Algae Protein Market Outlook:

Algae Protein Market size was valued at USD 1 billion in 2025 and is projected to reach USD 1.7 billion by the end of 2035, growing at around 5.3% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of algae protein is estimated at USD 1.1 billion.

The algae protein market is closely related to advances in large-scale algal biomass production economics and expanding global algae output. According to the U.S. Department of Energy’s National Renewable Energy Laboratory (NREL) 2022 data, the techno-economic analysis for commercial algae cultivation demonstrated that the minimum biomass selling prices (MBSP) could reach USD 681 per ton under mature nth-plant operating conditions using unlined cultivation ponds, while lined pond systems were estimated at USD 844 per ton. Under optimized environmental conditions modeled from the Algae Testbed Public-Private Partnership (ATP3) Florida site, costs declined further to nearly USD 602 per ton for unlined ponds. These findings show that the protein extraction economics are directly influenced by upstream biomass cultivation costs, water management efficiency, and nutrient recycling performance.

Besides, the Food and Agriculture Organization’s June 2024 data depict that the global fisheries and aquaculture production reached 223.2 million tons in 2022, including 37.8 million tons of algae production. This represented a 4.4% increase compared with 2020 levels, indicating expanding cultivation capacity and stronger integration of algae into global food and feed supply chains. Rising algae output supports greater availability of spirulina, chlorella, and other protein-rich biomass inputs used in nutritional ingredients and aquafeed formulations. Institutional demand is further supported by resource efficiency objectives, particularly because algae cultivation can operate on non-arable land and saline water systems. As commercial-scale cultivation improves and production costs decline, algae protein suppliers are positioned to strengthen supply agreements with food ingredient manufacturers, feed producers, and biotechnology companies seeking stable and traceable protein sourcing strategies.

Key Algae Protein Market Insights Summary:

Regional Highlights:

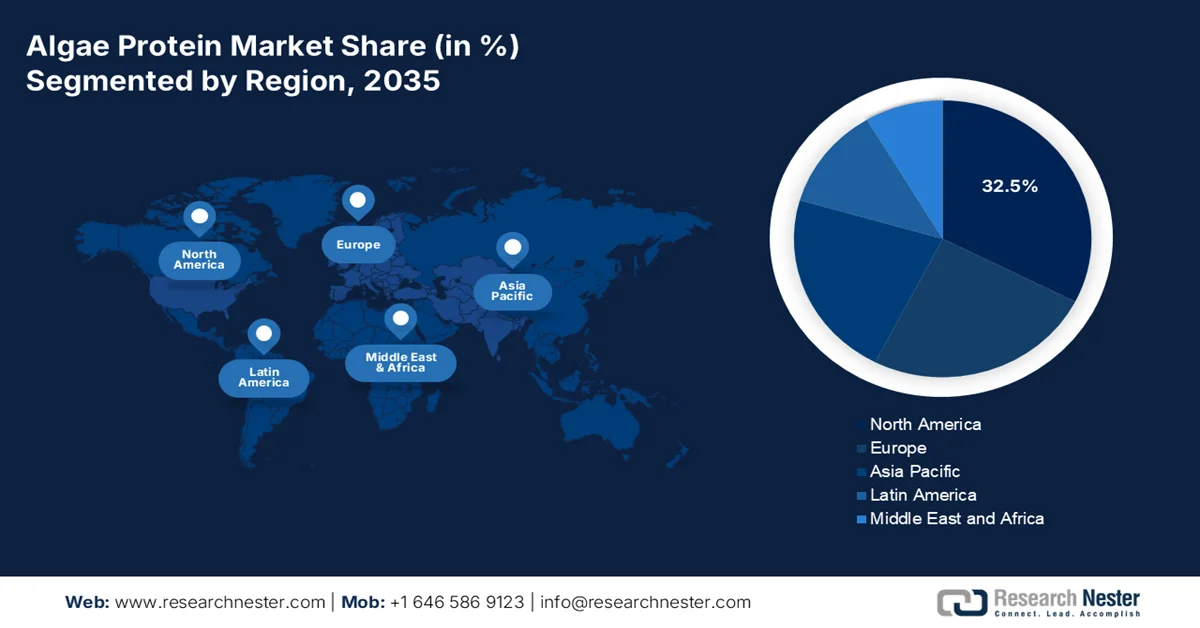

- The North America region is anticipated to capture 32.5% of the algae protein market share by 2035, fostered by rising demand for clean-label protein ingredients and expanding adoption across sports nutrition and functional food manufacturing

