Data Acquisition Hardware Market Outlook:

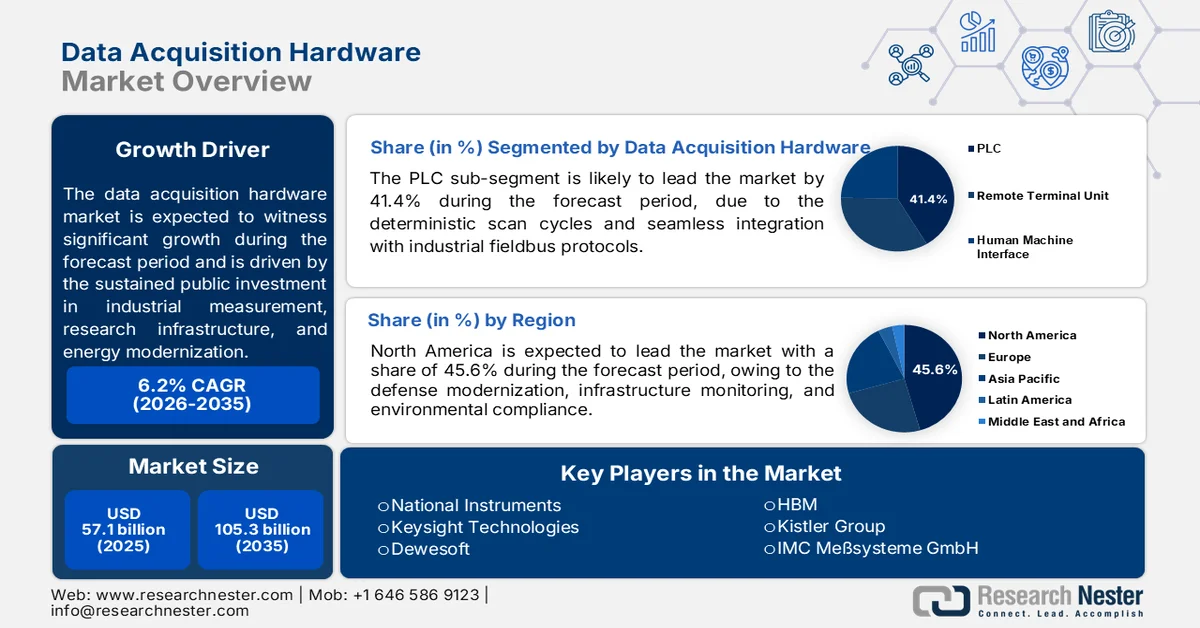

Data Acquisition Hardware Market size was valued at USD 57.1 billion in 2025 and is projected to reach USD 105.3 billion by the end of 2035, witnessing around 6.2% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of data acquisition hardware is estimated at USD 60.7 billion.

The data acquisition hardware market is being supported by sustained public investment in industrial measurement, research infrastructure, energy modernization, and advanced manufacturing programs. According to the Columbia University School of Professional Studies January 2026 data, total U.S. research and experimental development (R&D) expenditures reached approximately USD 940 billion, reflecting continued expansion of laboratory, testing, and instrumentation-intensive activities across government, academic, and industrial environments. These programs require reliable collection of operational, environmental, electrical, and process data for validation, compliance, and performance monitoring.

In manufacturing, the U.S. National Institute of Standards and Technology (NIST) March 2026 data reports that the manufacturing sector contributed USD 2.93 trillion to the U.S. economy, highlighting the scale of production facilities that increasingly depend on equipment monitoring and process-control systems. Demand is also being reinforced by federal initiatives supporting digitalized production, quality assurance, and industrial productivity improvements. Organizations operating in aerospace, defense, automotive, electronics, and pharmaceutical production continue to expand data collection capabilities to improve traceability and meet regulatory requirements. As industrial operators pursue higher asset utilization and lower downtime, procurement activity increasingly includes hardware capable of supporting continuous measurement and integration with plant-wide monitoring systems.

