Customer Analytics Market Outlook:

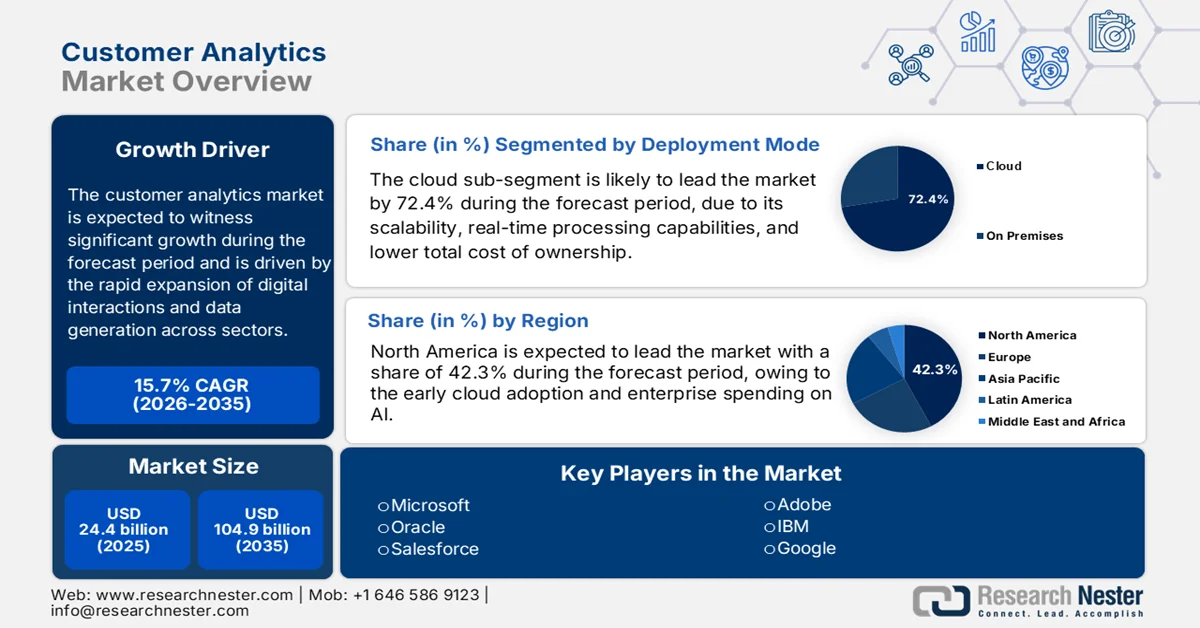

Customer Analytics Market size was valued at USD 24.4 billion in 2025 and is projected to reach USD 104.9 billion by the end of 2035, growing at a CAGR of 15.7% during the forecast period 2026 to 2035. In 2026, the industry size of customer analytics is assessed at USD 28.2 billion.

Enterprise investment in customer analytics is closely tied to the rapid expansion of digital interactions and data generation across sectors. According to the U.S. Census Bureau, March 2026 data indicates that the e-commerce sales reached over USD 1,233.7 billion in 2025, reflecting a sustained growth in digital transaction volumes that enterprises must analyze to manage customer acquisition and retention strategies. At the same time, the International Telecommunication Union's October 2023 data indicates that the global internet penetration exceeded 67% in 2023, representing more than 5.4 billion users generating continuous behavioral and transactional data streams. This scale of digital engagement is pushing organizations to strengthen analytics capabilities to support pricing optimization, demand forecasting, and customer lifecycle management.

Internet Penetration, 2023

|

Year |

People Using Internet Worldwide (billion) |

Percentage of Internet Users |

|

2019 |

4.1 |

53 |

|

2020 |

4.6 |

59 |

|

2021 |

4.9 |

62 |

|

2022 |

5.1 |

64 |

|

2023 |

5.4 |

67 |

Source: International Telecommunication Union October 2023

Data governance requirements and sector-specific compliance mandates are also shaping the enterprise adoption patterns. The National Institute of Standards and Technology highlights that effective data management frameworks are central to risk mitigation and operational efficiency, mainly as organizations handle large-scale personal and transactional datasets. Similarly, the AIS eLibrary March 2024 data indicates that the 80% of businesses consider data and analytics as important for their business to improve operational performance, with regulatory frameworks such as GDPR influencing how customer data is collected, processed, and analyzed. These factors collectively reinforce a customer analytics market environment where enterprises are prioritizing scalable analytics systems aligned with compliance workforce capabilities and measurable financial outcomes.

