Flip Chip Market Outlook:

Flip Chip Market size was valued at USD 41.2 billion in 2025 and is projected to cross USD 79.5 billion by the end of 2035, expanding at more than 6.8% CAGR during the forecast period i.e., 2026-2035. In 2026, the industry size of flip chip is evaluated at USD 44.1 billion.

The flip chip market is closely tied to broader semiconductor packaging demand, which continues to expand in response to high-performance computing, automotive electronics, and advanced communications infrastructure. According to the Semiconductor Industry Association (SIA), February 2024 data, global semiconductor sales reached USD 526.8 billion in 2023, with advanced packaging increasingly accounting for a larger share of backend manufacturing value due to rising chip complexity and heterogeneous integration requirements. The PIB March 2026 data indicates that the government has approved more than 29 proposals under the electronics component manufacturing scheme, reflecting its growing economic significance within the semiconductor value chain. Government-backed initiatives, such as the U.S. CHIPS and Science Act, allocate over USD 52 billion in funding as per the HAI August 2022 data, with a defined portion directed toward packaging innovation programs, reinforcing supply chain localization and capacity expansion for technologies such as flip-chip interconnects.

Besides, India’s semiconductor expansion provides a strong foundation for growth in advanced packaging segments such as flip-chip. According to the Invest India February 2026 data, the domestic semiconductor market is projected to exceed USD 100 billion by 2030, up from USD 38 billion in 2023. Demand for high-performance packaging solutions is expected to increase alongside growth in AI, automotive electronics, and telecom infrastructure. Government-backed investments under the USD 9.3 billion India Semiconductor Mission are accelerating the development of fabrication units, OSAT facilities, and supply chain ecosystems, all of which directly support flip-chip adoption. As global supply chains diversify, India’s emergence as a manufacturing and packaging hub is set to strengthen regional capacity for advanced interconnect technologies, reinforcing steady demand across industrial and electronics sectors.

Key Flip Chip Market Insights Summary:

Regional Highlights:

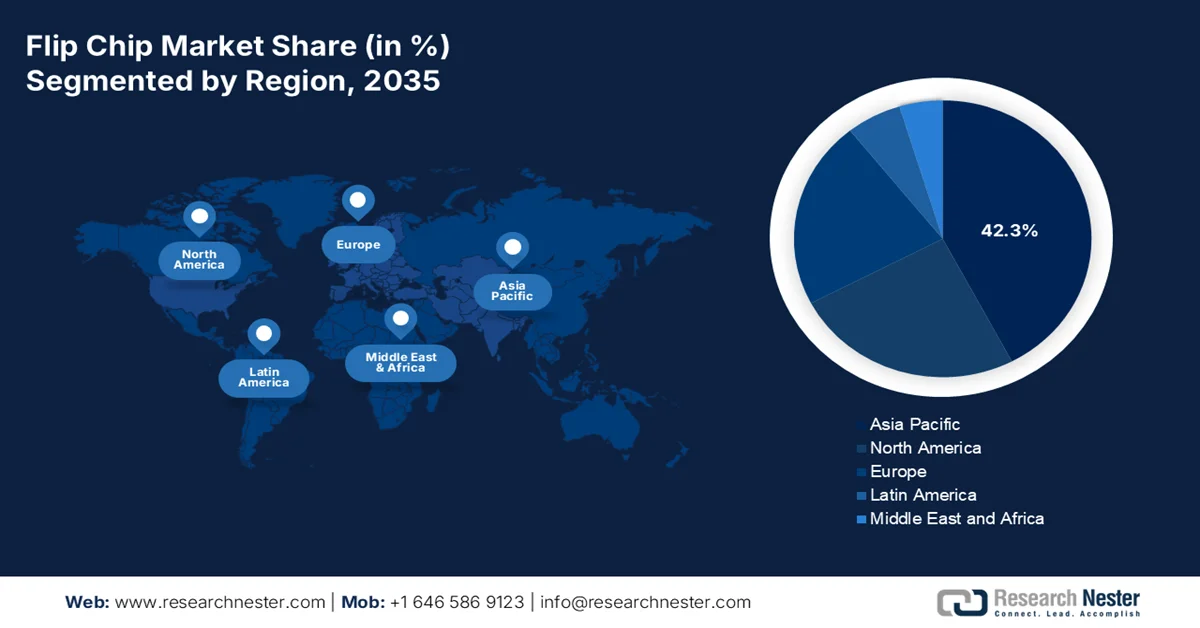

- The Asia Pacific is projected to account for 42.3% of regional revenue share by 2035, impelled by strong demand for consumer electronics, memory semiconductors, and mobile processors alongside large-scale advanced packaging capabilities

