to the heightened demand for automation and efficiency, with connected devices now exceeding the global population, thereby remarkably expanding data exchange across networks. Besides, this research emphasizes widespread deployment across healthcare, agriculture, smart cities, and Industry 4.0, in which IoT enables real-time monitoring, resource optimization, and improved operational outcomes through sensor-driven data collection. Apart from this, it states that continued advancements in AI, machine learning, and network technologies are highly essential, thus benefiting the IoT integration market.

Key IoT Integration Market Insights Summary:

Regional Highlights:

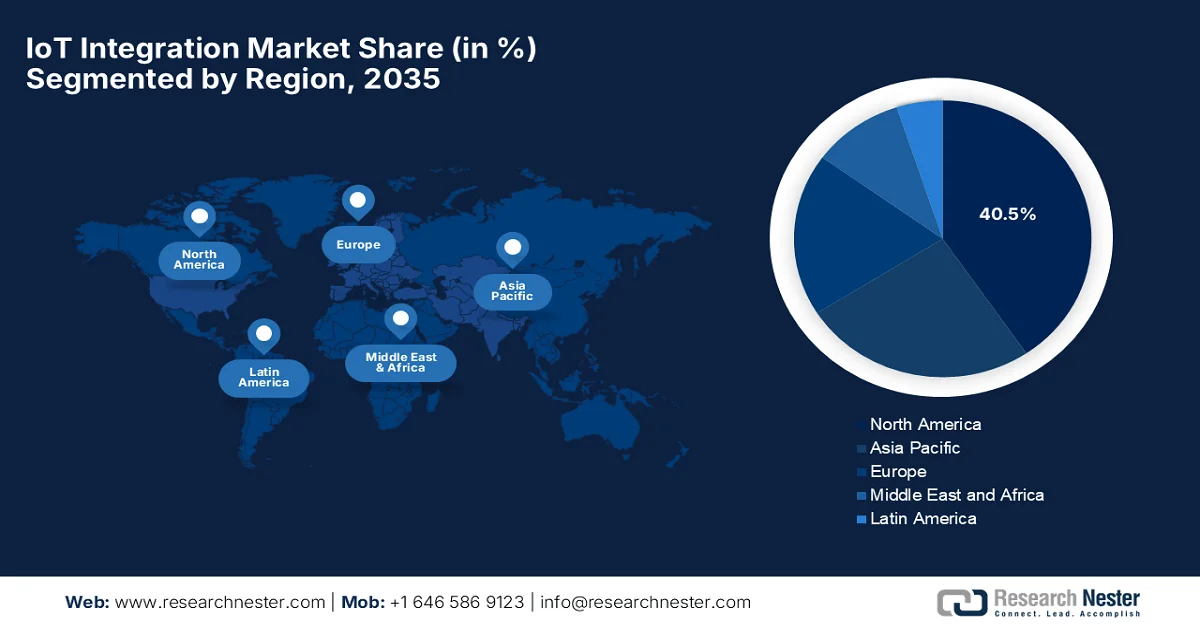

- North America IoT integration market is expected to command a 40.5% share by 2035, propelled by strong enterprise IoT adoption, advanced cloud infrastructure, and early deployment of AI and edge computing

- Asia Pacific is projected to witness the fastest growth throughout 2026-2035, impelled by expanding industrial IoT adoption and rising demand for smart healthcare and precision agriculture solutions

Segment Insights:

- The cloud-based segment in the IoT integration market is anticipated to account for a 76.8% share by 2035, driven by scalability, flexibility, and cost-effectiveness enabling seamless data integration across connected devices

- System integration services segment is expected to grow at a notable pace by 2035, fueled by increasing complexity in managing multi-vendor IoT ecosystems requiring centralized control and seamless data flow

Key Growth Trends:

- Proliferation of connected devices

- Growth of smart cities and industrial automation

Major Challenges:

- High implementation and maintenance costs

- Regulatory and compliance complexity

Key Players: International Business Machines Corporation (U.S.), Microsoft Corporation (U.S.), Amazon Web Services, Inc. (U.S.), Cisco Systems, Inc. (U.S.), Oracle Corporation (U.S.), Hewlett Packard Enterprise Company (U.S.), Intel Corporation (U.S.), Google LLC (U.S.), Accenture plc (Ireland), Capgemini SE (France), Siemens AG (Germany), Robert Bosch GmbH (Germany), SAP SE (Germany), Iridium Communications (U.S.), Qualcomm (U.S.), Augentix (Taiwan), Arduino (Italy), Edge Impulse (U.S.), Focus.AI (U.S.), Foundries.io (UK), Netmore Group (Sweden), Actility (France), Schneider Electric SE (France), Hitachi, Ltd. (Japan), Fujitsu Limited (Japan), Samsung SDS Co., Ltd. (South Korea), Tata Consultancy Services Limited (India), Tech Mahindra Limited (India), Telekom Malaysia Berhad (Malaysia).