Key Customer Analytics Market Insights Summary:

Regional Highlights:

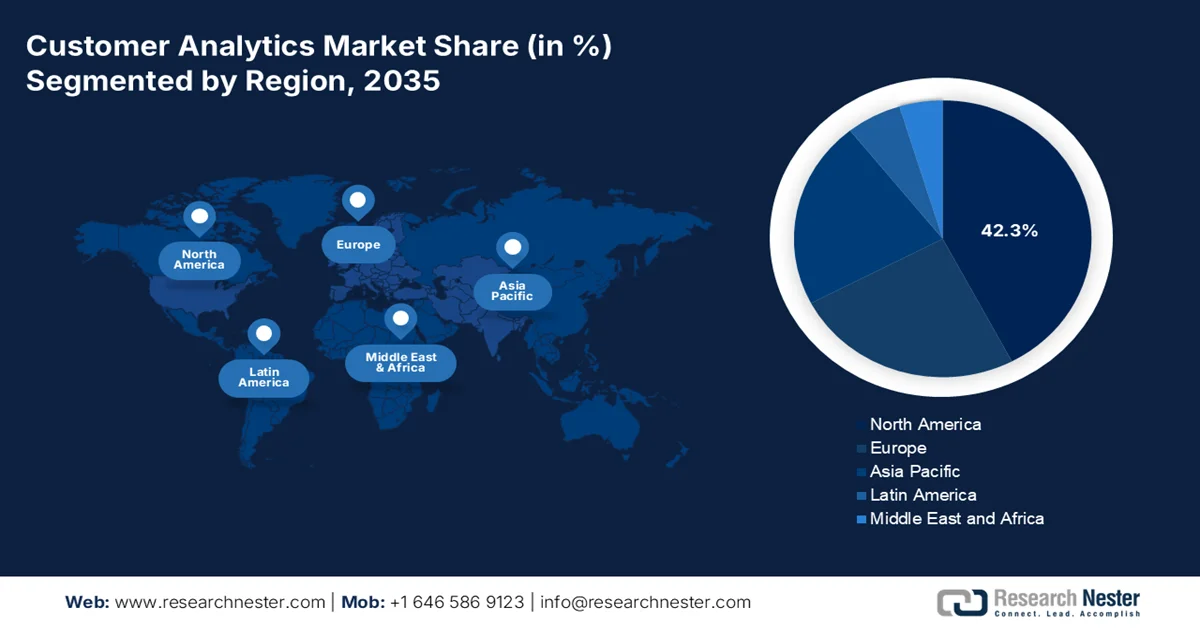

- North America is projected to dominate the customer analytics market with a 42.3% share by 2035, fueled by early cloud adoption and strong enterprise AI investments

- Asia Pacific is anticipated to register the fastest growth in the market at a CAGR of 18.5% during 2026-2035, propelled by government-backed AI infrastructure expansion and rising mobile-first data adoption

Segment Insights:

- Cloud deployment in the customer analytics market is expected to capture a 72.4% share by 2035, driven by scalability, real-time processing capabilities, and lower total cost of ownership

- Software segment is projected to hold the largest share by 2035, supported by growing adoption of AI-driven analytics platforms and increasing enterprise investment in in-house data capabilities

Key Growth Trends:

- Expansion of government digital service spending

- Growth in smart city and urban data investments

Major Challenges:

- Shortage of skilled analytics talent

- High integration costs

Key Players: Microsoft (U.S.), Oracle (U.S.), Salesforce (U.S.), Adobe (U.S.), IBM (U.S.), Google (U.S.), SAS Institute (U.S.), Teradata (U.S.), SAP (Germany), Qualtrics (U.S.), NICE Systems (France), Zoho (India), Freshworks (India), Hitachi (Japan), Fujitsu (Japan), Pegasystems (U.S.), Accenture (Ireland).

