Flexographic Printing Market Outlook:

Flexographic Printing Market size was valued at USD 9.8 billion in 2025 and is projected to reach USD 15.4 billion by the end of 2035, rising at a CAGR of 4.6% during the forecast period, i.e., 2026-2035. In 2026, the industry size of flexographic printing is assessed at USD 10.2 billion.

The flexographic printing market is supported by the steady industrial demand linked to packaging production, mainly in the food, beverage, pharmaceutical, and logistics sectors. According to the FRED April 2025 data, the real sectoral output for manufacturing, printing, and related support activities in 2024 was 78.390 units (2017=100), reflecting a consistent downstream demand from the packaging converters and label manufacturers. The growth in packaged goods consumption is a primary driver, with the Department of Agriculture reporting that packaging-related activities account for a significant share of the food system's costs. As per the Frontiers June 2025 data, food packaging accounts for 40.5% of all plastic production, and 35% of this waste is recycled. These figures indicate a sustained print volume requirement tied directly to the essential goods distribution and retail supply chains.

Moreover, the market has benefited from alignment with the environmental and efficiency initiatives outlined by the government bodies. The U.S. EPA October 2025 data depict that the packaging accounts for nearly 29.1% of the municipal solid waste generation, driving increased emphasis on recyclable substrates such as paper and flexible materials compatible with flexographic processes. In Europe, the regulatory frameworks under the Circular Economy Action Plan prioritize recyclable and reusable packaging formats with targets for 100% recyclable packaging by 2030, based on the European Commission’s February 2026 influencing the material and print technology choices. These policy and cost factors continue to shape procurement strategies among converters and brand owners, supporting the ongoing role of flexographic printing in high-volume packaging applications.

Key Flexographic Printing Market Insights Summary:

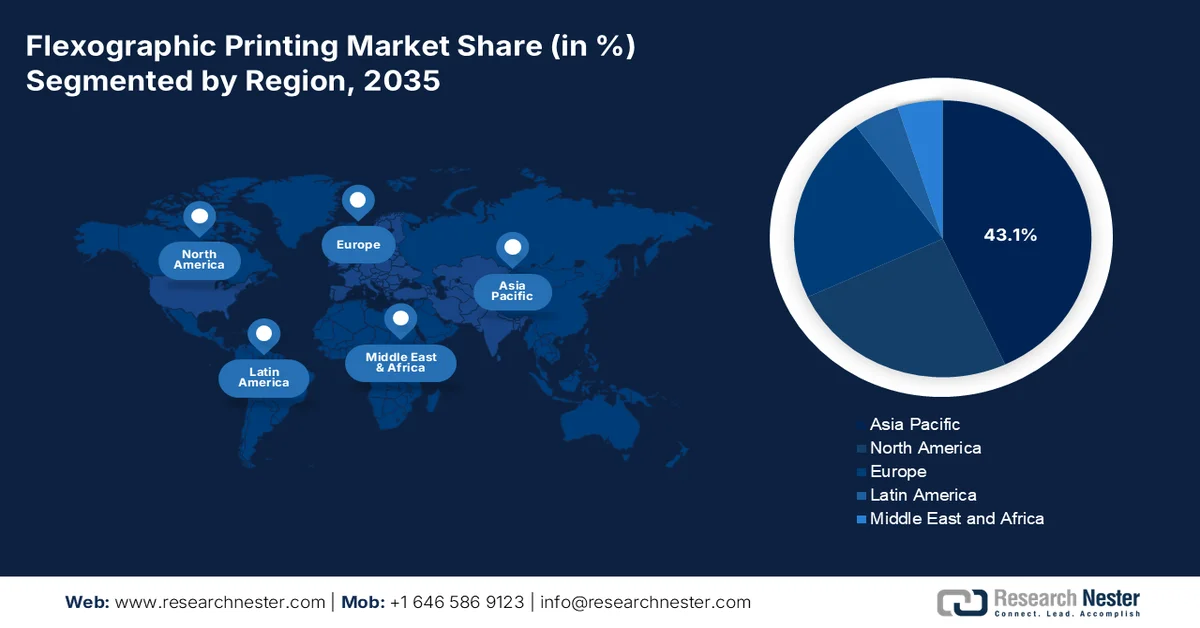

Regional Highlights:

- The Asia Pacific region anticipated 43.1% share by 2035, owing to expanding food processing industries, rising consumption, and government-led packaging modernization initiatives

- North America is forecasted to witness the fastest growth in the flexographic printing market at a CAGR of 4.2% during 2026-2035, attributed to steady demand from food, beverage, and pharmaceutical packaging alongside ongoing equipment modernization

