Power Transformer Market Outlook:

Power Transformer Market size was valued at USD 27.5 billion in 2025 and is projected to reach USD 52.2 billion by the end of 2035, rising at a CAGR of 7.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of power transformer is estimated at USD 29.5 billion.

There is a huge opportunity for the market, since the demand for reliable and efficient electricity transmission is surging. Market expansion is also being fueled by the need to modernize aging power networks in major countries. Based on the government data from the U.S. in December 2024, the U.S. Department of Energy allocated more than USD 20 million to nine projects under its flexible innovative transformer technologies program with a primary goal to advance smart and solid-state transformer technologies for a more resilient and reliable electric grid. These projects include hybrid and solid-state transformer demonstrations by institutions such as Clemson University, GE Vernova, and the University of Pittsburgh, each of which will be receiving between USD 1.45 million and USD 2.99 million. Hence, such instances reflect the consistent efforts to modernize grid infrastructure and accelerate the adoption of transformer and power electronics technologies, positively impacting market growth.

DOE-Funded FITT Power Transformer Projects 2024: Funding, Organizations, and Key Innovations

|

Organization |

Project |

Funding (USD million) |

Description |

|

Clemson University (Clemson, SC) |

Smart Hybrid Transformer for Abnormal Power Events (SHAPE) |

2.47 |

Hybrid transformer with power electronics and battery storage |

|

Eaton Corporation (Menomonee Falls, WI) |

Compact and Reliable Voltage Regulating Hybrid Transformer |

2.94 |

Hybrid transformer for utility and industrial networks |

|

Electric Power Research Institute, Inc. (Palo Alto, CA) |

Solid State PowerHub Development and Demonstration |

2.88 |

Solid-state transformer for voltage stability |

|

Electric Research and Manufacturing Cooperative, Inc. (Dyerberg, TN) |

Distribution Transformer Extender (DTE) Project |

1.84 |

Combines solid-state transformer and small battery storage |

|

GE Vernova Operations LLC (Schenectady, NY) |

Full-scale AC Solid-State Transformer Demonstration (FASST) |

1.99 |

1 MVA 3-winding solid-state transformer demo |

|

GE Vernova Operations LLC (Schenectady, NY) |

Single-Phase Universal Spare Power Transformer for Grid Resilience |

2.99 |

Single-phase 2-winding transformer with solid-state tap changer |

|

Resilient Power Systems, Inc (Austin, TX) |

Direct Current-as-a-Service SolidFlex Power Hub |

1.47 |

Solid-state transformer for efficient power distribution |

|

Transforma Energy, Inc. (Albuquerque, NM) |

Drop-In Replacement Electronically Controlled Transformer (DIRECT) |

1.45 |

Solid-state transformer for multiple voltage/power ratings |

|

University of Pittsburgh (Pittsburgh, PA) |

Grid-Tied Testbed for Efficient, Flexible, Intelligent Distribution Transformers |

2.50 |

Testbed for next-gen intelligent distribution transformers |

Source: U.S. Department of Energy

Furthermore, capacity expansions to meet the rising demand are yet another asset for the power transformer market, stimulating consistent growth in domestic manufacturing and strengthening supply chain resilience. In this context, Pennsylvania Transformer Technology, LLC, in December 2025, announced a total of USD 102.5 million for the expansion of its manufacturing facilities in Raeford, North Carolina. This plan will create 217 new jobs and will add 300,000 square feet across two facilities by efficiently strengthening domestic production of power and distribution transformers for utility, municipal, renewable, and industrial sectors. In addition, the expansion aligns with North Carolina’s broader energy and industrial growth strategy, supported by recent large-scale investments from companies such as Scout Motors and Toyota, hence increasing the growth potential of the market in the years ahead.

