Blood Banking Devices Market Outlook:

Blood Banking Devices Market size was valued at over USD 47.1 billion in 2025 and is projected to reach USD 101.4 billion by the end of 2035, with a CAGR of 8.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of blood banking devices is evaluated at USD 51.2 billion.

The global blood banking devices market is increasingly influenced by evolving healthcare reimbursement models, climate-based supply chain disruptions, and demographic transitions. Based on these factors, the aging population, introduction of volatility in blood supply logistics due to climate modifications, the shift towards value-driven reimbursement models, and technological advancements are fueling the market exposure. According to official statistics published by the America’s Blood Centers in June 2024, based on the U.S. Food and Drug Administration’s (FDA) Blood Establishment Registration database, there exist 53 community-based blood centers, along with 90 hospital-driven blood centers. Additionally, blood centers collect an estimated 60% of the blood supply, leading to a continuous supply of blood grouping reagents, which is proliferating the blood banking devices market growth.

Global Blood Grouping Reagent Export and Import Analysis, 2024

|

Countries/Components |

Export (USD) |

Import (USD) |

|

Switzerland |

153 million |

- |

|

Ireland |

152 million |

- |

|

Germany |

145 million |

102 million |

|

Saudi Arabia |

- |

229 million |

|

France |

- |

83.8 million |

|

Global Trade Valuation |

1.0 billion |

|

|

Global Trade Share |

Less than 0.005% |

|

|

Product Complexity |

1.1 |

|

|

Export Growth |

19.1% |

|

Source: OEC

Furthermore, the decentralized blood collection models, blockchain for blood traceability, and the gamification of donor retention are certain trends that are responsible for driving the blood banking devices market globally. As stated in an article published by the Journal of the Formosan Medical Association in August 2022, an increase in the unit of whole blood is expected from 1,182,973 to 1,115,803 as of 2018, to 1,230,500 and 1,250,760 by the end of 2030. Besides, the practice of blood collection readily depends on donors over the age of 40 years, while there has been a reduction in whole blood donations among people aged less than 25 years. Moreover, the appropriate age range for first-time blood donation is between 17 years and 64 years, while regular donors are permitted to donate blood until 69 years of age, thereby enhancing the blood banking devices market exposure globally.

Key Blood Banking Devices Market Insights Summary:

Regional Highlights:

