Chatbot Market Outlook:

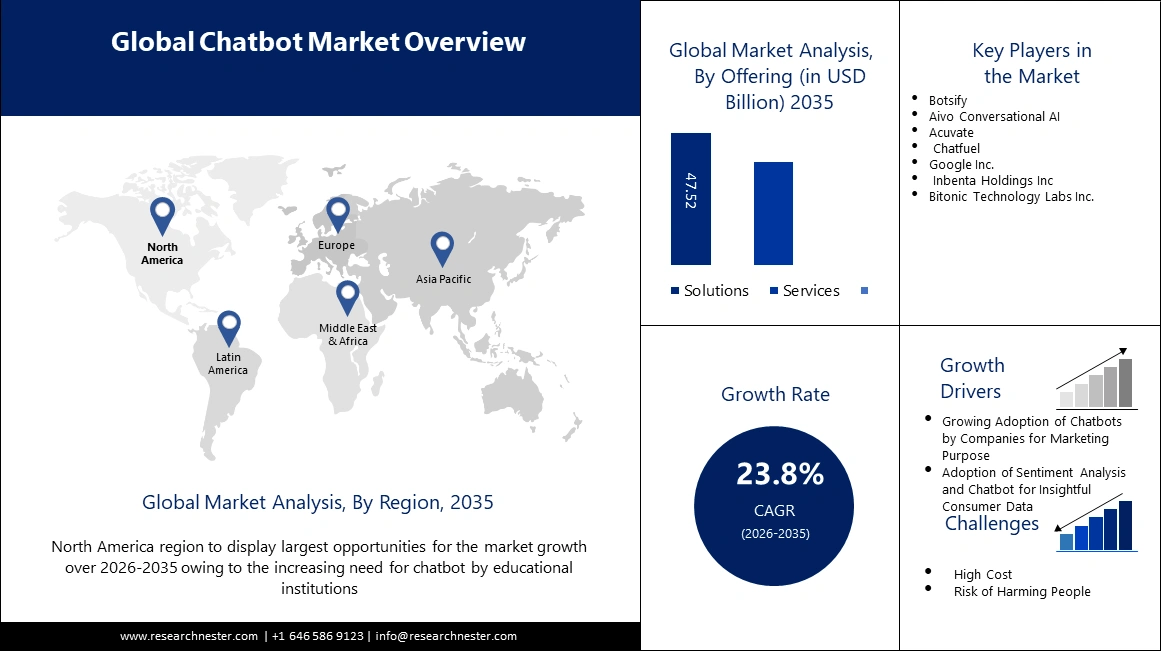

Chatbot Market size was valued at USD 8.57 billion in 2025 and is set to exceed USD 72.47 billion by 2035, registering over 23.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of chatbot is estimated at USD 10.41 billion.

The main purpose of chatbots, which use computer programs to mimic human responses, is to reduce the cost of hiring human customer service representatives. Financial institutions have recently begun experimenting with natural language processing, neural networks, and generative machine learning to automatically generate chat responses that can be spoken or written as text. Additionally, financial institutions are increasingly turning to chatbots as they offer a more cost-effective alternative to human customer support. For example, Bank chatbots will be used by more than 98 million users in 2022, representing more than 37% of the US population. By 2026, the number of users worldwide is expected to reach 110.9 million.

A practical and effective way to communicate with your customers is chatbot software. It acts as a resource for a variety of needs, including providing customer service and general information. The ideal chatbot software should have a dashboard that provides consumers with all the necessary details about the bot. This includes information about the bot's demographics, engagement, and performance. Additionally, you should provide easy-to-use tools to create new bots and monitor their activity. Additionally, it should provide comprehensive reporting on every possible topic, such as visitor engagement and sales conversion rates.

