Connector Market Outlook:

Connector Market size was valued at USD 42.6 billion in 2025 and is expected to reach USD 89.4 billion by the end of 2035, growing at around 7.7% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of connector is assessed at USD 45.9 billion.

The connector market is being supported by sustained growth in electronics manufacturing, transportation electrification, industrial automation, and communications infrastructure. According to the Semiconductor Industry Association February 2025 data, global semiconductor sales reached USD 627.6 billion, reflecting expanding production of electronic systems that require a broad range of interconnect solutions across computing, networking, automotive, and industrial equipment. In parallel, the International Energy Agency 2025 data reported that global electric car sales exceeded 17 million units in 2024, representing more than 20% of total car sales worldwide. Rising deployment of electric vehicles increases demand for high-voltage, charging, battery-management, and power-distribution connectors across vehicle platforms and charging infrastructure.

Public charging networks are also expanding rapidly; the IEA 2025 reported that the global stock of publicly accessible charging points surpassed 5 million units in 2024, creating additional procurement opportunities for ruggedized connector assemblies used in charging stations, power electronics, and grid interfaces. These trends are encouraging manufacturers and component suppliers to increase production capacity, strengthen supply-chain resilience, and develop products capable of supporting higher power densities and more demanding operating environments. As organizations invest in electrification, automation, and digital infrastructure, connector suppliers are positioned to benefit from long-term demand linked to equipment upgrades, system integration projects, and replacement cycles.

Key Connector Market Insights Summary:

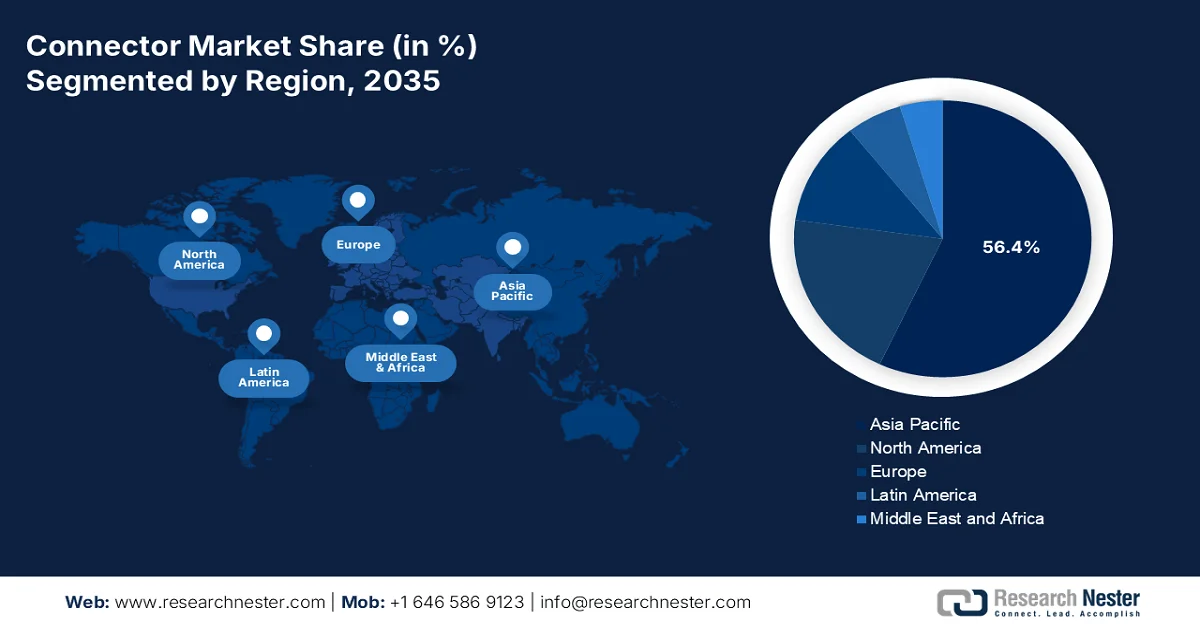

Regional Highlights:

- Asia Pacific is anticipated to command 56.4% of the connector market share by 2035, reinforced by high-volume electronics manufacturing, concentrated assembly operations, and robust demand across consumer electronics, automotive, and telecommunications industries.