Global IoT Integration Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.8 billion

- 2026 Market Size: USD 8.9 billion

- Projected Market Size: USD 81.6 billion by 2035

- Growth Forecasts: 31.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Brazil, Mexico

Last updated on : 4 May, 2026

IoT Integration Market - Growth Drivers and Challenges

Growth Drivers

- Proliferation of connected devices: There has been a swift rise in connected devices such as sensors, wearables, and smart appliances, which is an important growth driver for the IoT integration market. Organizations require integration solutions to manage interoperability and data exchange across different systems, thereby boosting demand for efficient IoT integration services. As per an article which was published by the Arxiv Organization in February 2025, there has been an evolution of wearable technology from simple devices to more advanced, AI-powered systems integrated into daily life. At the same time, it emphasizes that technologies such as IoT, AI, and AR are enhancing personalization, actual adaptability, and user experience across healthcare, productivity, and lifestyle domains. In addition, it concludes that wearable technology will continue transforming human-technology interaction.

- Growth of smart cities and industrial automation: The rise of smart city initiatives across different nations, along with Industry 4.0 adoption, is accelerating IoT integration demand. Governments and enterprises are deploying interconnected systems for traffic management, energy optimization, and automation, driving growth in the IoT integration market. As per an article published by Cambridge University in April 2024 states that there is a growing importance for smart cities in global markets, especially within ASEAN initiatives such as the ASEAN Smart Cities Network. It identifies three key regulatory areas, i.e., IoT-based trade in goods and services, international standard-setting, and data governance. The study emphasizes that smart cities operate as interconnected systems where data collection, processing, and AI-based services blur traditional trade distinctions between goods and services, thus positively contributing to the market’s expansion.

- Advancements in AI, cloud, and edge computing: The emergence of technologies is driving IoT integration expansion, whereas these innovations enable faster data processing and intelligent automation, prompting surging adoption in the IoT integration market. In this context, the Organization for Economic Co-operation and Development (OECD) in October 2023, stated that IoT adoption is expanding, wherein global IoT connections are surpassing non-IoT devices, and venture capital investment exceeded a significant value of USD 8 billion in a year. IoT-related patents also grew at nearly 20% annually, thereby accounting for more than 11% of global patenting activity. Semiconductor components for IoT now represent about 5% to 7% of the worldwide semiconductor industry. Apart from this, the report underscored that 29% of firms in Europe use IoT, whereas its 23% in Canada and 14% in Korea, thus denoting an optimistic market opportunity.

Challenges

- High implementation and maintenance costs: The deployment of IoT integration solutions involves extensive upfront and ongoing costs, which can cause limitations to adoption, especially in terms of small and medium-sized enterprises. These expenses are for hardware installation, sensor deployment, cloud infrastructure, software licensing, and system integration services. In addition, maintaining IoT ecosystems necessitates continuous monitoring, updates, and technical support, which in turn increases operational costs. Organizations in the IoT integration market need skilled personnel in order to manage complex IoT architectures, which adds to labor expenses. The large enterprises in this sector can absorb these costs, but smaller firms often face budget constraints, slowing down widespread adoption, thus negatively impacting the market’s growth.

- Regulatory and compliance complexity: The IoT integration market faces extensive regulatory and compliance challenges influenced by the increasing government focus on data privacy, cybersecurity, and cross-border data transfer. On the other hand, regulations such as GDPR and other regional data protection laws require organizations to implement strict data handling and storage practices. Therefore, compliance becomes more complex when it comes to IoT systems operating across multiple countries with changing legal frameworks. In this context, industries such as healthcare, automotive, and finance face even stricter standards. Maintaining system efficiency and scalability adds operational burden. Apart from this, non-compliance can result in legal penalties and loss of customer trust, which makes regulatory management a major concern in IoT integration.

