Carbon Capture Utilization and Storage Market Outlook:

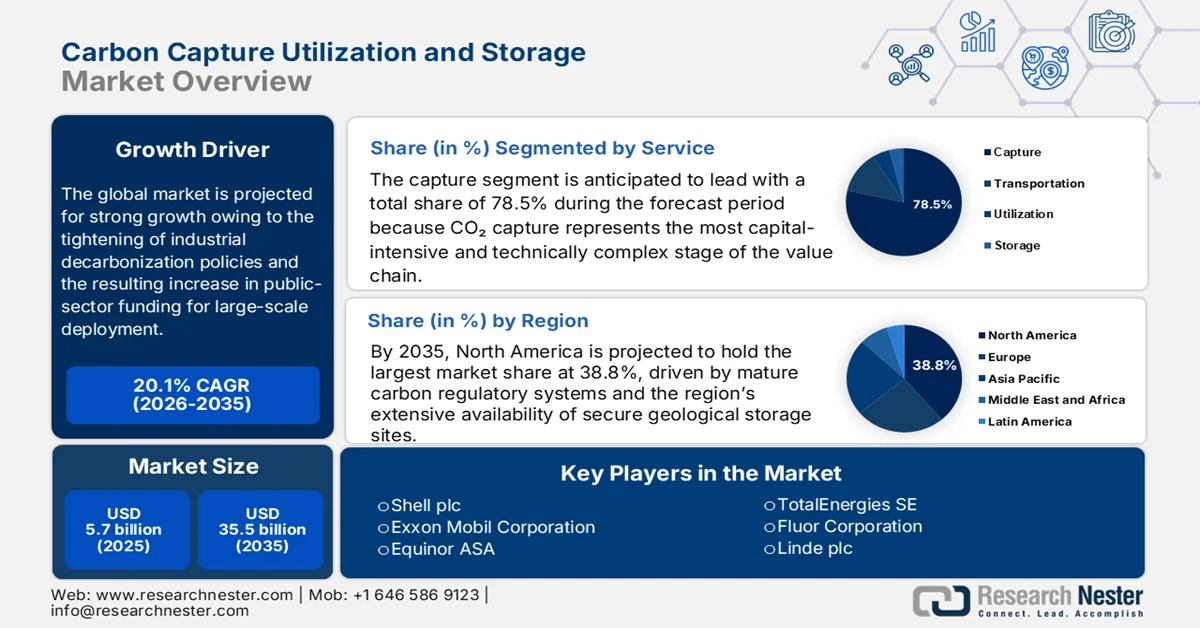

Carbon Capture Utilization and Storage Market size was valued at USD 5.7 billion in 2025 and is projected to reach USD 35.5 billion by the end of 2035, registering around 20.1% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of carbon capture utilization and storage is evaluated at USD 6.8 billion.

The global carbon capture utilization and storage market has gained enhanced momentum owing to the tightening of industrial decarbonization policies and the resulting increase in public-sector funding for large-scale deployment. Industrial activities remain a major source of emissions, which are creating sustained demand for carbon management infrastructure. In April 2024, the article published by the International Energy Agency revealed that CCUS is emerging, with more than 700 projects in development and 45 commercial facilities already operating worldwide. There is a 35% rise in announced capture capacity and a 70% increase in storage capacity in 2023, but still, deployment remains behind the net-zero emissions by 2050 scenario, reaching only 40% of the required capture and 60% of storage. Governments in the U.S., Europe, Germany, and Japan are driving progress through substantial funding, legislation, and strategic initiatives, and thus contributing to the market’s expansion.

Global Carbon Capture and Storage (CCUS) Statistics 2023-2030: Capacity, Projects, and Net Zero Targets

|

Metric |

Value |

|

Operating facilities |

45 |

|

Projects in development |

700+ |

|

Annual CO₂ captured (2023) |

50 Mt |

|

Announced capture capacity (2030) |

435 Mt |

|

Announced storage capacity (2030) |

615 Mt |

|

Target in the NZE 2050 scenario |

~1 Gt CO₂ per year |

Source: IEA

Furthermore, the burgeoning investments in terms of low-carbon infrastructure, advancements in capture technologies and are enhancing commercial viability for solutions in the market. Besides, the integration of carbon capture with emerging technologies such as hydrogen production and sustainable fuel development is also strengthening market prospects. In March 2026, the article published by IEA stated that it developed the CCUS Projects Explorer, which is a global database to track large-scale carbon capture, utilization, and storage initiatives. It includes projects commissioned over the past few decades with capacities above 100,000 tons per year, or 1,000 tons for direct air capture facilities. The dataset is highly focused on projects with clear emissions reduction goals, excluding low-benefit uses such as food and beverage applications or conventional industrial processes. Such a database complements other clean energy tracking tools, helping policymakers, researchers, and industry stakeholders monitor advancements in carbon management and thus providing a positive outlook for the market’s development.