- North America is expected to witness rapid growth during 2026–2035 in the market, fueled by sustained investments in EV infrastructure, defense electronics modernization, and expanding data center deployments.

Segment Insights:

- PCB connectors are projected to secure 26.2% of the connector market share by 2035, underpinned by their role in enabling cost-effective IoT platforms integrated with Digital Twin models for advanced structural monitoring and resilient infrastructure management.

- Automotive & electric vehicles (EVs) are set to account for the largest revenue share in the market by 2035, stimulated by rising connector requirements in battery systems, ADAS technologies, and accelerating EV adoption supported by declining battery pack costs.

Key Growth Trends:

- Government investment in grid modernization and power infrastructure

- Broadband and telecommunications infrastructure funding

Major Challenges:

- Stringent certification & compliance standards

- Intellectual property & patent thickets

Key Players: TE Connectivity (U.S.),Amphenol (U.S.),Molex (U.S.),Aptiv (U.S.),Yazaki (Japan),Hirose (Japan),Sumitomo (Japan),JAE (Japan),Rosenberger (Germany),Phoenix Contact (Germany),Harting (Germany),KYOCERA AVX (Japan),Belden (U.S.),Samtec (U.S.),ITT Cannon (U.S.),Weidmüller (Germany),Radiall (France),KET (South Korea),Minda Corporation (India),J.S.T. (Japan).

Global Connector Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 42.6 billion

- 2026 Market Size: USD 45.9 billion

- Projected Market Size: USD 89.4 billion by 2035

- Growth Forecasts: 7.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (56.4% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, Germany, South Korea

- Emerging Countries: India, Vietnam, Mexico, Indonesia, Thailand

Last updated on : 3 June, 2026

Connector Market - Growth Drivers and Challenges

Growth Drivers

- Government investment in grid modernization and power infrastructure: Connector demand is rising as governments expand transmission, distribution, and smart-grid infrastructure. Electrical connectors are critical components in substations, switchgear, transformers, smart meters, and grid communication systems. The U.S. Department of Energy 2026 data announced up to USD 10.5 billion through the Grid Resilience and Innovation Partnerships Program to modernize the electric grid and improve reliability. Additionally, the Bipartisan Infrastructure Law allocated billions toward transmission upgrades and clean-energy integration. In Europe, the European Commission's energy transition programs continue to support cross-border electricity networks and renewable-energy connections. Connector suppliers with products qualified for utility and industrial environments are positioned to benefit from long-term infrastructure spending cycles.

- Broadband and telecommunications infrastructure funding: Large-scale broadband deployment programs are increasing demand for fiber-optic, RF, and networking connectors. The Broadband USA 2025 data administers the Broadband Equity, Access, and Deployment (BEAD) Program, which provides USD 42.45 billion to expand broadband access nationwide. Telecommunications operators deploying fiber-to-the-home (FTTH), 5G networks, and edge infrastructure require extensive connector systems for network reliability and scalability. Similar digital connectivity initiatives are underway across Europe and Asia to support economic development and digital inclusion goals. Connector manufacturers supplying telecom-grade products are benefiting from long-term infrastructure rollouts, particularly in rural and underserved regions where network expansion remains a strategic priority.

Challenges

- Stringent certification & compliance standards: Connectors must meet rigorous industry standards requiring months for testing and qualification before market entry. Leading players have spent months certifying their connectors for automotive airbag systems, requiring hours of vibration and thermal cycling tests.

- Intellectual property & patent thickets: Established players hold thousands of patents covering basic connector geometries, contact geometries, and latching mechanisms, creating legal barriers for new entrants. Players successfully defended its patent on coaxial connector shielding against a Chinese startup, blocking their U.S. market entry.

