Clinical Practice Management Software Market Outlook:

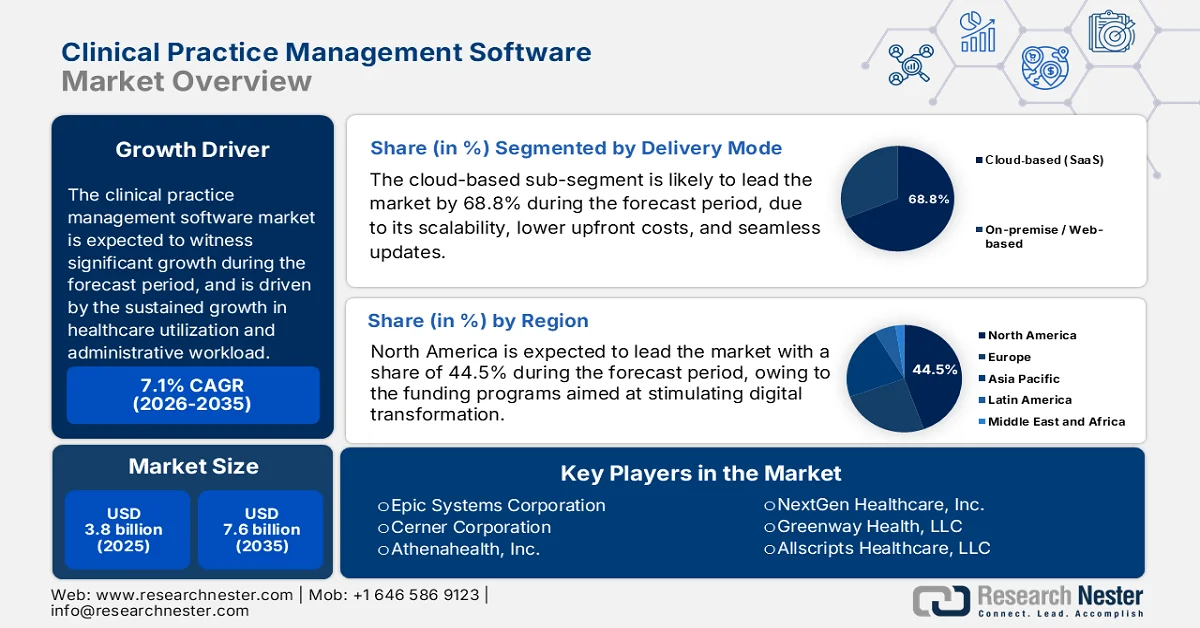

Clinical Practice Management Software Market size was valued at USD 3.8 billion in 2025 and is poised to reach USD 7.6 billion by the end of 2035, registering a CAGR of 7.1% during the forecast period, 2026 to 2035. In 2026, the industry size of clinical practice management software is estimated at USD 4.1 billion.

The clinical practice management software market is being shaped by sustained growth in healthcare utilization, administrative workload, and federal investments in health IT infrastructure. According to the American Medical Association's April 2025 data, national health expenditure reached USD 4.9 trillion in 2023, accounting for 17.6% of GDP. This puts continued pressure on providers to optimize billing, scheduling, and claims management workflows using digital systems. Similarly, the ONC March 2022 data indicates that 4 in 5 office-based physicians and nearly 96% of non-federal acute care hospitals have adopted certified electronic health record systems, creating a strong installed base for integrated practice management platforms. Moreover, the government-led interoperability mandates are also driving the healthcare providers to invest in systems that streamline revenue cycle management and data exchange across care settings.

Percentage of Acute Care Hospitals Adopted Certified EHR, 2022

|

Year |

Hospitals |

|

2008 |

9% |

|

2009 |

12% |

|

2010 |

16% |

|

2011 |

28% |

|

2012 |

44% |

|

2013 |

59% |

|

2014 |

97% |

|

2015 |

96% |

|

2016 |

96% |

|

2017 |

96% |

|

2018 |

96% |

|

2019 |

96% |

|

2021 |

96% |

Source: ONC March 2022

Besides, the international markets are experiencing similar structural drivers supported by public healthcare spending and digitization programs. According to the WHO January 2024 data, the global health expenditure exceeded USD 9.8 trillion, representing 10.3% of GDP, with governments prioritizing efficiency and transparency in the healthcare delivery systems. In India, the National Health Authority continues to expand the Ayushman Bharat Digital Mission, which has generated over a million digital health IDs, stimulating the integration of clinical and administrative platforms across public and private providers. These public-sector initiatives, combined with rising outpatient care demand and regulatory reporting requirements, are increasing reliance on centralized practice management solutions to ensure operational continuity, compliance, and financial performance across healthcare organizations.

