Data Governance Market Outlook:

Data Governance Market size was valued at USD 5.6 billion in 2025 and is projected to reach USD 38.3 billion by the end of 2035, rising at a CAGR of 21.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of data governance is assessed at USD 6.7 billion.

The demand for the data governance market is shaped by the regulatory expansion and public sector data modernization programs across major economies. In the U.S., the federal data strategy execution under the Foundation for evidence based policymaking act continues to require agencies to formalize data inventories, stewardship roles, and secure data sharing practices. According to the Open Knowledge Foundation, December 2025 data, the federal agencies collectively manage thousands of data assets with over 300,000 datasets cataloged, reflecting the scale of governance required to ensure accessibility, quality, and compliance. The National Institute of Standards and Technology has advanced frameworks addressing data integrity risk management and privacy engineering, which are being operationalized by enterprises working with federal systems. These policies are compelling organizations to formalize governance structures that align with cross-border data access, consent management, and auditability requirements.

Enterprise adoption is further reinforced by the cybersecurity and critical infrastructure protection priorities. The U.S. Cybersecurity and Infrastructure Security Agency's May 2023 data highlights that over 16 critical infrastructure sectors depend on secure and reliable data flows, increasing the need for a governance framework that integrates with risk and incident management practices. Similarly, as per the World Economic Forum, January 2026 data, nearly 70% of organizations across member countries have experienced data-related security incidents, promoting stronger governance controls around data classification, lineage tracking, and third-party access. Further efforts in APAC, such as India’s Digital Personal Data Protection Act implementation and national data sharing initiatives, are further expanding the governance requirements for enterprises operating across jurisdictions.

Key Data Governance Market Insights Summary:

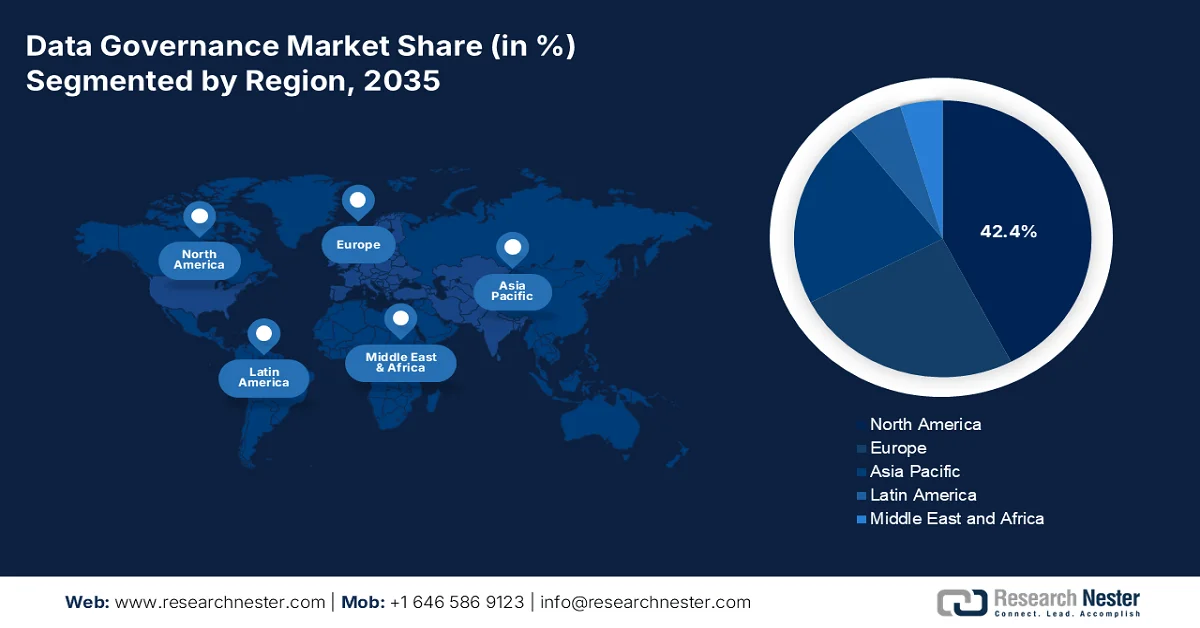

Regional Highlights:

- North America data governance market is projected to command a 42.4% share by 2035, reinforced by stringent privacy regulations, rising AI adoption, and federal cloud mandates

- Asia Pacific is anticipated to expand at a CAGR of 15.5% during 2026-2035, stimulated by national data authority laws, cross-border trade digitization, and accelerating AI adoption

Segment Insights:

- In the data governance market, the large enterprises segment is expected to secure a 62.5% share by 2035, propelled by complex regulatory compliance, cross-border data flows, and the need for centralized policy enforcement across multiple business units

- The cloud segment within deployment mode is gaining strong momentum over 2026-2035, fueled by AI-native governance tools and data fabric architectures

Key Growth Trends:

- EU data economy investments

- Cybersecurity funding and critical infrastructure protection

Major Challenges:

- High implementation complexity

- User adoption resistance

Key Players: Informatica (U.S.), Microsoft (U.S.), IBM (U.S.), SAP (Germany), Oracle (U.S.), Collibra (Belgium), Alation (U.S.), Talend (U.S.), TIBCO Software (U.S.), Atacama (Canada), Hitachi Vantara (Japan), NEC Corporation (Japan), Samsung SDS (South Korea), Infosys (India), Wipro (India), Tata Consultancy Services (India), Orion Governance (U.S.), Witboost (Italy), OneTrust (U.S.), DataGalaxy (France).

Global Data Governance Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.6 billion

- 2026 Market Size: USD 6.7 billion

- Projected Market Size: USD 38.3 billion by 2035

- Growth Forecasts: 21.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, South Korea, Brazil, Indonesia, Mexico

Last updated on : 6 April, 2026

Data Governance Market - Growth Drivers and Challenges

Growth Drivers

- EU data economy investments: The European Commission’s July 2024 report indicates that the data strategy is backed by large-scale funding and regulatory mandates, including the Data Governance Act and Digital Europe Programme, which have allocated USD 8.1 billion for digital capacity building. These initiatives are surging the enterprise adoption of structured data sharing mechanisms, mainly in sectors such as healthcare, energy, and manufacturing. The European Policy Center's May 2023 data highlights that the data economy reached USD 895 billion, creating direct pressure on enterprises to implement governance systems that ensure compliance, traceability, and cross-border data portability. Public funding programs are also supporting data spaces requiring standardized governance protocols. As enforcement tightens, organizations are investing in governance tools that support auditability and consent management. This regulatory-driven spending environment positions governance as a necessary operational layer rather than a discretionary investment.

- Cybersecurity funding and critical infrastructure protection: Government cybersecurity budgets are increasingly tied to the data governance requirements. According to the White House March 2023 data, the Cybersecurity and Infrastructure Security Agency budget exceeded USD 3.1 billion in 2024, focusing on securing data flows across 16 critical infrastructure sectors. These sectors, including energy, healthcare, and financial services, depend on structured data governance to manage risk, ensure data integrity, and support incident response. Governance tools are being deployed to enforce classification, access control, and audit trails as part of the zero-trust architecture. Further, the public sector contracts increasingly mandate governance capabilities aligned with NIST frameworks. This linkage between cybersecurity funding and data oversight is expanding the enterprise demand for the integrated governance solutions that support resilience and regulatory compliance.

- Defense and intelligence data management investments: Defense agencies are significantly increasing their spending on data management and governance to support intelligence surveillance and decision-making systems. According to the European Parliament, April 2025 data, the U.S. Department of Defense has allocated over USD 1.8 billion for data and AI-related initiatives under its Joint Artificial Intelligence Center and Chief Data Officer programs. These investments require strict governance frameworks to manage sensitive data, ensure security, and enable real-time analytics. Defense data strategies highlight the interoperability across allied systems, further increasing the governance complexity. Moreover, the contractors and technology providers must comply with stringent data standards, driving adoption of advanced governance tools. This represents a high-value demand driver in the market, as defense spending prioritizes secure, scalable, and compliant data ecosystems.

Challenges

- High implementation complexity: New players in the market find that customers underestimate the technical advancements required for deployment, leading to project delays and payment disputes. Top companies struggle with broad adoption because organizations lack a mature governance framework before implementation. The platform demands deep modeling configuration and a mature governance framework, which most mid-sized enterprises don’t possess. Licensing costs plus required consulting support make solutions feasible primarily for large enterprises, creating a significant barrier for new suppliers targeting the SME segment. Without turnkey solutions or scaled-down offerings, entrants cannot compete effectively.

- User adoption resistance: Even technically superior solutions fail when business users reject new workflows. The governance first interface is built for governance professionals, not always for data consumers, making analysts and engineers find the platform rigid and cumbersome. Without a data-driven culture, including clear ownership, stewardship, and accountability, even best-in-class tools become shelfware. The new players must invest heavily in change management, role-based training, and intuitive UX design. The rise of the lightweight alternatives demonstrates that modern users demand consumer grade experience, not compliance-focused interfaces.

