Battery Management System Market - Regional Analysis

APAC Market Insights

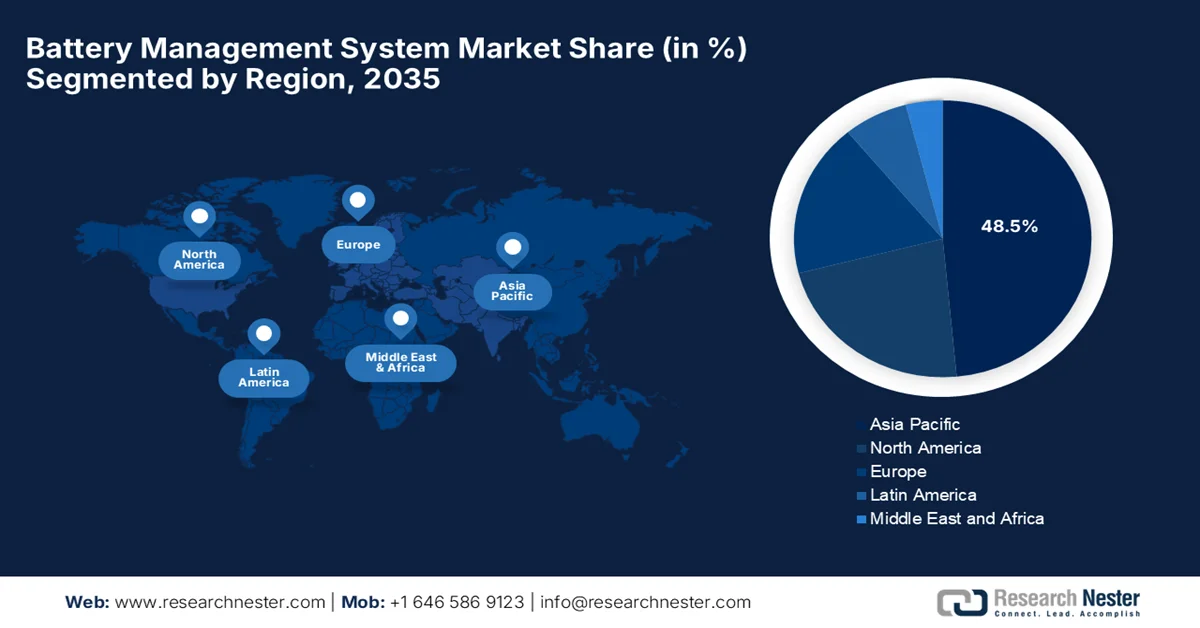

The Asia Pacific battery management system market is projected to be the largest market, capturing a revenue share of 48.5% during the forecast period. The region’s leadership is effectively attributable to the dominance in EV production, battery manufacturing, and renewable energy. The region benefits from suitable government subsidies, localized production of lithium-ion cells, and a robust supply chain centered in China, South Korea, and Japan. In this context, the IEA in 2023 revealed that battery demand and supply are heavily concentrated in China, which is dominating global lithium-ion production. Besides, China alone accounts for nearly 85% of global battery cell manufacturing capacity. The report also stated that the extraction and processing of critical minerals is similarly concentrated, with China at the forefront of producing the most essential materials, hence positively impacting BMS market growth.

China battery management system market is one of the largest and most influential landscapes, which is efficiently fueled by the country’s global leadership in electric vehicle manufacturing and the rapid expansion of large-scale energy storage projects. The country is witnessing a transition to renewable energy, due to which the BMS market is evolving from simple monitoring tools into integrated smart systems, which are essential for both the automotive and industrial sectors. As per the article published by IEA in 2025, China is the leader in the global EV battery supply chain, which has accounted for 80% of global battery cell production in 2024. It also supplies nearly 85% of cathode active materials and over 90% of anode active materials, giving it a near monopoly in component manufacturing. In addition, China refined about 65% of global lithium and three-quarters of cobalt, while dominating graphite mining and refining, in turn, denoting a lucrative growth opportunity for battery management systems.

The national push toward electric mobility and the inclusion of renewable energy into the power grid are driving the battery management system (BMS) market in India. Local manufacturing is gaining momentum as the government implements self-reliance initiatives and production incentives, which are providing encouraging opportunities for domestic firms to develop proprietary hardware and software solutions. In June 2025, the Press Information Bureau (PIB) reported that the Ministry of Power, Government of India, has launched a 30 GWh viability gap funding scheme to expand battery energy storage systems, aiming to attract USD 3.96 billion in investment and meet India’s storage needs by the end of 2028. The government also extended the ISTS waiver for storage projects until mid-2028 and added historic renewable capacity of 29.5 GW in 2024-25, contributing to a total installed capacity of 472.5 GW, hence making it suitable for exponential market growth in the years ahead.