Key Clinical Practice Management Software Market Insights Summary:

Regional Highlights:

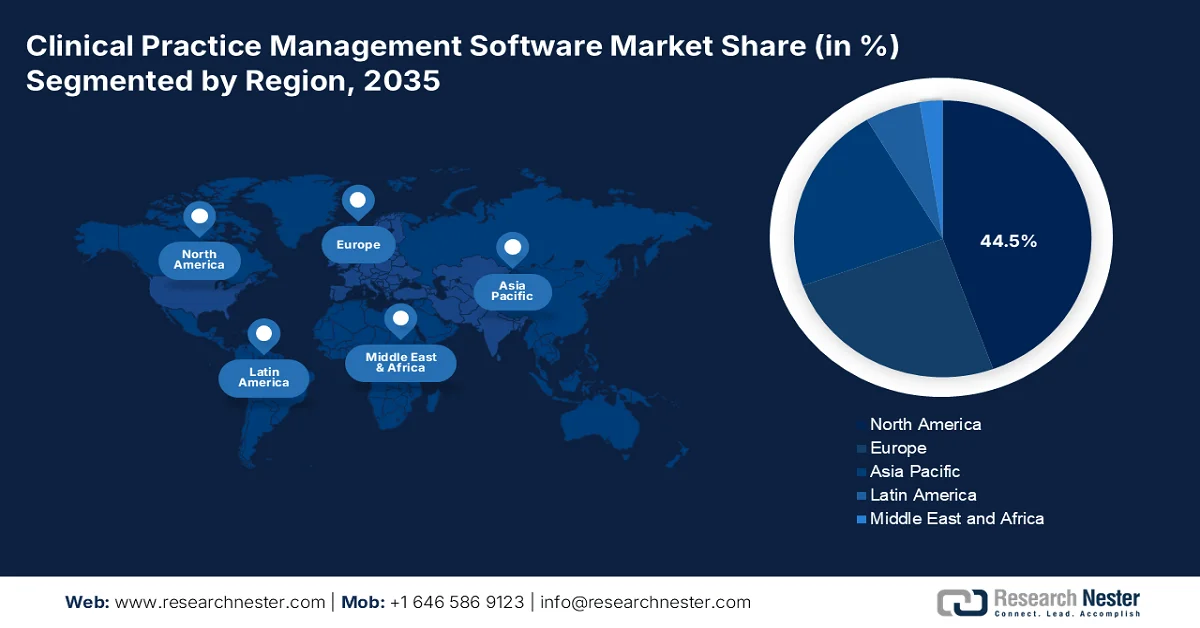

- North America clinical practice management software market is anticipated to command a 44.5% revenue share by 2035, supported by substantial public funding and rising healthcare expenditure facilitating digital healthcare transformation

- Asia Pacific is projected to witness the fastest growth at a CAGR of 10.2% during 2026–2035, fueled by expanding digital health infrastructure mandates and modernization of healthcare systems

Segment Insights:

- Clinical practice management software market cloud-based delivery mode segment is expected to capture a 68.8% share by 2035, propelled by its scalability, reduced upfront costs, and seamless system updates

- Integrated CPMS with EHR segment is projected to lead the market by 2035, impelled by its ability to streamline workflows and eliminate duplicate data entry

Key Growth Trends:

- Government led digital health infrastructure programs

- Increasing patient volume in public health systems

Major Challenges:

- Complex and costly EMR/HER Integration

- Navigating divergent and discriminatory regulatory frameworks

Key Players: Epic Systems Corporation (U.S.), Cerner Corporation (U.S.), Athenahealth, Inc. (U.S.), NextGen Healthcare, Inc. (U.S.), Greenway Health, LLC (U.S.), Allscripts Healthcare, LLC (U.S.), eClinicalWorks (U.S.), CareCloud Corporation (U.S.), CompuGroup Medical SE (Germany), Dedalus Group (Italy), DXC Technology (U.S.), Advanced MD (U.S.), Kareo (U.S.), DrChrono (U.S.), Practice Fusion (U.S.), NTT DATA Corporation (Japan), Reveleer (U.S.), Tieto Caretech (Finland), Vee Healthtek (India), PracticeSuite (U.S.).