- Asia Pacific is forecast to witness rapid expansion in the market throughout 2026-2035, stimulated by cost-efficient cultivation infrastructure and growing large-scale spirulina production for feed and food applications

Segment Insights:

- The spirulina sub-segment is projected to account for 55.6% of the algae protein market share by 2035, propelled by advancements in continuous cultivation systems and nutrient optimization strategies improving biomass and phycocyanin yields

- The isolates segment is emerging as a dominant category in the market through 2035, attributed to superior emulsifying functionality and increasing utilization in dairy alternatives and meat analog formulations

Key Growth Trends:

- Rising vegan and plant-based food consumption

- Pressure on agricultural land and water resources

Major Challenges:

- High production costs

- Regulatory hurdles and novel food approvals

Key Players: Corbion (Netherlands), Cyanotech Corporation (U.S.), TerraVia Holdings, LLC (U.S.), DIC Corporation (Japan), Far East Bio-Tec Co. (Taiwan), Algaecytes (U.S.), Roquette Frères (France), Seagrass Tech Private Limited (India), Sabinsa Corporation (U.S.), Synergy (U.S.), Parry Nutraceuticals (India), Algama (France), Aliga Microalgae (Denmark), Heliae Development, LLC (U.S.), Allma (Portugal), Triton Algae Innovations (U.S.), Cellana (U.S.), CEAMSA (Spain), SIG (Switzerland), Edonia (France).

Global Algae Protein Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1 billion

- 2026 Market Size: USD 1.1 billion

- Projected Market Size: USD 1.7 billion by 2035

- Growth Forecasts: 5.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (32.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, India

- Emerging Countries: South Korea, Canada, Malaysia, Indonesia, Thailand

Last updated on : 21 May, 2026

Algae Protein Market - Growth Drivers and Challenges

Growth Drivers

- Rising vegan and plant-based food consumption: The growing vegan population is becoming a demand driver for the algae protein market as the food manufacturers expand their alternative protein product portfolios. According to the World Population Review 2026 data, nearly 9% of the population is vegan in India. Government and intergovernmental organizations, including the Food and Agriculture Organization (FAO) and the U.S. Dietary Guidelines, continue to push diversified and sustainable protein consumption patterns. Algae proteins such as spirulina and chlorella are gaining commercial adoption in vegan beverages, nutritional supplements, meat substitutes, and functional foods because of their high protein density and lower land and water requirements compared with animal proteins. Rising sustainability targets among food companies are also accelerating the procurement of traceable algae-derived protein ingredients globally.

Countries with the Highest Share of Vegans, 2026

|

Country |

Percentage |

|

India |

9 |

|

Mexico |

9 |

|

Canada |

5 |

|

Israel |

5 |

|

Sweden |

4 |

|

Norway |

4 |

Source: World Population Review 2026

- Pressure on agricultural land and water resources: Governments and agricultural agencies are increasingly supporting the alternative protein systems due to the rising land and freshwater constraints. The Plant Based Food Institute April 2022 data depicts that the livestock production utilizes nearly 77% of global agricultural land while generating significantly lower calorie efficiency relative to total land use. Algae cultivation requires substantially less arable land and can operate using saline or wastewater systems, making it commercially attractive for industrial protein production. Water conservation policies in regions facing agricultural stress are encouraging investment in controlled algae cultivation infrastructure. The U.S. Environmental Protection Agency and DOE have also promoted algae systems capable of nutrient recovery and wastewater integration. These operational advantages are attracting food processors and ingredient suppliers seeking long-term supply resilience.

Challenges

- High production costs: The capital-intensive nature of the algae cultivation and processing remains the most formidable barrier in the algae protein market. Building large-scale photobioreactor or open pond systems requires millions in the upfront investment, ongoing operational costs for the nutrients, energy, and labor further inflate the expenses. The Center for Feed Innovation reported that algae oil prices are substantially higher than conventional fish oil, highlighting the economic difficulty of achieving competitive pricing.

- Regulatory hurdles and novel food approvals: Navigating international regulatory frameworks presents a complex, time-consuming challenge. In the EU, many microalgae species require approval under the Novel Food Regulation before commercialization, with rigorous safety assessments extending timelines considerably. The European Commission approved many algae species for food use, streamlining some pathways. The approval process remains resource-intensive for smaller entrants without dedicated regulatory teams.

