Building-integrated Photovoltaic Market Outlook:

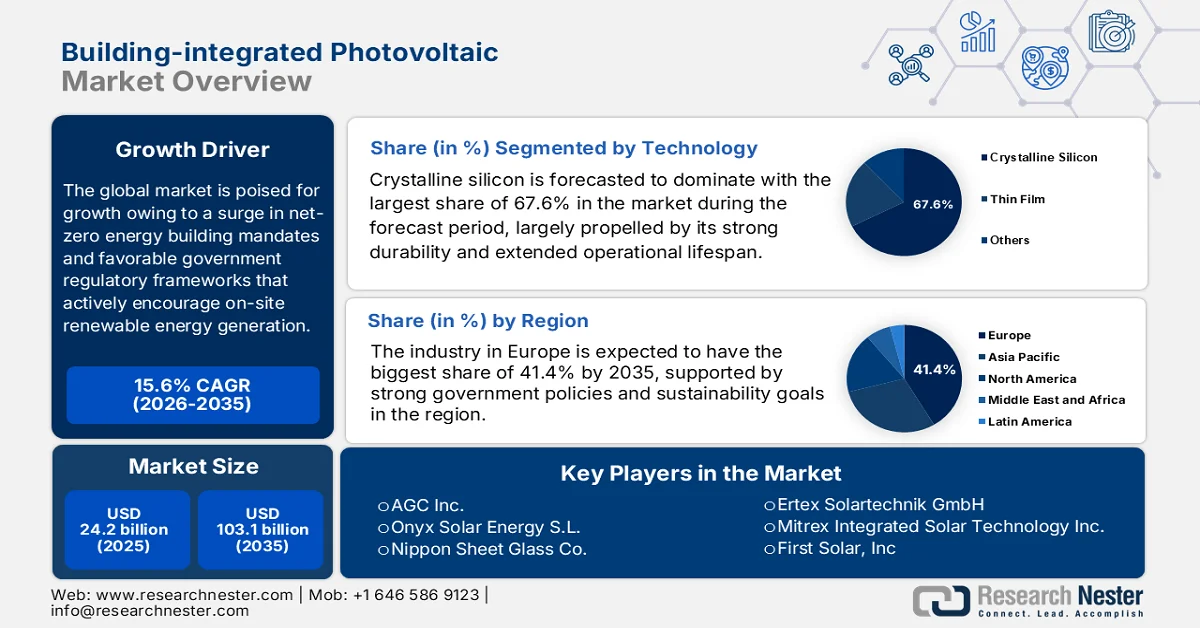

Building-integrated Photovoltaic Market size was over USD 24.2 billion in 2025 and is expected to reach USD 103.1 billion by the end of 2035, growing at around 15.6% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of building-integrated photovoltaic is estimated at USD 27.9 billion.

The global building-integrated photovoltaic market is projected for solid growth in the next decade, primarily propelled by a global surge in net-zero energy building mandates and favorable government regulatory frameworks that actively encourage on-site renewable energy generation. In this context, the study by Cornell University in December 2024 introduced a holistic methodology for estimating global BIPV potential by combining 3D building footprint models with spatio-temporal meteorological datasets to capture dynamic shadow effects. It analyzed 120 cities worldwide, whereas the results show that facade PV potential averages 68.2% of rooftop PV capacity, with 17.5% of cities demonstrating even higher facade potential. Hence, such findings underscore the importance of integrating facade PV into sustainable urban energy systems to maximize clean power generation, elevating the market’s growth potential.

Furthermore, the aesthetic advancements, i.e., the creation of colored, textured, and transparent solar glass, allow architects to blend energy generation into building envelopes, roofs, and windows without compromising design integrity. As corporate sustainability commitments intensify and the construction sector prioritizes decarbonization, the long-term outlook for the building-integrated photovoltaic market will be robust, owing to the expanding adoption of smart-city infrastructure and the rapid evolution of next-generation thin-film solar technologies. For instance, in August 2023, Panasonic Holdings Corporation announced the launch of the world’s first-ever long-term demonstration project for building-integrated perovskite photovoltaic glass at the Fujisawa Sustainable Smart Town in Japan. It was installed on the balcony of a model house to test the transparent and gradational designs for durability and efficiency, thus indicating a positive market outlook.

