Automotive Powertrain Electronics Market Outlook:

Automotive Powertrain Electronics Market size was valued at USD 69.14 billion in 2025 and is expected to reach USD 152.06 billion by 2035, registering around 8.2% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of automotive powertrain electronics is assessed at USD 74.24 billion.

The reason behind the growth is impelled by surge in the demand for automotive electronic components. The demand from consumers for high-end, technologically advanced vehicles with integration and implementation of current safety technologies such as automated airbags, parking assistance systems, and emergency braking, is expected to drive market growth.For instance, electronics are projected to account for about 50% of the cost of the new car by 2030.

The growing vehicle fleet is believed to fuel the demand for automotive powertrain electronics with research and custom development of advanced electronics used in automobiles to improve its overall performance and longevity.For instance, it was found that the Indian auto industry produced a total of 22,933,000 vehicles in the financial year 2020.

Key Automotive Powertrain Electronics Market Insights Summary:

Regional Highlights:

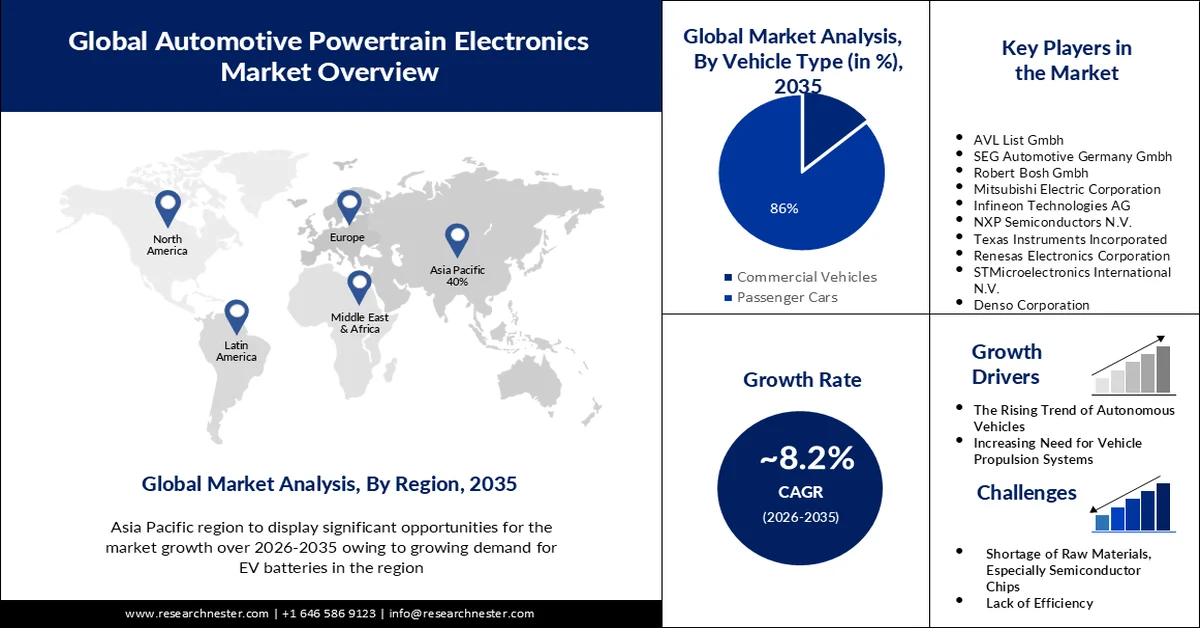

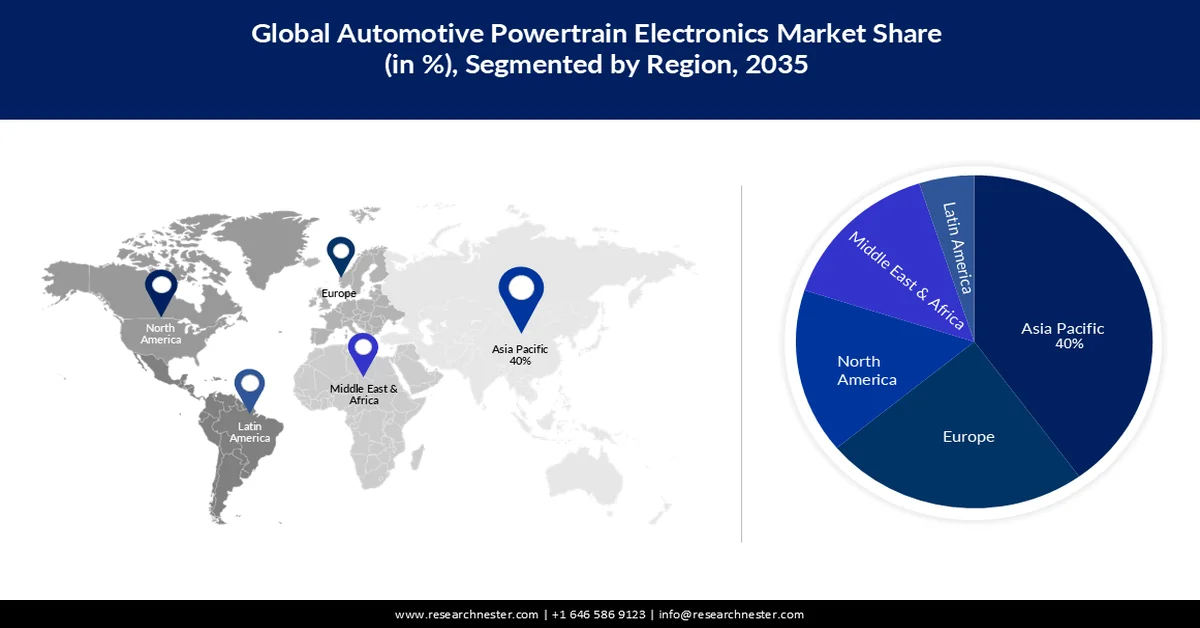

- Asia Pacific is projected to hold the largest market share of 40% by 2035, impelled by the surging demand for EV batteries and advanced battery management systems.