IoT Integration Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

31.8% |

|

Base Year Market Size (2025) |

USD 6.8 billion |

|

Forecast Year Market Size (2035) |

USD 81.6 billion |

|

Regional Scope |

|

IoT Integration Market Segmentation:

Deployment Mode Segment Analysis

The cloud-based, which is under deployment mode, is anticipated to garner the largest share of 76.8% in the IoT integration market over the forecasted duration. This strong position is efficiently driven by the scalability, flexibility, and cost-effectiveness, which enable data storage, processing, and integration across connected IoT devices. In July 2025, Siemens Smart Infrastructure entered into a partnership with Microsoft to enable interoperability between Building X and Azure IoT Operations by reducing integration efforts by up to 80%. It leverages standards such as W3C Thing Descriptions and OPC UA PubSub. The collaboration enhances IoT data accessibility across commercial buildings, data centers, and higher education facilities, thus solidifying the segment’s position in the IoT integration market.

Service Type Segment Analysis

System integration services, which are a part of the service type segment, are forecasted to grow at a noteworthy pace in the IoT integration market by the end of 2035. The increasing complexity of connecting diverse devices, platforms, and enterprise systems is the main factor behind the segment’s leadership. Organizations are deploying multi-vendor IoT ecosystems that require data flow and centralized control, which drives demand for specialized integration knowledge. In June 2025, AWS announced the general availability of managed integrations in IoT device management, which enables developers to onboard and manage diverse devices through a single unified interface. This supports ZigBee, Z‑Wave, Wi‑Fi, pre‑built cloud‑to‑cloud connectors, and over 80+ customizable device data model templates, and it streamlines IoT solution development, thus indicating an optimistic opportunity for the segment’s growth.

Enterprise Size Segment Analysis

By the end of 2035, the large enterprises in the IoT integration market are forecasted to witness considerable growth. The progression of the segment is mainly attributable to their financial capacity, advanced IT infrastructure, and ability to implement large-scale digital transformation initiatives. Also, these organizations are making heavy investments in IoT to enhance operational efficiency, enable predictive maintenance, and improve customer experiences. Apart from this, their global operations require real-time data integration across multiple locations, thereby driving demand for sophisticated IoT platforms. In addition, large enterprises are early adopters of technologies such as AI, digital twins, and advanced analytics. The presence of all of these factors responsibly uplifts the segment’s development in the IoT integration industry.

Our in-depth analysis of the IoT integration market includes the following segments:

|

Segment |

Subsegments |

|

Deployment Mode |

|

|

Service Type |

|

|

Enterprise Size |

|

|

Platform |

|

|

End use Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

IoT Integration Market - Regional Analysis

North America Market Insights

The North America IoT integration market is forecasted to be the dominant region, capturing the largest share of 40.5% during the stipulated timeframe. The region’s dominance is majorly propelled by strong enterprise IoT adoption, advanced cloud infrastructure, and early deployment of AI and edge computing. The region is also supported by large-scale investments from the U.S. and Canada in smart manufacturing, healthcare IoT, and industrial automation ecosystems. In September 2025, the National Institute of Standards and Technology’s study found that federal investments in IoT infrastructure could achieve a 10 to 20 times return, underscoring the technology’s economic and national security importance. It identified 11 strategic areas for research, and the study states that IoT supports AI while AI enhances IoT’s effectiveness, thus making it suitable for bolstering the region’s market growth.

An advanced technological infrastructure and a high concentration of hyperscale cloud providers and tech vendors are responsibly uplifting the IoT integration market in the U.S. Expansion is primarily driven by nationwide maturity of 5G standalone networks and the convergence of edge computing with artificial intelligence, enabling near-instant decision-making for autonomous logistics and high-speed industrial automation. In April 2026, the IoT M2M Council (IMC) reported that in the U.S., IoT policy is advancing through NIST’s finalized IR 8259 Rev. 1, which sets foundational cybersecurity standards for manufacturers to strengthen device security before reaching consumers. At the same time, federal and state initiatives, such as New York’s USD 10 million AI investment and DC’s launch of DC Compass, highlight IoT’s integration into smart city and innovation strategies. In addition, programs such as DOE’s USD 1.9 billion grid modernization funding further embed IoT into critical infrastructure, benefiting the overall IoT integration market growth.

In Canada, the IoT integration market is considerably growing, which is facilitated by significant investments in smart city initiatives across major urban centers, wherein these connected technologies are being deployed for intelligent transportation, waste management, and public safety. The agriculture, manufacturing, and energy sectors are identified as the primary adopters, which are utilizing integrated solutions for predictive maintenance and smart grid management. Based on government data published in February 2026, Canada is using IoT to strengthen agriculture by connecting weather stations in government fields to the cloud, to enable real-time data collection and analysis. The article also stated that this system provides farmers and researchers with reliable insights into crop science, climate resilience, and long-term planning. In addition, IoT is turning simple sensors into powerful tools, and is helping improve productivity and sustainability across the country’s agriculture.