Key Power Transformer Market Insights Summary:

Regional Highlights:

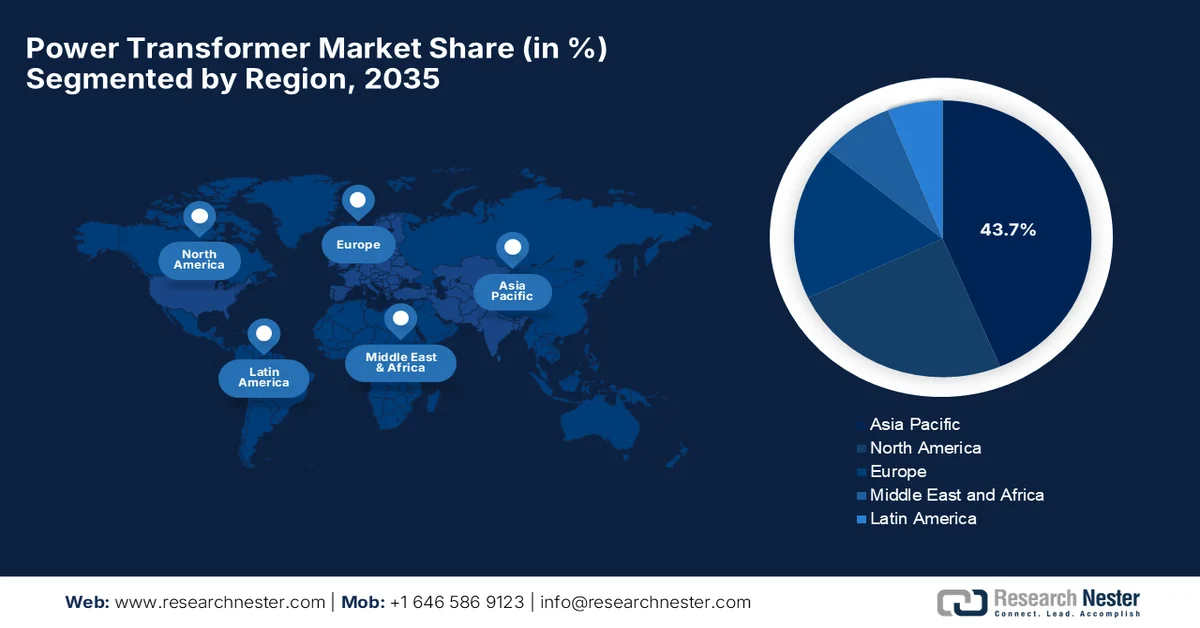

- By 2035, Asia Pacific is projected to command a 43.7% revenue share in the power transformer market, attributed to extensive grid expansions, stringent energy efficiency standards, renewable integration, and accelerating industrial demand.

- From 2026 to 2035, North America is expected to witness robust advancement in the power transformer market, fueled by large-scale replacement of aging transmission infrastructure and rising investments in grid automation and digital integration initiatives.

Segment Insights:

- By 2035, the Three-Phase segment is projected to account for a 66.6% share of the power transformer market, propelled by expanding electric transmission infrastructure relying on balanced high-capacity systems for efficient long-distance delivery.

- Throughout 2026–2035, the Oil-Insulated segment is expected to grow at a considerable rate, stimulated by rising grid modernization initiatives and renewable energy integration requiring high-capacity and thermally resilient transmission solutions.

Key Growth Trends:

- Rising global electricity demand

- Renewable energy integration

Major Challenges:

- Long lead times & high capital intensity

- Supply chain constraints and raw material volatility

Key Players: Hitachi Energy, GE Vernova, Siemens Energy, Schneider Electric, Mitsubishi Electric, Toshiba Energy Systems & Solutions, ABB Ltd., HD Hyundai Electric, TBEA Co., Ltd., China XD Electric Group, CG Power and Industrial Solutions, Bharat Heavy Electricals Limited, Voltamp Transformers Ltd., Transformers & Rectifiers India Ltd., Malaysia Transformer Manufacturing Sdn. Bhd., ECOTRAFO Energy, Hyosung Heavy Industries, Eaton Corporation, Howard Industries, Nissin Electric Co., Ltd.

Global Power Transformer Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 27.5 billion

- 2026 Market Size: USD 29.5 billion

- Projected Market Size: USD 52.2 billion by 2035

- Growth Forecasts: 7.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (43.7% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: - United States, China, Japan, Germany, India

- Emerging Countries: - South Korea, Brazil, Mexico, Saudi Arabia, Indonesia

Last updated on : 16 February, 2026

Power Transformer Market - Growth Drivers and Challenges

Growth Drivers

-

Rising global electricity demand: The sectors such as industrialization, urbanization, and increasing residential power consumption are the main factors driving demand for more reliable power infrastructure and transformer capacity. IEA in February 2026 reported that the worldwide electricity demand is projected to grow by more than 3.5% on a yearly basis by 2030, influenced by factors such as industrial electrification, EV adoption, data centers, and cooling needs. Meanwhile, renewables and nuclear are set to supply 50% of global electricity by the end of the decade. In addition, 2,500 GW of projects are currently stalled in connection queues worldwide, requiring regulatory reforms and grid-enhancing technologies to unlock capacity, hence denoting an optimistic opportunity for market growth.

