Curing Agents Market Outlook:

Curing Agents Market size was valued at over USD 7.4 billion in 2025 and is expected to reach USD 14.1 billion by the end of 2035, growing at a CAGR of 7.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of curing agents is evaluated at USD 7.9 billion.

The worldwide curing agents market is continuously witnessing expansion, owing to several factors, including demographic transition positively affecting industrial labor availability, climate modifications impacting raw material supply chain, globalization of technical standards for composite materials, and insurance underwriting for chemical manufacturing facilities. According to official statistics published by Heliyon in November 2024, there has been a significant growth in composites utilization globally, with a yearly increase of an estimated 5%. Moreover, global governments are significantly investing in upgrading public infrastructure, which has eventually led to an increase in the construction composites industry exceeding USD 65 billion by the end of 2025. Therefore, with such upliftments in the overall composites sector, the market is gradually gaining increased exposure.

Furthermore, the digitalization of curing process monitoring, hybrid curing agent formulations, and just-in-time and on-demand blending are a few trends that are responsible for bolstering the curing agents market globally. As stated in an article published by NLM in November 2022, the transportation and automotive industry constitutes the largest end user application of polyurethane adhesives, for which the industrial size grew by USD 9.1 billion as of 2024, along with a 5.6% yearly growth rate. Additionally, the flexibility, performance, and the ability to cure under ambient conditions within a short duration make polyurethane-based adhesives the most suitable curing agent for these industries. Therefore, with an increase in the availability of such adhesives, the market is continuously expanding and developing across both developed and developing nations.

Key Curing Agents Market Insights Summary:

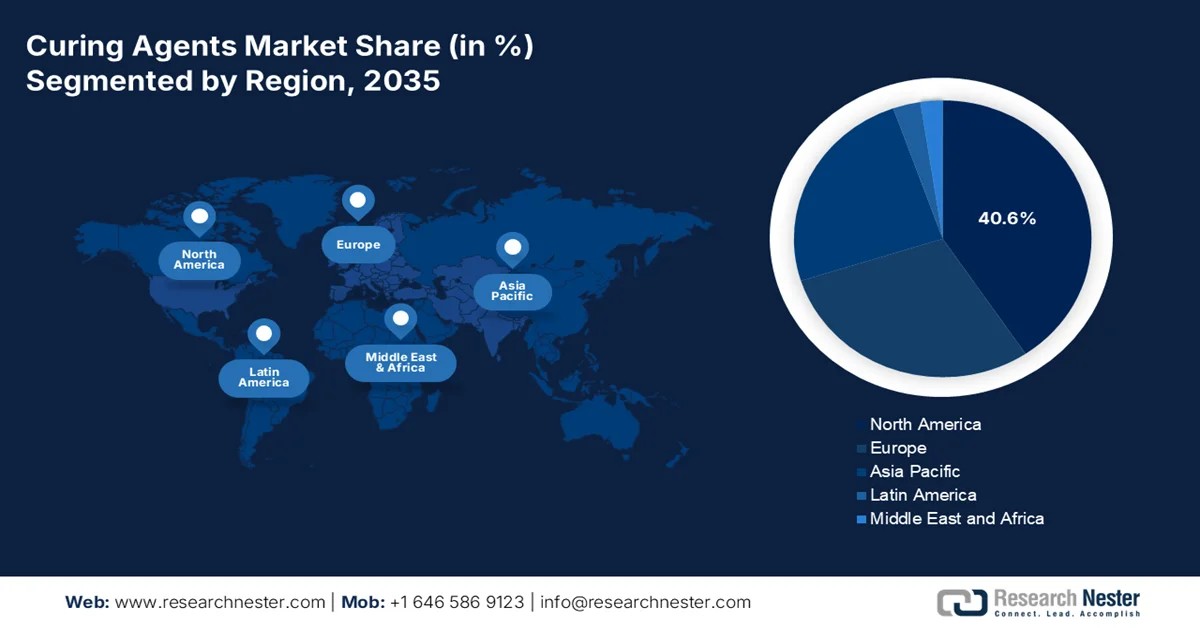

Regional Highlights:

- North America in the curing agents market is forecasted to dominate with a 40.6% share by 2035, attributable to rising demand from automotive and construction sectors alongside increasing adoption of composites in aerospace and wind energy

- Asia Pacific is set to witness the fastest expansion over the 2026–2035 period, fostered by rapid industrialization, urbanization, and growing demand from construction and automotive industries

Segment Insights:

- The liquids sub-segment of the form segment in the curing agents market is projected to capture a dominant 70.4% share by 2035, propelled by its extensive utilization in construction and manufacturing for enhancing material performance and ensuring effective crosslinking in epoxy resins

- The ambient temperature curing segment is expected to hold the second-largest share over the 2026–2035 period, impelled by its energy-efficient chemical cross-linking processes that eliminate the need for external heat in industrial applications

Key Growth Trends:

- Aging industrial infrastructure for rehabilitation

- Expansion of deepwater offshore oil exploration

Major Challenges:

- Stringent environmental regulations on VOC emissions

- Volatility in raw material prices

Key Players: BASF SE, Evonik Industries AG, Hexion Inc., Huntsman Corporation, Olin Corporation, Westlake Chemical Corporation, Mitsubishi Chemical Group Corporation, Resonac Holdings Corporation, DIC Corporation, Shikoku Kasei Holdings Corporation, Osaka Gas Chemicals Co., Ltd., Kukdo Chemical Co., Ltd., Aditya Birla Chemicals, Atul Ltd., Cardolite Corporation, Gabriel Performance Products, Allnex Group, Leuna-Harze GmbH, Nouryon, Reichhold LLC, DKSH Business Unit Performance Materials.

Global Curing Agents Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 7.4 billion

- 2026 Market Size: USD 7.9 billion

- Projected Market Size: USD 14.1 billion by 2035

- Growth Forecasts: 7.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: South Korea, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 8 April, 2026

Curing Agents Market - Growth Drivers and Challenges

Growth Drivers

- Aging industrial infrastructure for rehabilitation: This is a significant driver that focuses on rehabilitating public infrastructure and aging industries, which is positively impacting the curing agents market growth. Based on government estimates published by the PIB Government in December 2025, in terms of smart infrastructure, India comprises more than 4,500 industrial parks, effectively spanning across 7.7 lakh hectares, along with 1.3 lakh hectare availability. In addition, the country has established 306 plug-and-play parks and 20 National Industrial Corridor Development Corporation Limited (NICDC)-based parks and smart cities. These developments demonstrate that the country is focused on enhancing its industrial facilities, which is extremely suitable for driving the curing agents market growth.

- Expansion of deepwater offshore oil exploration: The aspect of deepwater and ultra-deepwater oil exploration demands specialized subsea equipment and pipelines that tend to withstand pressures, which is gradually expanding the curing agents market growth globally. As stated in an article published by the IEA in June 2025, the worldwide oil demand increased by 720 kb/d as of 2025, and is further expected to increase to 740 kb/d by the end of 2026. Simultaneously, there has been a rise in global oil supply by 330 kb/d in May 2025, which eventually surged to 104.9 mb/d by the end of 2025 and is expected to account for 1.1 mb/d by the end of 2026. Besides, a rise has been recorded for refinery throughputs by almost 460 kb/d between 2025 and 2026 to average 83.3 mb/d and 83.7 mb/d, respectively, thus positively impacting the market upliftment.

- Growth in modular and prefabricated construction: The international shift to modular and prefabricated construction methods has created the latest demand for rapid-cure sealants and adhesives. As per an article published by the Adhesives Organization in February 2025, the latest Xi’an plant in Singapore is focused on catering to localized consumers and is home to more than 6 million people. This particular facility positively drives the country’s construction industry, which is forecasted to extend with a 4.1% growth rate by the end of 2028. This growth is projected to be supported by the Land Transport Master Plan 2040, which has been mandated by the government’s infrastructure body. Therefore, this denotes a continuous growth for the curing agents market, especially across developing nations.