Data Governance Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

21.2% |

|

Base Year Market Size (2025) |

USD 5.6 billion |

|

Forecast Year Market Size (2035) |

USD 38.3 billion |

|

Regional Scope |

|

Data Governance Market Segmentation:

Enterprise Size Segment Analysis

Under the enterprise size segment, the large enterprises sub-segment is dominating in the data governance market and is poised to hold the share value of 62.5% by the end of 2035. The segment is driven by complex regulatory compliance, cross-border data flows, and the need for centralized policy enforcement across multiple business units. Large enterprises face strict audit requirements under laws like GDPR, CCPA, and sector-specific regulations. Moreover, the federal contractors and large vendors reported a rise in mandatory data governance audits compared to the previous period. This pressure forces the large enterprises to invest in automated metadata management, data lineage, and role-based access controls. They operate hybrid environments with legacy systems and cloud data lakes requiring enterprise-grade solutions.

Deployment Mode Segment Analysis

Within the deployment mode, the cloud sub-segment is driving the market. Organizations prefer cloud native governance for its scalability, real-time metadata harvesting, and seamless integration with data lakes and AI pipelines on AWS, Azure, and Google Cloud. The shift in hybrid and multi-cloud architecture accelerated due to remote work and digital transformation. According to the European Commission, March 2026 data, nearly 45.2% of businesses use cloud services. This growth reflects a broader enterprise trend where cloud governance reduces the infrastructure overhead and enables automated policy enforcement across distributed data environments. Though the cloud adoption is surging, it is mainly driven by driven by AI native governance tools and data fabric architectures.

Data Source Segment Analysis

The unstructured data, including the emails, documents, images, videos, and social media content, has become the leading sub-segment in the market due to the explosive growth of gen AI and large language models. The unstructured content lacks predefined schemas, making lineage consent tracking and compliance enforcement significantly more complex. Organizations are rapidly expanding their governance focus to include unstructured sources driven by the regulation requiring AI training data transparency. According to the NLM October 2023 data, 80% of the healthcare data is unstructured. This surge is attributed to automated document processing, video surveillance, storage, and LLM training datasets. Manufacturers prioritize AI-powered classification, sensitive data detection, and automated policy tagging for unstructured content.

Our in-depth analysis of the data governance market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Deployment Mode |

|

|

Enterprise Size |

|

|

Business Function |

|

|

Industry Vertical |

|

|

Data Source |

|

|

End user Role |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Data Governance Market - Regional Analysis

North America Market Insights

North America dominates the global data governance market and is expected to hold the regional revenue share of 42.4% by the end of 2035. The key drivers are privacy regulations, AI adoption, and federal cloud mandates. The U.S. leads via NIST AI governance frameworks and HIPAA enforcement, while Canada surges with the Treasury Board’s Directive on Automated Decision Making. The major trends are automated policy enforcement, data lineage tools for AI risk management, and privacy-preserving analytics. Government spending remains robust, with CIO June 2022 data showing nearly USD 1 billion allocated via ARP to technology modernization funds in the U.S. Further, cross-border data transfer rules and the indigenous data authority shape market expansion. The region remains the benchmark for regulatory-driven governance innovation.

The increasing federal mandates on data standardization, transparency, and security are driving the market in the U.S. According to the White House December 2022, data under the Foundations for Evidence-Based Policymaking Act, all 24 Chief Financial Officers Act agencies have established Chief Data Officers to formalize data governance and lifecycle management practices. Moreover, the OECD June 2025 data depict that 90% of federal agencies implemented formal data governance and risk management frameworks to strengthen data protection and compliance. Furthermore, the federal investments in data science and data infrastructure emphasize the growing need for governance mechanisms to manage research and public datasets. These data are accelerating the adoption of data governance solutions across the U.S., particularly in highly regulated and data-intensive sectors.

The strong federal data strategies, privacy regulations, and increasing public sector digitization are driving the data governance market in Canada. The Digital Research Alliance of Canada 2025 reported over 80,000 open datasets as of 2024, reflecting the expanding volume of public data requiring standardized governance and quality controls. Additionally, the federal departments and agencies have implemented formal data governance frameworks and appointed data leads, strengthening accountability and data stewardship across government operations. Further, businesses collecting digital data have adopted structured data management and governance practices, highlighting growing private sector alignment with regulatory and operational standards. These developments show an active market growth and expansion.