Algae Protein Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.3% |

|

Base Year Market Size (2025) |

USD 1 billion |

|

Forecast Year Market Size (2035) |

USD 1.7 billion |

|

Regional Scope |

|

Algae Protein Market Segmentation:

Source Segment Analysis

Under the source segment, the spirulina sub-segment is leading in the algae protein market and is poised to hold the share value of 55.6% by 2035. The segment is driven by the focus from strain selection to integrated continuous cultivation and harvesting strategies, which critically influence biomass and phycocyanin yields. According to the NLM March 2025 study, NaNO₃ deficiency drastically reduces Spirulina biomass productivity to just 0.015 g/L/day, while a harvesting ratio of 10% consistently yielded 0.20g to 0.22 g of dry biomass. Moreover, adding 2.50 g/L NaNO₃ boosted C-phycocyanin concentration from 34.37 mg/g to 68.35 mg/g and allophycocyanin from 27.08 mg/g to 33.23 mg/g. These findings underscore that the nutrient replenishment and continuous harvesting protocols are essential for maximizing the spirulina's value as a high-purity protein and the bioactive compound source in the industrial biorefineries.

Type Segment Analysis

Within the type segment, the isolates are leading in the algae protein market. The dominance is due to the neutral taste, smooth mouthfeel, and emulsifying capabilities, which outperform pea and soy isolates in dairy alternatives and meat analogs. As per the NLM study published in August 2025, isolates directly impact functional value in food applications. SDS-PAGE analysis shows that Tetraselmis sp. isolates feature distinct protein bands at 50, 40, 25, and 15 kDa, with a prominent 50 kDa band, while smaller bands represent RuBisCo enzymes. Soluble protein isolates from Nannochloropsis gaditana and Tetraselmis impellucida are rich in RuBisCo, comprising 20–40% of total protein, whereas Arthrospira maxima isolates are predominantly composed of C-phycocyanin. Notably, N. gaditana and T. impellucida isolates contain higher proportions of multimeric proteins compared to A. maxima, which shows elevated monomeric protein levels. A critical consideration for isolate quantification is that algae proteins contain 5.3% non-protein nitrogen on average, necessitating adjusted calculation methods versus animal proteins for accurate purity assessment.

Application Segment Analysis

In the algae protein market, the dietary supplements sub-segment consistently leads as the primary application, driven by consumer preference for natural, plant-based, and nutrient-dense health products. Algae protein, particularly from spirulina and chlorella, is widely incorporated into tablet, capsule, and powder formats targeting immune support, sports recovery, and daily wellness. The supplements segment benefits from algae's inherent micronutrient density, including bioavailable iron, vitamin B12, and phycocyanin, which are often lacking in other plant proteins. Manufacturers increasingly market algae-based supplements as clean-label, non-GMO, and sustainably produced. While food and beverage applications are growing rapidly, especially in dairy alternatives, baked goods, and meat analogs, the dietary supplements segment remains the largest revenue contributor due to established consumer trust, regulatory acceptance, and premium pricing potential.

Our in-depth analysis of the algae protein market includes the following segments:

|

Segment |

Subsegments |

|

Source |

|

|

Type |

|

|

Form |

|

|

Extraction Method |

|

|

Application |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Algae Protein Market - Regional Analysis

North America Market Insights

North America is dominating the algae protein market and is expected to hold the regional revenue share of 32.5% by 2035. The market is characterized by a mature dietary supplements channel and accelerating interest from food and feed manufacturers. In the U.S., the demand is driven by the sports nutrition brands seeking complete protein sources and clean-label color solutions using phycocyanin. Canada distinguishes itself via cold water strain cultivation and strategic blending of algae with pulse proteins to improve amino acid profiles. Government-funded research initiatives focus on reducing the harvesting and extraction costs, while the public procurement programs in the schools and federal institutions are emerging as stable demand channels. B2B contracting remains the dominant distribution model, with long-term agreements between the cultivators and finished goods manufacturers ensuring supply chain predictability.

The strong federal investment in algae biomanufacturing, carbon utilization, and sustainable fuel co-production programs is driving the algae protein market in the U.S. According to the U.S. Department of Energy, the July 2024 national microalgae biomass production potential is at 152 million tons annually, representing nearly 268 million tons of CO2 utilization capacity across 1,000 viable algae farm sites. DOE analysis also showed that algal fuel and protein co-production could reduce emissions by up to 90% compared with conventional fuel and whey protein systems when supported by low-emission electricity sources. In addition, DOE 2026 announced USD 20.2 million in funding for algae conversion and bioproduct development projects to strengthen low-carbon fuel, agricultural, and animal feed supply chains, directly supporting commercial expansion opportunities for algae protein producers in the U.S.