Key Carbon Capture Utilization and Storage Market Insights Summary:

Regional Highlights:

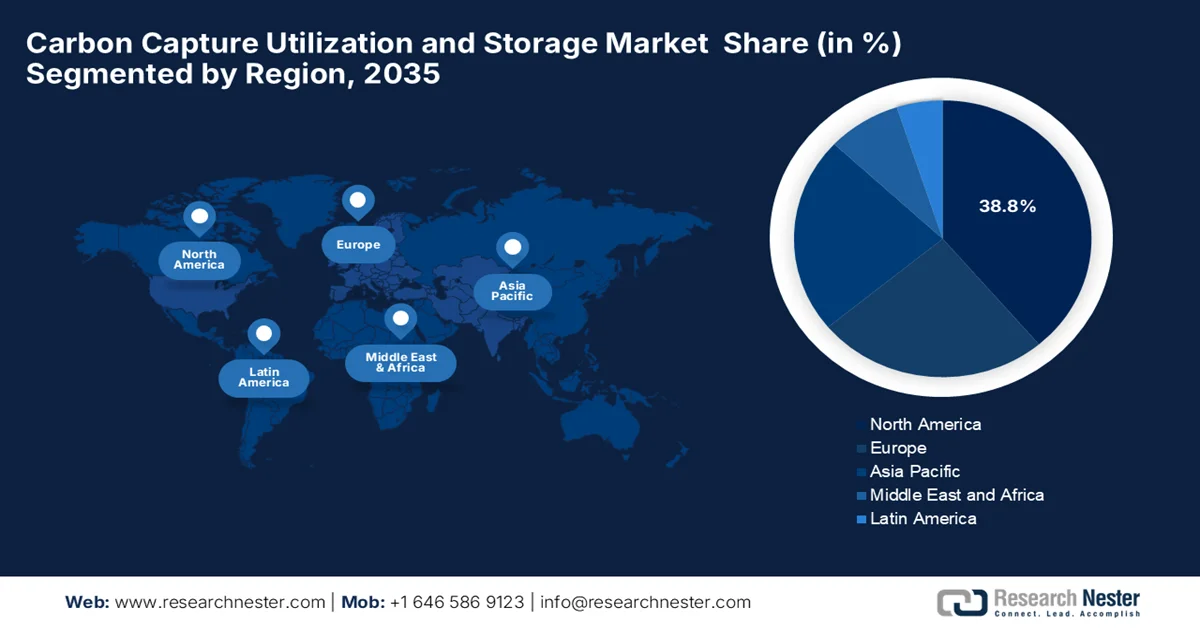

- North America is projected to account for 38.8% of the carbon capture utilization and storage market by 2035, reinforced by well-established carbon policy mechanisms, suitable geological storage sites, and extensive oil and gas infrastructure supporting large-scale deployment

- Asia Pacific is poised to witness considerable growth in the market throughout 2026-2035, stimulated by the need to balance economic expansion with national net-zero decarbonization mandates through large-scale industrial retrofitting

Segment Insights:

- The capture segment is anticipated to command 78.5% of the carbon capture utilization and storage market by 2035, underpinned by the capital-intensive nature of CO₂ capture requiring advanced separation technologies and substantial upfront engineering investment

- The solvents and sorbents segment is expected to secure a considerable share during 2026-2035, fueled by widespread industrial adoption of proven chemical absorption systems supported by mature supply chains and seamless integration into existing industrial infrastructure

Key Growth Trends:

- High-value subsidies and tax incentives

- Critical solution for hard-to-abate industries

Major Challenges:

- Regulatory, permitting, and storage liability challenges

- High capital investment and project financing constraints

Key Players: Shell plc (UK), Exxon Mobil Corporation (U.S.), Equinor ASA (Norway), TotalEnergies SE (France), Fluor Corporation (U.S.), Linde plc (UK), Mitsubishi Heavy Industries, Ltd. (Japan), JGC Holdings Corporation (Japan), SLB (U.S.), Aker Solutions ASA (Norway), Global Cement and Concrete Association (UK), Global CCS Institute (Australia), CarbonFree (U.S.).

