Spinal Surgery Market Outlook:

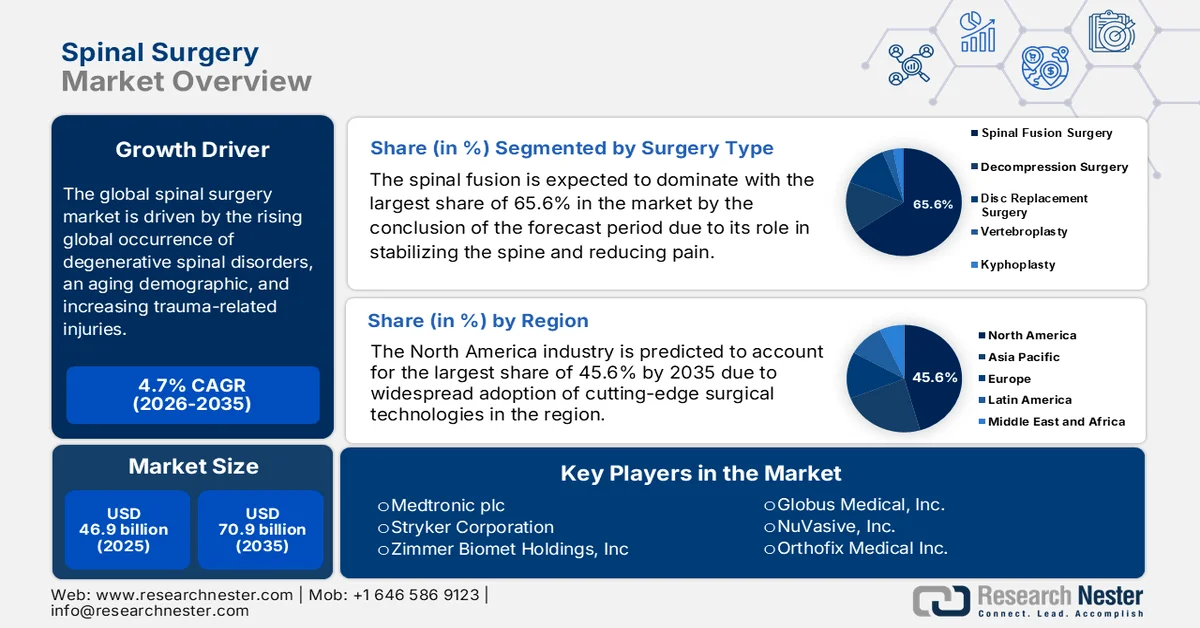

Spinal Surgery Market size was valued at USD 46.9 billion in 2025 and is anticipated to reach USD 70.9 billion by 2035, expanding at a CAGR of 4.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of spinal surgery is assessed at USD 49.1 billion.

The global spinal surgery market is all set to witness noteworthy expansion, which is primarily driven by the rising global occurrence of degenerative spinal disorders, an aging demographic, and increasing trauma-related injuries. In this regard, the article published by the World Health Organization (WHO) in April 2024 revealed that spinal cord injury affects more than 15 million people globally, with around 15.4 million cases in a year, and contributes to more than 4.5 million years lived with disability on a yearly basis. It also mentioned that traumatic causes, primarily falls and road traffic injuries, account for the majority of cases, whereas ageing populations are driving a rise in non-traumatic SCI associated with degenerative and vascular conditions. Therefore, these statistics underscore a huge opportunity for spinal surgery solutions in the years ahead.