The supportive regulatory approvals and expanding commercialization of algae-derived food ingredients are shaping the algae protein market in Canada. According to the Government of Canada, February 2023 data, Health Canada approved high oleic algal oils developed by Corbion Biotech using genetically modified Prototheca moriformis strains, confirming that the products are as safe and nutritious as conventional edible oils. The oils contain more than 80% oleic acid and are intended for use across multiple food categories in Canada. Health Canada’s assessment also noted that algae-derived products, including algal flour and protein ingredients, have already received prior approvals supporting broader acceptance of algae-based nutrition products. Commercial-scale production under current Good Manufacturing Practices, combined with growing regulatory confidence in algae-derived food ingredients, is strengthening investment opportunities for algae protein manufacturers targeting Canada’s plant-based food nutrition and specialty ingredient sectors.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035, in the algae protein market. The region is driven by the established cultivation infrastructure, lower production costs, and proximity to high-demand end markets. Japan and South Korea lead in phycocyanin extraction for functional beverages, while China and India scale spirulina biomass for both domestic feed applications and export. Southeast Asia nations, mainly Malaysia and Indonesia, leverage year-round tropical conditions for open pond cultivation, achieving higher annual yields than temperate regions. Government-backed farmer cooperatives in India and Thailand aggregate small-scale algae production for B2B ingredient supply. The region also serves as a manufacturing hub for algae-enriched noodles, baked goods, and meat analogs destined for local and Western markets.

The increasing pressure on livestock feed resources and rising demand for sustainable alternative proteins are driving the algae protein market in India. As per the Invest India September 2022 data, India supports 17.5% of the global population and nearly 20% of the world’s livestock on only 2.3% of global land area, creating severe feed shortages, including a 35.6% deficit in green fodder and a 44% shortage in concentrate feed ingredients. This imbalance is accelerating interest in non-conventional feed resources such as algae-based feed ingredients. Microalgae, including Chlorella, Scenedesmus, and Arthrospira, contain approximately 40% to 60% protein and are increasingly recognized for improving livestock growth and feed efficiency. Government-backed initiatives under the National Livestock Mission, including 50% capital subsidies for feed and fodder infrastructure, are further supporting investment opportunities for algae-derived protein and feed manufacturers in India.

The Japan algae protein market is expected to expand from USD 47.83 million in 2025 and reach USD 77 million by the end of 2035 at a CAGR of 4.86% during the assessed period. In 2026, the market is set to reach USD 50.17 million. The nation is driven by the rising demand for plant-based protein ingredients, driven by increasing health and environmental awareness. According to the USDA August 2023 data, the vegan and vegetarian population remains relatively small. The country’s plant-based protein ingredient market reached approximately USD 323 million in 2021, reflecting a 14.2% increase. Demand for meat alternatives is also expanding, with Japan’s plant-based meat market projected to grow from nearly USD 18 million in 2022 to USD 29 million by 2025. The rapid increase in plant-based products available in supermarkets and food-service channels is creating new opportunities for algae-derived proteins used in nutritional foods, beverages, and alternative meat formulations.

Production of Isolated Soy Protein in Japan, 2023

|

Year |

Volume (MT) |

|

2010 |

23, 560 |

|

2020 |

36, 046 |

|

2021 |

36, 054 |

|

2022 |

36, 703 |

Source: USDA August 2023

Europe Market Insights

The algae protein market in Europe is shaped by the stringent novel food regulations, strong sustainability mandates, and active government funding for alternative proteins. The European Commission's Farm to Fork Strategy supports algae as a strategic protein source, while the EU Algae Initiative facilitates B2B matchmaking and consumer acceptance campaigns. Germany, France, and the Netherlands lead in algae-enriched bakery pasta and dairy alternatives, with formulators prioritizing neutral-tasting isolates from Tetraselmis and Nannochloropsis strains. Nordic countries focus on cold water photobioreactor cultivation, reducing energy costs compared to heated systems. Direct B2B contracting via retail channels is expanding through certified organic and non-GMO algae products. Horizon Europe grants continue to fund the harvesting efficiency and protein extraction research, lowering technology risk for commercial entrants.

The algae protein market in Germany is driving due to the rising plant-based food demand, sustainability targets, and government-supported bioeconomy initiatives. According to FEED Magazine, May 2025 data show that nearly 126,500 tons of vegan and vegetarian meat substitutes were produced in Germany, reflecting continued demand growth for alternative proteins. The German Federal Ministry of Food and Agriculture also reported that Germany’s organic farming area share grew to 9.8%, supporting broader consumer preference for sustainable food ingredients. The Federal Ministry of Education and Research continues to invest in Germany’s National Bioeconomy Strategy, which supports algae biotechnology and sustainable protein innovation. Rising industrial focus on low-emission food production and traceable protein sourcing is creating commercial opportunities for algae protein suppliers in Germany’s food, nutraceutical, and animal nutrition sectors.