Key Building-integrated Photovoltaic Market Insights Summary:

Regional Highlights:

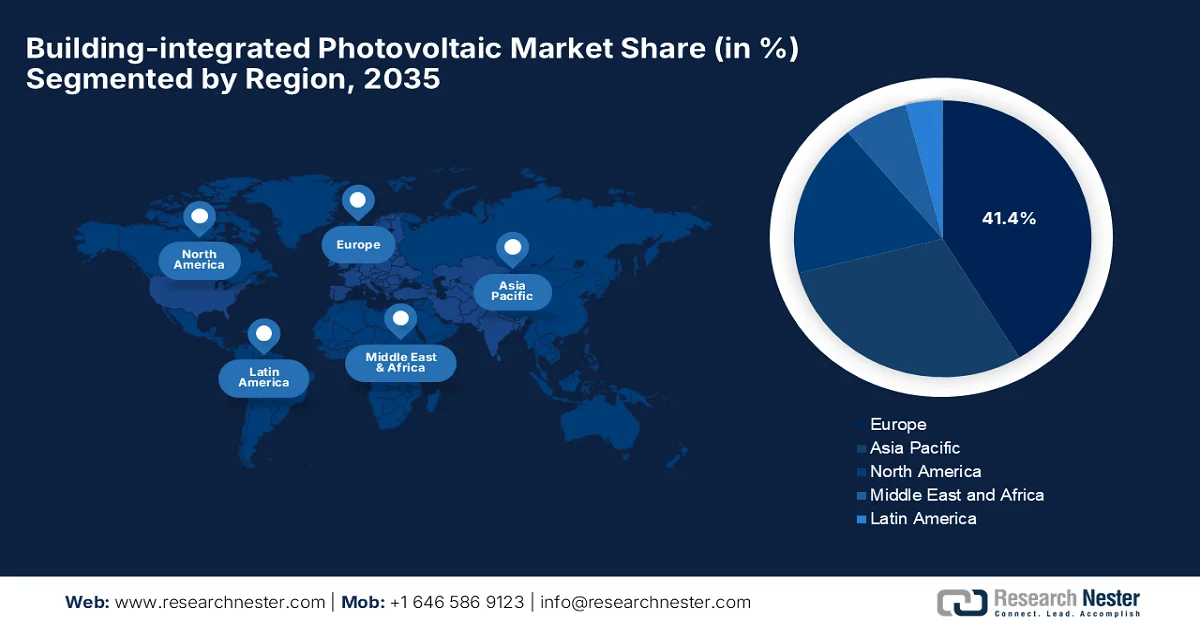

- Europe is projected to capture 41.4% of the building-integrated photovoltaic market by 2035, reinforced by strong policy frameworks, sustainability targets, and stringent energy efficiency regulations

- Asia Pacific is expected to witness considerable growth in the market during 2026-2035, stimulated by unprecedented urbanization rates and high population density across megacities

Segment Insights:

- The crystalline silicon segment is forecasted to account for 67.6% of the building-integrated photovoltaic market by 2035, underpinned by its high efficiency, strong durability, and extended operational lifespan

- Roof-integrated photovoltaics is anticipated to secure a considerable revenue share in the market by 2035, fueled by superior solar exposure and the ability to generate maximum energy without compromising building design

Key Growth Trends:

- Urbanization and space constraints

- Rising energy costs and energy security concerns

Major Challenges:

- Financial and economic barriers

- Supply chain and manufacturing limitations

Key Players: AGC Inc. (Japan),Onyx Solar Energy S. L. (Spain),Nippon Sheet Glass Co., Ltd. (Pilkington) (Japan),Ertex Solartechnik GmbH (Austria),Mitrex Integrated Solar Technology Inc. (Canada),First Solar, Inc. (U.S.),Hanwha Q CELLS Co., Ltd. (South Korea),Trina Solar Co., Ltd. (China),LONGi Green Energy Technology Co., Ltd. (China),JinkoSolar Holding Co., Ltd. (China),Vikram Solar (India) ,NEXT Energy Technologies (U.S.),WAAREE Energies Limited (India).