- North America is anticipated to witness the fastest growth in the flip chip market with a CAGR of 9.5% during 2026–2035, attributed to increasing investments in domestic advanced packaging capacity and secure semiconductor supply chains for AI and high-performance computing

Segment Insights:

- In the flip chip market, the 300mm wafer size sub-segment is anticipated to capture 68.4% share by 2035, propelled by superior die per-wafer economics and compatibility with advanced packaging nodes

- Foundry & IDM (Integrated Device Manufacturer) is expected to maintain its leading position in the end user industry segment throughout 2026–2035, fueled by the growing need for in-house control over advanced 2.5D and 3D flip-chip packaging processes

Key Growth Trends:

- Electrification and EV policy incentives

- Telecommunications infrastructure and 5G deployment

Major Challenges:

- Extreme technological complexity

- Severe capacity bottlenecks and supply-demand imbalance

Key Players: TSMC, Samsung Electronics, Intel Corporation, ASE Group, Amkor Technology, JCET, Powertech Technology Inc., STATS ChipPAC, Texas Instruments, Renesas Electronics, Sony Semiconductor, Toshiba Corporation, Infineon Technologies, STMicroelectronics, NXP Semiconductors, Micron Technology, Analog Devices, ASE, Indium Corporation, Daktronics.

Global Flip Chip Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 41.2 billion

- 2026 Market Size: USD 44.1 billion

- Projected Market Size: USD 79.5 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: Taiwan, South Korea, United States, China, Japan

- Emerging Countries: Malaysia, Canada, Germany, France, India

Last updated on : 14 May, 2026

Flip Chip Market - Growth Drivers and Challenges

Growth Drivers

- Electrification and EV policy incentives: Government incentives for electric vehicles are accelerating semiconductor demand, particularly for power electronics and advanced driver assistance systems, where flip-chip packaging is widely used. The International Energy Agency (IEA) May 2025 data reports that global EV sales exceeded 14 million units in 2023, supported by subsidies and policy frameworks across the U.S., EU, and China. Programs such as the U.S. Inflation Reduction Act provide tax credits and funding for EV adoption and domestic manufacturing, indirectly boosting semiconductor demand. EVs require significantly more semiconductors than internal combustion engine vehicles, increasing the need for compact and thermally efficient packaging. Flip-chip technology supports high-reliability automotive applications, including battery management systems and power modules. For suppliers, automotive electrification represents a long-term growth driver with predictable policy backing. As governments tighten emission regulations, semiconductor content per vehicle is expected to rise, sustaining demand for advanced packaging solutions.

- Telecommunications infrastructure and 5G deployment: Government-backed 5G infrastructure programs are driving demand for high-frequency semiconductor packaging where flip-chip plays a critical role. The NTIA, July 2025, and other agencies have allocated billions for broadband and 5G expansion, including the USD 42.45 billion Broadband Equity Access and Deployment (BEAD) Program. Similarly, the European Union’s Digital Decade policy aims for full 5G coverage by 2030, supported by public funding and regulatory frameworks. 5G base stations and network equipment require advanced RF components with high performance and thermal efficiency, making flip-chip a preferred packaging solution. The telecom infrastructure offers large-scale, government-backed procurement opportunities. The shift toward 6G research already supported by public funding in multiple regions is expected to further increase demand for advanced semiconductor packaging technologies over the next decade.

- Medical device digitization spending: Government healthcare investments are increasing the demand for miniaturized and high-performance semiconductor components used in medical devices, many of which rely on flip-chip packaging. Advanced diagnostic equipment, wearable devices, and imaging systems require compact, efficient chips, making flip-chip a suitable packaging solution. Public funding for healthcare infrastructure modernization, particularly in Europe and Asia, is accelerating the adoption of electronics-intensive medical devices. For suppliers, this segment offers stable demand supported by government budgets rather than consumer cycles. As healthcare systems invest in digital transformation and remote monitoring technologies, semiconductor packaging requirements are expected to become more advanced, reinforcing the role of flip-chip in medical electronics.