Global Electricity Demand & Generation Trends Impacting the Power Transformer Market (2024)

|

Parameter |

2024 Global / Key Regions |

|

Global electricity demand growth |

4.3% |

|

Global electricity consumption increases |

1,080 TWh |

|

Electricity consumption by sector |

Buildings: >600 TWh |

|

China electricity consumption increases |

550 TWh / 7% |

|

Advanced economies electricity increase |

230 TWh |

|

Southeast Asia's electricity consumption growth |

>7% |

|

Global electricity generation growth |

+1,200 TWh |

|

Renewable generation growth |

Solar PV: 480 TWh |

|

Global installed capacity (renewables) |

Total: approximately 700 GW added |

|

Power mix shift |

Renewables + Nuclear = 40% of total generation |

|

Emerging market share (India, SE Asia) |

India: coal 75%, renewables >20% |

Source: IEA

- Renewable energy integration: There has been a structural shift towards renewable energy, which in turn necessitates transformers for interfacing variable generation with existing grids. These include step-up, HVDC (high‑voltage direct current) transformers, and flexible units that efficiently support grid integration of intermittent energy sources. In June 2025, Hitachi Energy stated that it will supply HVDC equipment for China’s Gansu–Zhejiang ±800 kV UHVDC transmission project, which is the world’s first-ever ultra-high voltage flexible direct current line. It is stretching 2,370 km, and will deliver 36 billion kWh annually to Zhejiang, meeting the power needs of nearly 34 million people, with over half sourced from renewables. In addition, the company’s technologies, i.e., converter transformers and semiconductors, will strengthen China’s grid resilience and support its energy transition, thereby making it suitable for market growth.

- Smart grid deployment: Utilities across the globe are opting for upgradations of their aging electricity networks into improved, digital grids, which is driving the growth of the power transformer market globally. This also includes installing smart transformers with more efficient features that reduce energy loss and maintenance costs. According to the article published by the Energy Group in May 2025 revamped distribution sector scheme in India is a major grid modernization initiative that will run through March 2026 by targeting the installation of 250 million prepaid smart consumer meters and mandating smart metering of all feeders as well as the distribution transformers. As of March 2025, about 1.95 lakh feeders (72.5%) had been sanctioned for smart metering, wherein 87,000 had been installed and charged. Hence, such initiatives are driving large-scale deployment of smart transformers and digital metering infrastructure to reduce aggregate technical & commercial losses.

Challenges

- Long lead times & high capital intensity: The market is witnessing obstacles in terms of extended manufacturing lead times and increased capital investments. Large power and extra high voltage transformers mostly require substantial investments in machinery, testing facilities, skilled labor, and quality control systems. In addition, transformers are specially engineered for certain grid requirements, which results in long design, production, and testing cycles. Therefore, these long lead times cause increased project risk, constrain supply responsiveness, and limit manufacturers’ ability to scale quickly during demand surges. Furthermore, in the case of utilities, these delayed deliveries can slow down grid expansion and renewable integration, whereas for manufacturers, working capital pressure has become a major operational challenge.

- Supply chain constraints and raw material volatility: The power transformer market is subject to supply chain disruptions and price volatility for raw materials such as copper, electrical steel, transformer oil, and insulation materials. Therefore, any fluctuations in terms of commodity prices directly impact manufacturing costs and margins, whereas shortages of grain-oriented electrical steel (GOES) have become a persistent bottleneck over recent years. The aspects of international logistics disruptions, geopolitical tensions, and trade restrictions also complicate the sourcing strategies, especially for cross-border projects. In order to address this, manufacturers need to balance cost control with both quality and compliance, which often involves locking in long-term supplier contracts.