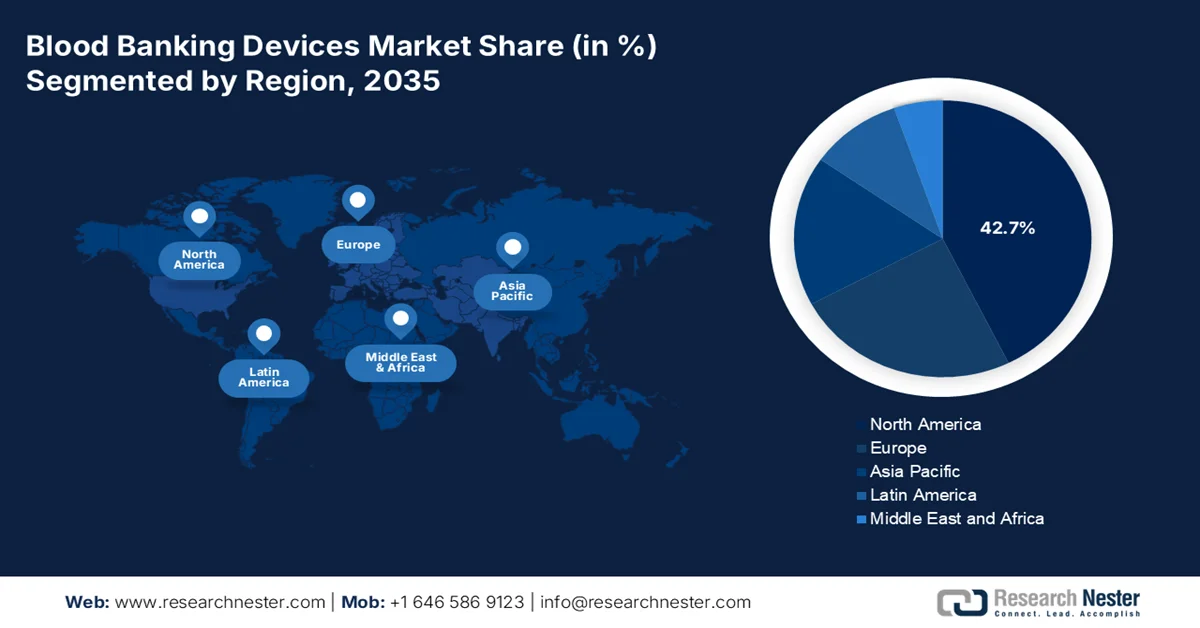

- North America in the blood banking devices market is projected to hold a 42.7% share by 2035, attributed to advanced healthcare infrastructure and rising chronic disease burden necessitating transfusions

- Asia Pacific is expected to witness the fastest growth over 2026-2035, propelled by expanding healthcare facilities and increasing adoption of automated blood collection and processing systems

Segment Insights:

- Manual Blood Collection sub-segment in the blood banking devices market is anticipated to account for a 70.7% share by 2035, driven by its critical role in ensuring accurate specimen collection for diagnosis

- Automated Devices sub-segment is likely to secure the second-largest share during the forecast period 2026-2035, fueled by enhanced efficiency, reduced human error, and improved operational safety

Key Growth Trends:

- Expansion in therapeutic apheresis indications

- Commercialization of blood substitute research

Major Challenges:

- Supply chain vulnerabilities for perishable consumables

- Workforce skill gaps and training deficits

Key Players: Terumo Corporation (Japan), Haemonetics Corporation (U.S.), Fresenius Kabi AG (Germany), Grifols, S.A. (Spain), Macopharma (France), Becton, Dickinson and Company (BD) (U.S.), Thermo Fisher Scientific, Inc. (U.S.), Beckman Coulter, Inc. (U.S.), Abbott Laboratories (U.S.), Bio-Rad Laboratories, Inc. (U.S.), Sysmex Corporation (Japan), Kawasumi Laboratories, Inc. (Japan), Siemens Healthineers (Germany), Roche Holdings AG (Switzerland).

Global Blood Banking Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 47.1 billion

- 2026 Market Size: USD 51.2 billion

- Projected Market Size: USD 101.4 billion by 2035

- Growth Forecasts: 8.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, Brazil, South Korea, Mexico, Indonesia

Last updated on : 23 April, 2026

Blood Banking Devices Market - Growth Drivers and Challenges

Growth Drivers

- Expansion in therapeutic apheresis indications: The clinical application for therapeutic apheresis, wherein patient blood is readily processed to diminish pathological components, is expanding the blood banking devices market globally. According to official statistics published by NLM in April 2025, over 90,000 haemopoietic stem cell transplantation significantly take place every year, and there has been a surge in the demand for guaranteeing mobilization, optimizing immune reconstitution, and optimizing tolerability to apheresis. Besides, peripheral blood stem cell collections usually take an average of 3 to 4 hours per day per donor, and frequently require consecutive durations to complete, thereby making it extremely suitable for bolstering the market growth.

- Commercialization of blood substitute research: The conduction of late-stage clinical trials for hemoglobin-driven oxygen carriers and perfluorocarbon emulsions is gradually progressing, which is enhancing the demand for the blood banking devices market across different regions. As stated in an article published by the Annals of Blood Organization in March 2026, red blood cells (RBCs) accounted for 25% to 30%, whereas the hydrochlorofluorocarbons method witnessed almost 60% growth rates. Besides, as of 2025, researcher-based investigators successfully generated an estimated 4.6×103 RBCs per induced pluripotent stem cells (iPSC). Moreover, there has been continuous progress regarding research on extending Hematopoietic stem cells (HSCs) through culture conditions and the utilization of small-scale molecule agonists, which is positively uplifting the market development.

- Increase in veterinary blood banking: There has been a significant establishment of the first-ever regional veterinary blood banks for companion animal medicine, particularly in Europe and North America, which is fueling the blood banking devices market demand. This resulted in an increased focus on canine and feline transfusion services that are categorized as specialty referral hospitals. These veterinary blood banks require scaled-down but functionally similar collection, processing, and storage devices calibrated for animal blood volumes and component characteristics. Besides, manufacturers are adapting existing human devices or developing veterinary-specific lines, often at lower price points but with comparable consumable attachment models. This driver originates from the pet healthcare economy, entirely separate from human demographic or regulatory forces.