Global Building-integrated Photovoltaic Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 24.2 billion

- 2026 Market Size: USD 27.9 billion

- Projected Market Size: USD 103.1 billion by 2035

- Growth Forecasts: 15.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Europe (41.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: Germany, China, United States, Japan, France

- Emerging Countries: India, South Korea, Netherlands, Singapore, United Arab Emirates

Last updated on : 23 June, 2026

Building-integrated Photovoltaic Market - Growth Drivers and Challenges

Growth Drivers

- Urbanization and space constraints: The building-integrated photovoltaic market is being heavily catalyzed by urban sprawl, along with limited available land in metropolitan regions. These BIPV systems can replace conventional building materials, which enable energy generation without additional space requirements. As of the March 2025 data from the Our World in Data article, more than 4 billion people live in urban areas. It also mentions that the global urban share recorded almost 50% owing to migration and natural urban population growth. The data further underscores big regional differences wherein high-income countries have urbanization rates above 80%, whereas lower-income regions still have a majority rural population, thus elevating the growth potential of the market.

- Rising energy costs and energy security concerns: The rising electricity costs, along with rising concerns over energy security, are readily accelerating demand in the building-integrated photovoltaic market globally. The on-site power generation reduces dependence on grid electricity and addresses operational costs, due to which businesses and homeowners opt for BIPV solutions. As per an article published by the International Energy Agency, global electricity demand rose around 2.2% in 2023, effectively driven by electrification, industrial activity, and expanding digital infrastructure. Countries such as India and Southeast Asia are experiencing rapid annual growth above 5% to 6%. Therefore, this accelerating demand is expected to intensify pressure on grid systems and strengthen the economic rationale for on-site renewable solutions such as building-integrated photovoltaics.

Global Electricity Demand Growth & Regional Trends 2023-2026 Forecast Data & Key Statistics

|

Indicator |

Value |

Year/Period |

|

Global electricity demand growth |

2.2% |

2023 |

|

Projected annual growth |

3.4% |

2024-2026 |

|

China's electricity demand growth |

6.4% |

2023 |

|

India's electricity demand growth |

7% |

2023 |

|

Europe's electricity demand change |

-3.2% |

2023 |

|

Data center electricity use |

460 TWh → >1000 TWh |

2022-2026 |

|

Electricity share in final energy |

20% |

2023 |

Source: IEA

Challenges

- Financial and economic barriers: One of the major burdens hindering the expansion of building-integrated photovoltaic market is the extensive upfront cost which is associated with product manufacturing, customization, and installation. These BIPV solutions are incorporated directly into building components such as facades, roofs, skylights, and windows. Therefore, this requires specialized design and construction skills, which in turn raises the project complexity and overall expenditure, whereas the need for customized products suitable to specific architectural requirements further elevates costs. In addition, the developers operating in the market face longer project planning and approval timelines, which can deter investment, posing a major barrier to widespread adoption.

- Supply chain and manufacturing limitations: The building-integrated photovoltaic market faces severe challenges that are related to supply chain maturity and manufacturing scalability. In this context, producing building-integrated solar components necessitates specialized materials such as photovoltaic glass, thin-film modules, and custom laminates, which are not as readily available as the traditionally used solar panel components. This can lead to longer lead times and higher procurement costs. Furthermore, the aspect of limited standardization across products increases dependence on specialized suppliers, making the supply chain more vulnerable to disruptions, thus negatively impacting the market’s growth.

Building-integrated Photovoltaic Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

15.6% |

|

Base Year Market Size (2025) |

USD 24.2 billion |

|

Forecast Year Market Size (2035) |

USD 103.1 billion |

|

Regional Scope |

|

Building-integrated Photovoltaic Market Segmentation:

Technology Segment Analysis

On the basis of technology, crystalline silicon is forecasted to dominate with the largest share of 67.6% in the building-integrated photovoltaic market during the forecast period. The segment’s dominance is largely propelled by its high efficiency, strong durability, and extended operational lifespan. They are extensively used in applications such as solar façades, integrated rooftop systems, and photovoltaic glass. Crystalline silicon modules also benefit from a well-established global manufacturing infrastructure, which ensures a steady supply and cost competitiveness when compared to emerging alternatives. Continuous improvements in cell architecture, such as PERC and TOPCon technologies, have also enhanced their performance efficiency. In addition, strong industry standardization supports easier integration into conventional construction materials and design frameworks, thus denoting a wider segment scope.