Challenges

- Extreme technological complexity: Flip chip technology requires specialized expertise in bumping underfill, thermal management, and alignment precision measured in microns. Manufacturers must master copper pillar solder bump and hybrid bonding techniques while maintaining yields. The learning curve is steep, and experienced engineers are scarce. New players often struggle with the die placement accuracy, warpage control, and interconnect reliability. Top companies have invested years of R&D in advanced packaging technologies, including EMIB and Foveros, holding patents and publishing papers. This demonstrates the deep long-term expertise required.

- Severe capacity bottlenecks and supply-demand imbalance: The AI boom has created unprecedented demand for the 2.5D flip chip packaging, mainly CoWoS. TSMC has struggled to keep pace with the orders from the other AI chip designers, leading to allocation shortages and extended lead times. New players face the challenge of building capacity in an environment where every available tool is already committed. Though the market is expected to expand, the capacity crunch creates opportunities but requires massive simultaneous investment.

Flip Chip Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 41.2 billion |

|

Forecast Year Market Size (2035) |

USD 79.5 billion |

|

Regional Scope |

|

Flip Chip Market Segmentation:

Wafer Size Segment Analysis

In the flip chip market, the 300mm wafer size is the dominant sub-segment in the wafer size segment and is poised to hold the share value of 68.4% by 2035. The segment is driven by its superior die per-wafer economics and compatibility with advanced packaging nodes. According to SEMI's March 2023 data, the global 300mm fab capacity is forecast to reach an all-time high of 9.6 million wafers per month by 2026, despite a temporary slowdown in 2023 due to soft memory and logic device demand. This expansion directly benefits flip-chip manufacturing as 300mm wafers enable finer copper pillar bumps and higher I/O densities required for AI HPC and automotive ADAS applications. Leading foundries and IDMs continue retiring older 200mm lines in favor of 300mm for 2.5D and 3D flip-chip processes. The sustained capacity build-out ensures that 300mm remains the preferred substrate size for high-volume flip-chip assembly through 2035.

End user Industry Segment Analysis

The end user industry segment of the market is led by the foundry & IDM (Integrated Device Manufacturer) sub-segment. This dominance arises from the strategic need to control advanced packaging processes in-house. Foundries such as TSMC and global IDMs like Intel integrate flip-chip assembly directly into their semiconductor manufacturing workflows to protect proprietary designs, reduce latency, and optimize chiplet-based architectures for high-performance computing. By keeping critical 2.5D and 3D flip-chip technologies within their own facilities, these players achieve tighter process integration, faster time to market, and better thermal and electrical performance compared to outsourcing. This captive model ensures that the most advanced flip-chip interconnects remain exclusive to their latest nodes, reinforcing their competitive moat against third-party OSATs. As heterogeneous integration becomes standard, Foundry & IDM leadership continues to strengthen, shaping the entire flip-chip supply chain.

Bump Type Segment Analysis

Copper pillar bumps is leading the bump type segment in the market. The segment relies heavily on surface finish quality for reliable thermo-compression bonding. As per the NLM February 2023 study evaluating Cu/SnAg pillar bumps on electroless palladium immersion gold (EPIG), found that EPIG’s surface roughness (82 nm) was 1.6 times higher than ENEPIG, due to EPIG’s inability to flatten rough bare Cu pads. Consequently, cross-sectional SEM revealed significantly higher filler trapping in TC‑bonded EPIG samples, attributed directly to the increased roughness. After 1500 thermal cycles, contact resistance rose 26% more for the EPIG sample than for ENEPIG. This demonstrates that while copper pillar bumps enable ultra‑fine pitch interconnects, sub‑optimal surface finishes like EPIG can degrade long‑term reliability by increasing resistance drift under thermal stress.