Connector Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.7% |

|

Base Year Market Size (2025) |

USD 42.6 billion |

|

Forecast Year Market Size (2035) |

USD 89.4 billion |

|

Regional Scope |

|

Connector Market Segmentation:

Product Type Segment Analysis

Within the product type segment, the PCB connectors are leading and is poised to hold the share value of 26.2% by the end of 2035. The segment is critical for enabling cost-effective IoT platforms integrated with Digital Twin models for advanced structural monitoring. As per the NLM March 2026 study, a customized PCB designed with robust communication architecture utilizing MQTT protocols synchronizes real-time data between physical structures and their digital twin counterparts. Validation tests confirm high accuracy in data capture, showing less than 1% deviation from conventional systems across multiple structural damage scenarios. This PCB facilitates reliable data transmission and efficient integration with MATLAB for processing, directly supporting structural health monitoring (SHM). Such cost-effective PCB connector solutions are driving more resilient, proactive infrastructure management strategies.

Application Segment Analysis

Under the application segment, automotive & electric vehicles (EVs) is the leader, accounting for the largest share in the market revenue by 2035. This sub-segment includes high-voltage power connectors for battery packs, inverters, and charging ports, plus high-speed data connectors for ADAS, cameras, LiDAR, and autonomous driving systems. An EV contains three to five times more connectors than a conventional internal combustion engine vehicle. According to the IEA 2026 data the EV battery pack costs are projected to decline by over 8%, accelerating mass adoption and increasing connector content per vehicle. This rapid electrification forces connector makers to develop ruggedized, corrosion-resistant, and high-thermal-performance interconnects for harsh automotive environments, ensuring sustained dominance of this application segment.

End user Segment Analysis

Original equipment manufacturers represent the largest end-user segment in the market, as they integrate connectors directly into new products during the initial manufacturing process. OEMs span diverse industries including automotive, consumer electronics, medical devices, telecommunications infrastructure, and industrial automation. Unlike the aftermarket, which focuses on replacements and repairs, OEMs drive demand through volume production and long-term design-in cycles. Connector manufacturers prioritize early engagement with OEM engineering teams to qualify components for specific platforms, ensuring recurring revenue streams over multiple product generations. The close collaboration between connector suppliers and OEMs enables customized solutions tailored to exact mechanical, electrical, and environmental specifications, making this end-user segment the primary focus for connector companies worldwide.

Our in-depth analysis of the connector includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Application |

|

|

End user |

|

|

Transmission Speed |

|

|

Connectivity Type |

|

|

Material |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Connector Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating the connector market and is poised to hold the regional revenue share of 56.4% by the end of 2035. The region is characterized by high-volume manufacturing, concentrated electronics assembly, and strong domestic demand across China, Japan, South Korea, India, and Southeast Asian nations. Original equipment manufacturers in consumer electronics, automotive, and telecommunications sectors drive substantial consumption of PCB connectors, FPC connectors, and battery connectors. Japan and South Korea lead in precision micro-connectors for mobile devices and automotive systems, while India and Vietnam emerge as alternative production hubs for global brands. The region benefits from vertically integrated supply chains, reducing lead times and logistics costs for local assembly operations. Price sensitivity remains a key factor in commodity connector segments, with intense competition among domestic and multinational suppliers serving export-oriented factories.

Rapid growth in electronics manufacturing, industrial modernization, and digital infrastructure deployment is driving the market in China. According to the People’s Republic of China February 2025 data, the country’s value-added industrial output of high-tech manufacturing increased by 8.9% year-on-year in 2024, reflecting expanding production of electronic equipment, communication systems, and industrial devices that require a wide range of connectors. Additionally, the ACM Digital Library 2024 data reported that China had deployed more than 4.48 million 5G base stations by early 2025, reinforcing demand for RF/coaxial, fiber-optic, and high-speed data connectors used in telecommunications networks. These developments, combined with continued investments in automation, electric vehicles, and data infrastructure, are strengthening long-term demand for advanced interconnect solutions across multiple industries.