Application Segment Analysis

In the application segment, roof-integrated photovoltaics is anticipated to grow with a considerable revenue share in the building-integrated photovoltaic market by the end of 2035. The segment’s growth is largely driven by its superior solar exposure and ability to generate maximum energy without compromising building design. Rooftops are extensively utilized in residential and commercial structures, supported by rising efficiency levels, government incentives, and increasing adoption of net-zero energy building standards. Based on the government data published in March 2024, NTPC Limited has laid the foundation stone for the 630-MW Barethi Solar Power Project in Madhya Pradesh, with a total investment of USD 385 million, with the main goal to power over 3 lakh households. It was developed under MNRE’s RE Park initiative, and the project will cut 12 lakh tons of CO₂ annually, supporting India’s climate goals and green energy targets.

End user Segment Analysis

By the conclusion of the forecast period, the commercial segment is expected to attain a notable share in the building-integrated photovoltaic market. The increasing focus on sustainability and energy efficiency among businesses and institutions is driving the sub-segment’s leadership. Commercial buildings such as office complexes, shopping centers, and public infrastructure are opting for building-integrated photovoltaic solutions, including solar facades, photovoltaic glass, and solar shading systems, to comply with green building standards like LEED and BREEAM. In October 2023, SP Group completed its first Building-integrated Photovoltaic project in China, which is a 4 MWp installation at Guangdong Lingxiao Pump Industry’s new plant in Yangchun City. It spans 17,000 m², and the system will generate 110 million kWh of clean power over 25 years, avoiding 1,600 tons of coal and nearly 4,500 tons of CO₂ annually, thus denoting a wider segment scope.

Our in-depth analysis of the building-integrated photovoltaic market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Application |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Building-integrated Photovoltaic Market - Regional Analysis

Europe Market Insights

Europe building-integrated photovoltaic market is anticipated to attain a commendable share of 41.4% during the stipulated timeframe. The region’s dominance is mainly propelled by strong policy frameworks, sustainability targets, and stringent energy efficiency regulations. In addition, countries such as Germany, France, and the Netherlands are actively encouraging BIPV adoption through financial incentives and regulatory mandates. In June 2026, FRV announced that it secured 2.3 GW of grid capacity in Germany, which is a major expansion of its battery energy storage, photovoltaic, and hybrid projects. It is spread across Brandenburg, Lower Saxony, and North Rhine-Westphalia. The portfolio includes large-scale storage systems up to 900 MW and hybrid solutions, thus making it suitable for standard market growth.

The nation’s aggressive energy transition and long-term climate neutrality goals are uplifting Germany, building-integrated photovoltaic market. This forward-looking momentum is structurally supported by the widespread deployment of state-level solar mandates, which turn active on-site generation into a compliance requirement for new constructions and major roof refurbishments across multiple federal states. In December 2024, Fraunhofer ISE and Fraunhofer UMSICHT together announced the development of a prefabricated BIPV façade element that integrates photovoltaics with thermal insulation, thereby enabling faster retrofits and reduced material use. Two prototypes using hemp fiber and mushroom-based insulation were installed in Holzkirchen in October 2024, which later underwent real-world monitoring for durability and energy yield.

In the UK, the building-integrated photovoltaic market is undergoing remarkable transformations due to the implementation of pioneering legislative frameworks. The country’s market is making a shift from standard, retrofitted solar fixtures toward highly functional aesthetic components such as solar slats, integrated roof tiles, and photovoltaic glass curtain walls. This shift is further accelerated by an influx of institutional ESG-led capital for large-scale commercial real estate. Based on the government data published in May 2023, its Solar Taskforce has set a target of 70 GW solar capacity by 2035, whereas the Taskforce aims to cut installation costs, boost British skills and jobs, and improve grid access to accelerate deployment. By the time it was already powering nearly 4 million homes, whereas solar is the UK’s most popular energy source, and scaling rooftop and utility projects will be crucial to meeting net-zero commitments, while denoting a lucrative opportunity for BIPVs.