Challenges

- Stringent environmental regulations on VOC emissions: A significant roadblock confronting the curing agents market is the enforcement of stringent regulations on volatile organic compound (VOC) emissions globally. Regulatory bodies such as Europe’s REACH program and the U.S.-based EPA have implemented strict limits on VOC content in coatings, adhesives, and sealants. This directly impacts conventional solvent-borne curing agents, particularly certain amine-based hardeners, due to their toxicity and environmental persistence. This regulatory pressure mandates a costly and complex shift towards eco-friendly alternatives, including low-VOC paint hardeners, waterborne systems, and bio-based curing agents.

- Volatility in raw material prices: The curing agents market is highly susceptible to fluctuations in the prices of petrochemical-based raw materials. Key ingredients such as bisphenol-A, epichlorohydrin, cycloaliphatic amines, polyamidoamines, and isocyanates are derived from crude oil and natural gas, making their costs inherently volatile. Recent years have seen significant disruptions due to geopolitical tensions, for instance, the Russia-Ukraine war, supply chain bottlenecks, and fluctuating energy prices. Besides, manufacturers often struggle to pass these increased costs directly to customers, particularly in highly competitive market segments, such as commodity industrial coatings or construction adhesives, where buyers are price-sensitive. This cost-squeeze erodes profit margins and can force companies to absorb losses or compromise on raw material quality to maintain pricing.

Curing Agents Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.5% |

|

Base Year Market Size (2025) |

USD 7.4 billion |

|

Forecast Year Market Size (2035) |

USD 14.1 billion |

|

Regional Scope |

|

Curing Agents Market Segmentation:

Form Segment Analysis

The liquids sub-segment, part of the form segment, is anticipated to grab the largest share of 70.4% in the curing agents market by the end of 2035. The sub-segment’s upliftment is highly fueled by its importance in manufacturing and construction to improve material performance, eventually by retaining moisture for suitable hydration in concrete and ensuring crosslinking in epoxy resins. For instance, in October 2024, Atul Ltd. made a suitable expansion in increasing its capacity for liquid epoxy resin. This expansion caters to the present capacity of 30,000 tpa, 99% of existing capacity utilization, and 50,000 tpa as the proposed capacity addition. Besides, to support this expansion, there has been the provision of required investments, amounting to USD 21.4 million, excluding USD 17.6 million working capital, thereby making it suitable for driving the sub-segment’s growth.

Curing Technology Segment Analysis

Based on the curing technology, the ambient temperature curing segment in the curing agents market is projected to account for the second-largest share during the forecast period. The segment’s growth is highly driven by the dependence on chemical cross-linking reactions that proceed at ambient conditions without external heat application, providing significant operational advantages for field-applied and large-scale industrial applications. Additionally, the segment's strong market position is propelled by several compelling factors, including ambient-cured systems that deliver substantial energy cost reductions, eliminating the need for industrial ovens or heat-curing facilities that typically consume more energy, in comparison to room-temperature systems. This energy efficiency has become increasingly critical amid sustained high energy prices across Europe and other industrial regions, thus boosting the segment growth.

Chemical Composition Segment Analysis

By the end of the stipulated timeline, the amine-based sub-segment, which is part of the chemical composition segment, is expected to hold the third-largest share in the curing agents market. The sub-segment’s development is primarily attributed to its crucial role in serving as a building block for pharmaceuticals, such as antidepressants and painkillers, along with dyes, textiles, and agricultural chemicals. According to official statistics published by the International Journal of Greenhouse Gas Control in January 2026, amine-based technologies are usually based on aqueous solutions of 30% of monoethanolamine, along with a 13% of phenylimidazole and 27% of 2-amino-2-methyl-1-propanol. Besides, these technological processes are effectively simulated by utilizing ProTreat by employing a rate-driven strategy to simulate and design absorber and stripper columns and target a 90% of capture, thus positively impacting the sub-segment’s exposure.

