Aircraft Interface Device Market Outlook:

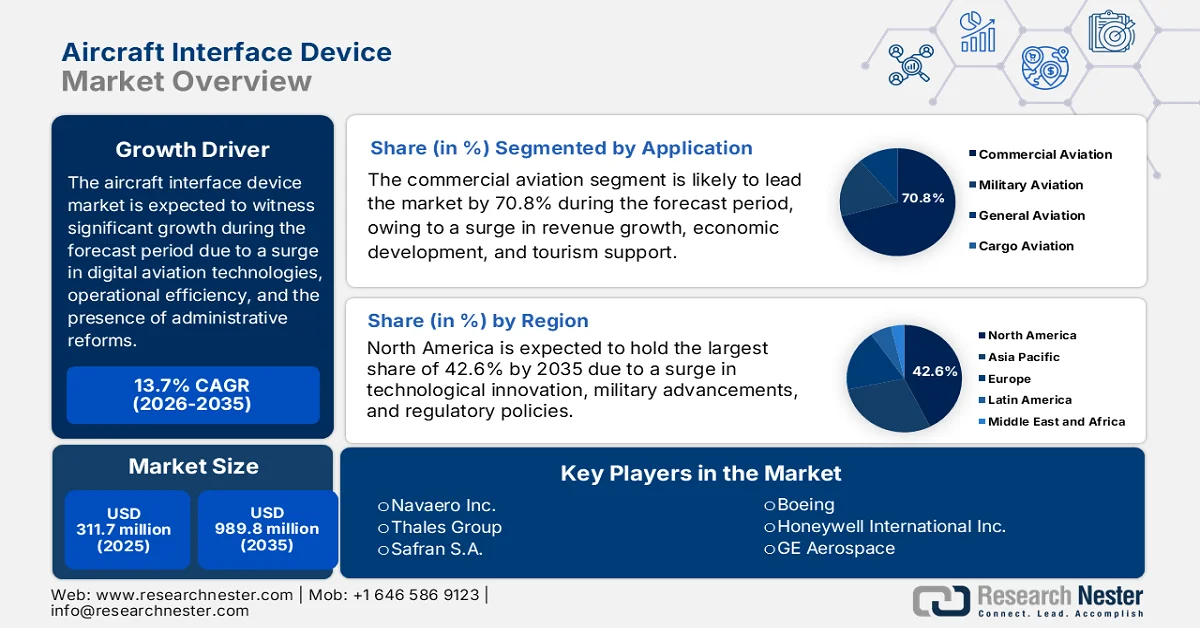

Aircraft Interface Device Market size was valued at over USD 311.7 million in 2025 and is expected to reach USD 989.8 million by the end of 2035, growing at a CAGR of 13.7% during the forecast period of 2026-2035. In 2026, the industry size of aircraft interface device is estimated at USD 354.4 million.

The worldwide aircraft interface device market is significantly undergoing a transformative phase, highly driven by the convergence of digitalized aviation technologies, evolving operator requirements for operational efficiency, and regulatory mandates. According to official statistics published by Heliyon in May 2025, in the upcoming years, 95% to 97% of airlines are projected to undertake large-scale research and development projects in three domains, including digital tags, business analytics, and aircraft maintenance. Besides, Indonesia, Malaysia, and Thailand effectively permit international ownership of almost 49% in the aviation industry. Meanwhile, the low-cost carrier segment is expanding rapidly, effectively dominated by VietJet Air, accounting for 37.6% of overall domestic flights in Vietnam during the first half of 2033, thereby making it suitable for bolstering the market globally.

Furthermore, the accelerated shift toward wireless connectivity, the integration of predictive maintenance capabilities, the aspect of cybersecurity as a core design imperative, the convergence of military and commercial interface requirements, and open architecture and modular platform design are certain trends that are fueling the aircraft interface device market globally. As stated in a data report published by the Department of Transportation in December 2025, the aviation sector in the U.S., along with its workforce, especially from large-scale commercial and manufacturing operations to strong general aviation, significantly supports USD 1.8 trillion in overall economic activity and contribute 4.0% of the gross domestic product (GDP). Besides, with almost 20,000 total landing facilities in the U.S., including an estimated 13,000 airports and more than 6,000 heliports, the country comprises an expanded network of infrastructure for accommodating flights. Of these, roughly 4,800 are publicly utilized, enabling passengers to access air transportation with transit connections, thus driving the aircraft interface device market demand.