APAC Market Insights

Asia Pacific is projected to emerge as the fastest-growing region in the market and is poised to expand at a CAGR of 15.5% during the assessed period, 2026 to 2035. The region is driven by the national data authority laws, cross-border trade digitization, and AI adoption. China enforces the Personal Information Protection Law and Data Security Law, mandating the local data storage and governance audits. India’s Digital Personal Data Protection Act pushes automated consent frameworks. Japan promotes Trusted Data Free Flow under G7 leadership. The key trends include classification automation, privacy-enhancing computation, and industry-specific governance. Government-backed data sandboxes are emerging across the region to test cross-border governance interoperability while balancing national security priorities.

The large-scale government initiatives focused on data integration, analytics, and regulatory oversight are driving the data governance market in China. According to the WCO News October 2024 data, China Customs’ Cloud Engine platform, which promotes a data-driven culture by enabling widespread data access and analytics with over 3,000 daily active users executing more than 28,000 analyses per day, leading to the identification of 2,917 fraud cases in 2023. Supporting this capability, China Customs has built a centralized data lake comprising over 15,000 data tables and more than 260 billion data entries reflecting the immense scale of structured and multi-source data being governed. Such developments demonstrate China’s strong emphasis on centralized data governance frameworks, real-time analytics, and enforcement-driven use cases, positioning the country as a high-growth market fueled by public-sector digitization and stringent data regulations.

The expanding digital economy, large-scale data generation, and increasing cloud adoption are shaping the market in India. According to the IBEF January 2024 data, India’s digital economy reached USD 1 trillion in 2025, supported by over 700 million internet users and more than a billion mobile devices, leading to exponential growth in digital transactions and data consumption. Additionally, cloud technology is expected to contribute 8% to India’s GDP by 2026, with a potential economic impact of USD 310 billion to USD 380 billion, while public cloud spending is projected to grow at a 27% CAGR through 2027. This surge in digital activity is driving infrastructure expansion, with India’s data center market expected to reach USD 7.44 billion in 2023 and continue growing significantly, alongside increasing capacity and new facility development, thus boosting the market growth.

Key Digital Infrastructure and Economic Drivers Supporting the Market (2024)

|

Category |

Key Data Points |

|

Macroeconomic Growth |

GDP expected to reach USD 26 trillion by 2047 |

|

Digital Population |

1.64 billion digital users; 700+ million internet users; 1+ billion mobile phones |

|

Digital Economy |

Growth from USD 200 billion (2017-18) to USD 1 trillion by 2025 |

|

Mobile Data Usage |

India has the highest mobile data consumption globally (2022) |

|

Cloud Market Growth |

Cloud to contribute 8% of GDP by 2026; USD 310 billion to USD 380 billion impact |

|

Cloud Investment |

Expected 25–30% annual growth, reaching USD 18.5 billion |

|

Public Cloud Expansion |

Expected 27% CAGR (2022 onwards) |

|

Data Center Market Size |

USD 7.44 billion (2023); projected strong growth |

|

Data Center Capacity |

637 MW (2022) → 1,015 MW by 2025 |

|

Number of Data Centers |

138 (2022); +45 new centers by 2025 |

|

Industry Growth |

Expected to reach USD 10.09 billion by 2027 |

|

Government Initiatives |

Digital India (DigiLocker, UMANG, e-health, digital finance) |

|

Employment & Innovation |

14 million jobs from the cloud by 2026 |

Source: IBEF January 2024

Europe Market Insights

The market in Europe is driven by the strict regulatory mandates and cross-border health data sharing. The European Health Data Space regulations enforced by the EMA require interoperable governance frameworks across member states. The key trends include automated consent management, synthetic data for research, and data altruism schemes. Germany leads with the industrial data spaces, while France prioritizes sovereign cloud governance. Government funding continues to prioritize secure data sharing infrastructures, particularly for cross-border clinical trials and public health surveillance. Privacy-enhancing technologies, such as federated learning and differential privacy, are being integrated into national governance roadmaps to comply with GDPR's data minimization principles. Additionally, public-private partnerships are emerging to standardize metadata management and data lineage across Europe's fragmented digital landscape.

Strict regulatory frameworks, industrial digitization, and strong government-backed data initiatives are shaping the data governance market in Germany. The OECD 2024 data shows that over 70% of enterprises in Germany have implemented digital adoption for structured data management and governance practices as part of their digital transformation strategies. Further, the data protection compliance audits increased across federal institutions, reinforcing the need for robust governance frameworks aligned with GDPR. Moreover, the European Parliament's December 2025 data depicts that under the GAIA-X initiative supported by the government and the European Commission, over 300 organizations participated by 2024 to build secure, standardized data ecosystems, emphasizing interoperability and sovereign data governance. These developments position Germany as a key European hub for advanced data governance adoption.

