Intraspinal Abscess Treatment Industry - Regional Synopsis

North America Market Forecast

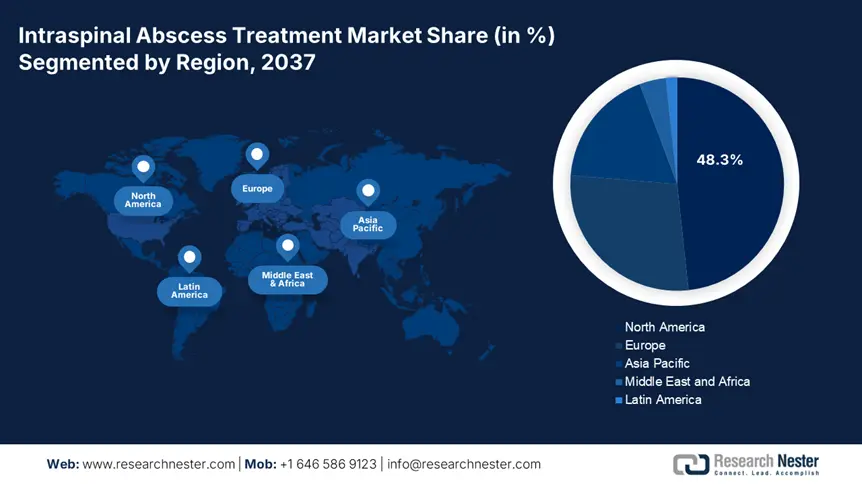

North America is poised to dominate the intraspinal abscess treatment market with a share of 48.3% throughout the discussed timeframe. This region is the origin of a large patient pool, pushing both public and private organizations to accommodate high-end solutions. For instance, in 2024, a CDC report calculated the number of new intraspinal abscess incidences in North America to be 45,030, representing a 9.4% rise from 2020. Its leadership is also attributable to Federal investments and technological advancements. For instance, till 2024, approximately 8.4% of the Federal Health Budget, totaling USD 3.4 billion, was dedicated to offering financial support to the spinal infection category in Canada. Similarly, in Ontario, a notable improvement in public access was observed by an 18.4% increment in spending from 2021 to 2024.

The U.S. is presenting a new scope of doing profitable business in the intraspinal abscess treatment market due to the widespread drug resistance among afflicted citizens. In this regard, the CDC reported that over 35.6% of cases from this particular patient pool in this country were resistant to methicillin, urging for alternatives. Additionally, the support from Medicare & Medicaid Services is significantly contributing to the nation’s recovery from the reimbursement gap by expanding their coverage in this category. For instance, in 2023, the net U.S. Medicare expenditure on intraspinal abscess treatment reached USD 850.4 million, saving USD 3200.4 out-of-pocket cost per patient. Furthermore, the nation’s spinal surgical device imports rose by 12.3% in 2024, attracting foreign forces to invest.

APAC Market Forecast

The Asia Pacific intraspinal abscess treatment market is projected to register the fastest growth by 2037. Several factors, such as the enlarging patient pool, investments in infrastructure, and favorable government initiatives, are driving the region’s remarkable pace of expansion and innovation in this sector. Its diverse demography and dynamics present a wide range of investment opportunities for both domestic and global pioneers. For instance, in Australia, the next-generation antibiotics segment is offering scope for garnering an annual sales value of USD 350.4 million from MSRA spinal infections. Simultaneously, South Korea and Malaysia are focusing on advanced surgical developments, such as minimally invasive techniques, to reduce the need for hospitalization expenses by 20.3%.

China is becoming a lucrative landscape of revenue generation for the intraspinal abscess treatment market due to the rising incidences of this ailment and the ambitious nationwide healthcare reformation. In this regard, the NMPA reported 1.7 million new diagnoses in 2023, among which, 25.4% received surgical treatment. Similarly, the country set its goals of doubling its neurological capacity by 2030, offering new opportunities for medical device suppliers with the potential to generate USD 1.3 billion in revenue. To obtain this level, China spent approximately 4.0 billion in 2024 on this category, demonstrating a notable 15.1% increase from 2019. This pathway is further fueled by proactive government participation in domestic API production escalation and accessibility enhancement.