Key Data Acquisition Hardware Market Insights Summary:

Regional Highlights:

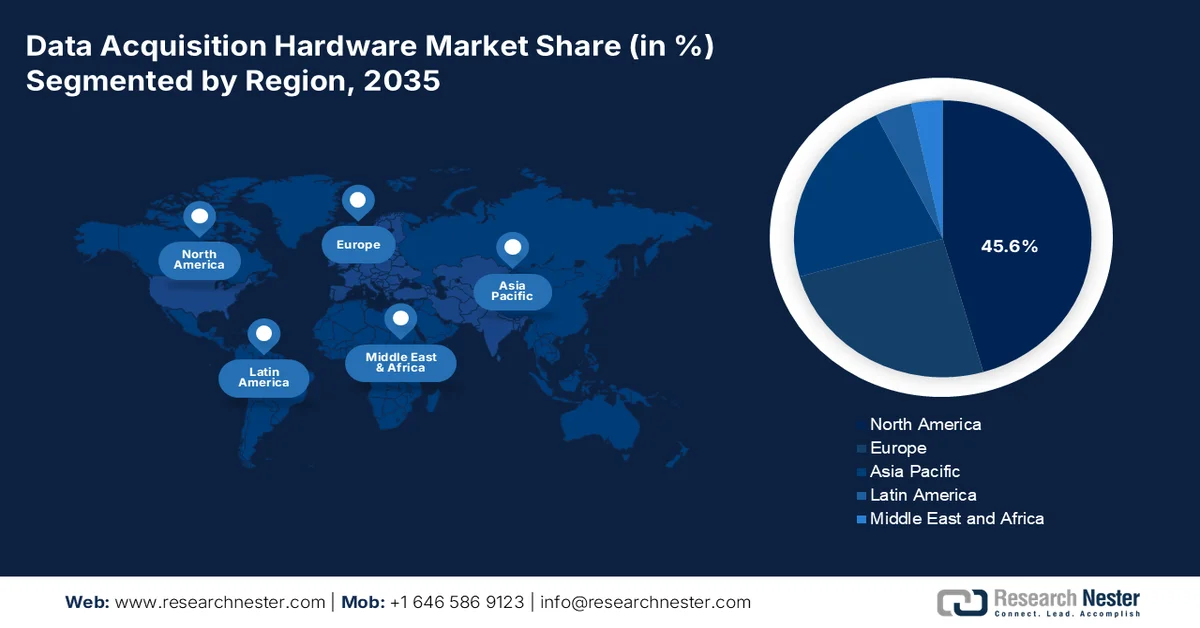

- In the data acquisition hardware market, North America is anticipated to capture a 45.6% revenue share by 2035, underpinned by rising defense modernization programs, infrastructure monitoring requirements, and stringent environmental compliance standards

- Asia Pacific is forecast to witness rapid expansion during 2026-2035, fueled by accelerating industrialization, growing electronics manufacturing capacity, and aggressive automotive electrification policies

Segment Insights:

- In the data acquisition hardware market, the PLC segment is projected to account for a 41.4% share by 2035, buoyed by ruggedized reliability, deterministic scan cycles, and seamless integration with industrial fieldbus protocols such as Profinet and EtherCAT

- Modular/PC-based DAQ systems are expected to maintain a significant position throughout 2026-2035, strengthened by reconfigurable channel counts and real-time PC-hosted processing capabilities

Key Growth Trends:

- Expansion of electric grid modernization programs

- Rising public investment in semiconductor manufacturing

Major Challenges:

- High R&D costs

- Stringent regulatory and certification compliance

Key Players: National Instruments (NI), Keysight Technologies, Dewesoft, HBM (Hottinger Brüel & Kjær), Kistler Group, IMC Meßsysteme GmbH, Acqiris SA, Emerson.

Global Data Acquisition Hardware Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 57.1 billion

- 2026 Market Size: USD 60.7 billion

- Projected Market Size: USD 105.3 billion by 2035

- Growth Forecasts: 6.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.6% share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: U.S., China, Germany, Japan, Canada

- Emerging Countries: India, South Korea, Brazil, Mexico, Vietnam

Last updated on : 23 June, 2026

Data Acquisition Hardware Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of electric grid modernization programs: Government-backed grid modernization initiatives are creating sustained demand for data acquisition hardware used in substations, transmission networks, distributed energy resources, and grid monitoring systems. Utilities increasingly require high-frequency data collection to manage grid stability, renewable integration, and predictive maintenance. In the U.S., the Department of Energy (DOE) in October 2023 announced up to USD 3.9 billion through the Grid Resilience and Innovation Partnerships (GRIP) Program, one of the largest federal investments in grid modernization. These projects involve large-scale deployment of sensors, monitoring equipment, and real-time operational data systems. Data acquisition hardware serves as a foundational layer for capturing electrical, environmental, and asset-performance data across transmission and distribution networks.