Global Customer Analytics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 24.4 billion

- 2026 Market Size: USD 28.2 billion

- Projected Market Size: USD 104.9 billion by 2035

- Growth Forecasts: 15.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, South Korea, Singapore, Brazil, United Arab Emirates

Last updated on : 30 April, 2026

Customer Analytics Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of government digital service spending: Rising public investment in the digital service delivery is directly increasing the demand for customer analytics capabilities within the enterprise ecosystems that support government-facing services. According to the GAO July 2025 data, the U.S. Federal Government allocated over USD 100 billion annually to IT spending with a strong focus on citizen-facing digital services and data optimization. Similarly, the EU’s Digital Europe Programme prioritizes advanced data utilization and analytics infrastructure. These investments require vendors and contractors to deploy analytics tools to monitor service usage, improve engagement, and optimize outcomes. Enterprises aligning solutions with government procurement standards, mainly in data interoperability and performance measurement, are better positioned to capture long-term contracts and recurring revenue streams tied to national digital transformation agendas.

- Growth in smart city and urban data investments: Smart city programs are generating high volumes of citizen interaction data, creating a downstream demand for customer analytics across utilities, mobility, and public services. According to the IBEF November 2025 data, the Government of India’s Smart Cities Mission has committed over USD 19.14 billion to urban digital infrastructure. Similarly, the U.S. Department of Transportation has invested in smart mobility initiatives requiring data analytics for user behavior and system optimization. These initiatives rely on private sector vendors to deploy an analytics platform that interprets user data, improves service delivery, and enhances operational efficiency. Companies that can integrate with public infrastructure projects and deliver measurable performance improvements are likely to see sustained demand.

- Digital skills growth: The development of workforce initiatives is stimulating the analytics adoption by expanding the skilled professionals. According to the BLS August 2025 data, there is a 34% growth in the data science roles, reflecting a strong demand for analytics expertise. Moreover, the European Social Fund Plus allocates significant funding to digital skills training across the member states. These programs enable enterprises to scale the analytics operations by addressing the talent shortages. For solution providers, this trend supports the broader adoption of analytics platforms as organizations gain the internal capability to implement and manage them. Companies that offer training support and user-friendly interfaces are better positioned to capitalize on this driver as workforce readiness becomes a critical factor in technology adoption decisions.

Challenges

- Shortage of skilled analytics talent: Entering the customer analytics market is severely constrained by a global shortage of professionals who possess both technical data science skills and business acumen. Manufacturers cannot simply deploy software; they need an analyst who can translate the customer behavioral patterns into actionable retention and personalization strategies. Without these hybrid professionals, even the most advanced analytics platforms remain underutilized, delivering dashboards instead of strategic customer insights.

- High integration costs: New manufacturers entering the customer analytics market face prohibitive costs when attempting to integrate a modern analytics platform with decades-old legacy infrastructure. These systems were never designed for real-time data ingestion API based connectivity or unified customer profiles requiring expensive middleware, custom coding, and lengthy migration projects. Though the market is projected to grow, businesses have not fully centralized their customer data due to these integration burdens.

Customer Analytics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

15.7% |

|

Base Year Market Size (2025) |

USD 24.4 billion |

|

Forecast Year Market Size (2035) |

USD 104.9 billion |

|

Regional Scope |

|

Customer Analytics Market Segmentation:

Deployment Mode Segment Analysis

Within the deployment mode, the cloud is leading and is poised to hold the largest share value of 72.4% by the end of 2035 in the customer analytics market. Cloud deployment has become the dominant mode in the customer analytics market due to its scalability, real-time processing capabilities, and lower total cost of ownership. The enterprises stimulated the migration from on-premises systems to public, private, and hybrid cloud environments to unify customer data from web, mobile, and IoT sources. Cloud native analytics platforms enable automatic updates, AI integration, and cross-departmental data sharing, which are critical for personalization and churn prediction. Recent advancements, such as in March 2026, CVS Health and Google Cloud announced a new strategic partnership that aims to reimagine health care experiences, increase customer engagement, and ultimately support better health outcomes. These partnerships are driving the real-time customer journey tracking, which directly impacts retention and revenue.