Key Aircraft Interface Device Market Insights Summary:

Regional Highlights:

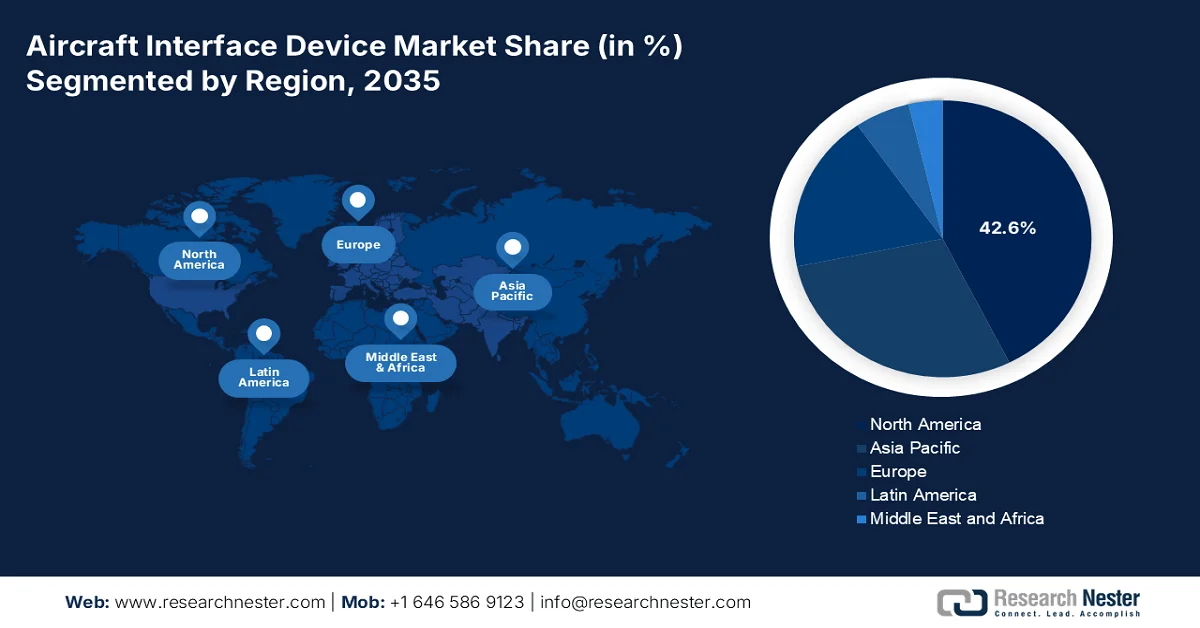

- North America aircraft interface device market is anticipated to command a 42.6% share by 2035, reinforced by technological advancements, regulatory investments, and military modernization initiatives.

- Europe is projected to register the fastest growth over the forecast period to 2035, accelerated by rising demand for advanced connectivity solutions and increasing investments in next-generation cockpit technologies.

Segment Insights:

- The commercial aviation segment in the aircraft interface device market is expected to account for a 70.8% share by 2035, propelled by its critical role in enabling global connectivity, tourism, and trade expansion.

- The fixed-wing segment is forecast to secure the second-largest share by 2035, bolstered by the extensive global fleet and growing adoption of advanced interface solutions for connectivity and operational efficiency.

Key Growth Trends:

- Expansion and modernization in commercial fleet

- Focus on next-generation air traffic management systems

Major Challenges:

- Increased development costs and long payback periods

- Skilled workforce shortage and technical expertise gap

Key Players: Collins Aerospace (RTX) (U.S.), Teledyne Controls (Teledyne Technologies) (U.S.), Astronics Corporation (U.S.), Boeing (U.S.), Honeywell International Inc. (U.S.), GE Aerospace (U.S.), L3Harris Technologies, Inc. (U.S.), Northrop Grumman Corporation (U.S.), Lockheed Martin Corporation (U.S.), Esterline Technologies Corporation (U.S.), MicroMax Computer Intelligence, Inc. (U.S.), Navaero Inc. (U.S.), Thales Group (France), Safran S.A. (France), Airbus SE (Netherlands), Elbit Systems Ltd. (Israel), Hindustan Aeronautics Limited (HAL) (India), Arconics (Ireland), Korea Aerospace Industries (KAI) (South Korea), Mitsubishi Heavy Industries, Ltd. (Japan), AvionTEq (U.S.), Trax (U.S.), Rolls-Royce (UK), Nextant Aerospace (U.S.), Shadin Avionics (U.S.).