- Rising public investment in semiconductor manufacturing: Semiconductor fabrication facilities depend on extensive process monitoring, environmental control, and equipment-performance measurement, all of which require advanced data acquisition hardware. Government incentives for domestic semiconductor production are expanding demand for industrial instrumentation and test infrastructure. As per the NGA March 2025 data, the U.S. Department of Commerce allocated over USD 39 billion in CHIPS Act manufacturing incentives to strengthen domestic semiconductor production. Semiconductor plants require thousands of measurement points to monitor temperature, pressure, vibration, power quality, and contamination levels throughout production lines. Data acquisition systems help manufacturers achieve process consistency and yield optimization.

Challenges

- High R&D costs: Developing precision DAQ hardware requires substantial investment in analog front-end design, high-resolution ADCs, and low-noise PCB layouts. New entrants struggle to match the performance of established players without years of iterative prototyping. The need for firmware development and compliance with multiple communication protocols further inflates budgets. Smaller firms often exhaust capital before achieving market-ready products, while incumbents benefit from economies of scale and amortized engineering costs.

- Stringent regulatory and certification compliance: DAQ hardware used in aerospace, medical, and automotive applications must meet rigorous standards like ISO 13485, DO-160, or IEC 61010. Achieving these certifications is time-consuming and expensive, often requiring third-party testing and documentation. New entrants face delays in market access, while established manufacturers leverage pre-certified platforms. The fragmented regulatory landscape across regions USA, Europe, and Asia, compounds complexity, forcing suppliers to maintain multiple product variants.

Data Acquisition Hardware Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.2% |

|

Base Year Market Size (2025) |

USD 57.1 billion |

|

Forecast Year Market Size (2035) |

USD 105.3 billion |

|

Regional Scope |

|

Data Acquisition Hardware Market Segmentation:

Data Acquisition Hardware Segment Analysis

The data acquisition hardware segment is driven by the PLC subsegment and is poised to hold the share value of 41.4% by the end of 2035. The segment is driven by their ruggedized reliability, deterministic scan cycles, and seamless integration with industrial fieldbus protocols like Profinet and EtherCAT. Modern PLCs now embed high-resolution analog inputs, onboard signal conditioning, and edge-computing capabilities, enabling real-time predictive maintenance in factories, power plants, and water treatment facilities. Their dominance is reinforced by the global installed base of legacy automation systems, where PLC-based DAQ provides the most cost-effective upgrade path for Industry 4.0 digital transformation initiatives.

Product Type Segment Analysis

Modular/PC-based DAQ systems dominate the data acquisition hardware market due to their reconfigurable channel counts and real-time PC-hosted processing, as exemplified by the Neurostim-3 system for simultaneous neural stimulation and recording. This modular architecture controls up to 512 independent bidirectional channels via custom ASICs and commercial Multi-Electrode Arrays, all without precomputed data—even under demanding experimental loads. The system achieves signal gain linearity across wide amplitude ranges and a high-pass cutoff near 0.6 Hz, enabling concurrent Local Field Potential and spiking activity capture from living rat brain tissue, as per NLM June 2021 study. Furthermore, its current stimulation circuitry reproduces complex patterns, proving that modular PC-based designs efficiently handle both recording and closed-loop stimulation. This validates that modular DAQ platforms—originally developed for industrial test—are equally transformative for advanced biomedical research, expanding their addressable market beyond traditional automation.

Application Segment Analysis

The automotive & EV Testing segment commands the largest share of the data acquisition hardware market, driven by national electrification mandates such as India's goal to achieve 30% electric vehicle penetration by 2030, as per the NITI August 2025 data. This policy accelerates demand for high-channel-count DAQ systems to validate battery thermal runaway, motor efficiency, and regenerative braking under real-world drive cycles. Indian OEMs and testing laboratories are rapidly procuring modular DAQ platforms with isolated high-voltage inputs and synchronized current shunts to comply with safety standards. The sheer volume of prototype vehicles requiring exhaustive testing—from cell-level formation to full-vehicle durability—creates sustained procurement cycles for precision measurement hardware, positioning automotive applications as the growth engine for DAQ suppliers targeting emerging EV manufacturing hubs.

Our in-depth analysis of the data acquisition hardware market includes the following segments:

|

Segment |

Subsegments |

|

Data Acquisition Hardware |

|

|

Product Type |

|

|

Input Signal Type |

|

|

Application |

|

|

End user |

|

|

Connectivity |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Data Acquisition Hardware Market - Regional Analysis

North America Market Insights

North America is dominating the data acquisition hardware market and is expected to hold the regional revenue share of 45.6% by the end of 2035. The region is driven by mature demand driven by defense modernization, infrastructure monitoring, and environmental compliance. The U.S. dominates regional spending through federal procurement channels, with the Department of Defense, Department of Energy, and Environmental Protection Agency constituting primary end-user segments. Canada contributes through transport safety monitoring, clean energy grid upgrades, and natural resource extraction automation. Both countries enforce rigorous certification standards—MIL-STD, CSA, and EPA protocols—which elevate barriers for new entrants. The market exhibits steady replacement cycles as legacy systems migrate toward modular, network-enabled platforms with wireless telemetry.