Our in-depth analysis of the flip chip market includes the following segments:

|

Segment |

Subsegments |

|

Packaging Technology |

|

|

Bump Type |

|

|

Application |

|

|

End user Industry |

|

|

Wafer Size |

|

|

Substrate Type |

|

|

Bump Pitch |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Flip Chip Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating the flip chip market and is projected to hold the regional revenue share of 42.3% by 2035. The region is the global center for high-volume advanced packaging, driven by consumer electronics, memory semiconductors, and mobile processors, fueling growth in the region. Taiwan leads through foundry integrated packaging for AI and HPC applications, while South Korea focuses on memory stack flip-chip interconnects. Japan contributes specialized equipment and materials alongside automotive flip-chip assembly. China rapidly expands domestic capacity targeted at smartphones and IoT devices. Malaysia serves as a major OSAT hub for the multinational corporations seeking diversified assembly locations. Asia Pacific prioritizes scale, cost efficiency, and rapid time-to-market. Key characteristics include the dense clustering of bumping fabs, mature supply chains for substrates and underfill materials, and intense competition among foundries, IDMs, and independent OSATs for premium packaging contracts.

High levels of innovation and increasing R&D expenditure are shaping the market in China. As per the ITIF August 2024 data, 55% of global semiconductor patent applications originated from China, with application volumes exceeding those of the U.S., indicating rapid technological advancement in chip design and packaging. This innovation momentum is reinforced by the national R&D spending, which exceeded USD 458.5 billion in 2023, marking an 8.1% YoY increase. Such sustained investment is stimulating the development of the high-performance semiconductors used in AI, telecommunications, and automotive sectors where flip-chip packaging is widely applied. As China continues to prioritize domestic semiconductor capabilities, the integration of advanced packaging technologies is expected to expand, supporting long-term market growth.

Japan flip chip market is expanding rapidly and reached USD 2.3 billion in 2025 and is expected to exceed USD 6.5 billion by the end of 2035 at a CAGR of 11.1%. In 2026, the market is projected to reach a size of USD 2.6 billion. The market is supported by rising semiconductor demand. JEITA December 2025 data estimates global electronics and IT industry production will reach USD 4,118.4 billion in 2025, growing 11% YoY, driven by generative AI data centers and cloud infrastructure. Japan electronics and IT companies are also expected to see production rise to USD 285 billion in 2025, increasing further to USD 295 billion in 2026. This growth is particularly strong in semiconductors and electronic components, where advanced packaging technologies such as flip-chip are critical. As per the ITA November 2025 data, the semiconductor industry rise with 9.4% in 2025. As AI-driven workloads expand, demand for high-performance chips is increasing, reinforcing the adoption of flip-chip solutions across computing and consumer electronics segments in Japan.

Japan Semiconductor Market, 2025

|

|

2022 |

2023 |

2024 |

2025 |

|

Market Size (Japan) |

48.158 |

48.751 |

47.410 |

51.886 |

|

Y-on-Y Growth (Yen basis) |

10.2% |

-2.9% |

1.4% |

9.4% |

|

Exchange Rate |

131.4 |

140.4 |

150.5 |

148.9 |

Source: ITA November 2025

North America Market Insights

The North America is projected to emerge as the fastest-growing region in the flip chip market and is expected to expand at a CAGR of 9.5% during the assessment period, 2026 to 2035. The region is driven by the strategic push to rebuild domestic advanced packaging capacity after decades of offshore outsourcing. The U.S. leads via defense-driven requirements and investments in pilot for 2.5D and 3D flip chip assembly with a focus on securing supply chains for AI and high-performance computing. Canada complements this by highlighting specialized R&D for telecommunications photonics and automotive sensor applications using research council facilities and industry partnerships. North America focuses on low to medium-volume, high-reliability segments, including aerospace, medical devices, and military systems. The market operates via close collaboration between IDMs, government labs, and select OSATs, ensuring process control and intellectual property protection for sensitive applications.

Both innovation in advanced interconnect technologies and federal funding initiatives are shaping the flip chip market in the U.S. As per the NLM July 2022 study, developments such as high-yield μ-bump bonding between InP and SiC for millimeter-wave applications demonstrate the growing adoption of flip-chip in high-frequency communication systems, particularly relevant for 5G and defense electronics. On the other hand, the Semiconductor Industry Association August 2024 data reports U.S. semiconductor sales reaching USD 264 billion in 2023, and the CHIPS Incentives Program is deploying USD 39 billion to establish advanced packaging facilities and fabrication clusters, based on federal register March 2023 data. This dual push of technology advancement and public investment is strengthening domestic packaging capabilities, positioning flip chip as a critical enabler in next-generation semiconductor manufacturing, and supporting long-term market growth in the U.S.