North America Market Insights

The rapid electrification of the transportation sector and significant lithium-ion trade flows are certain drivers responsible for uplifting the battery management system market in North America. The region's extensive focus on high-performance electric vehicles and stringent safety regulations encourages manufacturers to opt for advanced diagnostics and thermal management technologies. In this context, the November 2025 data from the Congress government disclosed that the U.S. lithium-ion battery manufacturing has grown sharply from 2020 to 2024, wherein the output rose 359%, and domestic assembly capacity also expanded. Besides, in the import aspect, China supplied 69% of finished batteries and 33% of non-lead-acid battery parts in 2024. On the other hand, exports surged, notably to Mexico, reflecting both growing production and cross-border trade, hence denoting a positive BMS market outlook.

The U.S. market is all set to witness extensive growth due to the presence of major automotive and technology firms, which fosters a competitive environment for innovation. The BMS market dynamics are also reshaped by government initiatives, which are aimed at strengthening domestic supply chains and manufacturing independence, and have accelerated the development of localized hardware and specialized battery control technologies. In July 2024, the IEA stated that under the U.S. Infrastructure Investment and Jobs Act, USD 7.5 billion has been allocated to establish a network of 500,000 electric vehicle chargers in the country. It stated that these funds are administered through the National Electric Vehicle Formula Program, thereby enabling states to deploy publicly accessible charging and fueling infrastructure. Moreover, this initiative aims to support the expansion of EV adoption by ensuring reliable charging access, hence denoting a huge growth opportunity for battery management systems.

Canada’s abundant critical mineral resources and a focus on building a domestic end-to-end electric vehicle supply chain are responsible for uplifting the battery management system market in Canada. Growth in the country’s market is efficiently propelled by significant federal and provincial investments in large-scale battery manufacturing plants and cross-border integration with the region’s automotive industry. The government of Canada, in October 2025, announced more than USD 22 million in funding for eight projects with the main goal of accelerating battery innovation and production capacity. Besides, these investments aim to enhance battery performance, reduce costs, strengthen Canada’s supply chains, and reduce the overall environmental impacts. Therefore, with scaling domestic production, the country is positioning itself as a predominant leader in clean energy and battery innovation.

Europe Market Insights

The primary emphasis on sustainability and circular economy principles boosts the battery management system market in Europe. Growth in this region is largely propelled by the carbon neutrality goals and the rapid transition of its established automotive industry toward full electrification. The European Commission in December 2025 reported that it has launched the battery booster facility to strengthen Europe’s battery manufacturing ecosystem as part of its clean energy transition. The report states that this facility will mobilize up to USD 1.6 billion from the Innovation Fund, financed through EU ETS revenues, to support battery cell producers during their ramp-up phase. In addition, as the continent expands its domestic battery cell production, the market is evolving toward intelligent systems that support second-life applications and integration with renewable energy networks.

The battery management system market in Germany is growing at a noteworthy pace due to the large automotive engineering expertise and the integration of smart software and cloud-based diagnostics. The country is highly focused on decentralized energy storage and grid stabilization, which is pushing the boundaries of BMS functionality, ensuring these systems are essential for both transport and the transition to renewable power. As per an article published by the National Institute of Health (NIH) in July 2025 in Germany, BMS requirements are largely shaped by national, regional, and international standards, which cover both hardware and software components. It also stated that these requirements are classified as functional i.e,., state of charge and energy management, and non-functional, such as reliability and robustness, and into qualitative and quantitative criteria. Furthermore, the report highlighted the urgent need for updated, consistent standards to enhance safety, interoperability, and performance.

UK’s net-zero targets and the mandatory transition toward zero-emission vehicles are accelerating the UK market growth. The country’s market is also driven by government-backed initiatives and substantial funding, which support moving battery technologies from research to production. Based on the government data, which was published in November 2023, the UK battery strategy outlined the government’s vision to build a competitive battery supply chain in the global landscape by the end of 2030. It is focused on designing and developing future batteries, strengthening domestic manufacturing resilience, and enabling a sustainable battery industry. The approach is built around design-build-sustain, ensuring innovation, supply chain security, and sustainability, hence making it suitable for standard market growth.