Key Chatbot Market Insights Summary:

Regional Highlights:

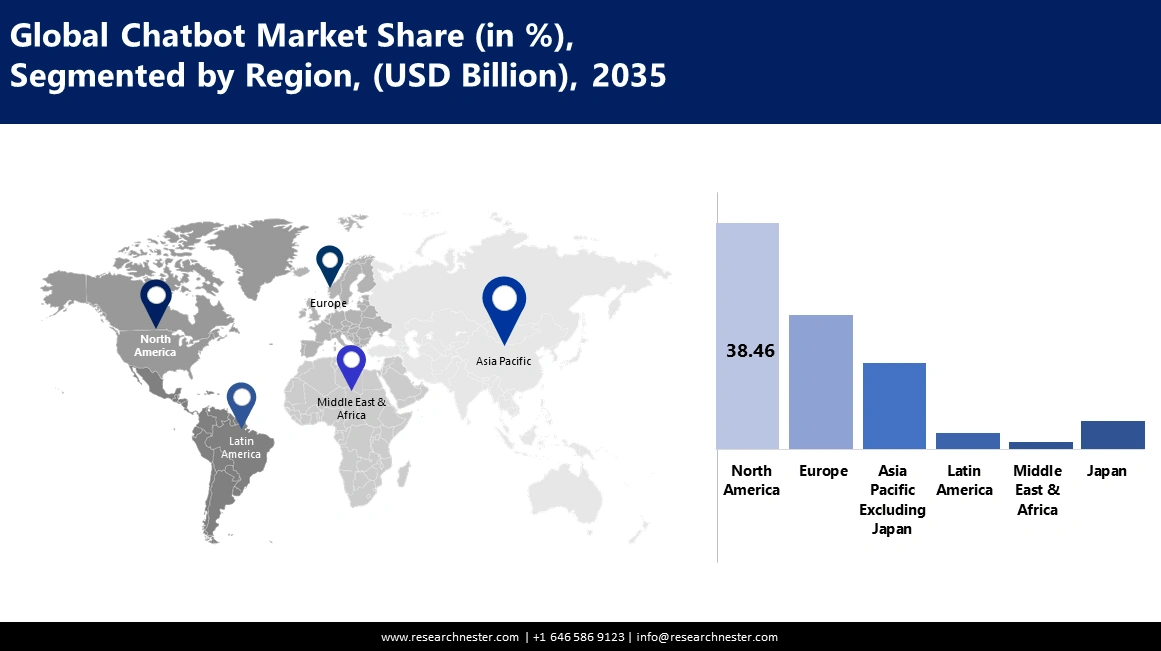

- North America chatbot market will hold more than 34% share by 2035, driven by chatbot integration in education improving experience and engagement.

- Europe market will secure 27% share by 2035, fueled by automation in contact centers offering better customer support.

Segment Insights:

- The solutions segment in the chatbot market is projected to achieve a 56% share by 2035, fueled by the introduction of innovative chatbot solutions aiding retail and e-commerce operations.

- Cloud segment in the chatbot market is projected to achieve 54% growth by the forecast year 2035, influenced by the scalability, adaptability, and 24/7 accessibility offered by cloud-hosted chatbots.

Key Growth Trends:

- Automation of Accounting Process by Using AI Chatbots

- Adoption of Sentiment Analysis and Chatbot for Insightful Consumer Data

Major Challenges:

- Automation of Accounting Process by Using AI Chatbots

- Adoption of Sentiment Analysis and Chatbot for Insightful Consumer Data

Key Players: of Botsify, Aivo Conversational AI, Acuvate, Chatfuel, Google Inc., Inbenta Holdings Inc, Bitonic Technology Labs Inc.

Global Chatbot Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 8.57 billion

- 2026 Market Size: USD 10.41 billion

- Projected Market Size: USD 72.47 billion by 2035

- Growth Forecasts: 23.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (34% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, India

- Emerging Countries: China, India, Singapore, South Korea, Malaysia

Last updated on : 16 September, 2025

Chatbot Market Growth Drivers and Challenges:

Growth Drivers

-

Automation of Accounting Process by Using AI Chatbots - There are many ways to facilitate online transactions, including UPI processing, ScanPay technology, net banking, and dedicated mobile applications. However, that number is very different today than it was a year ago. A lot has changed in recent years. This can be mainly explained by the fact that modern consumers want a seamless trading experience. User preference for digital payments will only increase as digitalization facilitates quick connections. Regardless of how a user uses their smartphone or card, digital payments have many additional benefits, such as smoother bill processing and easier product purchases. The development of digital payment solutions such as AI chatbots will further streamline the payment process and make it even more convenient.

-

Adoption of Sentiment Analysis and Chatbot for Insightful Consumer Data - Chatbot services can incorporate sentiment analysis technology to respond more effectively to consumers and improve their experience. By examining the polarity of sentences, companies can assess consumer satisfaction with their services and the effectiveness of their methods.. Sentiment analysis techniques can be successfully integrated into chatbots in any industry that interacts with customers, including finance, healthcare, insurance, real estate, and retail.

