Graphite Market Outlook:

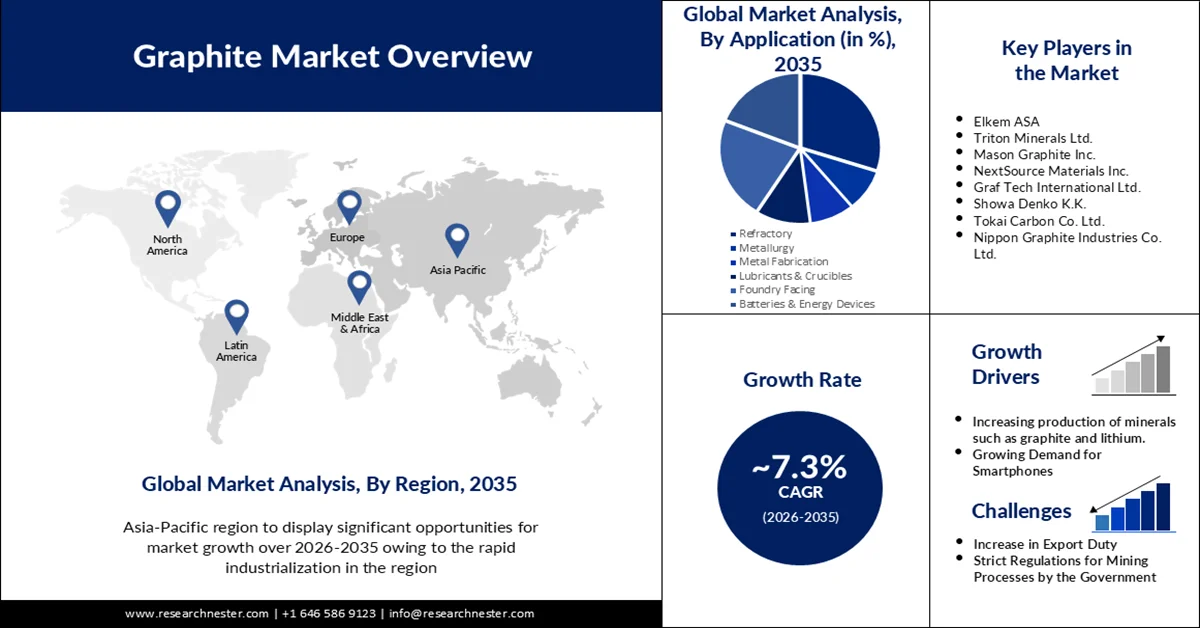

Graphite Market size was over USD 13.94 billion in 2025 and is poised to exceed USD 28.2 billion by 2035, witnessing over 7.3% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of graphite is estimated at USD 14.86 billion.

The graphite market growth is due to the increasing production of graphite globally to cater to rising demand from the automotive sector. Graphite mining is rising due to its usage in EV batteries. China was the largest graphite producer in 2023, with 1.23 million metric tonnes of production, according to the United States Geological Survey (USGS). China accounts for over 60% of global graphite production and many nations heavily rely on China’s supply chain for raw and refined graphite. This can be due to the rising usage of graphite in the production of lithium-ion batteries and other critical components of electric vehicles.

Top Exporters of Graphite in 2022

|

Country |

Export Revenue |

|

China |

USD 411 million |

|

Mozambique |

USD 89.9 million |

|

Madagascar |

USD 78.5 million |

|

Germany |

USD 35.4 million |

|

Brazil |

USD 30.4 million |

The demand for graphite is also increasing in the aerospace and defense sector. Graphite is commonly utilized in aerospace applications and lightweight composite parts for airplanes. In comparison to standard aircraft materials like metals and plastics, graphite has a high overall strength capacity. Several companies are also investing in developing graphite products and processing impacting the aerospace sector. In July 2023, Graphite One announced a 15% increase in their Graphite Creek Measured and Indicated Resource. This expansion underscores the rising need for high-quality graphite for aerospace and defense sector.