The increasing volumes of public data and rising regulatory scrutiny around data protection are driving the market in the UK. For instance, the British Geological Survey's March 2026 data reports that its Geology 50,000 datasets provide 99% nationwide coverage of geological data across Great Britain, highlighting the scale and complexity of structured public datasets requiring continuous governance and updates. At the same time, regulatory demand is intensifying as the Information Commissioner’s Office (ICO) February 2026 data noted that data protection complaints rose from over 40,000 in 2024/2025 to 66,000 in 2025/2026, with projections reaching 75,000 by year's end, indicating growing public awareness and enforcement pressure. Together, these data show a stimulating adoption of the market expansion.

Key Data Governance Market Players:

- Informática (U.S.)

- Microsoft (U.S.)

- IBM (U.S.)

- SAP (Germany)

- Oracle (U.S.)

- Collibra (Belgium)

- Alation (U.S.)

- Talend (U.S.)

- TIBCO Software (U.S.)

- Atacama (Canada)

- Hitachi Vantara (Japan)

- NEC Corporation (Japan)

- Samsung SDS (South Korea)

- Infosys (India)

- Wipro (India)

- Tata Consultancy Services (India)

- Orion Governance (U.S.)

- Witboost (Italy)

- OneTrust (U.S.)

- DataGalaxy (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Informatica is a dominant player in the data governance market, offering a comprehensive AI-powered intelligent data management cloud. The company has advanced the market by embedding automated data lineage metadata scanning and policy enforcement directly into its platform. Informatica’s strategic focus on cloud native governance enables organizations to unify siloed data across hybrid environments.

- Microsoft has rapidly expanded its presence in the market via Microsoft Purview, a unified data governance and risk management solution. The company leverages its deep integration with Microsoft Azure, Microsoft 365, and Power BI to provide automated data discovery, classification, and lineage across cloud and on-premises systems. In 2024, the company made a revenue of USD 245 billion.

- IBM addresses the data governance market with its IBM Knowledge Catalog and the Watson AI capabilities. The company focuses on active metadata management and automated policy enforcement to help enterprises build trusted AI and analytics pipelines. IBM’s strategic initiatives include integrating governance with data privacy solutions. In 2025, the company made a 6% of growth compared to the previous year.

- SAP competes in the data governance market primarily via SAP Master Data Governance and SAP Data Intelligence. The company targets large enterprises running SAP ERP landscapes, offering domain-specific governance for financial material customer and supplier data. SAP’s strategic initiative includes embedding governance into the Business Technology Platform for real-time data quality monitoring.

- Oracle delivers robust capabilities in the market via Oracle Enterprise Metadata Management and Oracle Cloud Infrastructure Data Catalog. The company emphasizes automated metadata harvesting, data lineage, and classification to support governed data lakes and warehouses. Oracle’s strategic initiative includes integrating governance with its autonomous database and AI/ML services, enabling policy-driven access and auditing.

Here is a list of key players operating in the global market:

The data governance market is highly competitive and is driven by the stringent regulations, such as GDPR and CCPA, and the need for AI-ready data. The key players from the U.S. dominate, and Europe and APAC are rapidly gaining ground via specialized solutions. The strategic initiatives include integrating AI and machine learning for automated data discovery, lineage, and quality management. The major vendors are also expanding via acquisitions and enhancing cloud native platforms. Partnerships with cloud hyperscalers are common to improve scalability. meanwhile the firms in South Korea, Japan, and Australia focus on industry-specific governance, and Indian players offer cost-effective managed services alongside product development. For example, in June 2025, Collibra announced the acquisition of Raito, a company specializing in data access governance.

Corporate Landscape of the Data Governance Market:

Recent Developments

- In September 2025, Witboost announces the launch of its Computational Governance solution, an innovative solution designed to govern data products at scale, enforce standards, accelerate deployments, and ensure end-to-end compliance.

- In May 2025, OneTrust announced its Data Use Governance solution, an industry-first set of capabilities designed to close the gap between traditional data governance and the real-time compliance demands of AI.

- In May 2025, DataGalaxy announced the launch of its next-generation data & AI value governance platform at the Gartner Data & Analytics Summit 2025 in London. This innovative solution redefines enterprise data governance in an era of AI transformation.

- Report ID: 8501

- Published Date: Apr 06, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.