Global Carbon Capture Utilization and Storage Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.7 billion

- 2026 Market Size: USD 6.8 billion

- Projected Market Size: USD 35.5 billion by 2035

- Growth Forecasts: 20.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Canada, Norway, United Kingdom

- Emerging Countries: Japan, South Korea, India, Saudi Arabia, Australia

Last updated on : 23 June, 2026

Carbon Capture Utilization and Storage Market - Growth Drivers and Challenges

Growth Drivers

- High-value subsidies and tax incentives: The existence of strong financial support is making projects from the carbon capture utilization and storage market more viable. The incentives readily improve project economics and shorten payback periods, thereby encouraging private-sector participation in this sector. According to the IEA reports published in February 2026, the U.S. Inflation Reduction Act of 2022 has deliberately strengthened the Section 45Q tax credit for carbon dioxide sequestration by increasing incentives for carbon capture, utilization, and storage projects. It provides up to USD 85 per ton of CO₂ permanently stored, USD 60 per ton for CO₂ used in industrial applications or enhanced oil recovery, and up to USD 180 per ton for Direct Air Capture with permanent storage. This particular policy also lowered eligibility thresholds for project size and extended the construction deadline to 2033, thereby making large-scale carbon capture projects more financially viable.

- Critical solution for hard-to-abate industries: CCUS has become highly essential for industries that do not have the capacity to fully decarbonize with the help of renewable energy alone. Sectors such as cement, steel, and chemicals produce unavoidable process emissions whereas CCUS allows existing industrial plants to continue operating while meeting climate targets. For instance, in December 2024, SLB Capturi completed construction of the world’s first industrial-scale carbon capture plant at Heidelberg Materials’ cement facility in Brevik, Norway. This plant is especially designed to capture up to 400,000 metric tons of CO₂ annually, and it enables the production of net-zero cement without compromising quality, thus making it suitable for bolstering the overall market’s growth.

Challenges

- Regulatory, permitting, and storage liability challenges: One of the major challenges for the carbon capture utilization and storage market is regulatory and permitting issues, which can delay project implementation. Developing carbon storage sites requires a huge range of geological assessments, environmental reviews, and approvals from multiple regulatory agencies, which can change across nations. Apart from this, the long-term liability associated with stored carbon dioxide is also a major concern, which includes responsibilities for monitoring, maintenance, and potential leakage risks decades after project completion. In most of the jurisdictions, regulations governing carbon transportation and cross-border storage remain underdeveloped, thereby creating a hindrance to the creation of large-scale carbon management networks.

- High capital investment and project financing constraints: This is also a major burden for the market. The establishment of carbon capture facilities, transportation infrastructure, and long-term storage sites necessitates higher upfront costs. Most of the players operating in the industry hesitate to make investments due to uncertain returns on investment and fluctuating carbon pricing mechanisms. In addition, securing financing for CCUS projects can be difficult due to long project payback periods and regulatory uncertainties. The government incentives, tax credits, and funding programs have improved project economics in several regions, but the financial viability of many projects still depends heavily on policy support, thereby limiting widespread adoption.

Carbon Capture Utilization and Storage Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

20.1% |

|

Base Year Market Size (2025) |

USD 5.7 billion |

|

Forecast Year Market Size (2035) |

USD 35.5 billion |

|

Regional Scope |

|

Carbon Capture Utilization and Storage Market Segmentation:

Service Segment Analysis

The capture segment is anticipated to lead with a total share of 78.5% during the forecast period in the carbon capture utilization and storage market. The dominance is mainly propelled by the fact that CO₂ capture represents the most capital-intensive and technically complex stage of the value chain, which requires advanced separation technologies and significant upfront engineering investment. As a result, capture-focused providers secure higher-value contracts and long-term operational agreements when compared to other service segments. In May 2023, BASF reported that its advanced OASE® blue technology is being deployed at a large-scale CO₂ capture facility through a joint venture between Linde and Heidelberg Materials. The plant is operated by CAP2, and it will capture and liquefy around 70,000 tons of CO₂ annually, marking the world’s first industrial-scale carbon capture and utilization facility.

Technology Segment Analysis

Under this technology category, solvents and sorbents are expected to hold a considerable share in the market during the discussed timeframe. The segment’s growth is largely propelled by widespread industrial adoption of chemical absorption systems, particularly amine-based solvents, which have been refined over decades and are supported by mature supply chains. Therefore, they remain the preferred, bankable option for large-scale emitters who are looking for proven and reliable carbon capture solutions over emerging or less-tested technologies. On the other hand, these systems are being deployed in natural gas processing, hydrogen production, and power generation, representing their commercial readiness at scale. Their ability to integrate into existing industrial infrastructure with minimal process redesign also strengthens adoption.