Global Aircraft Interface Device Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 311.7 million

- 2026 Market Size: USD 354.4 million

- Projected Market Size: USD 989.8 million by 2035

- Growth Forecasts: 13.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.6% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, Brazil, South Korea, Mexico, Indonesia

Last updated on : 24 March, 2026

Aircraft Interface Device Market - Growth Drivers and Challenges

Growth Drivers

- Expansion and modernization in commercial fleet: The sustained growth of the worldwide commercial aircraft fleet is one of the most fundamental drivers for the aircraft interface device market growth globally. According to official statistics published by the Federal Aviation Administration in 2025, the aspect of system traffic in revenue passenger miles (RPMs) is expected to increase by 2.8% by the end of 2045, and meanwhile, domestic RPMs are predicted to grow by 2.7% per year, while global RPMs are anticipated to grow slightly more rapidly at 2.8% each year. Moreover, the turbine aircraft fleet, such as rotorcraft, continued its growth of 3.6% in 2022, along with 2.3% as of 2023. Additionally, this particular fleet is further projected to account for an average growth rate of 2.1% every year, thus fueling the market exposure.

- Focus on next-generation air traffic management systems: The existence of regulatory mandates demanding aircraft to be equipped for next-generation air traffic management systems effectively serves as a powerful driver for the aircraft interface device market. As stated in a data report published by the Department of Transportation in May 2025, the yearly appropriation to the Facilities and Equipment (F&E) account is utilized to improve and sustain the majority of the Federal Aviation Administration’s (FAA) air traffic control facilities and remains effectively flat at an estimated USD 3 billion every year. However, this particular stagnant funding has caused the administrative organization to lose almost USD 1 billion in purchasing power, owing to inflation, thereby boosting the aircraft interface device market growth and development.

- Increase in predictive maintenance: The aviation sector’s transition from scheduled maintenance to predictive maintenance is escalating the aircraft interface device market adoption across different segments. Presently, airlines have identified that unscheduled maintenance incidents represent a significant financial and operational burden, along with engine-based delays that immensely cost the industry yearly. Besides, the industry serves as the transmission backbone and data acquisition for health monitoring systems by gathering real-time data from engines, systems, and airframes, while ensuring transmission to groundbreaking analytics platforms. Furthermore, the integration of innovative analytics, machine learning, and artificial intelligence has also enhanced the ability to detect anomalies, thus bolstering the market expansion across different regions.

Challenges

- Increased development costs and long payback periods: The aircraft interface device market is characterized by exceptionally high research, development, and certification costs coupled with extended revenue realization timelines, creating significant financial barriers for market participants. Besides, developing a certifiable interface device requires investment in specialized engineering talent, compliance with DO-178C and DO-254 design assurance standards, investment in environmental qualification testing, and navigation of multi-year certification processes with aviation authorities. Moreover, for a single product family, development costs can range from tens to hundreds of millions of dollars, with revenue generation commencing only after certification is achieved, often four to six years after initial investment.

- Skilled workforce shortage and technical expertise gap: The aircraft interface device market faces a mounting challenge in recruiting and retaining specialized engineering talent capable of navigating the intersection of aerospace certification, avionics architecture, software engineering, and cybersecurity domains. The workforce required to design, certify, and support these systems must possess deep expertise in real-time embedded systems, safety-critical software development, aerospace communication protocols, and regulatory compliance frameworks, which is a combination of skills that is increasingly scarce as experienced professionals retire and academic programs focus on non-aerospace technology sectors.

Aircraft Interface Device Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

13.7% |

|

Base Year Market Size (2025) |

USD 311.7 million |

|

Forecast Year Market Size (2035) |

USD 989.8 million |

|

Regional Scope |

|

Aircraft Interface Device Market Segmentation:

Application Segment Analysis

The commercial aviation segment in the aircraft interface device market is anticipated to garner the highest share of 70.8% by the end of 2035. The segment’s upliftment is highly driven by its importance for fueling worldwide economic growth, which supports various employment and revenue growth opportunities and acts as a primary catalyst for global connectivity, tourism, and trade. According to a data report published by the World Economic Forum in March 2025, airports play a critical role in the overall aviation industry that directly employs 11.6 million people globally. Besides, more than 100 member states have significantly adopted the ICAO Global Framework for lower-carbon aviation fuels, sustainable aviation fuels, and other cleaner energies, aiming to diminish carbon dioxide emissions in global aviation by 5% by the end of 2030 in comparison to zero cleaner energy utilization, thus driving the segment growth.