Key Graphite Market Insights Summary:

Regional Highlights:

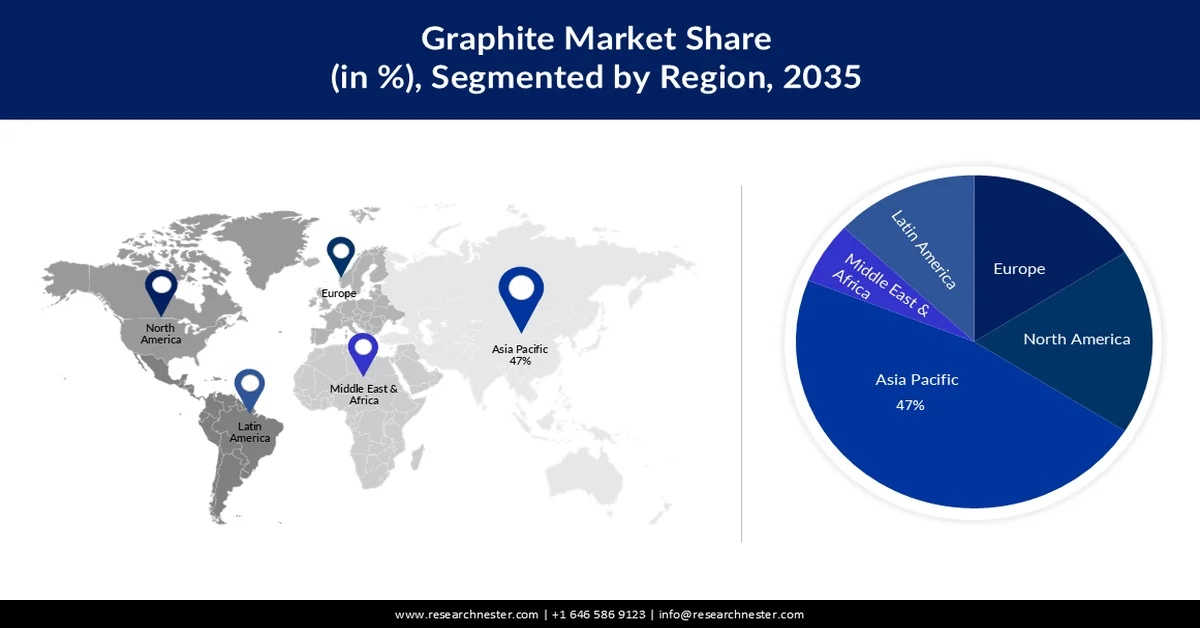

- The graphite market in Asia Pacific is anticipated to account for the largest revenue share of 47% by 2035, attributed to rising demand for consumer electronics and electric vehicles alongside rapid industrialization and growing graphite consumption from steel manufacturers.

- North America is projected to witness significant CAGR during 2026–2035, fueled by increasing electric vehicle production in the U.S. and Canada, strong demand from energy and consumer electronics sectors, and supportive government regulations promoting clean energy adoption.

Segment Insights:

- The synthetic graphite segment of the graphite market is projected to command a 60% share by 2035, propelled by its extensive utilization across friction materials, foundry applications, electrical carbons, fuel cell components, coatings, and drilling operations.

- The refractory segment is anticipated to secure a 30% revenue share by 2035, impelled by rising application of graphite as a refractory material supported by its superior heat resistance and expanding usage in iron and steel industries.

Key Growth Trends:

- Growing demand for smartphones and tablets

- Increasing demand for advanced electric battery technology

Major Challenges:

- Limited production in certain regions and challenges associated with mining

- Volatility in prices and rising focus on recycling

Key Players: Elkem ASA, Triton Minerals Ltd., Mason Graphite Inc., NextSource Materials Inc., National Minerals Information Center, AMG, Asbury Carbons, Grafitbergbau Kaisersberg GmbH, GrafTech International Ltd., Superior Graphite, Tirupati Carbons & Chemicals Pvt. Ltd.