End user Industry Segment Analysis

The oil and gas sector is expected to grow with a considerable share in the market by the end of 2035. This leadership is driven by the sector’s high regulatory exposure to carbon emissions, coupled with its established CO₂ handling infrastructure. A key advantage is the economic incentive from CO₂-based enhanced oil recovery, which enables operators to generate additional revenue while simultaneously managing emissions. In July 2023, ExxonMobil announced the acquisition of Denbury Inc., which is a leading developer of carbon capture, utilization, and storage solutions. This deal gives ExxonMobil control of the largest CO₂ pipeline network in the U.S., spanning 1,300 miles, with 925 miles concentrated in Louisiana, Texas, and Mississippi, along with 10 onshore sequestration sites. The acquisition strengthens the company’s ability to accelerate CCS deployment and supports multiple low-carbon value chains, including hydrogen, ammonia, biofuels, and direct air capture.

Our in-depth analysis of the carbon capture utilization and storage includes the following segments:

|

Segment |

Subsegments |

|

Service |

|

|

Technology |

|

|

End user Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Carbon Capture Utilization and Storage Market - Regional Analysis

North America Market Insights

The North America carbon capture utilization and storage market is anticipated to dominate with a leading share of 38.8% by the conclusion of 2035. The region’s dominance is driven largely by well-established carbon policy mechanisms, the availability of suitable geological storage sites, and a well-developed oil and gas infrastructure that enables large-scale deployment. Based on the government data which was published in November 2024, the U.S. Department of Energy plays a central role in CCS and carbon dioxide removal technologies through federally funded R&D. CCS is highly focused on capturing emissions from point sources such as power plants and storing them underground, whereas CDR aims to remove CO₂ directly from the atmosphere using methods such as direct air capture, forestry, and agricultural practices. Congress expanded DOE’s mandate through the Energy Act by authorizing substantial funding for CCUS demonstration projects, carbon utilization research, and new CDR programs, thus making it suitable for standard market growth.

U.S. Department of Energy CCUS & Carbon Removal Funding, 2022-2024

|

Program Area |

FY2022 Enacted (Regular) |

FY2022 (Supplemental) |

FY2023 Enacted (Regular) |

FY2023 (Supplemental) |

FY2024 Enacted (Regular) |

FY2024 (Supplemental) |

|

Carbon Capture |

99.0 |

1,344.0 |

135.0 |

720.0 |

127.5 |

720.0 |

|

Carbon Utilization |

29.0 |

41.0 |

50.0 |

65.3 |

52.5 |

66.6 |

|

Carbon Storage |

97.0 |

500.0 |

110.0 |

500.0 |

93.0 |

500.0 |

|

CIFIA |

- |

3.0 |

- |

2,097.0 |

- |

- |

|

CCS Subtotal |

225.0 |

1,888.0 |

295.0 |

3,382.3 |

273.0 |

1,286.6 |

|

Carbon Dioxide Removal (FECM) |

49.0 |

815.0 |

70.0 |

700.0 |

70.0 |

700.0 |

|

Carbon Dioxide Removal (other offices) |

55.0 |

- |

70.0 |

- |

48.0 |

- |

|

CDR Subtotal |

104.0 |

815.0 |

140.0 |

700.0 |

118.0 |

700.0 |

|

Total |

329.0 |

2,703.0 |

435.0 |

4,082.3 |

391.0 |

1,986.6 |

Source: Congress.gov

The federal policies are supporting the growth of the U.S. carbon capture utilization and storage market. The country’s market also benefits from enhanced performance-based tax incentives, major federal infrastructure grants, and streamlined regulatory pathways that heavily de-risk private capital investments. The Carbon Capture Demonstration Projects Program, which was funded by the Bipartisan Infrastructure Law, provided a total of USD 1.7 billion to advance integrated carbon capture, transport, and storage technologies. In December 2023, DOE announced a total of USD 890 million for three projects in California, North Dakota, and Texas, designed to prevent about 7.75 million metric tons of CO₂ annually, equivalent to emissions from 1.7 million gasoline cars. These projects will demonstrate novel solvents at a commercial scale while integrating carbon transport and storage in diverse geological settings.