The Japan connector market is estimated to grow from USD 8.5 billion in 2025 to USD 14.5 billion by the end of 2035 at a CAGR of 4.8%. The market is projected to reach USD 8.7 billion in 2026. The market is supported by the country's strong automotive and electronics manufacturing sectors. According to the JAMA 2023 data, Japan produced approximately 7.84 million automobiles in 2022, creating sustained demand for connectors used in vehicle electronics, power systems, sensors, and infotainment applications. In addition, data from the Japan Electronics and Information Technology Industries Association shows that the production value of electronic components and devices is reflecting continued activity in electronics and semiconductor-related industries. These sectors remain key contributors to connector demand across Japan.

North America Market Insights

North America is projected to emerge rapidly during the assessed period, 2026 to 2035 in the market. the region is driven by sustained investment in electric vehicle infrastructure, defense electronics modernization, and data center expansion across the United States and Canada. Manufacturers prioritize high-reliability solutions for automotive, aerospace, medical, and telecommunications applications, with a strong focus on ruggedized designs capable of operating in extreme environments. Cross-border integration under the USMCA trade agreement facilitates coordinated manufacturing between U.S. and Canadian facilities. Regulatory requirements, including UL certifications and military specifications, shape product development cycles. The market benefits from close collaboration between connector suppliers and original equipment manufacturers serving the automotive, defense, and industrial automation sectors.

The continued investment in advanced manufacturing, electronics production, and communications infrastructure is shaping the market in the U.S. The electronics products manufacturers are reflecting strong demand for electronic assemblies and interconnect components used across industrial, automotive, healthcare, and networking applications. In addition, the USA Facts September 2022 reported that fixed broadband services were available to more than 97% of the U.S. population in 2024, supporting ongoing deployment of networking equipment, fiber infrastructure, and associated connector systems. Growth opportunities are concentrated in data centers, aerospace, defense electronics, and industrial automation, where reliability, high-speed data transmission, and power-management capabilities remain key procurement priorities.

The investments in telecommunications infrastructure, advanced manufacturing, and clean-energy projects that require reliable power and data interconnect solutions is shaping the market in Canada. According to Statistics Canada, capital expenditures in the telecommunications industry is reflecting continued deployment of broadband and network infrastructure that utilizes fiber-optic, RF, and data connectors. In addition, Government of Canada August 2025 data reported that non-emitting electricity sources accounted for about 84% of Canada’s electricity generation in 2024, supporting ongoing investments in grid modernization, hydroelectric facilities, and renewable-energy systems where power connectors are essential. Demand is further strengthened by growth in industrial automation, transportation electrification, and digital infrastructure projects across major provinces.

Europe Market Insights

The Europe connector market is shaped by stringent environmental regulations, automotive electrification, and industrial automation across Germany, France, Italy, and the United Kingdom. Manufacturers focus on compliant designs meeting RoHS, REACH, and fire safety standards for rail and building applications. The region has strong demand for high-voltage connectors for electric vehicles and charging infrastructure, as well as ruggedized circular connectors for heavy machinery and renewable energy systems. Telecommunications infrastructure upgrades and smart grid deployments further drive consumption of fiber optic and power distribution connectors. Cross-border supply chains within the European Union facilitate component movement, though local production remains concentrated in Central and Eastern Europe. Suppliers prioritize long-term qualification cycles with automotive OEMs and industrial equipment manufacturers serving regional markets.

Strong industrial production, transportation electrification, and digital infrastructure investments is driving the market in Germany. According to the Destatis 2026 data, 380,609 battery-electric passenger cars were newly registered in Germany in 2024, highlighting continued demand for high-voltage, charging, and battery-management connectors used across electric vehicle platforms. In addition, the Advercharge 2025 reported that Germany had more than 161,000 publicly accessible EV charging points in 2025, reflecting ongoing expansion of charging infrastructure that requires power and communication interconnect systems. Demand is also supported by Germany’s advanced manufacturing base, automation projects, and industrial machinery sector, where connectors are essential for power distribution, control systems, sensors, and industrial networking applications.