Power Transformer Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

7.4% |

|

Base Year Market Size (2025) |

USD 27.5 billion |

|

Forecast Year Market Size (2035) |

USD 52.2 billion |

|

Regional Scope |

|

Power Transformer Market Segmentation:

Phase Segment Analysis

The three-phase subtype is anticipated to dominate the phase segment with the largest share of 66.6% in the power transformer market. The dominance is highly driven by electric transmission infrastructure, which uses balanced three-phase systems for high capacity and efficient long-distance delivery. These units are highly essential for high‑voltage transmission, industrial networks, and bulk power distribution. Bel Fuse Inc in November 2023 reported that its Signal Transformer division successfully expanded its 3PH Series of three-phase dry-type transformers by focusing on applications spanning medical, industrial, EV charging, lighting, and green energy sectors. It also notes that these transformers are permanently configured for a three-phase DELTA input and WYE output, for a balanced and efficient power delivery, hence highlighting the prominence of the sub-segment in supporting modern infrastructure and clean energy systems.

Insulation Type Segment Analysis

By the conclusion of the forecast period, the oil-insulated, which are based on the insulation type is predicted to grow at a considerable rate. These are widely used in high-capacity transmission and distribution since the fluid provides excellent cooling and dielectric properties, which sustain reliability in large utility networks. They are well-suited for high-voltage applications, where managing heat and maintaining insulation integrity is highly essential for continuous power delivery. In addition, the oil-insulated transformers offer longer service life and can have the capacity to handle overload conditions better than many dry-type alternatives. Since there has been a global push for grid modernization and renewable energy integration, demand for these high-capacity oil-insulated units is expected to rise over the forecasted years, making it suitable for the market growth.

Core Type Segment Analysis

The shell subtype is expected to garner a significant revenue share by 2035. The growth of the segment is mainly subject to its ability to provide compact geometry, reduced leakage flux, and strong mechanical support for high power units, making them suitable for utility and industrial applications. The electricity consumption in various sectors also necessitates these various core-type transformers. In September 2025, Hyosung Heavy Industries reported that it had secured more than KRW 200 billion (USD 150 million) in orders in 2025. The order is to supply 29 ultra-high voltage 765kV transformers, which use robust core and winding designs typical of shell or core configurations, reactors, along with 24 800kV circuit breakers for new transmission projects in the southern and eastern U.S. The company’s Memphis plant is the only U.S. facility that is capable of producing 765kV transformers, and is expanding capacity with investments to double production by 2026, thereby benefiting the power transformer market growth.

Annual Electricity Consumption Growth by Sector in 2023 and 2024 (TWh) -Buildings, Industry & Transport

![]()

Source: IEA

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Phase |

|

|

Insulation Type |

|

|

Core Type |

|

|

Power Rating |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Power Transformer Market - Regional Analysis

APAC Market Insights

The Asia Pacific power transformer market is expected to showcase unprecedented growth, capturing the largest revenue share of 43.7% by 2035. The region’s growth is mainly driven by massive grid expansions, energy efficiency standards, renewable integration, and industrial demand. In October 2023 Ministry of Economy, Trade, and Industry in Japan promulgated new energy efficiency standards for transformers used in buildings and factories. These standards have been set under the Act on the Rational Use of Energy, with the target of FY2026 for compliance, and cover 24 categories of transformers based on type, phase, frequency, capacity, and specification. In addition, these new standards are expected to improve transformer energy efficiency by 11.4% when compared to FY2019 levels, addressing losses that account for 2% to 3% of total transmitted energy, hence indicating a positive market opportunity.

FY2026 Japan Energy Efficiency Standards for Oil-Filled and Mold-Type Transformers - Target Values by Phase, Capacity, and Frequency