Aircraft Type Segment Analysis

During the forecast period, the fixed-wing segment, part of the aircraft type, is projected to hold the second-highest share in the aircraft interface device market. The segment’s growth is highly fueled by a diverse range of platforms, including commercial airliners, business jets, military transport aircraft, and special mission surveillance platforms. Additionally, this segment's leadership position is attributed to the sheer scale of the global fixed-wing fleet, which comprises tens of thousands of aircraft requiring interface solutions for cockpit modernization, fleet connectivity, and regulatory compliance. Besides, commercial aviation, in particular, drives substantial demand, with airlines increasingly adopting wireless AIDs to enable electronic flight bag integration, real-time aircraft health monitoring, and predictive maintenance capabilities that reduce operational disruptions and optimize fuel efficiency.

Platform Segment Analysis

The commercial aircraft sub-segment, which is part of the platform segment, is expected to account for the third-highest share in the aircraft interface device market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by the essential need for worldwide economic growth, readily supporting employment opportunities and transporting passengers. As per an article published by the IATA Organization in August 2025, the global commercial fleet comprises 35,550 aircraft, which includes 30,300 active units, along with 5,250 held in storage in June 2025. In addition, these aircraft represent 152 master series that are produced by 26 aircraft manufacturers globally. Besides, two manufacturers effectively account for 80% of the present active fleet, and the top five demonstrate nearly 95% of the overall aircraft in service, thus denoting an optimistic outlook for the sub-segment growth.

Our in-depth analysis of the aircraft interface device market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Aircraft Type |

|

|

Platform |

|

|

Connectivity |

|

|

Interface Type |

|

|

End use/Fit |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Aircraft Interface Device Market - Regional Analysis

North America Market Insights

North America in the aircraft interface device market is anticipated to garner the largest share of 42.6% by the end of 2035. The market’s upliftment in the region is primarily attributed to technological advancements, regulatory push by driving generous investments, and military modernization. Based on government estimates published by NASA in November 2023, over 873,000 Unmanned Aircraft Systems (UAS), also referred to as drones, have been registered to fly in the U.S. Additionally, with a host of different applications, such as the delivery of products, rescue, and search, along with agricultural monitoring, an increase in drone numbers is expected to the upcoming years. Besides, the National Airspace System (NAS) is undergoing to make flying safe, predictable, and efficient. Moreover, the NAS is made up of over 29 million square miles, which includes airport and landing areas, air navigation facilities, and airspace, thus driving the market growth.

The aircraft interface device market in the U.S. is growing significantly, owing to a combination of fleet modernization, the presence of a mature aviation ecosystem, regulatory mandates, and the presence of a strict regulatory framework, which is readily enforced by the Federal Aviation Administration for offering compliance with communication and safety protocols. As per a data report published by the Federal Aviation Administration in 2024, the country has more than 5,000 publicly utilized airports that support over 7,000 air transport and 200,000 general aviation aircraft, effectively performing over 52 million airport operations. Besides, in terms of civil aviation as of 2022, domestic air carriers significantly transported 853 million passengers with more than 948 billion revenue passenger miles. Meanwhile, over 32 billion revenue ton-miles of freight have been passed through the country’s airports, with civil commercial aircraft manufacturing accounting for an overall output of USD 57 billion and commercial airline operations supporting USD 363 billion of visitor spending on goods and services, thus fueling the market.

The presence of strong aerospace manufacturing, increased investment in connected aircraft technologies, a surge in demand from both military and commercial aviation industries, and proactive collaboration with OEMs for developing advanced avionics systems are certain factors responsible for bolstering the aircraft interface device market in Canada. As stated in an article published by Innovation, Science, Economic Development Canada in August 2025, the aerospace industry in the country generously contributed USD 34.2 billion to GDP, along with 225,000 employment opportunities to the economy. Of the overall GDP contribution, USD 26.9 billion has been provided to the aerospace industrial value chain, USD 15.6 billion for the total industry development, and USD 11.3 billion for domestic suppliers to the industry. Besides, of the total employment, 174,300 are entrusted to the value chain, 92,500 to the overall industry, and 81,800 to suppliers, thus proliferating the market expansion.