Historic Spine Surgery Volume Trends in New York City (2019-2023)

|

Year |

Total Surgeries |

% Change vs 2019 |

|

2019 |

26,066 |

- |

|

2020 |

20,437 |

−21.6% |

|

2021 |

24,829 |

−4.8% |

|

2022 |

26,271 |

+0.8% |

|

2023 |

30,485 |

+17.0% |

Source: NIH

Furthermore, the spinal surgery market is poised for continued transformation through digital surgery ecosystems and bioresorbable materials. There has been an intense economic burden, which is elevating the need for cost-effective surgical solutions. As per the article published by the National Institute of Health (NIH) in October 2025 in the U.S., adult spinal deformity affects around 0.5% of the commercially-insured adult population, which equates to more than 567,000 patients in a span of seven years. The economic burden per patient is substantial, with payer expenditures averaging USD 7,619 annually and societal costs reaching USD 8,759 per patient, influenced by both nonoperative 44% to 48% and operative care 51% to 55%. Surgical intervention rates represented 3.5% undergoing fusions and 2.9% decompressions annually, so these procedures account for the majority of costs. Over a two-year horizon, cumulative payer costs per 100,000 beneficiaries totaled USD 5.4 million, whereas societal expenditures reached almost USD 8.9 billion, thus highlighting areas for cost optimization and targeted clinical innovation.

Key Spinal Surgery Market Insights Summary:

Regional Highlights:

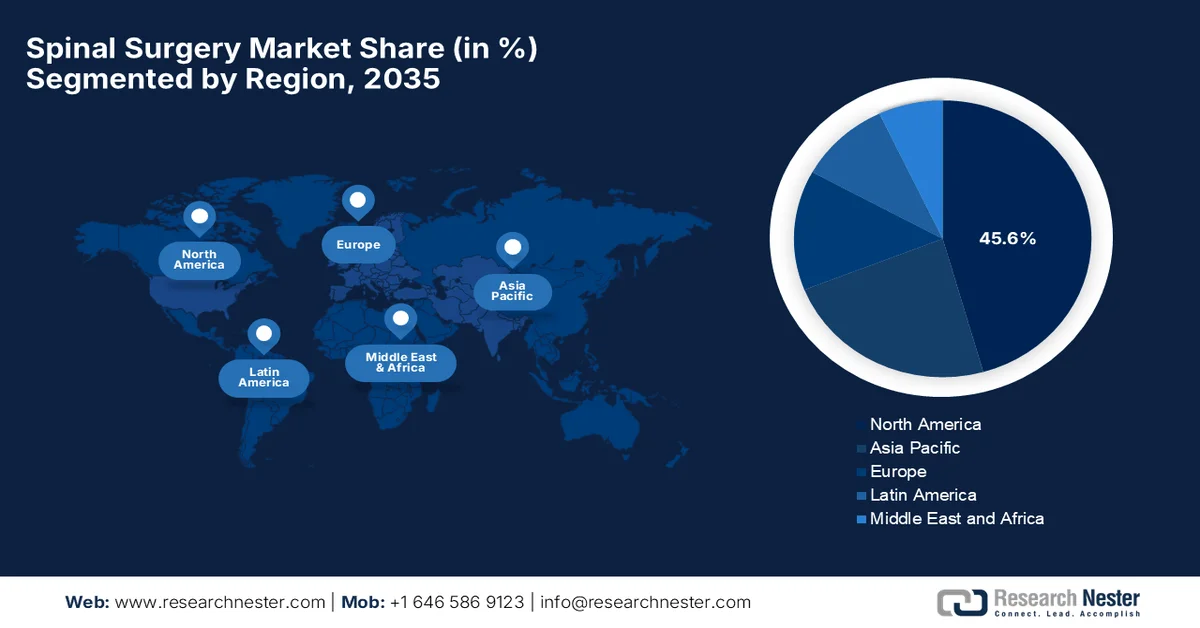

- North America spinal surgery market is projected to command a 45.6% share by 2035, reinforced by advanced healthcare infrastructure and increasing adoption of robotic-assisted surgical technologies

- Asia Pacific is poised to register significant expansion over the 2026–2035 period, fueled by expanding healthcare access and supportive government initiatives enhancing surgical capabilities

Segment Insights:

- Spinal Surgery Market spinal fusion segment is forecasted to capture a dominant 65.6% share by 2035, propelled by its proven effectiveness in stabilizing the spine and alleviating degenerative disc disease-related pain