The investments in digital connectivity, transportation electrification, and advanced electronics manufacturing is driving the market in UK. The UK information and communication sector is supporting demand for networking equipment, data centers, and telecommunications infrastructure that rely heavily on high-performance connectors. Additionally, the Aspect Resource April 2026 data reported that renewable sources generated approximately 50.8% of the UK’s electricity in 2024, encouraging continued investment in grid infrastructure, energy storage systems, and renewable-energy installations that require robust power and signal connectors. These trends are strengthening procurement activity across industrial, telecom, transportation, and energy applications.

Key Connector Market Players:

- TE Connectivity (U.S.)

- Amphenol (U.S.)

- Molex (U.S.)

- Aptiv (U.S.)

- Yazaki (Japan)

- Hirose (Japan)

- Sumitomo (Japan)

- JAE (Japan)

- Rosenberger (Germany)

- Phoenix Contact (Germany)

- Harting (Germany)

- KYOCERA AVX (Japan)

- Belden (U.S.)

- Samtec (U.S.)

- ITT Cannon (U.S.)

- Weidmüller (Germany)

- Radiall (France)

- KET (South Korea)

- Minda Corporation (India)

- J.S.T. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- TE Connectivity is a dominant player in the connector market, leveraging its expertise in high-speed data and power connectors to enable real-time monitoring and industrial automation. The company has integrated smart sensor and connector data into ruggedized solutions for electric vehicles and medical devices. In 2024, the company has made a net sale of USD 6,956 million.

- Amphenol has advanced the market by aggressively acquiring niche technology firms and integrating connector data analytics into mobile and wireless monitoring systems. Its broad portfolio of RF, fiber optic, and high-speed board-level connectors enables real-time, ambulatory cardiac telemetry outside hospital environments. In 2025, the company has made a net sale of USD 23,095 million.

- Molex is a key innovator in the market, particularly in developing high-density, micro-miniature connectors that facilitate wireless mobile cardiac telemetry and real-time ambulatory monitoring. The company leverages connector data streams to enable continuous patient surveillance outside clinical settings, optimizing arrhythmia detection through robust, low-latency connections.

- Aptiv has strategically positioned itself in the connector market by focusing on high-voltage and data connectivity solutions for electric and autonomous vehicles, while also extending into medical telemetry. The company utilizes connector data from its advanced smart junction boxes and vehicle architecture platforms to enable real-time, ambulatory cardiac monitoring outside traditional clinical environments.

- Yazaki, traditionally strong in automotive wiring harnesses is leading in the connector market, is expanding its presence in the Connector Market by adopting high-reliability miniaturized connectors for remote health monitoring and telematics. The company applies its expertise in sealed, vibration-resistant connector systems to enable mobile cardiac telemetry and ambulatory wireless monitoring outside clinical settings.

Here is a list of key players operating in the global market:

The global connector market is highly fragmented yet dominated by a mix of diversified industrial giants and specialized players from the Americas, Europe, and Asia. Intense competition drives continuous innovation in miniaturization, high-speed data transmission, and ruggedization for automotive, telecom, and industrial applications. Key strategic initiatives include vertical integration to control raw material costs, geographic expansion into emerging markets, and targeted acquisitions to fill technology gaps. For example, in April 2026, Molex completes the acquisition of Smiths Interconnect. Leading firms are also heavily investing in R&D for next-generation applications like 5G, autonomous driving, and Industry 4.0, while forming long-term supply agreements to secure demand.

Corporate Landscape of the Market:

Recent Developments

- In March 2026, Hirose Electric has announced plans to establish a new manufacturing site in Chennai, Tamil Nadu, India, to strengthen the company’s automotive business and supply chain capacity.

- In August 2025, TE Connectivity launched an Ultra Low-Profile PCIe Gen 7 connectors and cable assemblies. With an ultra-low-profile mating height, these products deliver data rates of 128 gigatransfers per second to support next-generation data center and AI applications.

- In August 2025, ATTEND announced the release of its Floating Board-to-Board Connector series, featuring an integrated compliant mechanism that accommodates X- and Y-axis PCB misalignment up to ±0.5 mm.

- Report ID: 8602

- Published Date: Jun 03, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.