Segment Insights:

- The central impression press sub-segment of the flexographic printing market is projected to capture a dominant 52.5% share by 2035, propelled by its high-quality flexible packaging capabilities supported by stable web tension and enhanced drying efficiencies

- The plastic films sub-segment is anticipated to maintain its leading position over the forecast period, impelled by rising demand for durable, moisture-resistant, and recyclable packaging solutions compatible with high-speed flexo printing

Key Growth Trends:

- Public investment in food supply chains and packaging

- Public spending on waste management

Major Challenges:

- Stringent environmental regulations

- Shortage in skilled labor

Key Players: Bobst, Windmöller & Hölscher, Mark Andy, PCMC (Paper Converting Machine Company), Nilpeter, Koenig & Bauer, Uteco Converting, OMET, Comexi, SOMA Engineering, Taiyo Kikai, Miyakoshi Printing Machinery, Weifang Donghang, BFM srl, GIAVE, Lohia Corp, Siegwerk, DuPont, XSYS, Eagle Flexible Packaging, Inc.

Global Flexographic Printing Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 9.8 billion

- 2026 Market Size: USD 10.2 billion

- Projected Market Size: USD 15.4 billion by 2035

- Growth Forecasts: 4.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (43.1% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Brazil, Mexico, Indonesia, Vietnam, Thailand

Last updated on : 6 April, 2026

Flexographic Printing Market - Growth Drivers and Challenges

Growth Drivers

- Public investment in food supply chains and packaging: The government's spending on the food systems is a driver for flexographic printing via its impact on the packaged goods. According to the USDA August 2024 data, the food expenditure reached USD 2.57 trillion in 2023, with packaging, transportation, and retail forming a substantial cost component. The public programs, such as SNAP and school meal initiatives, sustain high-volume food distribution, increasing the demand for printed flexible packaging and labels. According to the PIB March 2025 data, the Ministry of Food Processing Industries has allocated over USD 1.20 billion under the PMKSY scheme to strengthen the food processing and cold chain infrastructure. These governments prioritize food security and supply resilience; converters are seeking stable order pipelines.

- Public spending on waste management: Investments in waste management infrastructure are influencing the material selection and printing processes. Significant investment is allocated towards waste management and recycling systems. Similarly, the European Environment Agency's December 2025 data depicts that the member states spending to meet the recycling targets exceeds 55% for municipal waste. These initiatives promote the use of recyclable substrates such as paper and mono-material plastics, which are compatible with flexographic printing. This transition supports flexographic printing due to its adaptability to sustainable materials. Further, the suppliers can capitalize by developing inks and plates optimized for recycled substrates, aligning with government-funded recycling ecosystems.

- Demand for customized packaging solution: Customized packaging is emerging as a measurable demand driver for the market, supported by the government-backed growth in small businesses, local manufacturing, and the digital commerce ecosystem. According to the Pew Research Center's April 2024 data, small businesses account for 99.9% of all U.S. firms, many of which increasingly rely on differentiated packaging to compete in retail and online channels. These businesses require shorter print runs, SKU variation, and localized packaging formats, which are increasingly addressed via advancements in flexographic plate technology and hybrid press configurations. Further, the rise in e-commerce sales and personalized packaging enhances customer engagement and brand recall.

Challenges

- Stringent environmental regulations: Entering the market requires navigating a complex web of environmental regulations, particularly concerning volatile organic compound emissions. The EPA mandates that wide web flexographic printing operations limit the organic HAP emissions. Further, the compliance requires significant investment in capture systems, oxidizers, or solvent recovery units. New players must either adopt water-based or UV curable inks from the outset or invest heavily in emission control infrastructure. The company has established dedicated production hubs in the Asia Pacific with the formulations adapted for tropical climates and regional compliance standards.

- Shortage in skilled labor: The flexographic printing market faces a critical shortage of skilled operators capable of managing modern high-speed presses. This challenge is mainly acute for the new players who cannot afford production delays or quality inconsistencies. Lack of a qualified workforce and the sluggish transfer of technology impede modernization and restrict widespread adoption of the flexo. An industry professional noted that experienced personnel often hop for better pay, leaving operational gaps. Untrained staff promoted to operator roles further exacerbate the issue, leading to increased waste and machinery damage risks.