Challenges

- Supply chain vulnerabilities for perishable consumables: The blood banking devices market heavily relies on a just-in-time supply chain for sterile, single-use consumables such as collection bags, leukoreduction filters, and apheresis kits. These components have finite shelf lives and require climate-controlled logistics, making stockpiling economically unfeasible. Besides, any disruption, such as a raw material shortage, port congestion, or factory contamination incident, can cascade rapidly into regional blood collection shortfalls. Unlike pharmaceutical supply chains that often have redundant manufacturing sites, many blood device consumables are produced in specialized, geographically concentrated facilities.

- Workforce skill gaps and training deficits: The increasing sophistication of automated blood banking devices has outpaced the technical competency of the existing laboratory workforce. Phlebotomists and blood bank technicians trained in manual venipuncture and basic centrifugation now face interfaces requiring digital literacy, troubleshooting of electromechanical systems, and interpretation of software-generated alerts. Comprehensive training programs are expensive and time-consuming, often requiring staff to leave their posts for multi-day certification courses. High staff turnover in healthcare settings means that training investments are frequently lost before achieving a return on investment. Moreover, the shortage of biomedical engineers specializing in blood bank equipment leaves many facilities unable to perform even basic preventive maintenance, forcing expensive vendor service calls for minor issues, which is negatively impacting the blood banking devices market globally.

Blood Banking Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.9% |

|

Base Year Market Size (2025) |

USD 47.1 billion |

|

Forecast Year Market Size (2035) |

USD 101.4 billion |

|

Regional Scope |

|

Blood Banking Devices Market Segmentation:

Method Segment Analysis

Based on the method segment, the manual blood collection sub-segment is anticipated to garner the highest share of 70.7% in the blood banking devices market by the end of 2035. The sub-segment’s upliftment is highly fueled by its importance as a foundational and critical procedure in clinical practice that ensures the accurate monitoring and diagnosis of disorders by enabling the correctly gathered specimen. According to official statistics published by the World Health Organization (WHO) in May 2025, 40% of the 118.5 million blood donations globally are collected across high-income nations, which are home to 16% of the population. Besides, across low-income countries, almost 54% of blood transfusions are offered to children aged under 5 years. Moreover, there is the incidence of transfusion-transmissible infections through manual blood donations, which demand awareness programs globally.

Transfusion-Based Transmissible Infections Through Blood Donations by Median and Interquartile Range, 2024

|

Country Type |

HIV |

HBV |

HCV |

Syphilis |

|

High-Income Countries |

0.002% |

0.02% |

0.007% |

0.02% |

|

Less than 0.001% to 0.01% |

0.005% to 0.1% |

0.002% to 0.06% |

0.003% to 0.1% |

|

|

Upper Middle-Income Countries |

0.1% |

0.2% |

0.1% |

0.3% |

|

0.03% to 0.2% |

0.1% to 0.6% |

0.07% to 0.3% |

0.1% to 1.1% |

|

|

Lower Middle-Income Countries |

0.1% |

1.7% |

0.3% |

0.6% |

|

0.04% to 0.6% |

0.7% to 4.7% |

0.1% to 0.9% |

0.1% to 1.3% |

|

|

Low-Income Countries |

0.7% |

2.8% |

1.0% |

0.9% |

|

0.2% to 1.6% |

2.0% to 6.0% |

0.5% to 1.6% |

0.6% to 1.8% |

Source: WHO

Technology Segment Analysis

During the forecast period, the automated devices sub-segment, part of the technology segment, is projected to grab the second-highest share in the blood banking devices market. The sub-segment’s growth is primarily driven by the aspects of an increase in production speed, a decrease in human errors, and enhanced safety in residential and industrial settings. As stated in an article published by NLM in May 2022, the automated blood pressure measuring devices (BPMDs) industry was worth USD 1.5 billion as of 2022, which is expected to reach USD 3.2 billion by the end of 2028. Based on this future growth, many organizations readily manufacture more than 3,500 various models of automated BPMDs, the majority of which exist without evidence of having undergone approved validation evaluation. Therefore, with such developments, there is a huge growth opportunity for the sub-segment globally.