Global Clinical Practice Management Software Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.8 billion

- 2026 Market Size: USD 4.1 billion

- Projected Market Size: USD 7.6 billion by 2035

- Growth Forecasts: 7.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (44.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, United Kingdom, Japan, Canada

- Emerging Countries: China, India, Brazil, South Korea, Mexico

Last updated on : 28 April, 2026

Clinical Practice Management Software Market - Growth Drivers and Challenges

Growth Drivers

- Government led digital health infrastructure programs: National digital health missions are stimulating the adoption of integrated clinical and administrative systems. As per the World Bank 2023 data, nearly 442 million ABHA numbers were generated, and 293 million patient health records were linked to ABHA accounts. This enables interoperability across healthcare providers and payers. This initiative mandates digital record integration, increasing reliance on practice management platforms for scheduling, billing, and patient coordination. In the UK, NHS England has committed substantial funding toward digital transformation, targeting full digitization of health records and administrative systems across trusts. These initiatives create standardized digital ecosystems where practice management software acts as a core operational layer.

- Increasing patient volume in public health systems: Rising patient volumes in government-funded healthcare systems are intensifying the need for efficient administrative workflows. According to the CMS December 2025 data, 100 practitioners in the nation provide procedure codes over 10,000 times annually or have more than USD 10 million in annual allowed charges. This volume concentration means a small number of high-volume providers generate a disproportionate share of administrative burden, directly stimulating the demand for automated scheduling, claims management, and revenue cycle modules within the clinical practice management software market. Further, the public health systems facing these volumes cannot sustain manual processing without significant billing delays and denial rates. The government procurement bodies are now mandating CPMS adoption as a condition for continued reimbursement participation mainly for practices crossing a certain volume of annual procedure threshold.

- Shift toward value-based care: Government healthcare systems are increasingly transitioning toward value-based care models, which highlight the efficiency outcomes and cost control. The CMS has expanded alternative payment models with a significant portion of Medicare payments now tied to value-based arrangements. These models require detailed tracking of patient outcomes, costs, and administrative processes, increasing the reliance on integrated management systems. Practice management software supports providers in aligning financial operations with performance metrics, enabling better cost control and reporting. The trend is also visible in OECD countries, where the governments are implementing reforms to improve healthcare efficiency. Providers must adopt systems that enable accurate billing analytics and performance tracking to remain financially viable under these models.

Challenges

- Complex and costly EMR/HER Integration: Integration remains a technical and financial nightmare for the new clinical practice management software market. Healthcare providers often consider a lack of seamless EMR integration a deal breaker during procurement. New players must choose between costly direct integrations or middleware services such as Redox or Mirth, which add recurring subscription costs. The Push integration that writes data into the EMR can extend sales cycles due to stringent IT governance and safety reviews at hospital systems. Successful startups have tackled this by building FHIR-native APIs, reducing integration time to weeks rather than months.

- Navigating divergent and discriminatory regulatory frameworks: Regulatory compliance is a fragmented global minefield for clinical practice management software market suppliers. Laws of the GWB target dominant platforms but reverse the burden of proof, forcing designated companies to justify technical interoperability decisions. New entrants must simultaneously comply with HIPAA, GDPR, PIPEDA, and local data residency laws without internal legal expertise. To tackle this, many startups adopt compliance-as-code platforms to automate security audits across multiple jurisdictions.

Clinical Practice Management Software Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.1% |

|

Base Year Market Size (2025) |

USD 3.8 billion |

|

Forecast Year Market Size (2035) |

USD 7.6 billion |

|

Regional Scope |

|

Clinical Practice Management Software Market Segmentation:

Delivery Mode Segment Analysis

Within the delivery mode, the cloud-based delivery mode is the leading sub-segment in the clinical practice management software market and is expected to hold a share value 68.8% by the end of 2035. The segment is driven by its scalability, lower upfront costs, and seamless updates. According to the Health IT June 2021 data, nearly 78% of office-based physicians in the U.S. reported using a cloud-based or web-based practice management system. This rapid adoption reflects the need for remote access, automated billing, and interoperability with telehealth platforms. Cloud solutions allow small and mid-sized practices to avoid expensive on-premises servers while maintaining compliance with data security standards. Moreover, the cloud-based CPMS continues to dominate as healthcare organizations prioritize real-time data sharing across ambulatory and hospital settings.