- Lumbar segment is expected to secure a notable revenue share by 2035, impelled by the rising global prevalence of lower back disorders increasing surgical demand

Key Growth Trends:

- Technological advancements in surgical techniques

- Expansion of healthcare infrastructure

Major Challenges:

- Risk of complications and revisions

- Pricing pressure and intense competition

Key Players: Medtronic plc (U.S.), Johnson & Johnson - DePuy Synthes (U.S.), Stryker Corporation (U.S.), Zimmer Biomet Holdings, Inc. (U.S.), Globus Medical, Inc. (U.S.), NuVasive, Inc. (U.S.), Orthofix Medical Inc. (U.S.), Alphatec Spine, Inc. (U.S.), RTI Surgical Holdings, Inc. (U.S.), Xtant Medical Holdings, Inc. (U.S.), B. Braun Melsungen AG (Germany), Ulrich GmbH & Co. KG (Germany), Spinal Elements (U.S.), Highridge Medical (U.S.), Spineart SA (Switzerland), Medacta International SA (Switzerland), Joimax GmbH (Germany), Otsuka Medical Devices Co., Ltd. (Japan), Seikagaku Corporation (Japan), GS Medical Co., Ltd. (South Korea), Life Healthcare Group (Australia), Nutech Medical Devices Pvt. Ltd. (India).

Global Spinal Surgery Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 46.9 billion

- 2026 Market Size: USD 49.1 billion

- Projected Market Size: USD 70.9 billion by 2035

- Growth Forecasts: 4.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 13 April, 2026

Spinal Surgery Market - Growth Drivers and Challenges

Growth Drivers

- Technological advancements in surgical techniques: Technological innovation is readily transforming spinal surgery, thereby boosting procedural success and treatment options. Breakthroughs such as robotic-assisted systems, advanced imaging with real‑time navigation, and 3D‑printed implants improve precision and lower complication rates, thus boosting the overall spinal surgery market. In August 2024, DePuy Synthes announced the launch of the VELYS active robotic-assisted system (VELYS SPINE), which is its first dual-use robotics and standalone navigation platform for spine surgery. The system is FDA-cleared for cervical, thoracolumbar, and sacroiliac fusion procedures, and it integrates with J&J’s existing spine portfolio. Thus, with such continued advancements, the spinal surgery market will witness extensive growth in the years ahead.

- Expansion of healthcare infrastructure: Growing healthcare infrastructure in emerging markets is proactively enhancing access to spinal surgical services, deliberately contributing to spinal surgery market growth. Booming investments in hospitals, ambulatory surgical centers, and specialty clinics particularly enhance surgical capacity and the availability of advanced procedures. In this context, the Manitoba government, in March 2026, generously invested a total of USD 2.7 million to expand advanced spine surgery at Concordia Hospital, thereby enhancing surgical capacity and reducing patient recovery times. Surgeons performed the first navigated instrumentation spinal surgery in June 2025 by using 3D imaging and precision guidance, enabling minimally invasive procedures, with most patients discharged the same or next day, thus suitable for bolstering the overall spinal surgery market growth.

- Demand for minimally invasive and outpatient procedures: There is a structural shift towards minimally invasive and outpatient spinal surgeries, which is influenced by patient preference for faster recovery and shorter hospital stays. In June 2023, the article, published by NIH, revealed that it analyzed 164 minimally invasive cervical and lumbar spine surgeries performed in ambulatory surgery centers during the COVID-19 pandemic. The article underscored that procedures included ACDF, ALIF, MILD, PELD, and kyphoplasty, with all patients achieving same-day discharge. In this context, the surgeries demonstrated that outpatient, minimally invasive approaches are safe and effective, which have reduced hospital stays, perioperative pain, and recovery time. Therefore, this experience highlights the growing adoption of advanced minimally invasive techniques, thereby meeting patient demand for faster recovery and less invasive treatment options, thus benefiting the overall spinal surgery market.