Our in-depth analysis of the curing agents market includes the following segments:

|

Segment |

Subsegments |

|

Form |

|

|

Curing Technology |

|

|

Chemical Composition |

|

|

Type |

|

|

Application |

|

|

End use Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Curing Agents Market - Regional Analysis

North America Market Insights

North America in the curing agents market is anticipated to account for the highest share of 40.6% by the end of 2035. The market’s upliftment in the region is primarily attributed to a rise in the demand from the automotive and construction industries, an increase in the adoption of composite materials in wind energy and aerospace applications, technological innovations in curing processes, and the presence of strict environmental regulations. As depicted in an article published by the America Composites Manufacturers Association, in May 2025, Hexcel entered into a strategic partnership with JetZero through the FAA’s Fueling Aviation's Sustainable Transition (FAST) program. JetZero developed the Z4, which is the first-ever wing design commercial airplane that produces great lift and diminished drag, leading to almost 50% better fuel efficiency, in comparison to comparable-sized tube and wing aircraft. Moreover, the continuous increase in light vehicle trends is also positively impacting the curing agents market in the region.

Month Sales Growth Analysis of Light Vehicles in the U.S. (2024-2025)

|

Months |

Sales (in Million) |

|

May 2024 |

1.4 |

|

June 2024 |

1.3 |

|

July 2024 |

1.2 |

|

August 2024 |

1.4 |

|

September 2024 |

1.1 |

|

October 2024 |

1.3 |

|

November 2024 |

1.3 |

|

December 2024 |

1.4 |

|

January 2025 |

1.1 |

|

February 2025 |

1.2 |

|

March 2025 |

1.5 |

|

April 2025 |

1.4 |

|

May 2025 |

1.4 |

Source: America Composites Manufactures Association

The curing agents market in the U.S. is growing significantly, owing to the expansion of the automotive industry, a rise in the demand for composite materials, the growth in the coatings and paints industry, regulatory compliance driving advancements, an upsurge in construction activities, and technological innovations. Based on government estimates published by the Congress Government in March 2026, the automotive manufacturing industry in the country significantly accounts for 4.8% of gross domestic product (GDP) and readily employs 10.1 million people through indirect and direct employment opportunities. Besides, there has been an increase in international automotive manufacturers producing and selling vehicles in the country, with the industry being diversified, with 14 organizations catering to more than 90% of domestic sales as of 2024, thus enhancing the curing agents market demand in the overall country.

Automotive Industry Share Analysis by Vehicle Sales in the U.S. (2022-2024)

|

Automotive Companies |

2022 |

2023 |

2024 |

|

Volkswagen |

2.1% |

2.1% |

2.3% |

|

Toyota |

14.8% |

14% |

14.3% |

|

Tesla |

3.2% |

4.1% |

3.6% |

|

Subaru |

3.9% |

4% |

4.1% |

|

Nissan |

5.1% |

5.6% |

5.7% |

|

Mercedes-Benz |

2.5% |

2.2% |

2.2% |

|

Mazda |

2.1% |

2.3% |

2.6% |

|

Kia |

4.9% |

4.9% |

4.9% |

Source: Congress Government

The epoxy sector dominance, growth in the wind energy industry, infrastructure development investments, an increase in industrial coatings demand, regulatory and sustainability alignment, and emerging applications in aerospace and electronics are factors that are boosting the curing agents market in Canada. As per an article published by the Government of Canada in November 2025, wind power is expected to dominate the country’s power growth over the upcoming 5 years, readily accounting for almost 70% of planned renewable capacity additions. Additionally, it has been highlighted that wind projects are expected to lead domestic planned power additions, with 6,206 MW of new wind by the end of 2030. Besides, combined with solar power, these projects have the ability to add over 8,745 MW of renewable capacity, thus enhancing the market expansion in the overall country.