Office-based Physician Electronic Health Record Adoption, 2021

|

Year |

Any EHR |

Basic EHR |

Certified EHR |

|

2004 |

20.8% |

— |

— |

|

2005 |

23.9% |

— |

— |

|

2006 |

29.2% |

10.5% |

— |

|

2007 |

34.8% |

11.8% |

— |

|

2008 |

42.0% |

16.9% |

— |

|

2009 |

48.3% |

11.8% |

— |

|

2010 |

51.0% |

27.9% |

— |

|

2011 |

57.0% |

33.9% |

— |

|

2012 |

71.8% |

39.6% |

— |

|

2013 |

78.4% |

48.1% |

— |

|

2014 |

82.8% |

50.5% |

74.0% |

|

2015 |

86.9% |

53.9% |

77.9% |

|

2016 |

86.9% |

— |

77.0% |

|

2017 |

85.9% |

— |

79.7% |

|

2018 |

92.1% |

— |

78.7% |

|

2019 |

90.0% |

— |

72.0% |

|

2021 |

88.0% |

— |

78.0% |

Source: Health IT June 2021

Component Segment Analysis

Under the component segment, the integrated CPMS with EHR sub-segment leads in the clinical practice management software market because it eliminates duplicate data entry and streamlines clinical and administrative workflows. According to the OECD September 2023 data, nearly 83% of the eligible hospitals use a certified EHR system with integrated practice management functionality. This integration enables automatic charge capture eligibility verification and patient scheduling directly from the clinical record. Practices using integrated systems report fewer billing errors and improved revenue cycle times. Moreover, the adoption is rising as the providers move away from standalone CPMS to unified platforms that support value-based care reporting and population health analytics.

Practice Size Segment Analysis

Large hospitals and health systems represent the leading practice-size subsegment in the clinical practice management software market. The segment is driven to coordinate hundreds of providers across multiple outpatient locations. According to the PESP Private Equity Hospital Tracker, April 2025, there are nearly 8.5% of private hospitals and 22.6% of all proprietary for-profit hospitals. This concentration of for-profit ownership accelerates demand for standardized, enterprise-grade CPMS to maximize revenue cycle efficiency across multi-site networks. Additionally, large health systems increasingly mandate cloud-based CPMS to enable real-time data sharing between acute and ambulatory settings. Further, the vendors are tailoring their platforms with advanced analytics and automated scheduling to serve this high-value, consolidating customer base.

Our in-depth analysis of the clinical practice management software market includes the following segments:

|

Segment |

Subsegments |

|

Delivery Mode |

|

|

Practice Size |

|

|

Application |

|

|

End user |

|

|

Component |

|

|

Functionality |

|

|

Deployment Model |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Clinical Practice Management Software Market - Regional Analysis

North America Market Insights

North America is dominating the global clinical practice management software market and is poised to hold the regional revenue share of 44.5% by the end of 2035. The region has benefited from the targeted public investments and funding programs aimed at stimulating digital transformation across the healthcare systems. For instance, the DHDP 2024 report indicates that the Government of Canada has allocated up to USD 25 million by March 2027 under the Strategic Innovation Fund to support the technology-driven projects, with individual project funding ranging between USD 1 million and USD 7 million. Such initiatives indicate a structured push toward modernization of healthcare operations, including administrative and practice management systems. Moreover, the U.S. continues to lead in healthcare expenditure, reinforcing the scale of demand for efficient administrative solutions. These funding mechanisms and high expenditure levels are enabling the healthcare providers to invest in scalable software platforms that improve billing accuracy, patient scheduling, and compliance reporting.

The rising administrative complexity and the federal program scale are expanding the clinical practice management software market in the U.S. According to the MedPac July 2025 data, the Medicare enrollment surpassed 66 million beneficiaries in 2023, increasing the claims volume and billing coordination requirement across providers. Additionally, the Regulations July 2025 data reported that the Medicaid spending reached USD 807.5 billion in 2022, reflecting a significant growth in public insurance utilization and reimbursement workflows. The healthcare expenditure highlights the operational scale at which the administrative systems must function. These data point to a sustained demand for robust scheduling, claims management, and compliance tracking platforms. As federal healthcare programs continue to expand and diversify payment models, providers are prioritizing integrated software systems to manage high transaction volumes and ensure financial and regulatory alignment.