Challenges

- Risk of complications and revisions: Influenced by the continued technical advancements, spinal surgeries come with risks such as infection, nerve damage, implant failure, and even segment degeneration. Therefore, these complications can lead to repeated surgical procedures, which in turn increase both healthcare costs and patient burden. At the same time, negative clinical outcomes also affect patient confidence and physician adoption of new devices or techniques. In addition, medico-legal risks associated with surgical complications can discourage surgeons from adopting innovative but less-established technologies. Manufacturers in the spinal surgery need to make continuous investments in improving product safety and clinical evidence. Hence, the persistent risk of complications is considered to be a major challenge that is limiting the widespread acceptance and growth in the spinal surgery market.

- Pricing pressure and intense competition: The spinal surgery market is intensely competitive, which has dominant global players along with numerous regional manufacturers who are competing for revenue shares. The existence of this competition leads to pricing pressure, particularly for commoditized products such as spinal fusion implants. Hospitals and group purchasing organizations negotiate aggressively, which in turn is reducing profit margins for manufacturers. At the same time, emerging spinal surgery market players offer cost-effective alternatives, which exacerbates the intensifying competition. In this context, companies need to differentiate themselves through innovation, branding, and clinical outcomes rather than focusing on price alone. Balancing cost competitiveness with continuous investment in research and development is a major strategic challenge for both established and emerging players in the market.

Spinal Surgery Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.7% |

|

Base Year Market Size (2025) |

USD 46.9 billion |

|

Forecast Year Market Size (2035) |

USD 70.9 billion |

|

Regional Scope |

|

Spinal Surgery Market Segmentation:

Surgery Type Segment Analysis

The spinal fusion is expected to dominate with the largest share of 65.6% in the spinal surgery market by the conclusion of the forecast period. The segment’s dominance is largely propelled by its established effectiveness in efficiently stabilizing the spine and reducing pain from degenerative disc disease and other spinal issues. In February 2024, the U.S. Food and Drug Administration (FDA) approved the Xstim Spine Fusion Stimulator, which is a bone growth stimulator especially designed to support lumbar spinal fusion surgery. This particular device uses electrical signals delivered through skin electrodes to promote bone healing and fusion in the lower back. This approval underscores the ongoing innovation in spinal fusion treatments, solidifying its role as a primary surgical method for spinal stabilization, hence denoting a wider segment scope.

Historic Utilization Trends by Spine Surgery Procedure Type (2012-2021)

|

Procedure Type |

2012 |

2021 |

% Change |

|

Total Procedures |

30,449 |

36,294 |

+19.20% |

|

Cervical |

7,354 |

9,605 |

+30.61% |

|

Lumbar |

22,456 |

26,940 |

+19.97% |

|

Fusion |

19,388 |

23,141 |

+19.36% |

|

Decompression |

19,282 |

20,093 |

+4.21% |

Source: NIH

Application Segment Analysis

The lumbar, which is under the application segment, is anticipated to grow with a considerable revenue share in the spinal surgery market by the conclusion of the forecast period. The growth of the segment is largely attributable to the high prevalence of lower back disorders, which is significantly increasing lumbar surgery demand. In June 2023, the article published by the WHO reported that low back pain affected almost 619 million people worldwide in a year, and projections identified that this number will rise to 843 million by 2050, influenced by ageing and population growth. In addition, the article also stated that it is the leading cause of disability globally, with peak cases occurring between the ages of 50 and 55 and higher prevalence in women. Besides, about 90% of cases are non-specific, reflecting the importance of rehabilitation and lifestyle interventions to manage symptoms and improve function, thus denoting a positive spinal surgery market outlook.