Flexographic Printing Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.6% |

|

Base Year Market Size (2025) |

USD 9.8 billion |

|

Forecast Year Market Size (2035) |

USD 15.4 billion |

|

Regional Scope |

|

Flexographic Printing Market Segmentation:

Press Type Segment Analysis

Under the press type segment, the central impression press sub-segment is leading and is poised to hold the share value of 52.5% by the end of 2035 in the market. The segment is driven by its high-quality flexible packaging because they use a large central drum that stabilizes web tension across all color stations, ensuring precise registration at all speeds. According to the Flexographic Technical Association 2026 data, companies experience 63% in drying efficiencies. Moreover, the manufacturers are increasingly integrating automated sleeve systems and inline quality inspection to further reduce downtime. As sustainability mandates tighten globally, the CI press segment continues to outpace stack and inline press types, particularly in Asia-Pacific and North America, where flexible packaging demand remains robust.

Key Evaluation Factors in Central Impression (2026)

|

Category |

Features |

|

Quick-Change Features |

88% of OEMs highlight the importance of reduced downtime and faster job transitions |

|

Waste Reduction |

88% emphasize minimizing material waste and improving sustainability |

|

Automation |

100% stress automation for improved uptime, consistency, and efficiency |

|

Operator-Friendly Interface |

88% prioritize easy-to-use man/machine interfaces |

|

Ergonomics & Modularity |

88% highlight design for ease of operation and flexible configurations |

|

Drying Efficiency |

63% consider efficient drying systems important |

|

Ease of Maintenance |

63% emphasize simplified maintenance for reduced downtime |

Source: Flexographic Technical Association 2026

Substrate Segment Analysis

Within the substrate segment, the plastic films are leading in the market. These films are favored for their durability, transparency, moisture resistance, and compatibility with high-speed flexo presses. The shift toward mono-material recyclable packaging has further increased the demand for flexo-printed PE and PP films. Flexography’s ability to print fine details and high opacity whites on thin gauge films makes it the preferred process. The key innovations include surface treatment technologies and water-based primer coatings that enhance the ink adhesion on non-porous films. Despite regulatory pressure on single-use plastics, demand for recyclable and bio-based PE films continues to rise, especially in food and medical packaging applications.

Application Segment Analysis

In the market, flexible packaging is the dominant application segment. This includes pouches, stand-up bags, shrink sleeves, flow wraps, and lidding films used extensively for snacks, beverages, pet food, and personal care products. Flexographic printing is the technology of choice due to its high throughput, low cost per impression, and adaptability to thin, extensive films. According to the FPA 2026 data, the flexible packaging industry has made sales of USD 41.5 billion in the U.S. The key drivers include brand owners shifting from rigid containers to lightweight resealable pouches to reduce the logistics costs and carbon footprints. Additionally, advancements in high-barrier, recyclable mono-material films have expanded flexo’s role in shelf-stable food packaging. The segment is further propelled by e-commerce growth and demand for high-impact graphics in retail environments.

Our in-depth analysis of the flexographic printing market includes the following segments:

|

Segment |

Subsegments |

|

Print Width |

|

|

Technology |

|

|

Application |

|

|

End user Industry |

|

|

Substrate |

|

|

Press Type |

|

|

Ink Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Flexographic Printing Market - Regional Analysis

APAC Market Insights

The flexographic printing market in the Asia Pacific is dominating and is expected to hold the regional revenue share of 43.1% by the end of 2035. The region is driven by the expanding food processing sectors, rising domestic consumption, and government-led packaging modernization initiatives. China dominates the regional production, supported by its position as a global manufacturing hub for flexible packaging exports. India is experiencing stimulated growth due to government investment in food processing infrastructure and the shift from rigid to flexible packaging formats. Japan and South Korea represent mature technology, advanced markets where converters prioritize automation, servo-driven presses, and low migration inks for pharmaceutical and premium food applications. Key trends include the adoption of water-based and UV-LED ink systems to meet evolving environmental standards, increasing consolidation among converters, and the integration of hybrid flexo-digital presses for shorter runs.

The large-scale e-commerce activity and government-driven sustainability mandates in packaging are driving the market in China. According to the Packnode November 2025 data, China handles over 100 billion parcels annually, and the demand for corrugated boxes, mailers, and labels, core applications for flexographic printing, remains structurally high. Pilot programs in major logistics hubs like Shanghai and Shenzhen are testing reusable packaging systems and standardized formats, encouraging higher efficiency in high-volume printing operations. Additionally, the national roadmap aims to reduce packaging-related CO2 emissions by over 20 million tons annually, pushing converters to adopt water-based inks and environmentally compliant substrates. These regulatory and operational shifts are driving modernization across printing facilities while aligning packaging production with circular economy principles.