Global Graphite Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 13.94 billion

- 2026 Market Size: USD 14.86 billion

- Projected Market Size: USD 28.2 billion by 2035

- Growth Forecasts: 7.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (47% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, Germany, Canada

- Emerging Countries: United States, Germany, Japan, South Korea, India

Last updated on : 25 February, 2026

Graphite Market - Growth Drivers and Challenges

Growth Drivers:

- Growing demand for smartphones and tablets: Graphite is increasingly used in designing and performing various electrical products, including smartphones. Its outstanding features enable the seamless integration of new technology into everyday life, such as powering smartphones and laptops via batteries, regulating heat, and being used in touchscreens. The rising demand for advanced smartphones and tablets with advanced processors, high-resolution screens, and 5G connectivity is set to propel the graphite market growth. According to a report, in 2022, around 1.39 billion smartphones were sold globally. This has resulted in growing demand for high-quality graphite. As smartphone designs are becoming thinner and lighter, the demand for high-thermal materials like graphite is rising, fueling overall market growth.

- Increasing demand for advanced electric battery technology: The transition towards green energy is likely to boost demand for better electric battery technology. Graphite is a vital component in graphite-anode battery designs because it can provide enormous storage and quick charging periods while maintaining high power. Further, technical developments in steel production employing calcined petcock or electric arc furnaces (EAF), as well as the emergence of battery-powered automobiles, are anticipated to have a substantial impact on the worldwide graphite market size.

Challenges:

- Limited production in certain regions and challenges associated with mining: Natural graphite production is concentrated only in certain areas across the globe such as China, Brazil, India, and Mozambique. This geographical dependency can expose the market to geopolitical risks and trade restrictions. Moreover, developing new graphite mines is capital-intensive and time-consuming due to regulatory requirements, environmental concerns, and fluctuating market demand.

- Volatility in prices and rising focus on recycling: Over the years, the demand for graphite has been increasing from several emerging sectors. This has resulted in rising concerns about supply chain fluctuations, causing volatility in prices. Traders in commodity markets add uncertainty, driving product prices. In addition, the development of recycling technologies for graphite used in batteries can be a potential threat to graphite miners.

Graphite Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.3% |

|

Base Year Market Size (2025) |

USD 13.94 billion |

|

Forecast Year Market Size (2035) |

USD 28.2 billion |

|

Regional Scope |

|

Graphite Market Segmentation:

Product Type Segment Analysis

The synthetic graphite market is poised to garner a 60% share by 2035, driven by its utilization in a variety of applications, including friction, foundry, electrical carbons, fuel cell bipolar plates, coatings, electrolytic processes, corrosion products, conductive fillers, rubber and plastic compounds, and drilling operations. The purity of natural graphite ranges from around 70.1% to 99.0%, while synthetic graphite purity is usually above 99.0%. According to a report by OEC, synthetic graphite was the world’s 617th most-traded product in 2022, with a total trade of USD 3.89 billion, and top exporters included, China (USD 1.84 billion), Germany (USD 256 million), Japan (USD 247 million), and U.S. (USD 205 million).

Application Segment Analysis

The refractory segment in the graphite market is estimated to gain a robust revenue share of 30% by 2035, impelled by the rising application of graphite as a refractory material, which is projected to grow soon due to its properties, such as heat resistance, stability, and high thermal properties. Furthermore, the growth of the segment can also be attributed to rapid industrialization and the increased use of graphite in the iron and steel industries. In a study, it was observed that in a steelmaking process, the tip of the electrode is heated up to 3,000 degrees Celsius. Electrodes are made of graphite since only graphite is capable of handling such intensive heat. In addition to that, nearly 70%-80% of the graphite electrodes are used in EAF steelmaking.

Moreover, graphite is also used as mold wash in several casting processes and facing sand by the foundry industry, which is counted as the second-highest use of this market. Ferrous castings account for the highest global share of many casting types, either by non-ferrous castings such as copper, aluminum, lead, zinc, magnesium, or titanium-based castings. The most popular uses for foundry-cast metals include automotive, pipelines, and machinery.

Our in-depth analysis of the global graphite market includes the following segments:

|

Product Type |

|

|

End use |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Graphite Market - Regional Analysis

APAC Market Insights

The graphite market in Asia Pacific industry is likely to hold the largest revenue share of 47% by 2035 owing to increasing demand for consumer electronics and electric vehicles, rapid industrialization in countries such as China, India, South Korea, and Japan, and increasing demand for graphite from steel manufacturers. China dominates the market due to its abundant natural graphite resources, low production costs, and rising demand across several industries.

