Cutaneous Radiation Injury Treatment Market - Regional Analysis

North America Market Insights

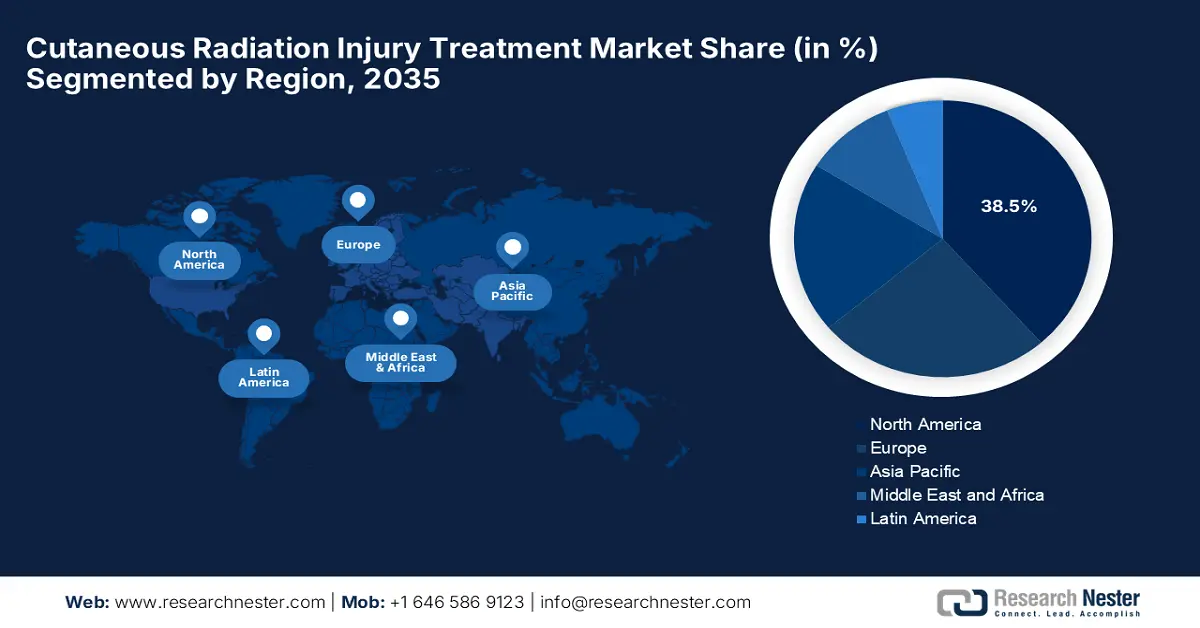

North America is dominating the market and is projected to capture the largest share of 38.5% by 2035. The region benefits from an advanced healthcare infrastructure and substantial reimbursement policies. According to the U.S. Department of Health & Human Services, agencies like the Biomedical Advanced Research and Development Authority provide a significant funding for the development and procurement of medical countermeasures, including treatments for radiation exposure. Furthermore, telemedicine adoption is anticipated to grow post-radiation follow-ups, thereby denoting a positive market outlook.

The U.S. is the dominating player in the market, highly fueled by the military and oncology demand. As per the NLM study in March 2022, almost 650,000 cancer patients in the U.S. undergo radiotherapy and they experience skin injuries and need to undertake cutaneous radiation injury treatment. Various researches on stem cell therapies and hydrogel system are conducted to cure the skin injuries related to radiation. The presence of key market players and their innovative strategies positions the U.S. as the global hotspot in this field.

Canada represents exceptional growth in the cutaneous radiation injury treatment market, owing to the federal and provincial allocations. Testifying this the CMA report in October 2022 stated that Canada spends more than USD 300 million on healthcare, including emergency preparedness and radiation incident management. Besides Public Health Agency of Canada prioritizes stockpiling silver dressings, whereas Alberta’s tele-radiotherapy program cuts rural disparities, providing a prolific market opportunity. These coordinated federal and provincial initiatives are surging nationwide adoption of advanced cutaneous radiation injury treatments, solidifying Canada’s position as a key growth market.

APAC Market Insights

Asia Pacific market is likely to exhibit the fastest growth at a CAGR of 6.5% from 2026 to 2035. The growing radiotherapy adoption, nuclear energy expansion, and government-backed programs are key factors propelling this progress. Governments across this region are proactively contributing to this expansion with a collective goal to enhance healthcare services and encourage innovation. Besides KIRAM's advances in stem cell therapies on the other hand Malaysia’s Nuclear Agency focuses on emergency response training, thus suitable for standard market growth.

China is augmenting its dominant position in the cutaneous radiation injury treatment market, grabbing a significant regional share on account of government-backed R&D and radiotherapy demand. As evidence, the Royal Society of Chemistry study published in December 2023 states that hydrogel based treatment on wound has achieved an exception efficiency in minimizing the growth of bacteria by 99%. Besides, the country is a manufacturing hub of APIs, effectively supported by the production of topical agents and biologics. Furthermore, the Healthy China 2030 initiative prioritizes nuclear emergency preparedness for CRI dressings and systemic therapies.

India is propagating in the regional cutaneous radiation injury treatment market, effectively driven by generic drug production and expanding radiotherapy access. In this regard, the PRS Legislative Research for 2025 to 2026 has stated that the Rs 99,859 crore was allocated by the Ministry for healthcare budget, which is expected to rise by 11% in the next year. Besides the CDSCO-EMA collaboration in 2024, has accelerated the approvals for CRI generics, benefiting million patients. The National Cancer Grid aims to bridge this by doubling CRI treatment centers. In addition, Mylan NV reduced prices by emphasizing domestic API manufacturing and reinforcing the country’s position in the worldwide landscape.

Europe Market Insights

Europe is expected to retain its position as the second-largest stakeholder in the global market owing to the rising demand for radiotherapy, nuclear safety protocols, and nationwide healthcare initiatives. The funding grants also contribute to standard development with the EU’s Health Data Space investing in cutaneous radiation injury research & development, as stated by EC 2024 data. Also, the EMA fast-tracked CRI therapies in 2024, thus attracting both national and international players to invest in this sector.

Germany leads the Europe’s market with significant revenue share, mainly driven by substantial healthcare spending and a vast patient base. The Federal Ministry of Health and the Robert Koch Institute are key bodies responsible for stockpiling and response planning. Besides the Destatis report in April 2022 depicts that there is a rise of 81% in skin cancer due to high radiation. Furthermore, the domestic players, such as Siemens Healthineers, lead in terms of innovation with IoT-enabled CRI monitors.

The U.K. is demonstrating strong growth in the regional cutaneous radiation injury treatment market. Market demand is defined by the maintenance of the UK's national stockpile of medical countermeasures. According to a UK government review of health emergency preparedness, funding for these capabilities has been prioritized, with a significant portion of the dedicated health security budget allocated to procuring and replenishing CRI treatments to ensure national resilience. Therefore, all of these factors appreciably amplify financial outputs from this sector.