End user Segment Analysis

In terms of end user hospital segment is predicted to hold a significant share in the spinal surgery market during the stipulated timeframe. The segment’s growth is propelled by its comprehensive infrastructure, access to multidisciplinary surgical teams, and the capability to handle complex spinal procedures. They provide full-spectrum care, i.e., preoperative evaluation, advanced surgical technologies, and postoperative rehabilitation, which makes sure there is better patient outcomes for intricate cases. At the same time, hospitals are considered to be the preferred setting for most spinal surgeries, particularly those requiring specialized equipment, high-risk management, or multi-level interventions. On the other hand, their established expertise and resources sustain their leading position in the market. Thus, the presence of all of these factors responsibly uplifts the subtype’s position in this category.

Our in-depth analysis of the spinal surgery market includes the following segments:

|

Segment |

Subsegments |

|

Surgery Type |

|

|

Application |

|

|

End user |

|

|

Product Type |

|

|

Procedure Type |

|

|

Material |

|

|

Indication |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Spinal Surgery Market - Regional Analysis

North America Market Insights

The North America spinal surgery market is expected to dominate with the largest share of 45.6% by the end of the forecast period. The advanced healthcare infrastructure, rising adoption of surgical technologies, and a heightened demand for spinal procedures are the main factors behind the region’s leadership in this sector. North America’s well-established hospital systems and skilled surgical workforce also solidify its leading position in the global landscape. In June 2025, Ascension’s Dell Children’s Medical Center North Campus became the first pediatric hospital globally to perform spine surgeries using an advanced active robotic-assisted and navigation platform. It mentions that this particular technology enhances precision in complex spinal deformity cases, thereby supporting improved screw placement and faster recovery for patients. In addition, the platform combines standalone navigation with active robotics, and with such technological implementation, the region will witness unprecedented growth in the years ahead.

The presence of an aging demographic and a rapid shift toward outpatient care are responsible for uplifting the overall spinal surgery market in the U.S. Technological advancements are central to this evolution, influenced by a clear move away from traditional open surgeries in support of minimally invasive techniques and robotic-assisted navigation. In June 2023, the U.S. FDA announced the approval of the TOPS system from Premia Spine, Ltd. as a spinal implant especially designed to stabilize the lower spine, and it maintains motion after lumbar decompression surgery. It is attached with pedicle screws, and it supports body weight, allowing movements such as rotation, bending, and flexion. The system can be indicated for patients aged 35-80 with Grade I degenerative spondylolisthesis and lumbar spinal stenosis, thus suitable for bolstering the country’s market growth.

The publicly funded healthcare system that emphasizes wait-time management and the adoption of cost-efficient surgical technologies is supporting the expansion of the spinal surgery market in Canada. Growth is also supported by a rising need for degenerative disc treatments among an aging population, along with a shift toward advanced biomaterials such as 3D-printed titanium. NIH in May 2025 reported that its study in the country assessed around 5,049 patients undergoing elective spinal surgery for degenerative conditions, observing significant improvements in health-related quality of life one year postoperatively. It also mentioned that the mean preoperative SF-12 physical component score of 29.5 improved to 40.5, whereas the mental component score increased from 44.1 to 49.3, with 70% to 75% of patients achieving clinically meaningful benefit. These findings highlight the effectiveness of spinal surgery in restoring physical function, thus uplifting adoption in the country.

APAC Market Insights

The Asia Pacific spinal surgery market is expected to showcase remarkable growth during the discussed tenure. The region’s market is largely driven by a growing middle class with increasing access to sophisticated healthcare infrastructure. The market dynamics are being reshaped by localized manufacturing efforts and government initiatives, which are aimed at improving surgical outcomes while managing the rising demand for degenerative disc disease treatments. As per the official release by J Stage, Japan has established a nationwide spine and spinal cord surgery registry by analyzing 158,263 cases from 1,032 facilities in 2022. The most common diagnoses were lumbar spinal canal stenosis being 32.5%, lumbar disc herniation at 16.6%, and cervical spondylotic myelopathy with 9.7%. It also mentions that the frequently performed procedures are posterior lumbar interbody fusion, posterior spinal fusion, and balloon kyphoplasty, hence denoting a lucrative growth opportunity.