Application Segment Analysis

By the end of the stipulated timeline, the diagnostics sub-segment, which is part of the application segment, is expected to account for the third-highest share in the blood banking devices market. The sub-segment’s development is highly propelled by its importance in managing, diagnosing, and preventing disorders by identifying health risks early, guiding suitable treatment options, and monitoring organ function. As per an article published by NLM in September 2025, this particular method is utilized to detect anemia, which readily accounts for 24.8% of the prevalence among the overall global population. This prevalence is extremely higher than 1.6 billion people witnessing distress from anemia, which is driving the segment’s demand. Therefore, through diagnosis, it has been demonstrated that anemia presently impacts 40% of preschool children and 30% of the female population, and also results in 52 million years of disability.

Our in-depth analysis of the blood banking devices market includes the following segments:

|

Segment |

Subsegments |

|

Method |

|

|

Technology |

|

|

Application |

|

|

Product Type |

|

|

End user |

|

|

Technique |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Blood Banking Devices Market - Regional Analysis

North America Market Insights

North America in the blood banking devices market is anticipated to garner the highest share of 42.7% by the end of 2035. The market’s upliftment in the region is primarily driven by the presence of the innovative healthcare facility, increased prevalence of chronic disorders demanding transfusions, robust regulatory frameworks, a rise in surgical volumes, and the adoption of automated processing and collection systems across hospitals and blood banks. According to official statistics published by NLM in February 2024, approximately 129 million people, especially in the U.S., are impacted by almost 1 major chronic disease, such as hypertension, obesity, diabetes, cancer, and heart disease. In addition, 5 of the top 10 notable death causes in the country are strongly related to treatable and preventable chronic diseases, which are responsible for boosting the blood banking devices market growth in the region.

Chronic and Multiple Chronic Condition Analysis in the U.S., 2023

|

Components |

Prevalence |

|

Chronic Conditions |

|

|

Number of Adults |

76.4%, 194 million |

|

Chronic Condition |

More than 1 |

|

Young Adult Impact |

59.5% |

|

Midlife Adult Impact |

78.4% |

|

Old Adult Impact |

93.0% |

|

Overall Prevalence (2013-2023) |

52.5% to 59.5% |

|

Multiple Chronic Conditions |

|

|

Number of Adults |

51.4%, 130 million |

|

Young Adult Impact |

27.1% |

|

Midlife Adult Impact |

52.7% |

|

Old Adult Impact |

78.8% |

|

Overall Prevalence (2013-2023) |

21.8% to 27.1% |

Source: CDC Government

The blood banking devices market in the U.S. is growing significantly, owing to generous federal budget allocation, Medicaid support, Medicare funding, and industrial associations. As stated in a data report published by the America’s Blood Centers Organization in February 2026, an estimated 3% of donors are old enough to effectively donate blood in the domestic donation program every year. In addition, the country comprises roughly 6.5 million donors as of 2023, depicting a slight fall by 0.1% than an estimated 6.54 million donors. Simultaneously, there are roughly 11,586,000 overall whole blood and apheresis red blood cell units collected, demonstrating a 1.7% decrease from previous years. Besides, there has been a suitable prevalence of different blood types that are distributed to the domestic population, which is also positively impacting the blood banking devices market expansion.

Blood Type Prevalence Among the U.S. Population, 2026

|

Blood Type |

Prevalence |

Common Factor |

|

O Rh-positive |

40% |

1 in 2.5 |

|

O Rh-positive |

7% |

1 in 14 |

|

A Rh-positive |

32% |

1 in 3.1 |

|

A Rh-negative |

6% |

1 in 17 |

|

B Rh-positive |

11% |

1 in 11 |

|

B Rh-negative |

2% |

1 in 50 |

|

AB Rh-positive |

4% |

1 in 25 |

|

AB Rh-negative |

1% |

1 in 100 |

Source: America’s Blood Centers Organization

The provincial healthcare coordination, centralized medical operations, an escalation in adopting safety-engineered blood collection systems, automated component processing equipment, and an increase in prioritizing pathogen reduction technologies are certain factors that are bolstering the blood banking devices market in Canada. As per an article published by NLM in April 2022, more than 18,600 donations have been evaluated by Héma-Québec based on collaboration with the Ministère de la Santé et des Services sociaux du Québec and the Government of Canada. Besides, blood donors in the country need to be aged 17 years or 18 years in Quebec for donating blood, and there are few donors over the age of 72 years. Besides, from yearly 1.2 million donations, an additional ethylenediaminetetraacetic acid blood tube is readily collected, which is extremely suitable for fueling the blood banking devices market growth.