Challenges

-

Risk of Harming People - In markets for consumer financial products and services, chatbots have the potential to cause significant damage both in terms of loss of customer confidence as well as on account of their failure. There are serious consequences to making a mistake when someone's financial security is at stake. The ability to detect and manage consumer disputes, which is often the only feasible way of quickly correcting mistakes before they get out of hand, constitutes an important element.

-

Risk of Violating Federal Laws Associated with Consumer Finance is Expected to Hamper the Market Growth in the Forecast Period

- Limited Capabilities of Chatbot are Set to Restrict the Market Growth in the Upcoming Period

Chatbot Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

23.8% |

|

Base Year Market Size (2025) |

USD 8.57 billion |

|

Forecast Year Market Size (2035) |

USD 72.47 billion |

|

Regional Scope |

|

Chatbot Market Segmentation:

Offering Segment Analysis

In terms of offering, the solutions segment share in the chatbot market is predicted to surpass 56% by the end of 2035. Chatbot solutions are services aimed at solving common or specific problems related to the application of personalized products, such as Software, Applications, and Web Platforms. The introduction of new chatbot solutions in the global market is expected to drive the growth of the chatbot solutions segment during the forecast period. Such as, Kore.ai introduced his RetailAssist, his solution for a conversational retail sales assistant, at the National Federation of Retailers trade show in New York City in January 2023. RetailAssist helps retail and e-commerce companies modernize their operations by developing expertise in self-service automation, customized omnichannel fulfillment, and 24/7 pre- and post-sales assistance and support. They support expansion and transformation.

Deployment Mode Segment Analysis

Based on deployment mode, the cloud segment is set to hold 54% chatbot market share by 2035. Cloud chatbots are hosted on third-party cloud servers, easily accessible over the internet, and can be scaled up or down as needed. Chatbots deployed in the cloud have many benefits, including scalability, adaptability, and access to different platforms and devices such as desktops, tablets, and mobile devices. Moreover, these chatbots are accessible 24/7, so your website visitors and customers can access them from anywhere at any time. Additionally, cloud chatbots offer various cost subsidies, such as reduced maintenance costs and subscription-based pricing models.

Our in-depth analysis of the global chatbot market includes the following segments:

|

Offering |

|

|

Type |

|

|

Deployment Mode |

|

|

Technology |

|

|

Organization Size |

|

|

Application |

|

|

End User |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Chatbot Market Regional Analysis:

North American Market Forecast

The chatbot market share in the North America region is anticipated to reach 34% by the end of 2035. Chatbots are used by educational institutions in the region to improve the student experience and speed up administrative tasks. These chatbots assist with course registration and answer frequently asked questions. Additionally, it provides youth with the knowledge they need to have a smoother academic experience. Chatbot integration increases student productivity and engagement in the education industry in the North America region.

European Market Statistics

The Europe chatbot market is set to account for 27% revenue share by 2035. The combination of chatbots and humans is ushering in a new era of fully automated contact centers, with unprecedented efficiency and consistency, even as human interfaces remain essential for sensitive and complex conversations. They promise a great customer support experience in the region. However, chatbots rely on user data to operate, so there are concerns about data collection methods and privacy. Without proper cybersecurity measures in place, chatbots can leak sensitive user data. For example, in April 2023, the European Data Protection Board authorized the establishment of a task force of EU data protection authorities to coordinate the implementation of ChatGPT.

Chatbot Market Players:

- Creative Virtual

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- eGain Corporation

- IBM Corporation

- Botsify

- Aivo Conversational AI

- Acuvate

- Chatfuel

- Google Inc.

- Inbenta Holdings Inc

- Bitonic Technology Labs Inc.

Recent Developments

In The News

- May 2023 A new advanced version of VOn Person, Gluon, has been released by CREATIVEVIRTUAL. Gluon's user interface is more intuitive, and it's more natural. It provides support to LLMs, GPTs, Vportals and more.

- Google will release Bard's chatbot in March 2023, with even more capabilities and advances. Its competitor Microsoft will gain a competitive advantage with this release. The Bard service will initially be available in the United States and the United Kingdom and will be expanded to other users and countries in due course.

- Report ID: 5567

- Published Date: Sep 16, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Chatbot Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.