Increased digital health adoption and government-backed investment, alongside structural inefficiencies in existing systems, are driving the growth of the clinical practice management software market in Canada. According to the NLM April 2023 data, the share of physicians offering telemedicine during the pandemic surged from 20% to 80%, expanding the reliance on digital platforms for patient management and administrative workflows. The federal government has already invested over USD 3.1 billion in health information technology, with an additional USD 505 million allocated in 2023 to Canada Health Infoway to improve system integration. However, decentralized provincial systems remain non-interoperable and inconsistent, creating operational challenges and driving demand for unified administrative solutions. Further, with provinces requesting an additional USD 28 billion in healthcare funding, the focus on cost efficiency and interoperability is expected to accelerate the adoption of integrated practice management platforms across Canada.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the clinical practice management software market and is poised to expand at a CAGR of 10.2% during the assessed period, 2026 to 2035. The region is driven by the national digital health infrastructure mandates and the rapid modernization of public healthcare delivery systems. Governments across the region are prioritizing the standardization of patient scheduling, billing, and claims management workflows to address the growing patient volumes and improve administrative efficiency in public hospitals and primary care clinics. Cross-border health data exchange frameworks under the regional cooperation agreements are pushing the CPMS vendors to adopt interoperable architectures, allowing seamless patient record sharing across different healthcare facilities within and sometimes between countries. The shift toward value-based reimbursement models in the nation is pushing the providers to invest in the platforms that can track clinical outcomes alongside financial performance.

Rapid public digital health adoption and government-backed infrastructure development are expanding the clinical practice management software market in India. According to the India Budget June 2024 article, over 64.86 crore ABHA accounts have been created along with 39.77 crore health records linked digitally in 2024, enabling standardized patient data management across care settings. The ecosystem is further strengthened by the registration of 3.06 lakh health facilities and 4.06 lakh healthcare professionals, indicating widespread system participation. Additionally, large-scale outreach initiatives such as 25.25 lakh health melas with 20.66 crore cumulative footfall highlight the growing patient base entering formal healthcare systems. These developments are increasing the need for scalable administrative platforms to manage patient flow records and billing, positioning practice management software as a critical component of India’s evolving digital healthcare infrastructure.

The clinical practice management software market in China is growing rapidly alongside the expansion of its digital healthcare ecosystem and strong institutional support. The country’s digital healthcare market reached USD 27.5 billion in 2022 and in 2024, USD 57.5 billion, reflecting a sustained high growth momentum. Adoption of the digital systems is widespread, with the electronic medical record coverage reached 90% of tertiary hospitals, 60% in secondary hospitals, and 40% in primary hospitals, creating a robust foundation for integrated administrative platforms. Additionally, the establishment of over 3,000 internet hospitals and telemedicine services benefiting 25.9 million people is increasing the demand for scalable patient management and billing systems, as per the NLM October 2024 study. Moreover, the ongoing government focus on infrastructure and regulatory frameworks continues to support long-term clinical practice management software market expansion.

Europe Market Insights

The national digital health mandates and cross-border interoperability requirements are driving the clinical practice management software market in Europe. According to the SVEIKATOS CENTRAS October 2025 data, the European Health Data Space manages health data for 450 million citizens across 27 member states. This unified governance framework compels all CPMS vendors operating in Europe to align their platform with EHDS technical specifications, including standardized APIs and common semantic data models. Further, the member states are increasingly linking national reimbursement payments to EHDS compliance, creating financial consequences for practices using non-compliant software. As a result, the CPMS suppliers that certify their products against EHDS interoperability standards gain preferential access to public procurement tenders across multiple European countries.

The clinical practice management software market in Germany is expanding in line with the national digital health transformation initiatives and strong institutional backing. According to the NLM May 2024 study, the Federal Ministry of Health, holding 51% of the stake in Gematik, is actively driving the implementation of telematics infrastructure and electronic health records, creating a foundation for integrated administrative systems. The clinical practice management software market is further supported by the country’s large healthcare base, with around 84.3 million citizens requiring coordinated care delivery. Digitization presents a significant economic opportunity, with estimates indicating USD 45.5 billion in annual potential savings and efficiency gains within the healthcare systems. Further, the policy reforms, such as lifting the 30% cap on telemedicine services and targeting 80% paperless communication by 2026, as per the Bundesministerium für Gesundheit, March 2023 data, are stimulating the demand for scalable interoperable practice management solutions across providers.

High adoption of digital systems and strong data integration across primary care are shaping the clinical practice management software market in the UK. According to the NLM August 2023 study, the EMIS Health and TPP together cover 90% of GP practices in England, indicating a highly consolidated and digitized provider landscape that facilitates integration of administrative and clinical workflows. In Wales, the Welsh Longitudinal General Practice Dataset covers 83% of the population and 80% of GP practices, demonstrating an extensive use of linked health data systems to support care coordination and reporting. Further, the January 2025 acquisition of Meddbase by Cority reflects the ongoing investment and consolidation in cloud-based practice management solutions. These factors support the market growth by enabling scalable interoperable platforms aligned with national healthcare digitization priorities.