Canada-Based Aerospace Industrial Direct Employment Index Analysis (2019-2024)

|

Year |

Aerospace Manufacturing |

Aerospace MRO |

|

2019 |

60,000 |

32,700 |

|

2020 |

57,500 |

26,400 |

|

2021 |

54,400 |

25,600 |

|

2022 |

56,200 |

29,400 |

|

2023 |

56,600 |

32,300 |

|

2024 |

57,700 |

34,800 |

Source: Innovation, Science, Economic Development Canada

Europe Market Insights

Europe in the aircraft interface device market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by an increase in the need for innovative connectivity solutions across military and commercial aviation platforms, with active investments in next-generation cockpit interface technologies. According to official statistics published by Surfeo Europe in 2026, the aviation industry in the region is continuously rising from USD 2.2 billion to USD 2.6 billion, or 3.5%, as of 2025, with Airbus expected to deliver 22,000 helicopters by the end of 2036, as well as 37,400 aircraft projected within 20 years. Besides, a consortium between Rolls-Royce, MBDA, and Leonardo resulted in a project for replacing Eurofighter Typhoon with a generous budget of USD 2.6 billion in 2025, thereby making it suitable for boosting the market development.

The aircraft interface device market in Germany is gaining increased traction, owing to the existence of a massive aerospace manufacturing facility, an innovative industrial base, the presence of aerospace suppliers, along with a dense network of avionics component manufacturers. Based on government estimates published by the ITA in August 2025, the 2024 U.S.-based aerospace exports to the country amounted to USD 3.3 billion, while the trade surplus was worth USD 1.1 billion, accounting for a 39% in comparison to USD 1.9 billion as of 2023. Besides, defense and aerospace in the country are readily complemented by security and safety, denoting an industry spanning across 15 vertical markets with a worldwide turnover of USD 154.5 billion in 2025. Moreover, the overall air passenger traffic in the country amounted to 18.6 million, denoting a rise by 6.8% in comparison to April 2024, thus boosting the aircraft interface device market development.

German Industrial Size Analysis for Aerospace and Defense (2022-2025)

|

Components |

2022 (USD Million) |

2023 (USD Million) |

2024 (USD Million) |

2025 (USD Million) |

|

Localized Production |

41,067 |

49,740 |

56,285 |

61,914 |

|

Total Exports |

29,979 |

33,326 |

37,711 |

41,482 |

|

Total Imports |

19,712 |

23,875 |

27,017 |

29,719 |

|

Total Industry Size |

30,800 |

40,289 |

45,591 |

50,150 |

|

Imports from the U.S. |

8,349 |

9,481 |

3,323 |

3,655 |

|

EUR-USD Exchange Rate |

1,05 |

1.08 |

1.82 |

1.086 |

Source: ITA

The significant investments in aviation modernization, suitable growth in the aerospace manufacturing industry, strong government support for industrial innovation, notable defense and aerospace organizations, and proactively integrating innovative interface technologies into its military and commercial aircraft platforms are certain trends that are proliferating the aircraft interface device market in Italy. As per a data report published by the International Civil Aviation Organization in 2024, sustainable aviation fuel (SAF) has the capability to reduce greenhouse gas emissions by 80% on average, and the available SAF in the domestic market covers less than 2% of the overall demand. Moreover, the SAF projection in the country is projected to cater to 70% of the aviation industry by the end of 2050, thereby denoting a huge growth opportunity for the market.

APAC Market Insights

The Asia Pacific in the aircraft interface device market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by the rapid expansion in fleet, an increase in the air passenger traffic, substantial investments in aviation infrastructure modernization, and government-funded initiatives supporting both aviation and commercial expansion, as well as defense modernization programs. According to official statistics published by the IATA Organization in January 2026, the overall passenger demand accounted for a 5.7% increase in terms of revenue passenger kilometers in November 2024. Besides, the total capacity, measured in available seat kilometers, also increased by 5.4% year-on-year (YoY), while the load factor was 83.7%, thereby making it suitable for uplifting the market in the overall region.

The aircraft interface device market in China is gaining increased exposure, owing to the expansion of the commercial aviation industry, growth in fleet, and the Made in China 2025 industrial policy, which effectively prioritizes domestic avionics manufacturing. As stated in an article published by the State Council Information Office in February 2026, the country’s civil transport airports significantly handled almost .5 billion passenger trips in 025, denoting a 4.8% increase YoY. Additionally, mail and cargo throughput surged by 9% to 21.8 million tons, and meanwhile, aircraft landings and takeoffs totaled nearly 12.4 million, demonstrating a rise by 0.4% from the previous year. Moreover, by the end of 2025, the country comprised 270 certified transport airports, with 266 providing regular flight services, thus fueling the aircraft interface device market exposure.