APAC Market Insights

The Asia Pacific IoT integration market is projected to represent the fastest growth from 2026 to 2035. The region’s progress in this field is mainly due to a strong industrial base, where sectors such as manufacturing and automotive are aggressively adopting industrial IoT for end-to-end automation and supply chain optimization. In addition, the rising demand for smart healthcare solutions driven by aging populations and the adoption of precision agriculture in emerging economies is creating new growth opportunities for professional and managed integration services. As of the June 2025 data from the Infocomm Media Development Authority, Singapore is building a secure and interoperable IoT ecosystem through standards that were developed by IMDA and ITSC’s IoT Technical Committee. This SS 695:2023 is highly focused on interoperability for Smart Nation, whereas SS 711:2025 establishes foundational IoT security concepts and requirements. Therefore, together with the IMDA IoT Cyber Security Guide, these frameworks lower deployment costs and strengthen cybersecurity for businesses and consumers.

Large-scale coordination between industrial modernization programs and digital infrastructure rollouts is responsibly reshaping the growth dynamics of the IoT integration market in China. At the same time, logistics operators and port authorities are linking container tracking, fleet telematics, and warehouse management systems into shared data environments with the main goal to streamline high-volume export operations. Based on the government data published in March 2026, the country has set a target for its IoT industry to cross USD 505.8 billion by 2028, along with plans to reach 10 billion terminal connections. This action plan is highly structured around upgrading IoT devices, strengthening platforms, expanding applications, and building a robust network foundation. Apart from these advancements in sensing, networking, data processing, and security, these are expected to drive smarter, more innovative IoT systems in the country.

In India, the IoT integration market is gearing up for a transformative surge facilitated by the rapid nationwide rollout of 5G networks, by providing the low-latency infrastructure. This is highly essential for mission-critical applications in healthcare, such as remote patient monitoring, and in the automotive sector for smart fleet management. In addition, the ecosystem of domestic IT giants and specialized startups is fostering innovation through no-code, low-code platforms, making IoT integration even more accessible. In June 2025, an IMC article stated that the country’s IoT regulatory framework is anchored in the IT Act, and is strengthened by the SPDI Rules and the Digital Personal Data Protection Act, 2023, which together establish accountability for data security and privacy. At the same time, the complementary measures, such as the code of practice for securing consumer IoT devices, the IoT system certification scheme, and ITSAR standards, enforce security by design principles and mandatory certification for market access, thus fostering continued growth of the country’s market.

Europe Market Insights

The IoT integration market in Europe maintains a strong position, fostered by a high demand for industrial digitalization and a sophisticated regulatory environment. Expansion in the region is highly driven by Industry 4.0 initiatives in major manufacturing hubs, in which companies are integrating smart sensors and digital twins to optimize production and predictive maintenance. As per an article published by IMC in April 2026, Europe’s IoT policy landscape is being shaped by strong sovereign AI investment, tighter cybersecurity regulation, and expanding digital governance frameworks such as the Digital Networks Act and Cybersecurity Act 2, along with the UK’s Sovereign AI initiative. In terms of infrastructure, IoT adoption is heightening across energy, transport, and utilities, wherein major initiatives such as Poland’s battery storage funding, Spain’s NB-IoT smart water metering, and the regional AI-based grid optimization and ITS procurement. Governments are also focused on encouraging smart city and industrial IoT deployments through living labs, digital twins, and reindustrialisation programmes across Germany, France, and Estonia.

The widespread implementation of digital twins and remote asset monitoring significantly improves resource efficiency and production flexibility, which are certain factors driving the overall IoT integration market in Germany. The country’s market also benefits from a well-established ecosystem of domestic engineering giants such as Siemens, Bosch, and Infineon, along with a burgeoning startup scene focused on edge computing and cybersecurity for interconnected assets. In April 2023, Siemens, along with its eight other partners, showcased an interoperable digital twin using the asset administration shell standard at Hannover Messe 2023. The company also notes that by exchanging standardized component data, it enabled Bausch+Ströbel to build a digital twin of its labeling machine faster and more efficiently. Hence, this collaboration reflects the prominence of AAS in driving Industry 4.0 by simplifying engineering and fostering open ecosystems across both manufacturers and customers.