The regulatory enforcement and expanding flexible packaging demand are fueling the market in India. According to the PIB February 2023, the introduction of Extended Producer Responsibility guidelines has significantly increased industry participation, with registered Producers, Importers, and Brand Owners rising from around 310 to nearly 5,400 covering approximately 2.26 million tons of plastic packaging in 2022 to 2023, compared to 3.4 million tons of total plastic waste generated. Additionally, flexible plastic packaging accounts for 73% of total plastic packaging in India, making it a dominant segment for flexographic applications. The flexible packaging market reached USD 12.72 billion in 2025, supported by a 45% increase in the film manufacturing capacity over the past four years, based on India Plastics Pact December 2024 data. These trends indicate strong substrate availability and the rising production volumes, positioning India as a high-growth market.

North America Market Insights

The North America is projected to emerge as the fastest-growing region in the flexographic printing market and is expected to expand at a CAGR of 4.2% during the assessed period, 2026 to 2035. The market is defined by the steady demand from the food, beverage, and pharmaceutical packaging sectors, supported by a mature converting industry and ongoing equipment modernization. Regulatory compliance remains a defining factor with the environmental standards driving the transition toward lower-emission ink systems and energy-efficient press technologies. The region benefits from a concentrated base of global press manufacturers, ink suppliers, and plate makers, enabling converters to access advanced automation and technical support. Further, the market is supported by consistent end-user demand, regulatory-driven capital investment, and strong export activity in flexographic consumables and converting equipment to Latin American and European markets.

The industrial production and packaging-linked demand across manufacturing sectors is driving the market in the U.S. According to the EPA's February 2026 data, over 90% of flexographic applications are tied to packaging and specialty products, including flexible materials such as plastic films, paper, foil, and labels. This high concentration underscores the market’s dependence on consumer goods, food, and industrial packaging demand. Moreover, central impression (CI) stack and inline presses dominate production environments, with CI presses widely adopted for flexible packaging due to efficiency in handling continuous substrates. Regulatory frameworks also shape market dynamics, as the Florida Department of Environmental Protection's April 2024 data specifies that facilities using less than 80,000 pounds annually of water-based inks and coatings or 20,000 pounds of solvent-based materials fall under controlled emission thresholds, influencing technology selection toward low-VOC and water-based systems. These compliance limits are driving converters to modernize equipment and shift ink usage patterns, thus driving the market growth.

The demand from packaging manufacturing and trade-driven sectors is shaping the flexographic printing market in Canada. According to Statistics Canada, December 2023 data, total manufacturing revenue increased by 17.4% to USD 922.4 billion in 2022, with goods production contributing USD 866.7 billion, indicating robust industrial output that drives demand for printed packaging and labeling solutions. Moreover, the OEC 2024 data shows that Canada exported USD 224 million worth of corrugated carton boxes and cases, highlighting the role of paper-based packaging widely printed using flexographic processes in trade activities. Further, the ITA July 2025 data depicts that e-commerce continues to strengthen packaging demand, with online retail accounting for 6.1% of total retail sales in December 2024, generating about USD 3.14 billion in monthly sales, while the broader market reached nearly USD 89.4 billion in GMV. These data support consistent utilization across high-volume applications.

Canada Export Data on Corrugated Carton Boxes, 2024

|

Country |

Value (USD) |

|

U.S. |

222 M |

|

Jamaica |

678 K |

|

Mexico |

355 K |

|

Cuba |

259 K |

Source: OEC

Europe Market Insights

The flexible printing market in Europe is characterized by mature demand, stringent environmental regulations, and a stimulating transition toward sustainable packaging solutions. The region’s packaging converters face dual pressures from the European Union’s Packaging and Packaging Waste Regulations, which mandate that all packaging be recyclable, and from brand owners committing to recycled content targets. These drivers have surged the investment in flexographic presses capable of printing on mono material fills paper-based substrates incorporating post-consumer recyclate. Key trends include the adoption of water-based and EB curable ink systems to meet the VOC emission limits under the Industrial Emissions Directive, consolidation among label converters, and integration of inline inspection and color management systems.

The strong packaging regulations, industrial output, and sustainability-driven material transitions are shaping the market in Germany. According to the Destatis 2026 data, the country’s industrial sector reported total sales of approximately USD 2.27 trillion, highlighting a large manufacturing base that generates consistent demand for packaging, labeling, and transport materials. Moreover, the plastics remain widely used across industries, with around 21.1 million tons of plastic produced in 2021, but only 1.65 million tons derived from recycled content, indicating a significant gap and a push toward circular material use, based on the Kreislaufwirtschafts Strategie Deutschland May 2025 data. This transition is reinforced by environmental policies, as Germany has achieved packaging waste recycling rates above 65%, among the highest in Europe. These dynamics are shifting demand toward recyclable and paper-based substrates, which are well-suited for flexographic printing processes.