Component Segment Analysis

Under the component segment, the software sub-segment is expected to hold the largest share value in the customer analytics market, encompassing customer data platforms, analytics dashboards, and AI-driven predictive engines. The organizations prioritized investments in standalone analytics software over professional services due to the expansion of user-friendly no-code tools that empower business teams directly. Software solutions now integrate seamlessly with CRM marketing automation, and ecommerce platforms, enabling automated segmentation, next best action recommendations, and lifetime value modeling. The National Telecommunication and Information Administration has indicated that firms have increased their spending on customer analytics software. This highlights a strategic shift toward in-house software-driven analytics capabilities that offer faster iteration, lower marginal costs, and greater data governance control, solidifying software as the dominant component.

Enterprise Size Segment Analysis

Large enterprises dominate the customer analytics market because they possess the data volume, infrastructure budget, and cross-functional teams required to deploy advanced predictive and behavioral analytics. The large organization stimulated the adoption of an AI-driven customer platform to reduce churn and personalize omnichannel experiences at scale. A significant catalyst is government-backed AI infrastructure, such as the IndiaAI Mission, which allocated over USD 1.24 billion over the five years with 38,000 GPUs deployed for enterprise-grade AI research and commercial applications, according to the PIB December 2025 data. This national compute resource lowers the cost barrier for India's large enterprises in BFSI, telecom, and retail to train complex customer churn and lifetime value models on hundreds of millions of records.

Our in-depth analysis of the customer analytics market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Deployment Mode |

|

|

Enterprise Size |

|

|

Application |

|

|

End use Industry |

|

|

Analytics Type |

|

|

Function |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Customer Analytics Market - Regional Analysis

North America Market Insights

North America is dominating the global customer analytics market and is expected to hold the regional revenue share of 42.3% during the projected timeframe. The U.S. dominates the regional revenue share due to early cloud adoption and enterprise AI spending. The primary drivers include federal cloud mandates, NIST predictive analytics standardization, and FTC first-party data enforcement. According to the World Intellectual Property Organization, June 2025 data indicates that the software spending in the U.S. reached USD 368.5 billion. Government spending flows via GSA FedRAMP procurement and NIH healthcare analytics programs. Canada’s contribution grows via localized privacy regulations and public sector citizen journey analytics. Moreover, the requirement of analytics professionals with both technical and business domain expertise continues to demand the deployment of a customer analytics platform across both countries.

High frequency digital engagement across federal platforms, reinforcing the enterprise demand for scalable analytics capabilities, is shaping the customer analytics market in the U.S. According to the Analytics.USA 2026 data, the U.S. Federal Government analytics data shows over 1 million active users and 2.9 million total views within a 30-minute window, indicating a substantial real-time interaction volume that requires continuous monitoring and optimization. Additionally, more than 562,000 first-time users in the same period highlight ongoing user acquisition dynamics that drive the need for segmentation and behavioral analysis. Moreover, nearly 528,000 publicly available datasets, as per the Data.gov April 2026 article, enable organizations to enrich customer models and improve decision accuracy. These factors support sustained investment in the analytics solutions aligned with the public sector digital infrastructure and enterprise data integration strategies.

Number of Datasets, 2026

|

Metric |

Number |

|

City Government |

10471 |

|

Country Government |

2735 |

|

Federal Government |

504661 |

|

State Government |

10739 |

Source: Data.gov April 2026

The expanding digital adoption, strong public data infrastructure, and government-backed innovation program are shaping the customer analytics market in Canada. According to the ITA July 2025 data, the retail e-commerce sales in 2024 reached USD 3.14 billion, reflecting sustained digital transaction volumes that require advanced analytics for customer insights. Additionally, the CIGI April 2026 data indicated that the Government of Canada allocated USD 2 billion Canadian Sovereign AI Compute Strategy to strengthen the data-driven capabilities across industries. Moreover, the total number of datasets by the Government of Canada in April 2026 was 46,843, enabling enterprises to integrate public data into customer models and forecasting tools. These factors are driving enterprise investment in analytics solutions to enhance customer targeting, improve retention strategies, and align with national digital transformation priorities.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region and is poised to expand at a CAGR of 18.5% during the assessed period, 2026 to 2035. The customer analytics market is defined by the extreme diversity of mobilizing giants such as India and China, each with distinct regulatory and infrastructural realities. Privacy compliance often dominates the conversation. APAC markets prioritize scalability, real-time processing of massive mobile-first behavioral data, and alignment with national AI compute subsidies. Government across the region actively funds domestic analytics infrastructure via data localization laws, cloud migration mandates, and state-backed AI research programs, making public sector procurement a significant demand driver. Telecommunications, retail, healthcare, and financial services lead adoption rapidly as the aging population and public health infrastructure modernization surge the investment.