APAC Market Insights

The Asia Pacific in the blood banking devices market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the existence of large-scale healthcare facilities, an increase in disease burden, government-based blood safety strategies, along with the transition from manual to automated blood collection and processing systems. According to official statistics published by the Asia Development Bank Organization in June 2025, over 20 nations in the region have a 20% higher risk of people being prematurely affected by rare diseases. This comprises the Philippines, Indonesia, and India, along with other Pacific-based regions, exceeding by 40%. Likewise, based on a screening program in Mongolia, rare diseases affected almost 40% of the population by the end of 2023, thus enhancing the market demand in the overall region.

The blood banking devices market in China is gaining increased traction, owing to suitable approvals for processing equipment and automated blood collection, generous government expenditure on blood banking, and a surge in transfusion support for surgical procedures and hematological diseases. As stated in an article published by the State Council in June 2025, the country has bolstered public awareness of voluntary blood donation by creating a partnership between the National Health Commission (NHC) and China Railway Group for displaying promotional posters and videos on 260,000 screens across over 3,000 railway stations for more than 4,200 high-speed trains throughout the country. Moreover, the country has a blood donation rate of 11.4 per 1,000 people, thereby denoting an optimistic outlook for the market development and expansion.

The aspects of an increase in government expenditure, the presence of blood processes and banks, a surge in the patient population receiving transfusion-based treatments, and continuous focus on investing in blood safety infrastructure upgradation are a few trends that are responsible for driving the blood banking devices market in India. As per an article published by the WHO in December 2025, there has been an upsurge in the yearly blood collection from 12.6 million units as of 2023 to 14.6 million units in 2024. Besides, voluntary-based blood donation also caters to 74.5% of overall collections in the nation, demonstrating a robust public participation, along with the impact of suitable awareness campaigns. Moreover, blood donor motivators operate across the country to encourage the public to make donations, and proactively advocates in strengthening the network across 1,131 centers, thereby positively influencing the market development.

Europe Market Insights

Europe in the blood banking devices market is projected to experience considerable growth by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by the aging demographic profile, the adoption of the Blood Directive, regulatory policies for compelling hospitals and blood banks to implement automated and closed-system devices, and a rise in rare disorders. According to official statistics published by the Europe Parliament in February 2026, rare disorders effectively impact roughly 27 million to 36 million people in the region, and also impose a persistent and substantial burden across economic, social, and health domains. Based on this growth, there has been the identification of 6,000 and 8,000 rare diseases in the country, and these diseases are frequently life-threatening, debilitating, and chronic, thereby denoting an optimistic outlook for the blood banking devices market expansion.

The blood banking devices market in Germany is gaining increased exposure, owing to regulated and decentralized healthcare systems, upgradation in testing equipment and blood processing, the rapid adoption of completely automated blood typing, the presence of antibody screening systems, and the demand for device and consumables maintenance. As stated in an article published by NLM in January 2023, the per capita blood unit production in the country is significantly defined by the number of blood donations per 1,000 inhabitants. Additionally, the per capita distribution in the nation has also been defined by the number of blood components distributed per 1,000 inhabitants. Moreover, almost 60% of blood donations in the nation are whole-blood donations, with red blood cells accounting for the largest blood component share for almost 73%, thereby fueling the market growth.

The centralized blood banking operations, robust government commitment to ensure transfusion safety, generous investment plans, an increase in the deployment of automated blood connection systems, and the aging population are highly responsible for proliferating the blood banking devices market in France. As per an article published by NLM in December 2022, the French Blood Transfusion Service (BTS) recorded nearly 1.5 million donors, of which almost 250,000 are considered new or first-time donors, which is 16%, for an overall 2.8 million blood donations. Therefore, this increased demand for blood in the country is due to progress in the medical sector in combination with the enhanced life expectancy of the domestic population. In addition, the demand for blood has been effectively stabilized for the past 10 years, thereby making it suitable for driving the market development.