APAC Market Insights

The Asia Pacific in the curing agents market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by increased industrialization, urbanization, an upsurge in demand from both the construction and automotive industries, and a shift towards sustainable agents. According to official statistics published by the International Labor Organization in September 2025, industrial supply chains significantly account for 41% of worldwide merchandise trade valuation and readily support almost 75 million workers, particularly in Southeast Asia. This employment opportunity is built on large-scale organizations, along with small and medium-sized and micro enterprises, deliberately making up 97% of overall enterprises and employing about 70% of the overall region’s labor force, thus proliferating the market development.

The curing agents market in China is gaining increased traction, owing to the existence of the largest manufacturing facility, a huge infrastructure development pipeline, the sustained government support, rapid electric vehicle adoption, an escalation in the adoption of sustainable chemical processes, and expansion in the wind energy capacity. As stated in an article published by the Belt and Road Portal in January 2026, the country has significantly attracted almost USD 98.2 billion in actual foreign direct investment, with the domestic manufacturing sector receiving nearly USD 24.4 billion, which is approximately 1/4th of the overall investment. Besides, the industry is readily supported by generous labor resources, favorable policies, and robust infrastructure, which are suitable for increasing the average yearly rate of 12%, thus denoting an optimistic outlook for the market development.

The aspects of strong government strategies, domestic chemical manufacturing, the provision of generous investments, an increase in the demand for specialty chemicals, and renewable energy investments are certain trends that are ensuring the development of the curing agents market in India. Based on government estimates published by the PIB Government in July 2025, the chemical industry in the country accounts for 3.5% of global chemical value chains, along with the chemical trade deficit of USD 31 billion as of 2023 has underscored its reliance on imported feedback. However, with suitable reforms focused on incorporating a wide-ranging fiscal and non-fiscal interventions is projected to enable the country to constitute a USD 1 trillion chemical industry and successfully achieve 12% of gross value chain share by the end of 2040, thereby creating a huge growth opportunity for the market.

Europe Market Insights

Europe in the curing agents market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by the existence of strict environmental regulations, innovative industrial base, the transition to circular economy, and commitment towards the Europe Green Deal. According to official statistics published by the ECIPE Organization in March 2026, the industrial production in the region grew by an average of only 0.6% every year as of 2024. Regarding this growth, the yearly industrial growth in Ireland accounts for 5.6%, followed by 4.9% growth in Poland. Besides, the Commission stated that the Industrial Accelerator Act has aimed to ensure that the manufacturing industry represents 20% of the regional GDP by the end of 2035, thereby denoting an optimistic outlook for the market’s growth.

The curing agents market in Germany is gaining increased exposure, owing to the presence of the largest domestic chemical producer, the continuous growth in machinery industries, rapid transformation in electric vehicles, an increase in manufacturing lightweight carbon-fiber-reinforced polymer components, and the robust governmental policy support for industrial decarbonization. As stated in an article published by the C&EN Organization in May 2024, there has been a rise in the country’s chemical production by 4.4%, along with an additional 3.5% growth in production, with a 1.5% rise in sales as of 2024. Besides, according to an article published by Green Carbon in March 2024, an estimated 60% of polymers, such as mulch films, packaging materials, and shopping bags, are produced in the country for single-use. Therefore, with the production of polymers, the chemical industry is rising, which in turn is positively impacting the market growth.

The combination of industrial catch-up, huge infrastructure investment, a tactical pivot towards import substitution, an increase in its national industrial policy, a surge in the domestic production of critical materials, and the demand for local manufactured or sourced products are certain factors that are responsible for bolstering the curing agents market in Russia. As per an article published by the Trap Organization in July 2025, military shipyards and airlines in the country utilize coatings, based on which Russian Coatings JSC’s yearly revenue effectively surpassed roughly USD 139 million. This particular joint-stock organization constituted a joint venture with DuPont and proactively participates in developing special varnishes, paints, and primers for the defense industry through generous investments, thus making it suitable for fueling the market demand.