The major push towards domestic medical device innovation is the main factor that is responsible for uplifting the spinal surgery market in China. The market is being reshaped by centralized procurement policies that emphasize cost-efficiency while maintaining high clinical standards across provincial hospital networks. For instance, in September 2025, Shanghai East Hospital introduced a spinal endoscopic technology called uni-port bichannel dual-media by reducing the incision size from 20 cm to just 1 cm. Besides, the dual-channel design provides high-definition visibility and precise surgical control. It also mentioned that since 2021, UBD has been adopted in about 100 hospitals across China, benefiting nearly 4,000 patients, and has expanded to Japan and Thailand for international training, thus making it suitable for standard market growth.

The continuous modernization of private healthcare infrastructure is accelerating growth in the overall spinal surgery market in India. The market is seeing a notable increase in medical tourism and a burgeoning domestic manufacturing sector that aims to provide high-quality, cost-effective alternatives to imported global brands. In September 2023, Shrimad Rajchandra Hospital and Research Centre organized a spine surgery camp in South Gujarat with the main goal of providing specialized care for rural communities. Besides this particular camp, more than 340 patients were registered, wherein many were suffering from severe spinal conditions, and underwent multiple complex surgeries with detailed after-care plans. The initiative brought spine treatment to a rural setting, thereby making specialized care accessible to underserved populations. Therefore, with such awareness programs, the country is encouraging the adoption of spine surgeries, allowing more players to establish their footprint in the country.

Europe Market Insights

Europe spinal surgery market has established itself as a predominant leader in the global dynamics, effectively attributable to a strong emphasis on clinical evidence and a rapid shift toward motion preservation techniques. In addition, the market is characterized by a high degree of fragmentation across different nations, wherein the growth is driven by a steady migration of procedures toward specialized outpatient spine centers and ambulatory settings. As per an article published by NIH in January 2026, the Swiss National Spinal Implant Registry, which is governed by the SIRIS Foundation and operated by EUROSPINE, is one of the world’s first mandatory nationwide spinal implant registries, capturing data from 91 hospitals between 2021 and 2023. It recorded 12,815 surgeries involving 75,522 implants across 11,789 patients, focusing on degenerative disease, osteoporotic fractures, and spondylolisthesis. Therefore, these statistics underscore that Europe’s leadership in spinal surgery is strongly supported by evidence-based practices, enabling continuous improvement in surgical outcomes.

A primary priority towards high-quality clinical outcomes and the early adoption of improved technologies is driving the expansion of the spinal surgery market in Germany. The landscape is positively influenced by a well-established reimbursement system that readily encourages technical innovation with a strong focus on cost-efficiency and the shift away from certain procedures to specialized outpatient settings. In October 2024, the RKH Orthopedic Clinic in Markgröningen introduced the LoopX robotic imaging system to enhance precision and safety in spinal surgeries. It also notes that this advanced technology provides high-resolution 2D and 3D imaging with minimal radiation, guided instrument placement, and real-time monitoring. Enabling minimally invasive procedures, it reduces risks such as nerve damage, infections, and implant misplacement, thus making it suitable for standard market growth.

The UK spinal surgery market has gained enhanced exposure owing to the noteworthy rise in day-case procedures within both public and private healthcare sectors. The country’s market also benefits from centralized procurement frameworks, which are aimed at standardizing high-quality care and an increasing reliance on specialized elective hubs to manage the growing demand for degenerative spinal treatments. In January 2026, the James Cook University Hospital in Teesside introduced the ExcelsiusGPS robotic-assisted spine system, which was acquired for almost USD 1.2 million. Besides this, advanced technology efficiently enhances implant positioning accuracy, reduces blood loss and infection risks, and shortens operation times, thereby enabling minimally invasive procedures with quicker recovery. Therefore, with such instances in the country, the market will grow proactively, supported by improved efficiency and wider adoption of minimally invasive techniques.