The rapid platform digitization, large-scale identity-linked data systems, and sustained public investment in digital infrastructure are fueling the customer analytics market in India. According to the PIB October 2024 data, the Unique Identification Authority of India reported over 138.04 crore, creating a foundational dataset for identity-linked service delivery and customer profiling. The PIB January 2025 data indicates that over 16,730 million UPI transactions were recorded in 2024, reflecting a massive volume of real-time consumer interaction data. Additionally, the IBEF January 2025 data indicates that the number of internet users will exceed 900 million in 2025, indicating broad-based digital access and data generation. These factors are reinforcing the enterprise demand for an analytics platform to manage high-volume customer data, improve targeting accuracy, and support scalable data-driven engagement models.

Large scale digital consumption, expanding connectivity, and a strong government-backed data infrastructure are fueling the customer analytics market in China. According to the People’s Republic of China, January 2025 data indicates that the online retail sales reached USD 2.15 trillion in 2024, indicating high volumes of digital transactions requiring advanced analytics. Moreover, China noted that the number of internet users exceeded 1.1 billion, reflecting extensive digital engagement and continuous data generation. Additionally, the China Internet Network Information Center's January 2025 data depicts that the mobile internet traffic exceeded 306.6 billion GB in 2024, highlighting the scale of the data consumption across platforms. These trends are driving the enterprise investment in analytics solutions to improve customer targeting, enhance engagement strategies, and support data-driven decision-making across sectors.

Mobile Internet Access Traffic, 2025

|

Year |

Unit (100 million GB) |

|

2020 |

1656 |

|

2021 |

2216 |

|

2022 |

2618 |

|

2023 |

3015 |

|

2024 |

3066 |

Source: China Internet Network Information Center January 2025

Europe Market Insights

The customer analytics market in Europe is shaped by a complex interplay of stringent privacy regulations, fragmented national implementations of GDPR, and increasing public sector demand for citizen journey analytics. Cloud adoption and enterprise AI spending dominate the region; moreover, the organizations prioritize compliance first, analytics platforms that embed consent management, data minimization, and right to erasure functionalities directly into customer data processing workflows. Recent advancements in the customer analytics market, such as in June 2025, ATLANTA & LISBON announced its acquisition of Climber, are driving the expansion of the market. The continent’s diverse regulatory landscape, encompassing the EU Digital Services Act, the proposed AI Act, and national data protection authority interpretations, pushes the analytics vendors to offer highly configurable deployment options rather than standard solutions.

Strong digital infrastructure, industrial data usage, and expanding public data ecosystems are driving the customer analytics market in Germany. According to ITA August 2025 data, nearly 90% of the companies in Germany are using the cloud in their business, reflecting the continued digitalization of business processes and increased data generation. Moreover, the e-commerce revenue in Germany exceeded USD 100.6 billion, indicating high volumes of digital transactions requiring advanced analytics for customer targeting and retention. Besides, the enterprises are increasingly prioritizing integrated data environments to unify customer information across channels and improve decision consistency. The growing emphasis on regulatory compliance and data governance is also supporting the adoption of structured analytics frameworks to ensure secure and transparent data utilization.

The widespread digital adoption, strong public data assets, and sustained government investment in data capabilities are driving the customer analytics market in the UK. According to the Office for National Statistics, April 2026 data indicates that online retail sales accounted for around 27.9% in March 2026, reflecting high volumes of digital transactions requiring advanced analytics. Moreover, nearly 92% of UK enterprises had internet access, as per the London Borough of Hammersmith & Fulham 2026 data, enabling the continuous generation and integration of customer data across operations. Further, the UK Government’s open data platform hosts datasets supporting enterprise use of external data for customer modeling and forecasting. These factors are driving demand for analytics solutions that enhance customer targeting, improve retention, and align with the UK’s broader digital economy strategy.