The targeted federal investments in semiconductor production and next-generation computing technologies are shaping the market in Canada. In April 2024, the Government of Canada committed USD 44 million to IBM Canada and C2MI to expand domestic semiconductor manufacturing, including advanced packaging capabilities. A USD 27 million investment in Ranovus Inc. supported AI-focused semiconductor production, which relies on high-density interconnect technologies such as flip-chip. Moreover, Canada announced up to USD 185 million for semiconductor projects under bilateral cooperation with the U.S. Further, the Government of Canada's April 2026 data shows USD 360 million in quantum funding is accelerating demand for high-performance chip packaging. These investments collectively strengthen Canada’s ecosystem for advanced semiconductor assembly, positioning flip-chip technologies for sustained growth across AI, telecom, and quantum applications.

Government Investments Supporting Semiconductor, 2021-2024

|

Year |

Initiative / Program |

Investment Amount |

Key Focus Area |

|

2024 |

IBM Canada & C2MI Projects |

$59.9 million |

Semiconductor manufacturing & innovation |

|

2023 |

Ranovus Inc. (SRF) |

$36 million (part of $100M project) |

AI semiconductor production |

|

2023 |

Canada–U.S. Semiconductor Cooperation (SRF) |

Up to $250 million |

Supply chain strengthening |

|

2023 |

North American Semiconductor Supply Chain Declaration |

Strategic (non-monetary commitment) |

Regional supply chain resilience |

|

2022 |

Semiconductor Challenge Callout (ISED) |

$150 million |

R&D, advanced packaging, MEMS |

|

2022 |

Budget 2022 (ISED Support) |

$45 million |

Market analysis & industry development |

|

2021 |

National Research Council – CPFC |

$90 million |

Photonics & compound semiconductor fabrication |

Source: Government of Canada January 2026 data

Europe Market Insights

The flip chip market in Europe is defined by automotive electrification, industrial automation, and high-reliability applications for medical and defense sectors. Europe prioritizes medium-volume, high-mix production with stringent quality and regulatory standards. Germany leads in power semiconductor flip chip assembly for electric vehicle drive trains, while France concentrates on aerospace and defense packaging. The region operates via strong collaboration between IDM research institutes such as Fraunhofer and CEA-Leti and select OSATs rather than large standalone packaging foundries. Key characteristics include emphasis on copper pillar bumps for thermal management, localization requirements for medical device semiconductors, and a growing ecosystem for chiplet-based designs.

The flip chip market in Germany is advancing steadily, supported by strong R&D intensity and large-scale public investments in semiconductor manufacturing. According to the GTAI 2026 data, the electronics sector accounts for 23% of the country’s total R&D spending, highlighting sustained innovation in microelectronics and advanced packaging technologies. A major growth driver is the government’s commitment of up to USD 5.5 billion to support the over USD 11 billion European Semiconductor Manufacturing Company (ESMC) joint venture, involving TSMC, Bosch, Infineon, and NXP. Such investments are expected to strengthen domestic semiconductor production while creating parallel demand for advanced packaging solutions, including flip-chip, particularly in automotive and industrial applications. As Germany continues to expand its semiconductor ecosystem under EU-wide initiatives, the integration of fabrication and packaging capabilities is likely to reinforce long-term market growth.

National semiconductor strategy and public investment in advanced electronics is fueling the flip chip market in UK. As per the Government UK May 2023 data the UK government launched a USD 1.28 billion National Semiconductor Strategy to strengthen design compound semiconductors and advanced packaging capabilities. Moreover the UK allocated USD 256 million to support innovation in semiconductor R&D mainly via initiatives involving compound semiconductor clusters in South Wales. The electronics sector also contributes significantly to the economy, with UK manufacturing generating USD 287 billion in output in 2022 underpinning demand for high performance semiconductor components. These investments combined with the UK’s focus on telecom defense and photonics are driving adoption of advanced packaging technologies such as flip-chip particularly in high frequency and high reliability applications.

Key Flip Chip Market Players:

- TSMC (Taiwan)

- Samsung Electronics (South Korea)

- Intel Corporation (U.S.)

- ASE Group (Taiwan)

- Amkor Technology (U.S.)