Key Spinal Surgery Market Players:

- Medtronic plc (U.S.)

- Johnson & Johnson - DePuy Synthes (U.S.)

- Stryker Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Globus Medical, Inc. (U.S.)

- NuVasive, Inc. (U.S.)

- Orthofix Medical Inc. (U.S.)

- Alphatec Spine, Inc. (U.S.)

- RTI Surgical Holdings, Inc. (U.S.)

- Xtant Medical Holdings, Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Ulrich GmbH & Co. KG (Germany)

- Spinal Elements (U.S.)

- Highridge Medical (U.S.)

- Spineart SA (Switzerland)

- Medacta International SA (Switzerland)

- Joimax GmbH (Germany)

- Otsuka Medical Devices Co., Ltd. (Japan)

- Seikagaku Corporation (Japan)

- GS Medical Co., Ltd. (South Korea)

- Life Healthcare Group (Australia)

- Nutech Medical Devices Pvt. Ltd. (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Medtronic is the global leader in this market, which has a product portfolio spanning spinal implants, biologics, navigation, and robotic-assisted systems. The company is highly focused on integrated digital surgery ecosystems and continues to expand through acquisitions and R&D investments.

- Johnson & Johnson DePuy Synthes, which is a subsidiary of Johnson & Johnson, is a major player that is offering a broad range of spinal implants, biomaterials, and enabling technologies. The company deliberately emphasizes innovation in terms of minimally invasive surgery and data-driven surgical planning.

- Stryker Corporation is a leading competitor in this sector, which is best known for its Mako-inspired expansion into robotics and advanced spine solutions. The firm’s spine division concentrates on implants, navigation systems, and enabling technologies for minimally invasive procedures.

- Zimmer Biomet Holdings, Inc. benefits from a focus on spinal fusion devices, motion preservation technologies, and biologics. Besides, the company leverages its expertise in orthopedics to offer integrated musculoskeletal solutions.

- Globus Medical, Inc. is one of the fastest-growing spine-focused companies, which is mostly known for its innovation in implant design and robotic-assisted surgery. The company makes a differentiation through rapid product development cycles and a strong pipeline of advanced technologies.

Below is the list of some prominent players operating in the global spinal surgery market:

Medtronic, Johnson & Johnson, Stryker, and Globus Medical are dominating the spinal surgery market due to their strong portfolios and global reach. Competition in this field is majorly driven by innovation, particularly in minimally invasive surgery, robotics, and navigation systems. At the same time, firms are opting for distinct growth strategies such as mergers, acquisitions, and partnerships with the main goal of expanding capabilities and geographic presence. In this context, in July 2025, Demetra announced the acquisition of OrthoFundamentals, LLC, which is a U.S.-based provider of single-use solutions for sacroiliac joint fusion, and launched Demetra Spine, that is a new global division. In addition, the company is proactively looking to transform spinal surgery through minimally invasive, infection-risk reducing, and value-based solutions.

Corporate Landscape of the Spinal Surgery Market:

Recent Developments

- In March 2026, Spinal Elements received the U.S. FDA 510(k) clearance and completed its first cases with its Ventana A ALIF System, expanding the Ventana platform of 3D printed titanium interbodies. It is especially designed to maximize bone graft delivery, restore alignment, and reduce subsidence risk.

- In February 2026, Medtronic received the U.S. FDA clearance for its Stealth AXiS surgical system, the first platform to integrate planning, navigation, and robotics for spine surgery. It consists of LiveAlign real-time tracking and seamless AiBLE ecosystem integration to streamline workflows, reduce variability, and support personalized care.

- In September 2025, Highridge Medical announced the acquisition of Accelus’s FlareHawk and Toro expandable interbody fusion systems, along with the LineSider pedicle screw system, strengthening its spine surgery portfolio. These products, consists of Adaptive Geometry designs, enhance minimally invasive lumbar solutions.

- Report ID: 3280

- Published Date: Apr 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.