APAC Market Insights

The Asia Pacific building-integrated photovoltaic market is anticipated to grow at a considerable rate from 2026 to 2035. The region’s upliftment is fundamentally propelled by unprecedented rates of urbanization and population density across megacities. The region benefits immensely from its status as the world’s manufacturing powerhouse for solar components, allowing domestic developers to capitalize on immediate supply chain access and innovations in lightweight thin-film and perovskite tandem cell technologies. In March 2023, Kaneka Corporation and Taisei Corporation, in collaboration with the Tokyo Bureau of Environment, announced the launch of the renewable energy visualization model project by using T-Green Multi Solar BIPV systems at Tokyo Big Sight and the Water & Green Museum. This initiative will run until March 2027, and it aims to showcase building-integrated photovoltaic technology by making renewable energy visible in Tokyo-owned facilities.

The green building action plans and overarching carbon neutrality objectives are uplifting China building-integrated photovoltaic market. Adoption is fundamentally accelerated by China’s global dominance in terms of solar supply chains and manufacturing. In addition, enhanced by deep integration with smart-grid urban infrastructure, the country solidifies its status as both the largest manufacturer and the fastest-growing consumer of decentralized architectural solar systems globally. In January 2025, the article published by IEA-PVPS in 2023, China installed a record 216.3 GW of new PV capacity in 2023, which is a 147.5% year-on-year increase, bringing cumulative capacity to 609 GW and meeting 6% of national electricity demand. Centralized PV grew 230.7% to 120 GW, surpassing distributed PV at 96.29 GW, driven by utility-scale and residential projects. The PV industry contributed USD 96 billion to the economy, indicating a positive outlook for the country’s market.

The India building-integrated photovoltaic market is poised for exponential expansion in the upcoming years, energized by the proactive implementation of the energy conservation building code and the extensive Smart Cities Mission. This encourages real estate developers to move past passive building materials, thereby favouring energy-generating infrastructures. As Tier-1 cities face soaring urban density and high-rise commercial verticality, BIPV facades, solar glass windows, and integrated roofing systems are being chosen to optimize space and alleviate heavy grid reliance. For instance, in April 2026, Intertek announced the acquisition of Mitsui Chemicals India’s solar PV laboratory assets in Ahmedabad to strengthen its leadership in renewable energy assurance. The ISO 17025 accredited lab will provide BIS and IECEE CB Scheme certifications, supporting domestic manufacturers and global firms with faster, harmonized market access.

India Solar PV Cells and Modules Shipment Imports by Country 2022-2023: Trade Flow Analysis

|

Country |

2022-23 Solar PV Cells (USD Million) |

2022-23 Solar PV Modules (USD Million) |

|

Anguilla |

- |

- |

|

Australia |

0.22 |

- |

|

Cambodia |

52.72 |

- |

|

Canada |

0.01 |

- |

|

Chad |

- |

- |

|

Chile |

- |

- |

|

Taiwan |

1.92 |

0.13 |

|

China |

581.45 |

874.89 |

|

France |

- |

- |

|

Germany |

0.05 |

0.13 |

|

Hong Kong |

1.17 |

3.04 |

Source: PIB

North America Market Insights

The North America building-integrated photovoltaic market has acquired a central position in the global landscape, propelled by progressive clean energy policies and a corporate-driven push for commercial real estate decarbonization. In addition, the market is structurally supported by major federal initiatives that provide long-term investment tax credits that incentivize the adoption of energy-generating building materials when compared to standard construction alternatives. In July 2024, at Greenbuild 2024, the U.S. DOE Solar Energy Technologies Office presented its building-integrated photovoltaics strategy, underscoring the prominence of solar integrated into roofs, façades, curtain walls, and other building elements. It notes that BIPV systems offer dual functionality, which serves as part of the building envelope, thereby generating clean electricity, improving aesthetics, resilience, and reducing grid reliance.

The U.S. building-integrated photovoltaic market is strongly progressing at a rapid pace of progress as architects, developers, and utilities embed solar technologies directly into building envelopes. At the same time, the country’s market also benefits from collaboration between technology providers, construction firms, and real estate developers, which is accelerating pilot deployments in commercial offices, institutional campuses, and high-performance urban buildings. PBS Organization in June 2026 revealed that the U.S. solar power reached a historic milestone, supplying 12.8% of national electricity, surpassing coal’s 12.2% share for the first time. It also mentioned that solar has become the third-largest electricity source behind natural gas and nuclear, reflecting a lucrative opportunity for building-integrated photovoltaic players.