The strong packaging consumption and evolving waste management policies are driving the market in the UK. According to the Swansea University October 2024 data, nearly USD 2.15 million in funding from the Welsh Government, Innovate UK, and EU programs has been delivered to measurable industrial impact across the flexographic value chain. These advancements have contributed to annual production cost savings of USD 539 million and a 15% reduction in material waste, equivalent to USD 113 million in savings, demonstrating strong efficiency gains for converters and packaging producers. Moreover, the improvements in ink transfer and plate technology have enabled up to 30% reduction in run time and a 20% increase in global plate sales for industry participants. The ability to reduce curing time by up to 100 times has further enhanced throughput in high-volume packaging applications. These developments are strengthening the UK’s position in advanced printing technologies.

Key Flexographic Printing Market Players:

- Bobst (Switzerland)

- Windmöller & Hölscher (Germany)

- Mark Andy (U.S.)

- PCMC (Paper Converting Machine Company) (U.S.)

- Nilpeter (Denmark)

- Koenig & Bauer (Germany)

- Uteco Converting (Italy)

- OMET (Italy)

- Comexi (Spain)

- SOMA Engineering (Czech Republic)

- Taiyo Kikai (Japan)

- Miyakoshi Printing Machinery (Japan)

- Weifang Donghang (China)

- BFM srl (Italy)

- GIAVE (France)

- Lohia Corp (India)

- Siegwerk (Germany)

- DuPont (U.S.)

- XSYS (Germany)

- Eagle Flexible Packaging, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Bobst is a global leader known for its integrated printing and converting solutions in the flexographic printing market. The company has pioneered automation and digital workflow integration, including its proprietary oneECG technology, which reduces the setup time and ink waste. The company focuses on Industry 4.0 connectivity and sustainable processing. In 2024, the company made a total sale of USD 2,080 million.

- Windmoller & Holscher is a dominant player in the flexographic printing market, mainly for high-end central impression flexo presses. The company has advanced servo-driven press technology and automated sleeve systems to minimize downtime. The company initiative includes developing the HELIOSTAR series high-speed printing and integration AI based quality inspection. In 2024, the company made a revenue of USD 25,941 million.

- Mark Andy is a key innovator in the flexographic printing market, mainly for narrow web and label printing applications. The company has strategically adopted digital hybrid platforms that combine flexo stations with inkjet modules. The company initiative includes developing quick charge print decks and automated registration servo upgrades for legacy presses.

- PCMC, part of Barry Wehmiller, is a premier manufacturer in the flexographic printing market specializing in CI flexo presses for flexible packaging, tissue, and nonwovens. The company’s strategic initiatives include the Fusion series, which features fully enclosed doctor blade systems and automated impression setting.

- Nilpeter is a renowned name in the flexographic printing market, mainly for modular narrow and mid web flexo presses used in labels, cartons adn light films. The company’s strategic initiatives focus on the FA platform, which allows quick conversion between the flexo screen and digital units. Nilpeter has pioneered automatic register control to reduce the maker-ready time.

Here is a list of key players operating in the global market:

The global flexographic printing market is highly competitive, characterized by a mix of established legacy players from Europe and the U.S. and specialized manufacturers from Asia. The key players focus on technological advancements, such as servo-driven presses, hybrid digital flexo solutions, and automation to improve efficiency and reduce waste. Strategic initiatives include mergers and acquisitions to expand geographic reach, partnerships for sustainable inks and substrates, and investment in Industry 4.0 capabilities. For example, in March 2026, Siegwerk announced the signing of a definitive agreement for the acquisition of Hi-Tech Inks, a prominent Indian producer of flexographic and gravure printing inks. To meet the rising demand for flexible packaging, companies are also developing energy-saving UV/LED systems and quick-change tooling to serve short-run orders profitably.

Corporate Landscape of the Flexographic Printing Market:

Recent Developments

- In March 2025, DuPont Cyrel Flexographic Solutions announced a new agreement with All Printing Resources (APR) to distribute its innovative flexographic platemaking solutions to customers across North America.

- In June 2024, Eagle Flexible Packaging, Inc. (Eagle), a leader in the flexible packaging industry, announces the acquisition of a SOMA Optima2 wide web flexographic printing press.

- In May 2024, XSYS introduced two new plates under the newly established Nyloflex Eco brand. This innovative approach demonstrates the company’s strong commitment to advancing sustainability in the printing industry.

- Report ID: 8502

- Published Date: Apr 06, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.