Internet Sales as a Percentage of Total Retail Sales, 2026

|

Month (2026) |

Percentage |

|

January |

28.6 |

|

February |

27.4 |

|

March |

27.9 |

Source: Office for National Statistics, April 2026

Key Customer Analytics Market Players:

- Microsoft (U.S.)

- Oracle (U.S.)

- Salesforce (U.S.)

- Adobe (U.S.)

- IBM (U.S.)

- Google (U.S.)

- SAS Institute (U.S.)

- Teradata (U.S.)

- SAP (Germany)

- Qualtrics (U.S.)

- NICE Systems (France)

- Zoho (India)

- Freshworks (India)

- Hitachi (Japan)

- Fujitsu (Japan)

- Pegasystems (U.S.)

- Accenture (Ireland)

- Model N (U.S.)

- RADCOM Ltd. (Israel)

- Actable (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Microsoft has established a dominant presence in the customer analytics market by deeply integrating AI-driven insights into its Dynamics 365 Customer Insights and Azure Machine Learning platforms. The company leverages its vast ecosystem, including LinkedIn, Office 365, and Power BI, to provide unified customer profiles and predictive analytics at scale.

- Oracle competes strongly in the customer analytics market via its Oracle Fusion Cloud Customer Experience and Oracle Analytics Cloud, which combine native AI and machine learning with robust data management. The company’s strategic emphasis lies in its customer data platform and recently enhanced Unity platform, offering real-time ingestion, identity resolution, and journey analytics.

- Salesforce is a dominant player in the customer analytics market, mainly via its Einstein AI and Tableau analytics layers integrated across Sales Service and Marketing Clouds. The company’s strategic focus is on democratizing customer analytics by offering no-code predictive models, automated insights, and real-time dashboards. In 2025, the company has made a revenue rise of 9% YoY.

- Adobe has carved a leadership position in the customer analytics market via its Adobe Experience Platform and Real Time Customer Data Platform, core components of its marketing and analytics suite. The company’s strategic initiatives revolve around combining behavioral analytics from Adobe Analytics with journey orchestration and AI-powered insights from Adobe Sensei.

- IBM distinguishes itself in the customer analytics market via its enterprise-grade WatsonX AI and data platform alongside legacy offerings such as IBM SPSS and Cognos Analytics. The company’s strategic focus is on trustworthy, explainable AI for customer forecasting, churn analysis, and journey mining. According to the 2025 annual report, the company has made a revenue of USD 67.5 billion.

Here is a list of key players operating in the global customer analytics market:

The customer analytics market is highly competitive, dominated by the U.S.-based tech giants along with strong specialists from Europe and Asia. The key players focus on the AI-driven predictive analytics, real-time customer data platforms, and hyper-personalization. Strategic initiatives include heavy R&D investments in generative AI for sentiment analysis, mergers and acquisitions, and expanding cloud-based analytics suites. For example, in August 2024, Accenture acquired GemSeek, a leading customer experience analytics provider helping businesses understand customers via insights, analytics, and AI-powered predictive models. Europe firms highlight privacy-compliant analytics, while Asian players integrate omnichannel data from super apps. Moreover, the partnerships with the CRM and e-commerce platforms are common to enhance data ingestion and actionable insights, aiming to reduce churn and improve lifetime value.

Corporate Landscape of the Customer Analytics Market:

Recent Developments

- In December 2025, Model N, the leader in revenue optimization and compliance for life sciences and high-tech companies, announced Data nSights, an integrated data and analytics solution. Data nSights provides timely access to curated, artificial intelligence (AI) and analytics-ready data, along with no-code data exploration and a growing library of comprehensive insights for life sciences revenue management.

- In October 2025, RADCOM Ltd., a leader in next-generation intelligent assurance, announced the availability of its High-Capacity User Analytics solution. The solution enables telecom operators to process massive volumes of traffic across the entire network at the edge, reducing costs while unlocking real-time, customer-level insights.

- In March 2025, Actable, a leader in Customer Intelligence and data activation, announced the launch of its groundbreaking Intelligence Factory, a proprietary framework and suite of pre-built accelerators that transforms raw customer data into actionable insights and outcomes to drive measurable business impact.

- Report ID: 8545

- Published Date: Apr 30, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.