The increasing demand for sustainable protein, alternative nutrition products, and low-carbon food systems is shaping the algae protein market in the UK. According to the Government of the UK, July 2025 data, the agri-food sector contributed 6.2% of national GVA, supporting investment in innovative food ingredients and alternative proteins. The UK Office for National Statistics reported that vegetarian and vegan product sales continued to expand across retail channels as consumers increasingly adopted plant-based diets. In addition, Innovate UK and UK Research and Innovation have continued funding sustainable biotechnology and alternative protein projects, including algae-based food innovations. These developments are strengthening commercial opportunities for algae protein suppliers targeting food manufacturing, nutraceutical, aquafeed, and functional nutrition applications across the UK.

Key Algae Protein Market Players:

- Corbion (Netherlands)

- Cyanotech Corporation (U.S.)

- TerraVia Holdings, LLC (U.S.)

- DIC Corporation (Japan)

- Far East Bio-Tec Co. (Taiwan)

- Algaecytes (U.S.)

- Roquette Frères (France)

- Seagrass Tech Private Limited (India)

- Sabinsa Corporation (U.S.)

- Synergy (U.S.)

- Parry Nutraceuticals (India)

- Algama (France)

- Aliga Microalgae (Denmark)

- Heliae Development, LLC (U.S.)

- Allma (Portugal)

- Triton Algae Innovations (U.S.)

- Cellana (U.S.)

- CEAMSA (Spain)

- SIG (Switzerland)

- Edonia (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Corbion is a dominant player in the algae protein market via its AlgaPrime™ DHA brand, which integrates lipid-rich algae protein into aquafeed and plant-based meats. The company leverages large-scale fermentation in its Brazil facility to produce a sustainable non-land-based protein. In 2024, the company made net sales of USD 1.42 billion.

- Cyanotech operates in the algae protein market mainly via its Hawai cultivation facility, producing BioAstin® astaxanthin and spirulina-based protein powders. The company emphasizes open-raceway pond technology in a controlled tropical climate to achieve high biomass output. In 2024, the company made a net sales of USD 23.2 million.

- TerraVia played a transformative role in the algae protein market by pioneering the fermentation of heterotrophic microalgae to produce high-protein flour and oil. Despite its later restructuring, TerraVia’s legacy includes the AlgaVia® platform, which yielded whole algae protein with superior functional properties for baked goods, dressings, and dairy alternatives.

- DIC Corporation is the world’s largest producer of organic spirulina in the algae protein market via its subsidiary DIC Lifetec. Headquartered in Tokyo, the company operates cultivation sites in Thailand and the U.S., focusing on phycocyanin, a blue protein pigment used as a natural colorant and functional protein.

- Far East Bio-Tec Co. has carved a specialized niche in the algae protein market by focusing on Chlorella vulgaris and Spirulina platensis grown in photobioreactors with proprietary low heavy metal protocols. The company’s headquarters in Taipei oversees R&D into enzyme-hydrolyzed algae peptides for enhanced digestibility.

Here is a list of key players operating in the global algae protein market:

The global algae protein market is moderately fragmented, with key players pivoting from niche supplement ingredients to mainstream food applications. Strategic initiatives include heavy investment in photobioreactor technology to increase yield purity, vertical integration to reduce production costs, and strategic partnerships with plant-based food giants. Companies are also focusing on strain-specific patents and expanding application portfolios into sports nutrition, meat analogs, and dairy alternatives. Geographic expansion via mergers and acquisitions is driving the production costs and rising vegan populations. For example, in December 2025, Cellana acquired PhytoSmart, which integrates an industrial foundation with revenue-generating capabilities.

Corporate Landscape of the Algae Protein Market:

Recent Developments

- In January 2026, CEAMSA announced the acquisition of the fibre line and associated intellectual property of PeelPioneers. This acquisition strengthens its strategy to offer a comprehensive and differentiated portfolio of fibre solutions.

- In October 2025, SIG and Nutrition from Water announced the partnership to advance product concepts that combine algae-based protein beverages with enhanced aseptic packaging. The initiative is designed to support the nutrition gap in quickly growing economies, delivering protein-rich nutrition to communities where it is needed most.

- In April 2024, Edonia, a start-up company in Paris, raised €2 million in a pre-seed funding round to produce its nutrient-dense, sustainable, plant-based protein from microalgae. The start-up will launch its flagship product, Edo-1, a ground beef-style clean protein with a meat-like texture, umami flavor, and no additives or artificial flavorings.

- Report ID: 4734

- Published Date: May 21, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.