- Europe is expected to secure the second-largest share by 2035, driven by growing investments in electric and hybrid powertrain technologies.

Segment Insights:

- The passenger cars segment is projected to account for 86% share by 2035, driven by the rising global production of passenger vehicles and the increasing demand for fuel-efficient powertrain systems.

- The electric motor segment is anticipated to capture a significant share by 2035, owing to the growing adoption of electric vehicles requiring advanced powertrain electronics.

Key Growth Trends:

- Increasing Need for Vehicle Propulsion Systems

- The Rising Trend of Autonomous Vehicles

Major Challenges:

- Shortage of Raw Materials, Especially Semiconductor Chips

- Lack of Efficiency

Key Players: Bio-Rad Laboratories, Inc., New England Biolabs, Inc., Nippon Gene Co., Ltd., Omega Bio-tek, Inc., LGC Limited, Excellgen.com, Meridian Bioscience, Inc., HiberGene Diagnostics, Jena Bioscience GmbH.

Global Automotive Powertrain Electronics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 69.14 billion

- 2026 Market Size: USD 74.24 billion

- Projected Market Size: USD 152.06 billion by 2035

- Growth Forecasts: 8.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (40% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, South Korea

- Emerging Countries: China, India, Japan, South Korea, Germany

Last updated on : 25 February, 2026

Automotive Powertrain Electronics Market - Growth Drivers and Challenges

Growth Drivers

-

Increasing Need for Vehicle Propulsion Systems – These systems are increasingly being used in electric and hybrid vehicles, which often require sophisticated energy management, which necessitates the use of automotive powertrain electronics.

-

The Rising Trend of Autonomous Vehicles- These vehicles rely on complex electronic systems such as electronic control units (ECUs) and domain control units (DCUs) to control the powertrain effectively. This has significantly driven market growth.

It was found that there were over 30 million autonomous cars globally in 2019, and this number is expected to reach nearly 54 million in 2024.

Challenges

-

Shortage of Raw Materials, Especially Semiconductor Chips – The expanding use of new semiconductors in various applications, such as automotive and industrial applications was altered by the coronavirus outbreak, which also affected the world’s supply of chips. The pandemic’s initial impact was felt in China and Taiwan, the most prominent chip-producing nations, where companies were forced to close down. Even though the production bounced back, semiconductor sales increased in 2020, and unexpected demand spikes spurred on by shifting consumer behavior as well as issues with capacity allocation led to a worldwide chip shortage in the year 2021.

-

Lack of Efficiency

- Low-Cost Power Module Packaging

Automotive Powertrain Electronics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.2% |

|

Base Year Market Size (2025) |

USD 69.14 billion |

|

Forecast Year Market Size (2035) |

USD 152.06 billion |

|

Regional Scope |

|

Automotive Powertrain Electronics Market Segmentation:

Vehicle Type Segment Analysis

The passenger cars segment in the automotive powertrain electronics market is estimated to gain a robust revenue share of 86% in the coming years owing to the growing production of passenger cars across the globe. As the per capita income of people across the globe is rising more people can afford passenger cars, which has increased its production. These cars require powertrain electronic systems to meet fuel efficiency, control emissions, and manage battery systems.

For instance, globally more than 55 million passenger cars were produced worldwide in 2021.

Component Type Segment Analysis

The electric motor segment is set to garner a notable share shortly backed by growing demand for electric motors in EVs. All-electric vehicles, also known as battery electric vehicles (BEVs), have an electric motor since they only run on battery power. These motors require powertrain electronics to control and optimize the complete flow of energy in EVs and also manage the motor’s speed.

Our in-depth analysis of the global market includes the following segments:

|

Component Type |

|

|

Device Type |

|

|

Application |

|

|

Vehicle Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Powertrain Electronics Market - Regional Analysis

APAC Market Insights

Automotive powertrain electronics market in Asia Pacific is predicted to account for the largest share of 40% by 2035 impelled by the growing demand for EV batteries. China is the largest market for electric vehicles (EVs) in the region which has increased the demand for EV batteries. These batteries require advanced power management systems and battery management systems to improve overall performance and efficient charging, leading to higher demand for automotive powertrain electronics in the region. For instance, it was found that as of 2022 China dominated EV battery production with approximately 70% of all battery cells.

European Market Insights

The Europe automotive powertrain electronics market is estimated to be the second largest, during the forecast timeframe led by growing investment in electric and hybrid powertrains. Since hybrid electric vehicles are powered by internal combustion engines, there may be a rise in the demand for automotive powertrain electronics in the region.

Automotive Powertrain Electronics Market Players:

- Schaeffler AG

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- AVL List Gmbh

- SEG Automotive Germany Gmbh

- Robert Bosh Gmbh

- Mitsubishi Electric Corporation

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- STMicroelectronics International N.V.

- Denso Corporation

- Alps Alpine Co., Ltd.

Recent Developments

- Schaeffler AG developed high quality electric motors for commercial vehicles that are more than 97% efficient providing a continuous drive power output of up to 300 kW. It has 800-volt power electronics that deliver weight and cost savings for manufacturers, and require shorter charging times with an innovative thermal management system.

- Renesas Electronics Corporation announced a new Intelligent Power Device (IPD) for automobiles, known as the RAJ2810024H12HPD. With this device, vehicles can distribute power safely and flexibly, addressing E/E (electrical/electronic) architecture requirements in the future.

- Report ID: 4511

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.