In Canada, the carbon capture utilization and storage market is gaining momentum owing to the stringent national carbon pricing framework and federal and provincial investment tax credits that incentivize large-scale industrial decarbonization. The country has positioned itself as an international hub for clean energy innovation, thereby accelerating the commercialization of homegrown technologies in direct air capture, low-carbon blue hydrogen, and carbon-negative concrete production. Based on the government data published in April 2026, the CCUS Investment Tax Credit (ITC) is a refundable credit that is available for qualified CCUS project expenditures incurred between January 1, 2022, and December 31, 2040. Besides, it is administered jointly by the Canada Revenue Agency and Natural Resources Canada, and the program supports companies in claiming credits through corporate tax returns, while ensuring compliance and audits.

APAC Market Insights

The Asia Pacific carbon capture utilization and storage market is expected to grow at a considerable rate during the discussed timeframe. The region’s growth is largely driven by an imperative to balance economic growth with national net-zero decarbonization mandates. The region’s market momentum is focused on retrofitting coal-fired power utilities, steel mills, and chemical plants to prevent asset stranding. International Environmental NGO in February 2024 reported that Japan’s CCS policy aims to support long-term carbon neutrality by enabling large-scale storage of CO₂ in sectors where emissions are difficult to eliminate. In addition, the country’s government has set a target of 120 to 240 million tons of CO₂ storage annually by the end of 2050, which represents around 10% to 20% of total emissions, and it plans to commercialize CCS by around 2030 with assistance from regulatory reforms, cost reduction strategies, and infrastructure development.

Japan CCS Policy 2023 - 2050: Targets, Costs, Funding Programs, and Key Carbon Storage Projects Overview

|

Category |

Value |

|

CO₂ Storage Target (2050) |

120 to 240 million tons/year |

|

National Emissions (2021) |

1.122 billion tons CO₂e |

|

CCS Cost Range |

USD 85 to USD 135/ton CO₂ |

|

Cost Reduction Target |

60% reduction by 2050 |

|

Commercialization Target |

2030 |

|

Tomakomai Demonstration |

300,000 tons CO₂ |

|

Nagaoka Pilot Project |

10,000 tons CO₂ |

|

GX Investment Plan |

USD 26 billion (10 years) |

|

GX Transition Bonds |

USD 130 billion |

Source: IEN

The state-directed industrial policies and targeted funding from national development banks are certain visible trends reshaping the growth dynamics of China carbon capture utilization and storage market. The country has a strong emphasis on utilization pathways, where captured carbon is widely deployed for enhanced oil and gas recovery in major mature oilfields or converted into industrial chemicals and building materials. Based on the government data published in June 2026, China has announced a three-year action plan that started in 2026 to cut energy use and carbon emissions in nine high-emission industries, including steel, cement, oil refining, and coal-fired power generation. The plan is to be led by the National Development and Reform Commission, and it sets clear targets through 2028 to improve efficiency and accelerate green transformation, thus elevating the growth potential of the CCUS industry in China.

India carbon capture utilization and storage market has a huge opportunity to grow in the next decade as it is structurally supported by government-led policy roadmaps and state-backed research grants. The country possesses localized resource dynamics, due to which it heavily prioritizes carbon utilization pathways, actively developing commercial applications that convert captured carbon dioxide into synthetic fuels, green chemicals, and mineralized building materials. In August 2024, the International Trade Administration stated that India is advancing a large-scale decarbonization and CCUS policy led by NITI Aayog, with an aim for 750 million metric tons of CCUS capacity annually by 2050. This plan emphasizes industry clusters, financial incentives, and collaboration across steel, cement, oil and gas, petrochemicals, and fertilizers in order to meet emission reduction goals. There are opportunities for U.S. companies in CO2 utilization technologies such as building materials, chemicals, polymers, and enhanced oil recovery, supported by India’s membership in the Asia CCUS Network.

Europe Market Insights

Europe market has acquired a prominent position in the global landscape owing to the increasing deployment of large-scale industrial decarbonization projects, cross-border CO₂ transport networks, and the development of shared storage hubs. The coordinated funding mechanisms and public–private partnerships are accelerating project development across power generation, heavy industry, and hydrogen production. In April 2024, the article published by IEA disclosed that the European Commission has allocated more than USD 500 million under its Connecting Europe Facility program to support CO2 transport and storage projects across member states. This funding complements the proposed Net Zero Industry Act, which was released in March 2023, and it sets a target of injecting 50 million tons of CO2 annually by 2030.