The expanding industrial capacity, energy-system monitoring requirements, and infrastructure digitization initiatives is driving the data acquisition hardware market in the U.S. A key demand indicator is the continued growth in manufacturing investments; according to the U.S. Census Bureau, annual manufacturing construction spending is reflecting large-scale development of production facilities that require process monitoring, testing, and operational data collection systems. In parallel, the U.S. Energy Information Administration (EIA) June 2025 projects U.S. electricity consumption in 2024 Q1 to increase to 977 billion kWh, highlighting the need for enhanced grid monitoring, power-quality measurement, and asset-performance tracking across utilities and industrial users. These trends are encouraging procurement of data acquisition hardware across manufacturing plants, energy networks, research facilities, and critical infrastructure environments.

The investments in industrial modernization, energy infrastructure, and research-intensive sectors requiring continuous monitoring and operational data collection is shaping the data acquisition hardware market in Canada. The capital investments in major energy projects under construction is creating demand for monitoring systems across power generation, transmission, and resource operations. Additionally, Government of Canada December 2024 reported that national expenditures on research and development reached approximately CAD 51.7 billion, reflecting growing activity in laboratories, advanced manufacturing facilities, and technology development centers that rely on precision measurement and data acquisition equipment. These investments are strengthening demand for hardware solutions used in industrial automation, asset performance monitoring, testing environments, and critical infrastructure management.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the data acquisition hardware market. the region is driven by the rapid industrialization, electronics manufacturing expansion, and aggressive automotive electrification policies. China leads in production-scale test equipment for semiconductor and EV battery assembly lines, while Japan contributes through precision instrumentation for robotics and automotive R&D. India's emerging EV testing infrastructure and South Korea's semiconductor fabrication facilities generate sustained demand for high-channel-count DAQ systems. The market remains price-sensitive, with domestic manufacturers offering cost-competitive alternatives to Western brands, while multinational suppliers differentiate through certification support and application engineering services.

The expanding industrial automation, power infrastructure upgrades, and public investment in electronics manufacturing is driving the data acquisition hardware market in India. According to the PIB October 2025 data, India’s electronics production reached INR 11.3 lakh crore, reflecting substantial growth in manufacturing facilities that require process monitoring, testing, and real-time data collection systems. Additionally, the PIB June 2025 data reported that India’s total installed power generation capacity increased to approximately 476 GW, creating greater demand for grid monitoring, asset diagnostics, and operational data acquisition across generation and transmission networks. These developments are supporting wider adoption of data acquisition hardware in manufacturing plants, utilities, transportation infrastructure, and industrial research environments.

The investments in industrial automation, advanced manufacturing, and energy infrastructure is shaping the data acquisition hardware market in China. According to the People’s Republic of China April 2026 data, the country's high-tech manufacturing value-added output grew by 8.9% year-on-year, outpacing overall industrial production and increasing demand for process monitoring and data collection systems across factories. In addition, the People’s Republic of China January 2025 data reported that China’s total installed power generation capacity reached approximately 3.35 billion kilowatts, reflecting substantial expansion of power generation assets requiring continuous performance monitoring and grid management. These developments are driving adoption of data acquisition hardware across manufacturing facilities, utilities, transportation infrastructure, and industrial research environments, supporting long-term demand for reliable measurement and monitoring solutions.

Europe Market Insights

The data acquisition hardware market in Europe is shaped by stringent environmental regulations, automotive testing mandates, and renewable energy integration. The European Union's Industrial Emission Directive drive continuous emissions monitoring and vehicle validation, requiring high-precision DAQ systems across manufacturing and transport sectors. Germany, France, and the UK lead in aerospace, wind energy, and railway condition monitoring, while Nordic countries prioritize hydropower and grid stability applications. The market emphasizes compliance with CE marking, IEC 61010 safety standards, and RoHS directives, raising certification barriers for non-European suppliers. Replacement cycles align with regulatory updates, creating predictable but fragmented demand across member states.