|

Type |

Number of Phases |

Rated Frequency |

Rated Capacity |

Specification |

Target Standard Value (E) |

|

Oil-filled |

Single-phase |

50 Hz |

Not more than 500 kVA |

Standard |

E = 9.34 × (kVA)^0.737 |

|

Oil-filled |

Single-phase |

60 Hz |

Not more than 500 kVA |

Standard |

E = 8.60 × (kVA)^0.744 |

|

Oil-filled |

Three-phase |

50 Hz |

Not more than 500 kVA |

Standard |

E = 14.5 × (kVA)^0.694 |

|

Oil-filled |

Three-phase |

50 Hz |

Beyond 500 kVA |

Standard |

E = 10.6 × (kVA)^0.797 |

|

Oil-filled |

Three-phase |

60 Hz |

Not more than 500 kVA |

Standard |

E = 14.4 × (kVA)^0.681 |

|

Oil-filled |

Three-phase |

60 Hz |

Beyond 500 kVA |

Standard |

E = 8.00 × (kVA)^0.825 |

|

Mold |

Single-phase |

50 Hz |

Not more than 500 kVA |

Standard |

E = 14.1 × (kVA)^0.685 |

|

Mold |

Single-phase |

60 Hz |

Not more than 500 kVA |

Standard |

E = 13.3 × (kVA)^0.692 |

|

Mold |

Three-phase |

50 Hz |

Not more than 500 kVA |

Standard |

E = 16.9 × (kVA)^0.699 |

|

Mold |

Three-phase |

50 Hz |

Beyond 500 kVA |

Standard |

E = 31.2 × (kVA)^0.659 |

|

Mold |

Three-phase |

60 Hz |

Not more than 500 kVA |

Standard |

E = 16.2 × (kVA)^0.702 |

|

Mold |

Three-phase |

60 Hz |

Beyond 500 kVA |

Standard |

E = 17.4 × (kVA)^0.742 |

|

Oil-filled |

Single-phase |

50 Hz |

Not more than 500 kVA |

Semi-standard |

E = (9.34 × (kVA)^0.737) × 1.10 |

|

Oil-filled |

Single-phase |

60 Hz |

Not more than 500 kVA |

Semi-standard |

E = (8.60 × (kVA)^0.744) × 1.10 |

|

Oil-filled |

Three-phase |

50 Hz |

Not more than 500 kVA |

Semi-standard |

E = (14.5 × (kVA)^0.694) × 1.10 |

|

Oil-filled |

Three-phase |

50 Hz |

Beyond 500 kVA |

Semi-standard |

E = (10.6 × (kVA)^0.797) × 1.10 |

|

Oil-filled |

Three-phase |

60 Hz |

Not more than 500 kVA |

Semi-standard |

E = (14.4 × (kVA)^0.681) × 1.10 |

|

Oil-filled |

Three-phase |

60 Hz |

Beyond 500 kVA |

Semi-standard |

E = (8.00 × (kVA)^0.825) × 1.10 |

|

Mold |

Single-phase |

50 Hz |

Not more than 500 kVA |

Semi-standard |

E = (14.1 × (kVA)^0.685) × 1.05 |

|

Mold |

Single-phase |

60 Hz |

Not more than 500 kVA |

Semi-standard |

E = (13.3 × (kVA)^0.692) × 1.05 |

|

Mold |

Three-phase |

50 Hz |

Not more than 500 kVA |

Semi-standard |

E = (16.9 × (kVA)^0.699) × 1.05 |

|

Mold |

Three-phase |

50 Hz |

Beyond 500 kVA |

Semi-standard |

E = (31.2 × (kVA)^0.659) × 1.05 |

|

Mold |

Three-phase |

60 Hz |

Not more than 500 kVA |

Semi-standard |

E = (16.2 × (kVA)^0.702) × 1.05 |

|

Mold |

Three-phase |

60 Hz |

Beyond 500 kVA |

Semi-standard |

E = (17.4 × (kVA)^0.742) × 1.05 |

Source: Ministry of Economy, Trade and Industry

The high-voltage and ultra-high-voltage transmission development has positioned China power transformer market at the forefront of regional development. Also, the country’s government is putting constant efforts in terms of clean electricity, whereas the emphasis on domestic production and technology localization has strengthened the industry and enabled faster rollout of UHV lines. Based on the government data from China, which was published in August 2024, its 2024 to 2027 action plan for a new electricity system, issued by the National Development and Reform Commission and the National Energy Administration, has the main priority towards clean energy transmission and grid modernization. In addition, this particular plan is looking forward to 455 million kW of wind and solar capacity in deserts by 2030, and will be upgrading coal plants for lower emissions. It also found that by the middle of 2024, electricity consumption rose 8.1% to 4.66 trillion kWh, and EV charging infrastructure expanded to 10.24 million units, underscoring the need for stronger distribution networks and hence increasing the growth potential for power transformers in the country.