In Germany, the carbon capture utilization and storage market is structured around the development of integrated hydrogen and CO₂ transport networks, designed to connect inland manufacturing hubs with cross-border maritime export terminals and offshore storage sites. At the same time, collaboration between industrial players, technology providers, and research institutions is strengthening pilot projects and early commercial deployments. In May 2024, Germany’s federal cabinet declared the clearance of the path for CCS and CCU with the adoption of key principles for a Carbon Management Strategy and draft revisions to the Carbon Storage Act. The policy permits offshore CO2 storage, by excluding marine protected areas while allowing Länder to opt in for onshore storage. The focus is on hard-to-abate industrial emissions, with public funding directed toward CCS/CCU projects in sectors where alternatives are limited, thus elevating the market’s growth potential.

The government-led industrial cluster strategies that integrate capture, transport, and offshore storage infrastructure are transforming the growth dynamics of the UK carbon capture utilization and storage market. Meanwhile, the country is also encouraging private sector participation through long-term project frameworks that support power generation decarbonization, low-carbon hydrogen production, and industrial emissions reduction. Based on the government data published in April 2025, it generously invested USD 27.3 billion over 25 years to support its first CCUS clusters, including HyNet and the East Coast Cluster, marking the country’s largest investment in carbon capture infrastructure. The CCUS is projected to generate USD 5 billion to USD 6.3 billion GVA annually, and the country is positioning itself as a global leader in carbon capture technologies.

Key Carbon Capture Utilization and Storage Market Players:

- Shell plc (UK)

- Exxon Mobil Corporation (U.S.)

- Equinor ASA (Norway)

- TotalEnergies SE (France)

- Fluor Corporation (U.S.)

- Linde plc (UK)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- JGC Holdings Corporation (Japan)

- SLB (U.S.)

- Aker Solutions ASA (Norway)

- Global Cement and Concrete Association (UK)

- Global CCS Institute (Australia)

- CarbonFree (U.S.)

- Univar Solutions (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Shell plc is considered to be one of the most prominent participants in the global market, leveraging its extensive expertise in energy infrastructure and subsurface storage. The company operates and makes investments in several projects, which also include industrial decarbonization hubs across Europe and North America.

- Exxon Mobil Corporation is a leading developer of large-scale carbon capture projects and has established a remarkable presence in the CCUS value chain. In addition, the firm benefits from expertise in geological formations, reservoir management, and pipeline infrastructure to provide carbon storage solutions for industrial customers.

- Linde plc is a central player in this field that benefits from its advanced gas processing, carbon capture, and engineering capabilities. The company develops proprietary capture technologies that are extensively used in industrial facilities, hydrogen production plants, and petrochemical operations.

- Mitsubishi Heavy Industries, Ltd. is recognized globally for its proprietary post-combustion carbon capture technologies and extensive project experience. The firm has deliberately deployed carbon capture systems across power generation, cement, steel, and chemical industries.

- Aker Carbon Capture ASA specializes exclusively in carbon capture solutions and has emerged as one of the leading pure-play CCUS technology companies across the globe. The company provides modular capture systems, which are especially designed for hard-to-abate industries such as cement, waste-to-energy, and refining.

Here is a list of key players operating in the global market:

The global carbon capture utilization and storage market represents a consolidated landscape with the presence of large energy companies, industrial gas suppliers, and carbon capture technology providers who are intensely competing to expand their market positions. Leading pioneers such as Shell, ExxonMobil, Equinor, TotalEnergies, and Linde are making heavy investments in terms of large-scale carbon capture hubs, CO₂ transportation infrastructure, and permanent geological storage projects. Apart from this, companies are opting for joint ventures, cross-border storage partnerships, acquisitions, and long-term carbon management agreements to secure strong market positions. In February 2026, ExxonMobil announced the launch of its second commercial carbon capture and storage project in Louisiana, to transport and store CO₂ from the new generation gas gathering facility in Gillis. It has the capacity to remove up to 1.2 million metric tons annually and thus contributes to the market’s expansion.

Corporate Landscape of the Market:

Recent Developments

- In June 2026, the Global Cement and Concrete Association and the Global CCS Institute signed a two-year partnership to accelerate carbon capture and storage adoption in the cement industry, aiming to advance industrial decarbonization through shared expertise, outreach, and stakeholder engagement.

- In October 2025, CarbonFree and Univar Solutions signed a letter of intent with a main goal to expand the supply of endurocal®, which is the world’s first carbon-neutral, mine-free calcium carbonate, to North America markets.

- Report ID: 8622

- Published Date: Jun 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.