Key Blood Banking Devices Market Players:

- Terumo Corporation (Japan)

- Haemonetics Corporation (U.S.)

- Fresenius Kabi AG (Germany)

- Grifols, S.A. (Spain)

- Macopharma (France)

- Becton, Dickinson and Company (BD) (U.S.)

- Thermo Fisher Scientific, Inc. (U.S.)

- Beckman Coulter, Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Sysmex Corporation (Japan)

- Kawasumi Laboratories, Inc. (Japan)

- Siemens Healthineers (Germany)

- Roche Holdings AG (Switzerland)

- Medtronic plc (Ireland)

- Immucor, Inc. (U.S.)

- Baxter International Inc. (U.S.)

- Steris Corporation (U.S.)

- Hindustan Syringes and Medical Devices Ltd. (HMD) (India)

- Orbis Diagnostics Pvt. Ltd. (India)

- GVS S.p.A. (Italy)

- Haemonetics Corporation (U.S.)

- Tata Memorial Center (TMC) (India)

- StemCyte International (Taiwan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Terumo Corporation is recognized as a global leader in automated blood collection systems, particularly apheresis technology, which allows for the selective separation and collection of specific blood components from donors. The company focuses heavily on integrating digital connectivity into its blood processing platforms to enhance traceability and operational efficiency for large-scale blood banks.

- Haemonetics Corporation specializes in integrated blood management solutions, offering a comprehensive portfolio that spans collection, filtration, and diagnostic devices designed to optimize the entire blood supply chain. The company has strategically shifted toward providing software-driven platforms that help hospitals and blood centers reduce reliance on donor blood through patient blood management protocols.

- Fresenius Kabi AG holds a strong position in the blood collection and transfusion segment, manufacturing a wide range of single-use consumables, including blood bags, transfusion sets, and apheresis kits for plasma collection. The company leverages its deep expertise in sterile manufacturing and closed-system design to support blood safety across both developed and emerging healthcare markets.

- Grifols, S.A. is a vertically integrated player with a strong focus on plasma-derived therapies, which has driven its expertise in large-scale automated plasma collection systems and companion diagnostic devices. The company has invested heavily in digitalization, developing connected platforms that link collection devices directly to fractionation facilities to streamline plasma supply chain management.

- Macopharma is a specialist manufacturer of blood bag systems and transfusion-related devices, known for its innovations in pathogen reduction technology that helps inactivate viruses and bacteria in donated blood components. The company focuses on providing customized solutions for blood centers, including closed processing systems that maintain sterility throughout component separation and storage.

Here is a list of key players operating in the global blood banking devices market:

The blood banking devices market is moderately consolidated, with North America and Europe-specific multinationals holding significant share through diversified portfolios spanning collection, processing, and storage systems. Simultaneously, Japan-based firms excel in apheresis and automated technologies. Strategic initiatives focus on three vectors, including automation integration, geographic expansion into the Asia Pacific's high-growth markets, and vertical integration of consumables to secure recurring revenue. Besides, in December 2024, GVS S.p.A. initiated an agreement to acquire Haemonetics Corporation’s Transfusion Medicine business, deliberately marking a suitable milestone for GVS. This acquisition strengthened the company’s position in the healthcare filtration industry and further expanded its worldwide reach, thus positively impacting the blood banking devices industry.

Corporate Landscape of the Blood Banking Devices Market:

Recent Developments

- In April 2026, Grifols indicated that its Procleix Plasmodium Assay received approval from the U.S. FDA for effectively screening blood donors for malaria. Additionally, this particular organizational assay received the CE mark as of 2022, and emerged as the first-ever automated nucleic acid test (NAT).

- In November 2025, StemCyte International launched its Public Bank Matching Protection Service in Taiwan, which was developed by collaborating with notable insurance partners, including Taishin Life, which is the first-of-its-kind model for connecting insurance coverage to public cord blood resources.

- In June 2025, ICICI Bank collaborated with Tata Memorial Center (TMC) and began the construction of the newest building at the Homi Bhabha Cancer Hospital and Research Center (HBCHRC) in Andhra Pradesh to provide specialty care for blood cancer with a commitment of more than USD 58.6 million.

- Report ID: 8529

- Published Date: Apr 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.