The IoT integration market in the UK is maintaining a strong position in the regional landscape owing to the rising adoption in sectors such as smart manufacturing, where connected sensors and digital twins optimize production lines, and healthcare, which utilizes remote patient monitoring and connected medical devices. In addition, government-backed initiatives such as the manufacturing made smarter program and investments in smart city infrastructure are bolstering the demand for professional integration services. Based on the government data published in February 2026, the phase 2 smart metering Internet of Things system project, which is led by Hildebrand with partners including DCC, University of Salford, and Utilita, reflects secure smart sensing of temperature and humidity via the smart meter network. In parallel, Octopus Energy’s project expands its ‘Octopus Home’ platform to connect IoT devices directly to the smart metering system, adding new sensors and certified security features, thus making it suitable for bolstering the overall country’s market growth.

Key IoT Integration Market Players:

- International Business Machines Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Cisco Systems, Inc. (U.S.)

- Oracle Corporation (U.S.)

- Hewlett Packard Enterprise Company (U.S.)

- Intel Corporation (U.S.)

- Google LLC (U.S.)

- Accenture plc (Ireland)

- Capgemini SE (France)

- Siemens AG (Germany)

- Robert Bosch GmbH (Germany)

- SAP SE (Germany)

- Iridium Communications (U.S.)

- Qualcomm (U.S.)

- Augentix (Taiwan)

- Arduino (Italy)

- Edge Impulse (U.S.)

- Focus.AI (U.S.)

- Foundries.io (UK)

- Netmore Group (Sweden)

- Actility (France)

- Schneider Electric SE (France)

- Hitachi, Ltd. (Japan)

- Fujitsu Limited (Japan)

- Samsung SDS Co., Ltd. (South Korea)

- Tata Consultancy Services Limited (India)

- Tech Mahindra Limited (India)

- Telekom Malaysia Berhad (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- International Business Machines Corporation has registered itself as a foundational player in the market, which is offering end-to-end solutions. The company is highly focused on industrial IoT, predictive analytics, and AI-based automation, enabling enterprises to connect and manage complex device ecosystems.

- Microsoft Corporation is yet another dominant force in the market, which offers scalable cloud services, device management, and advanced analytics. The firm deliberately enables seamless connectivity between edge devices and cloud environments by supporting industries such as healthcare, automotive, and smart cities.

- Amazon Web Services is a leading force in IoT integration, which is offering highly scalable cloud infrastructure and services such as AWS IoT Core and Greengrass. These platforms enable secure device connectivity, data processing, and some edge computing capabilities for millions of connected devices worldwide.

- Cisco Systems, Inc. is considered to be a key enabler of IoT integration through its networking infrastructure, cybersecurity solutions, and industrial IoT platforms. The firm is highly focused on secure connectivity across distributed IoT environments.

- Oracle Corporation contributes to IoT integration through its Oracle IoT Cloud platform, which supports device connectivity and enterprise analytics. Besides, the company integrates IoT data with its strong database and enterprise resource planning systems, thereby enabling organizations to gain actionable insights.

Below is the list of some prominent players operating in the global IoT integration market:

The IoT integration market is witnessing intense competition among technology and industry leaders. The U.S.-based hyperscalers such as Microsoft, AWS, IBM, Cisco, Oracle, HPE, Intel, and Google are dominating the cloud platforms, edge computing, and AI-driven IoT ecosystems. At the same time, Europe-specific firms such as Siemens, Bosch, SAP, Schneider Electric, Accenture, and Capgemini are highly focused on industrial automation, smart infrastructure, and consulting-led integration. Players are also making heavy investments in edge AI, interoperability, partnerships, and platform ecosystems. In January 2026, Netmore Group announced the acquisition of Actility, thereby creating the world’s largest LoRaWAN® network with more than 14 million contracted IoT devices and deployments across more than 100 countries, thus suitable for bolstering the overall IoT integration market growth.

Corporate Landscape of the IoT Integration Market:

Recent Developments

- In February 2026, Iridium Communications introduced the Iridium 9604, which is a compact IoT module that unifies satellite, cellular, and GNSS connectivity in one platform to reduce costs and simplify design for global deployments. It delivers dual‑mode IoT connectivity in Iridium’s smallest form factor.

- In January 2026, Qualcomm completed its IE‑IoT expansion by introducing new Dragonwing™ Q‑7790 and Q‑8750 processors, along with acquisitions of Augentix, Arduino, Edge Impulse, Focus.AI, and Foundries.io to power edge AI innovation. This unified ecosystem delivers scalable, secure, and developer‑friendly solutions.

- Report ID: 8554

- Published Date: May 04, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.