- JCET (China)

- Powertech Technology Inc. (Taiwan)

- STATS ChipPAC (Singapore)

- Texas Instruments (U.S.)

- Renesas Electronics (Japan)

- Sony Semiconductor (Japan)

- Toshiba Corporation (Japan)

- Infineon Technologies (Germany)

- STMicroelectronics (Switzerland)

- NXP Semiconductors (Netherlands)

- Micron Technology (U.S.)

- Analog Devices (U.S.)

- ASE (Taiwan)

- Indium Corporation (U.S.)

- Daktronics (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- TSMC dominates the flip clip market via its advanced CoWoS and InFO technologies, enabling high-density interconnects for AI and HPC chips. The company has invested heavily in expanding its flip chip bumping capacity at advanced nodes serving clients such as NVIDIA and AMD. TSMC’s strategic shift to hybrid bonding further reduces the flip chip pitch, solidifying its leadership.

- Samsung Electronics competes fiercely in the flip chip market via its I-Cube and X-Cube packaging solutions, integrating memory and logic chips. The company uses its vertically integrated model from foundry to flip chip assembly to optimize performance for its Exynos processors and HBM memory stacks. In 2024, the company made an operating profit of USD 32,725,961.

- Intel Corporation has re-entered the flip chip market with its EMIB and Foveros technologies, targeting chiplet-based designs. As an IDM, Intel uses flip-chip interconnects in its Sapphire Rapids and Ponte Vecchio products. The company’s foundry services now offer advanced flip chip capabilities to external customers aiming to rival TSMC.

- ASE Group is the largest OSAT player in the market, providing cost-competitive flip chip BGA and chip scale packaging for smartphones, GPUs, and networking devices. The company has automated its flip chip bonding lines and expanded capacity in Kaohsiung and Shanghai. ASE’s strategic acquisition of advanced packaging IP and partnerships with material suppliers enable it to offer pitch copper pillar bumps. In 2024, the company made an operating revenue of USD 595,409.6 million.

- Amkor Technology is a key U.S.-based OSAT in the flip chip market, specializing in flip chip CSP and flip chip BGA for automotive, mobile, and IoT applications. The company operates high-volume manufacturing sites in Korea, Japan, and Portugal. Amkor’s strategic initiatives include developing next-gen flip chip modules for mmWave 5G and investing in panel-level packaging to improve performance.

Here is a list of key players operating in the global market:

The flip chip market is highly consolidated, led by TSMC, Samsung, and Intel, which dominate advanced nodes for AI and HPC. Key players from the U.S., Taiwan, Japan, and Europe focus on heterogeneous integration and chiplets. Strategic initiatives include heavy R&D investments in copper hybrid bonding, panel-level packaging, and architectures. In July 2025, SHINKO ELECTRIC INDUSTRIES CO., LTD. announced acquiring IATF 16949 certification, an international quality management system standard for the automotive industry, at Kohoku and Wakaho Plants, both located in Nagano City, for the design and manufacturing of flip-chip type packages for CPUs and GPUs. Recent capacity expansions and foundry OSAT collaborations aim to reduce supply chain bottlenecks. China and Malaysia OSATs are scaling advanced flip chip capabilities to capture spillover demand from semiconductor decoupling trends.

Corporate Landscape of the Market:

Recent Developments

- In February 2025, ASE officially launched its fifth plant in Penang, which will significantly build on the company’s strong packaging and testing capabilities in the Bayan Lepas Free Industrial Zone. The new plant is part of a strategic expansion plan that will expand the floor space of ASE’s Malaysia facility from its current area of 1 million square feet to approximately 3.4 million square feet.

- In July 2025, Indium Corporation, a leading materials refiner, smelter, manufacturer, and supplier, announced the global availability of WS-910 Flip-Chip Flux, a new water-soluble flip-chip dipping flux designed to meet the demands of cutting-edge semiconductor devices.

- In May 2024, Daktronics of Brookings, South Dakota, released its Flip-Chip COB (Chip On Board) LED display technology worldwide. The company’s latest addition to its Narrow Pixel Pitch (NPP) product family brings tighter pixel spacings ranging from 1.8 millimeters to 0.9 millimeters with increased durability and reliability, combined with lower power consumption for an overall improved experience for customers.

- Report ID: 5690

- Published Date: May 14, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.