The government-backed grid modernization and rural electrification initiatives are the main factors propelling the growth of the market in India. The designs that are capable of withstanding extreme weather and fluctuating loads are being deployed to improve grid reliability and reduce transmission losses in both urban and rural regions. In June 2025, Hitachi Energy India officially reported that it had secured a major order from Power Grid Corporation of India Limited to supply 30 units of 765 kV, 500 MVA single-phase transformers. The company also stated that these transformers will be manufactured at its Vadodara facility and will readily enhance bulk power transfer capacity, reducing transmission losses. Furthermore, this deployment supports the country’s energy transition, wherein the transformer demand has grown by 15% annually over the past two years, based on renewable integration and industrial electrification.

North America Market Insights

The North America power transformer market is highly driven by utilities, which focus on replacing aging transmission infrastructure. Advanced monitoring systems and grid automation initiatives are enhancing reliability while minimizing outages by fostering an increased adoption of transformers that support digital grid integration. As stated by the Governor of Georgia in November 2025, Virginia Transformer Corp. is anticipated to fund USD 40 million to facilitate its Georgia transformer facility expansion in Effingham County by creating more than 400 new jobs and retaining more than 800 existing positions. It also notes that the 250,000-square-foot plant produces large custom power transformers that will range from 30 MVA to 500 MVA at up to 525 kV by serving utilities, data centers, and renewable energy sectors. From a strategic perspective, such investments from governments will accelerate the region’s market development and strengthen local economic growth in the upcoming years.

The growth of renewable energy integration, which includes large-scale solar and wind farms are propelling the growth of the U.S. power transformer market. Also, the heightened transformer demand, coupled with federal incentives which are supporting clean energy adoption are accelerating the deployment of innovative transformer technologies. In March 2024, the National Renewable Energy Laboratory, which is funded by the U.S. Department of Energy, found that transformer capacity in the country needs to increase by 160% to 260% by 2050 when compared to 2021 levels. This is driven by the electrification of buildings, transportation, and industrial sectors, along with resilience programs and extreme weather impacts. It also notes that most of the nation’s transformers are owned by over 3,000 distribution utilities, and the study states there is an urgency to address supply chain shortages that have already led to two-year procurement delays and steep price hikes.

Investments in northern and remote communities with the main goal to improve grid stability and expanding electrification are rearranging the growth dynamics of the power transformer market in Canada. There has been a push for sustainable insulating materials in transformers, which reflects national concentration to reduce environmental impact. In September 2025, the Government of Canada notified that, through FedDev Ontario, it made a total investment of USD 6 million to support Northern Transformer Corporation’s new 183,000-square-foot large power transformer facility in Innisfil. Besides, this project will deliberately expand domestic transformer production capacity to meet rising demand from utilities, strengthen the country’s energy security, and support both grid modernization and electrification initiatives across North America, hence making it suitable for standard market growth.

Europe Market Insights

Europe power transformer market is anticipated to grow at a considerable rate from 2026 to 2035. The region’s market is majorly influenced by the transition to low-carbon energy systems. The region’s market also benefits from the integration of offshore wind farms and interconnectors across countries, which requires high-capacity transformers with enhanced cooling and voltage regulation features. Meanwhile, the policies on energy efficiency and carbon reduction are promoting the deployment of transformers that are designed for optimal performance and minimal environmental footprint. In April 2025 government of Ireland announced the launch of the Greenlink Interconnector, which is a 190 km subsea 500 MW HVDC cable linking Wexford and Pembrokeshire. It also notes that this particular project doubles Ireland’s interconnection capacity to 1 GW, strengthening energy security, grid resilience, and renewable integration.

The preference towards renewable integration and grid stability is the key factor behind the robust growth of the power transformer market in Germany. Both the domestic and foreign players operating in the country are expanding their production bases to meet the demand across the industrial and residential sectors. In addition, the country’s focus on research and development is also fostering advanced transformer technologies with improved efficiency. In September 2025, Siemens Energy notified that it made a total investment of €220 million (USD 235 million) to expand its transformer factory in Nuremberg, Germany, with the main goal boost production capacity by 50%. It is supported by up to €20 million (USD 21 million) in funding from Bavaria, whereas the expansion will add 16,000 square meters of new facilities, which is suitable for bolstering the market growth in the upcoming years.

