Cloud Gaming Market - Regional Analysis

North America Market Insights

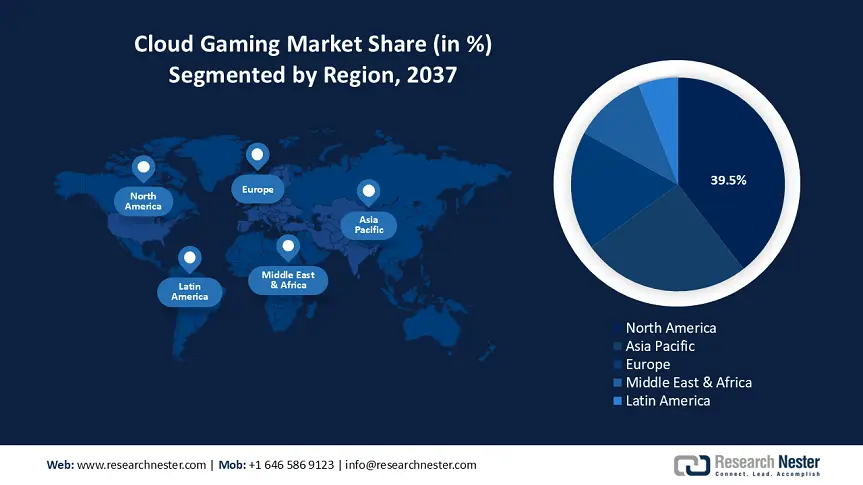

North America is projected to secure a significant cloud gaming market share of 39.5% from 2025 to 2037, driven by extensive broadband coverage and the swift rollout of 5G networks in both urban and suburban areas. Prominent technology leaders based in the region, including Microsoft, NVIDIA, and Amazon, provide early access to advanced cloud gaming platforms. The rise of cross-platform gaming and the increasing popularity of subscription-based services have boosted consumer adoption. Furthermore, rising investments in AI-powered optimization technologies are enhancing gameplay quality and lowering latency. Government programs focused on digital equity and broadband infrastructure expansion continue to support the market’s scalable growth.

The U.S. cloud gaming market is set to retain a dominant revenue share throughout the forecast period. This growth is driven by widespread smartphone and smart TV adoption, which facilitates access to device-agnostic gaming platforms. Leading cloud providers are enhancing edge computing to reduce latency in real-time gameplay. Consumer demand is moving toward flexible subscription models rather than traditional consoles, benefiting services such as Xbox Cloud Gaming and Amazon Luna. Additionally, investments by the FCC and NTIA in 5G and broadband infrastructure are strengthening cloud connectivity, creating a powerful synergy between private innovation and government support that accelerates market growth.

Asia Pacific Market Insights

The APAC cloud gaming market is anticipated to experience the fastest growth at a CAGR of 47% during the forecast timeline due to high mobile internet penetration and a large base of tech-savvy youth. Countries like South Korea, Japan, and India are witnessing the rising adoption of 5G networks, supporting seamless, low-latency gaming experiences. The rising smartphone use and widely available, affordable mobile data plans are allowing widespread access to cloud gaming platforms. Government support for digital economies and smart infrastructure is accelerating technological deployment. Additionally, the popularity of competitive eSports and mobile-first gaming culture is fueling sustained demand.

China is poised to account for a dominant revenue share in the APAC cloud gaming market throughout the forecast timeline due to its massive gaming population and aggressive investment in domestic cloud infrastructure. The Ministry of Industry and Information Technology (MIIT) and tech giants like Tencent and Alibaba are prioritizing AI-integrated cloud services. Advanced 5G expansion across major cities has improved streaming stability for real-time gaming. Regulatory encouragement for digital content innovation is supporting new business models like game-as-a-service. Moreover, increasing adoption of smart TVs and cloud-native platforms is transforming how games are accessed in households.