Key Clinical Practice Management Software Market Players:

- Epic Systems Corporation (U.S.)

- Cerner Corporation (U.S.)

- Athenahealth, Inc. (U.S.)

- NextGen Healthcare, Inc. (U.S.)

- Greenway Health, LLC (U.S.)

- Allscripts Healthcare, LLC (U.S.)

- eClinicalWorks (U.S.)

- CareCloud Corporation (U.S.)

- CompuGroup Medical SE (Germany)

- Dedalus Group (Italy)

- DXC Technology (U.S.)

- Advanced MD (U.S.)

- Kareo (U.S.)

- DrChrono (U.S.)

- Practice Fusion (U.S.)

- NTT DATA Corporation (Japan)

- Reveleer (U.S.)

- Tieto Caretech (Finland)

- Vee Healthtek (India)

- PracticeSuite (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Epic Systems Corporation is a dominant player in the clinical practice management software market, offering an integrated platform that unifies scheduling, billing, and patient record management across large hospital networks. Epic has advanced the market by embedding real-time data analytics and interoperability tools into its CPMS, enabling seamless ambulatory and inpatient care coordination.

- Cerner Corporation leverages its broad health IT ecosystem to strengthen the clinical practice management software market mainly via cloud-based solutions that streamline the revenue cycle management and appointment scheduling. A key advancement by Cerner is the integration of CPMS data with its population health analytics and remote monitoring capabilities, allowing practices to track patient outcomes across care episodes.

- Athenahealth, Inc has redefined the clinical practice management software market with its cloud native, continuously updated platform that combines practice management HER and patient engagement. The company’s strategic advancement lies in using live CPMS data for various providers to benchmark performance and automate medical coding and billing. In April 2026, the company announced that it is bringing rater8’s AI-powered reputation management capabilities into AI-native athenaOne.

- NextGen Healthcare, Inc focuses on customizing the clinical practice management software market for ambulatory and specialty practices, offering robust tools for scheduling, claims management, and interoperability. Its major advancement involves embedding CPMS data into next-gen population health and patient engagement modules, which support remote monitoring and care gap detection.

- Greenway Health, LLC serves the clinical practice management software market with its Intergy and SuccessEHS platforms designed for small to mid-sized ambulatory practices. The company has advanced its CPMS by integrating telehealth and patient reminder systems directly with clinical data, enabling real-time synchronization of appointments, lab results, and billing. According to the 2024 annual report, the number of CCDA created in the year was nearly 2,181,699.

Here is a list of key players operating in the global clinical practice management software market:

The global clinical practice management software market is highly competitive, featuring a mix of established U.S. giants and emerging regional players. Key strategic initiatives include aggressive mergers and acquisitions to expand integrated Electronic Health Record capabilities, cloud-based deployment models for scalability, and AI-driven analytics to enhance the clinical decision making and revenue cycle management. For example, in April 2025, Reveleer announced the acquisition of Novillus, a provider of insight-driven care gap management and frictionless provider engagement solutions. Vendors are also focusing on interoperability and patient engagement tools to improve care coordination. While the U.S. firms dominate specialized providers from Europe, Asia Pacific, and Australia are gaining traction via localized solutions, government digitalization mandates, and customized offerings for small to mid-sized practices.

Corporate Landscape of the Clinical Practice Management Software Market:

Recent Developments

- In April 2026, Tieto Caretech, x‑tention, and Better have entered into a strategic partnership to accelerate the next generation of open, patient‑centric healthcare systems. United by complementary strengths and a shared commitment to openness, interoperability, and data freedom, the three companies are setting a new benchmark for how healthcare IT can evolve.

- In September 2025, Vee Healthtek, a leader in AI-enabled healthcare solutions, announced its acquisition of Precision Practice Management (Precision). This strategic acquisition unites two trusted revenue cycle management companies with a shared commitment to improving financial performance and operational outcomes for healthcare organizations.

- In September 2025, PracticeSuite announced the successful acquisition of MicroMD, a 40-year-old company with a certified Electronic Health Record (EHR) platform, trusted by thousands of healthcare providers nationwide. This acquisition adds a matured, trusted, and feature-rich EHR to PracticeSuite’s portfolio of offerings and brings with it a long-standing, loyal customer base.

- Report ID: 8534

- Published Date: Apr 28, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.