Key Curing Agents Market Players:

- BASF SE (Germany)

- Evonik Industries AG (Germany)

- Hexion Inc. (U.S.)

- Huntsman Corporation (U.S.)

- Olin Corporation (U.S.)

- Westlake Chemical Corporation (U.S.)

- Mitsubishi Chemical Group Corporation (Japan)

- Resonac Holdings Corporation (Japan)

- DIC Corporation (Japan)

- Shikoku Kasei Holdings Corporation (Japan)

- Osaka Gas Chemicals Co., Ltd. (Japan)

- Kukdo Chemical Co., Ltd. (South Korea)

- Aditya Birla Chemicals (India)

- Atul Ltd. (India)

- Cardolite Corporation (U.S.)

- Gabriel Performance Products (U.S.)

- Allnex Group (Germany)

- Leuna-Harze GmbH (Germany)

- Nouryon (Netherlands)

- Reichhold LLC (U.S.)

- DKSH Business Unit Performance Materials (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- BASF SE offers a broad portfolio of epoxy curing agents, including amine-based and polyamide hardeners, serving applications from industrial coatings to composites. The company focuses on developing sustainable, low-VOC curing agent solutions to align with tightening environmental regulations across Europe and North America.

- Evonik Industries AG is a leading supplier of specialty curing agents, particularly its VESTAMIN line of isophorone diamine (IPDA) and other aliphatic amines for high-performance epoxy systems. The company has expanded its curing agents production capacity at its Nanjing, China facility to capture growing demand from the wind energy and automotive lightweighting sectors.

- Hexion Inc. is a major producer of epoxy resins and accompanying curing agents, with a strong presence in the protective coatings, adhesives, and composites end-markets. The company has invested in next-generation bio-based curing agents and low-temperature cure technologies to support sustainability goals and field-applied maintenance applications.

- Huntsman Corporation delivers a comprehensive range of advanced amine-based curing agents under its ARADUR series, widely used in aerospace-grade composites, structural adhesives, and high-durability coatings. The company continues to expand its footprint in high-growth Asia-Pacific markets through localized technical service and production partnerships.

- Olin Corporation offers epoxy curing agents as part of its integrated epoxy systems portfolio, primarily serving the industrial coatings, construction, and wind blade manufacturing sectors. Following its acquisition of Dow's epoxy business, Olin has leveraged backward integration into epichlorohydrin and bisphenol-A to maintain cost competitiveness in the commodity curing agents segment.

Here is a list of key players operating in the global curing agents market:

The global curing agents market is moderately consolidated, with leading multinational chemical companies holding significant market share through extensive distribution networks and broad product portfolios. Besides, the Asia Pacific dominates global demand, accounting for the majority of consumption, driven by rapid industrialization and infrastructure expansion. Moreover, notable players are pursuing strategic initiatives, including capacity expansions, mergers and acquisitions, and new product developments focused on bio-based and low-VOC formulations. For instance, in February 2026, Aditya Birla Chemicals expanded its worldwide manufacturing footprint by successfully acquiring Cargill’s specialty chemical manufacturing facility in the U.S. The purpose of this acquisition was to bolster the company’s epoxy capacity for its high strength, corrosion resistance, durability, and light-weight, thereby making it suitable for uplifting the curing agents industry globally.

Corporate Landscape of the Curing Agents Market:

Recent Developments

- In March 2025, Westlake Corporation introduced different new products for its brand Westlake Epoxy, with its latest innovative epoxy products that are designed to enhance performance, safety, and robustness.

- In April 2024, DKSH Business Unit Performance Materials made an expansion of its outstanding distribution agreement with ddchem, with the ultimate objective to bolster business opportunities for the partnership in the key economy.

- In February 2024, DIC Corporation succeeded in creating a basic technology for a groundbreaking epoxy resin curing agent that significantly resists heat up to almost 200 degrees Celsius and can also be further recycled.

- Report ID: 8506

- Published Date: Apr 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035 (Updated Version Available)

Copyright @ 2026 Research Nester. All Rights Reserved.