The modernization of aging urban transmission networks and increasing electrification of transport are prompting a favourable business ecosystem for pioneers in the UK power transformer market. The country’s government focus on decarbonization and electrified mobility is also boosting the demand for transformers that support the energy infrastructure. In this regard, the UK government in November 2023 announced that it allocated £960 million (USD 1.2 billion) investment to accelerate green industries and reform the electricity grid. The package includes halving power line construction times from 14 to 7 years and cutting average grid connection delays from 5 years to just 6 months. Therefore, such supportive initiatives from the country’s government will boost the market growth by accelerating the demand for advanced transformers and creating new opportunities for manufacturers and service providers in the UK power sector.

Key Power Transformer Market Players:

- Hitachi Energy (Switzerland)

- GE Vernova (U.S.)

- Siemens Energy (Germany)

- Schneider Electric (France)

- Mitsubishi Electric (Japan)

- Toshiba Energy Systems & Solutions (Japan)

- ABB Ltd. (Switzerland)

- HD Hyundai Electric (South Korea)

- TBEA Co., Ltd. (China)

- China XD Electric Group (China)

- CG Power and Industrial Solutions (India)

- Bharat Heavy Electricals Limited (India)

- Voltamp Transformers Ltd. (India)

- Transformers & Rectifiers (India) Ltd. (India)

- Malaysia Transformer Manufacturing Sdn. Bhd. (Malaysia)

- ECOTRAFO Energy (Malaysia)

- Hyosung Heavy Industries (South Korea)

- Eaton Corporation (Ireland)

- Howard Industries (U.S.)

- Nissin Electric Co., Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Hitachi Energy is formed from ABB Power Grids and is now headquartered in Switzerland. The company is identified as an international leader in terms of high-voltage and extra-high-voltage transformers, HVDC systems, and grid automation solutions. Hitachi also has extensive manufacturing and service networks, with major capacity expansions and eco-efficient innovations that are efficiently supporting global electrification and decarbonization.

- Siemens Energy is one of the leading engineering groups originating from Germany, and it has a range of power transformers and grid equipment. The company mainly focuses on high-voltage transmission, digital transformer technology, and integrated grid solutions that allow it to maintain a stronger position in this field

- GE Vernova is the energy division of General Electric, and is a major U.S.-based player in power transformers, distribution systems, and grid solutions. The firm supplies a broad range of voltage classes for utilities and industrial customers and has been expanding its market presence through strategic investments and acquisitions.

- Mitsubishi Electric is yet another powerful player in this sector, which is offering power transformers, especially extra-high-voltage units for national grids and industrial applications. The company has strong engineering knowledge, and it focuses mainly on advanced insulation, thermal performance, and reliability in challenging environments.

- ABB Ltd is one of the long-established industrial technology firms, and is a major transformer manufacturer that has a strong international presence across distribution and high-voltage segments. In addition, the company deliberately emphasizes digitalization, energy efficiency, and smart grid integration, with solutions that span IoT, predictive maintenance, and low-loss materials.

Below is the list of some prominent players operating in the global power transformer market:

The global power transformer market hosts both multinational industrial players and specific regional manufacturers. Leading pioneers from the U.S., Europe, and Japan are focused on improved grid technologies, digital monitoring, and eco-efficient designs to meet heightened demand for renewable integration and smart grid applications. On the other hand, manufacturers from South Korea, China, India, and Malaysia concentrate on cost-competitiveness, expanding production capacity for high-voltage and extra-high-voltage transformers. In December 2025, AMSC reported that it had acquired Brazil-based Comtrafo for a combination of cash and equity valued at a total of USD 162 million, thereby expanding its power and distribution transformer portfolio for utility as well as industrial applications, which is suitable for uplifting the market growth.

Corporate Landscape of the Power Transformer Market:

Recent Developments

- In February 2026, Siemens Energy announced a total of USD 1 billion in investment in U.S. manufacturing to scale up the production of grid equipment, power transformers, and gas turbines, as there is a surging electricity demand from AI, data centers, and industrial electrification.

- In September 2025, Hitachi Energy announced an additional CAD 270 million (USD 195 million) investment to expand its large power transformer manufacturing facility in Varennes, Quebec, nearly tripling production capacity.

- In May 2025, GE Vernova reported that it had secured an order from POWERGRID to supply more than 70 units of 765 kV class extra high-voltage transformers and shunt reactors for renewable power transmission corridors across multiple states in India under the TBCB framework.

- Report ID: 5977

- Published Date: Feb 16, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.