The strong industrial base, energy-transition initiatives, and continued investment in research infrastructure is driving the data acquisition hardware market in Germany. According to the DWIH June 2025 data, expenditures on research and development reached approximately EUR 129.7 billion in 2023, highlighting substantial activity across industrial laboratories, engineering centers, and technology development facilities that depend on advanced measurement and data collection systems. Additionally, the EMBER April 2026 reported that renewable energy sources accounted for approximately 59% of Germany’s gross electricity generation in the first half of 2024, increasing the need for monitoring and control systems across distributed energy assets and grid infrastructure. These trends are driving demand for data acquisition hardware in manufacturing, energy, transportation, and scientific research applications.

The investment in research-intensive industries, infrastructure monitoring, and energy-system modernization is driving the data acquisition hardware market in the UK. UK's gross domestic expenditure on research and development (GERD) is supporting demand for advanced measurement and data collection systems across laboratories, engineering facilities, and industrial testing environments. Additionally, the Renewable UK 2024 reported that renewable sources generated approximately 50.8% of the UK's electricity, increasing requirements for real-time monitoring, grid management, and performance measurement solutions across power networks. These developments are encouraging broader adoption of data acquisition hardware in manufacturing, energy, transportation, and scientific research sectors, supporting sustained market growth.

Key Data Acquisition Hardware Market Players:

- National Instruments (NI) (U.S.)

- Keysight Technologies (U.S.)

- Dewesoft (Slovenia)

- HBM (Hottinger Brüel & Kjær) (Germany)

- Kistler Group (Switzerland)

- IMC Meßsysteme GmbH (Germany)

- Acqiris SA (Switzerland)

- Emerson (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- NI is a dominant force in the data acquisition hardware market, pioneering modular PXI and CompactDAQ platforms that integrate seamlessly with its LabVIEW software ecosystem. The company has strategically shifted from pure hardware sales to subscription-based software and system-level solutions, targeting semiconductor validation, EV battery testing, and aerospace telemetry.

- Keysight commands a premium segment of the data acquisition hardware market, leveraging its heritage in high-frequency oscilloscopes and digitizers. Its DAQ solutions, ranging from benchtop multimeters to high-speed A/D modules—are engineered for extreme dynamic range and low noise, critical for radar, quantum computing, and 5G infrastructure testing. In 2024, the company has made a revenue of USD 5,375 million.

- Dewesoft has disrupted the data acquisition hardware market with its philosophy of “all-in-one” portable data loggers that combine voltage, CAN bus, thermocouple, and vibration inputs in rugged, battery-powered chassis.

- HBM (now part of HBK) in the data acquisition hardware market is synonymous with precision strain-gauge and torque sensors, paired with its QuantumX and SomatXR DAQ families. These systems are ruggedized for aerospace, wind energy, and heavy machinery testing, offering galvanically isolated inputs and 24-bit resolution.

- Kistler holds a specialized yet influential position in the data acquisition hardware market, centered on piezoelectric pressure, force, and acceleration sensors, coupled with its own KiDAQ modular data loggers. These systems are critical for combustion analysis, injection system testing, and high-speed crash dynamics. In 2024, the company has made a sales of CHF 465 million.

Here is a list of key players operating in the global data acquisition hardware market:

The global data acquisition hardware market is moderately fragmented, dominated by diversified test & measurement giants alongside specialized niche players. Key strategies include deep integration with software ecosystems, expansion into IIoT and edge computing, and development of high-speed modular systems for 5G and EV testing. Acquisitions are frequent to consolidate technology in areas like signal conditioning and wireless telemetry. To counter supply chain pressures, leaders are regionalizing production and enhancing direct digital sales channels. Simultaneously, Asian manufacturers are aggressively competing on cost and high-volume portable units, while Western firms focus on precision, ruggedized solutions for aerospace and defense.

Corporate Landscape of the Market:

Recent Developments

- In January 2026, Acqiris SA announced the launch of the SA6, which is a new high-performance compact 12-bit data acquisition (DAQ) solution developed to meet the requirements of Swept-Source Optical Coherence Tomography (SS-OCT) systems for image quality, size, and cost.

- In September 2024, Emerson expanded its NI™ USB data acquisition (DAQ) product line with the new NI mioDAQ device. The NI mioDAQ solution offers improved measurement performance, more powerful software and an easier setup experience.

- In June 2023, imc Test & Measurement, a brand of Axiometrix Solutions, has announced the launch of its new modular data acquisition system imc ARGUSfit. The imc ARGUSfit base unit and additional amplifier and fieldbus interface modules, are clicked together providing ultimate flexibility in vehicle and monitoring and machine testing.

- Report ID: 8621

- Published Date: Jun 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.