China is the world's largest consumer and producer of graphite electrodes. Based on USGS data, China produced 820,000 tons of graphite in 2021; this number increased to approximately 1.25 million tons in 2023. This accounts for 79% of the world's graphite production. China is also a significant producer of synthetic graphite, often used in high-tech applications, including lithium-ion batteries. In addition, the favorable government regulations to manage the environmental impacts of graphite mining and optimize resource use are expected to support market growth going ahead.

The graphite market in India is expected to register rapid growth during the forecast period. This growth can be attributed to rapid urbanization, increasing sales of electric vehicles, and growing domestic demand for steel, batteries, and electronics. India holds significant graphite reserves, estimated at around 11 million tonnes in Jharkhand, Odisha, Tamil Nadu, and Arunachal Pradesh. In addition, it exports raw or semi-processed graphite and according to the OEC, it exported USD 170K in natural graphite in 2022.

North America Market Insights

The North America graphite market is expected to register significant CAGR between 2026 and 2035, propelled by increasing production of electric vehicles in the U.S. and Canada, high demand for graphite in energy and consumer electronics applications, and government norms to promote clean energy and reduce carbon emissions. In addition, the presence of industry giants and tremendous investments in research and development activities to increase graphite production is expected to fuel market growth during the forecast period.

The U.S. currently has minimal natural graphite production, relying heavily on imports to meet its industrial needs. However, to reduce the dependence on imports, the country is investing in synthetic graphite production. For instance, Novonix, an Australian company is constructing a large-scale synthetic graphite factory in Chattanooga with a conditional loan of USD 755 million from the U.S. Department of Energy. The company aims to supply graphite for 3,25,000 EVs by 2028.

In 2022, Canada exported USD 22 million worth of natural graphite and USD 14 million of synthetic graphite, primarily to the U.S. The graphite market is rapidly expanding due to rising EV production, high focus on renewable energy storage, and strong government support. In addition, rising investments in enhancing graphite production capabilities and increasing applications of graphite across several sectors are expected to boost market growth in the country.

Graphite Market Players:

- Imerys Graphite & Carbon

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Elkem ASA

- Triton Minerals Ltd.

- Mason Graphite Inc.

- NextSource Materials Inc.

- National Minerals Information Center

- AMG

- Asbury Carbons

- Grafitbergbau Kaisersberg GmbH

- Graf Tech International Ltd.

- Superior Graphite

- Tirupati Carbons & Chemicals Pvt. Ltd.

The global graphite market is highly competitive and dynamic, shared by key players, regional influences, technological advancements, and demand from end use industries such as batteries, refractories, and lubricants. The key players in the market are adopting several strategies such as mergers and acquisitions, partnerships, product launches, and license agreements to sustain their market position and enhance their product base. Here are some key players operating in the global graphite market:

Recent Developments

- In July 2024, Hycamite, a global hydrogen producer announced the launch of graphite production with a low-carbon footprint that can be used in EV batteries. The company’s novel methane-splitting technology provides low-carbon hydrogen and high-quality carbon products.

- In September 2024, Aurubis and Talga announced a partnership to develop battery-grade recycled graphics. The partnership aims to extend the Talga technology to all Aurubis graphite feed material via closer collaboration between both companies.

- In October 2024, South Star Battery Metals Corp announced the launch of its first product at its Santa Cruz Phase 1 Graphite Mine in Bahia, Brazil. The company aims to produce 25,000 tonnes in 2026 and 50,000 tonnes in 2028.

- n October 2024, Northern Graphite and Rain Carbon announced the agreement to jointly develop and commercialize advanced natural graphite-based Battery Anode Material. The new materials are expected to improve the performance of natural versus synthetic graphite-based battery anode materials.

- In November 2024, NOVONIX Limited and PowerCo SE announced the signing of a binding offtake agreement for a minimum of 32 thousand tons of high-performance synthetic graphite material. NOVONIX Limited will supply the materials over a five-year term starting in 2027.

- Report ID: 181

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.