The nation’s aggressive net-zero emissions targets and the continuous winterization of sustainable building technologies are responsibly boosting the overall building-integrated photovoltaic market in Canada. The country’s market growth is extensively supported by strict municipal green building standards in major urban hubs such as Toronto and Vancouver, along with corporate ESG mandates aiming to reduce the carbon footprint of commercial high-rises. Based on the government data published in July 2024, it launched its first Canada green buildings strategy to accelerate energy-efficient and low-carbon building development with a prime focus on retrofitting existing buildings, constructing climate-resilient new buildings, and advancing clean building technologies. The strategy supports net-zero objectives through initiatives that require new federal buildings to achieve net-zero emissions standards. These measures are creating a favorable business environment for building-integrated energy technologies, which include BIPV systems, particularly in commercial and institutional buildings.

Key Building-integrated Photovoltaic Market Players:

- AGC Inc. (Japan)

- Onyx Solar Energy S. L. (Spain)

- Nippon Sheet Glass Co., Ltd. (Pilkington) (Japan)

- Ertex Solartechnik GmbH (Austria)

- Mitrex Integrated Solar Technology Inc. (Canada)

- First Solar, Inc. (U.S.)

- Hanwha Q CELLS Co., Ltd. (South Korea)

- Trina Solar Co., Ltd. (China)

- LONGi Green Energy Technology Co., Ltd. (China)

- JinkoSolar Holding Co., Ltd. (China)

- Vikram Solar (India)

- NEXT Energy Technologies (U.S.)

- WAAREE Energies Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- AGC Inc. is one of the most dominating and influential players in the market, which benefits from its extensive knowledge in architectural glass and advanced materials. The company is highly focused on integrating photovoltaic functionality into high-performance glass products used in commercial buildings, facades, and skylights.

- Onyx Solar Energy S.L. has registered itself as a specialist in photovoltaic glass solutions as a global leader in customized BIPV applications. Besides, the firm develops transparent and semi-transparent solar glass products that can be integrated into facades, curtain walls, canopies, and skylights.

- Nippon Sheet Glass Co., Ltd. has emerged as a foundational player in this building-integrated photovoltaic market propelled by its photovoltaic and solar-control glass products. The company benefits from its strong brand recognition in architectural glass, along with an extensive distribution network.

- Mitrex Integrated Solar Technology Inc. has gained immense visibility in the BIPV sector through its innovative solar facade and building envelope technologies. In addition, the firm specializes in terms of integrating photovoltaic modules directly into exterior cladding systems, enabling buildings to generate clean energy while maintaining modern architectural designs.

- Heliatek GmbH is yet another dominant force in this sector, which is known for pioneering organic photovoltaic solutions suitable for building integration. The company’s competitive strategy is structured around continuous innovation in organic solar technology, intellectual property development, and partnerships with construction material manufacturers.

Here is a list of key players operating in the global building-integrated photovoltaic market:

The global building-integrated photovoltaic market is witnessing intense competition due to constant technological innovations, architectural integration capabilities, and tactical partnerships with construction and real estate stakeholders. The leading companies in this sector are focused on the development of high-efficiency photovoltaic glass, solar facades, and transparent modules to strengthen their market presence. Mergers, acquisitions, product launches, and collaborations with architects, developers, and government agencies have become the most prominent growth strategies opted for by the market participants. As stated by AGC in November 2023, it showcased SunEwat (SUNJOULE®) BIPV technology at the COP28 Japan Pavilion in Dubai, which is its first exhibition at the global climate conference. SunEwat enables electricity generation through building facades while enhancing architectural design, aligning with Japan’s carbon neutrality goals by 2050.

Corporate Landscape of the Building-integrated Photovoltaic Market:

Recent Developments

- In April 2026, Vikram Solar surpassed 10 GW in global solar module deployments, doubling its capacity in just two years and powering more than 5 million homes in India. This underscores its pivotal role in India’s clean energy journey and expanding global presence across 39 countries.

- In July 2025, NEXT Energy Technologies introduced the world’s first commercial BIPV facade, which was powered by transparent OPV coatings, installed at its Santa Barbara headquarters, and it consists of six energy-generating windows.

- Report ID: 3370

- Published Date: Jun 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.