The aspects of the regional connectivity scheme operating include increased air routes, expansion in the commercial fleet, growth in the commercial aircraft fleet, and the government designating electronic chemicals, such as semiconductor-grade materials are certain trends that are bolstering the aircraft interface device market in India. As stated in an article published by the PIB Government in October 2025, the UDAN scheme has revolutionized regional connectivity, with 15 million passengers and 320,000 flights. Besides, the government’s vision is to increase the number of airports from 350 to 400 by the end of 2047, while the overall country’s aviation industry significantly supports more than 7.7 million jobs. Therefore, with all such developments in the aviation industry, the market in the country is continuously revolutionizing and expanding.

Key Aircraft Interface Device Market Players:

- Collins Aerospace (RTX) (U.S.)

- Teledyne Controls (Teledyne Technologies) (U.S.)

- Astronics Corporation (U.S.)

- Boeing (U.S.)

- Honeywell International Inc. (U.S.)

- GE Aerospace (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Esterline Technologies Corporation (U.S.)

- MicroMax Computer Intelligence, Inc. (U.S.)

- Navaero Inc. (U.S.)

- Thales Group (France)

- Safran S.A. (France)

- Airbus SE (Netherlands)

- Elbit Systems Ltd. (Israel)

- Hindustan Aeronautics Limited (HAL) (India)

- Arconics (Ireland)

- Korea Aerospace Industries (KAI) (South Korea)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- AvionTEq (U.S.)

- Trax (U.S.)

- Rolls-Royce (UK)

- Nextant Aerospace (U.S.)

- Shadin Avionics (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Collins Aerospace (RTX) is a premier provider of advanced aircraft interface systems, delivering integrated solutions that bridge cockpit avionics with modern flight operations. The company focuses on developing secure, high-reliability interface devices that support both commercial aviation and defense mission requirements.

- Teledyne Controls (Teledyne Technologies) specializes in aircraft data management and interface solutions that enable real-time connectivity between aircraft systems and ground operations. The company's portfolio emphasizes ruggedized, certified products designed for reliable performance in demanding aerospace environments.

- Astronics Corporation designs and manufactures advanced interface technologies that enhance cockpit efficiency and aircraft connectivity. The company serves both commercial airline and military aviation customers with a focus on innovative, high-performance interface solutions.

- Boeing integrates aircraft interface devices as part of its comprehensive avionics and cockpit systems across its commercial and defense aircraft platforms. The company leverages its original equipment manufacturer position to develop seamlessly integrated interface solutions that meet stringent safety and certification standards.

- Honeywell International Inc. delivers advanced aircraft interface technologies that enable seamless data integration between flight decks, onboard systems, and ground operations. The company focuses on developing scalable, certifiable solutions that support fleet modernization and operational efficiency.

Here is a list of key players operating in the global aircraft interface device market:

The aircraft interface device market is highly consolidated, dominated by U.S.-headquartered aerospace giants such as Collins Aerospace (RTX), Teledyne Controls, and Astronics Corporation, which collectively hold a significant share of the global revenue. The competitive landscape is defined by a focus on wireless connectivity and modular open systems, as key players shift from hardware-centric models to integrated data solutions. Moreover, strategic initiatives center on developing dual-use platforms that serve both commercial and military aviation. Besides, in March 2024, AvionTEq and Flight Data Systems entered into a multi-year partnership to prepare the Aircraft Electronics Association for gathering technicians, distributors, business leaders, and manufacturers on a collaborative platform, thus fueling the aircraft interface device industry globally.

Corporate Landscape of the Aircraft Interface Device Market:

Recent Developments

- In April 2025, Trax and Rolls-Royce launched a seamless interface between Trax’s eMRO application and Rolls-Royce’s Blue Data Thread platform. This particular collaboration denotes a suitable advancement in integrating maintenance, repair, and overhaul operations with real-time data analytics, while enhancing reliability and efficiency for airlines globally.

- In November 2024, Nextant Aerospace achieved the FAA certification for Bombardier Global 5,000/5,500 Starlink Inflight Connectivity Kit, which can be readily installed through Starlink Authorized Dealers to rapidly expand the portfolio of approved certifications of popular large-scale cabin business jets, such as the Bombardier Global 7500, Global 6500/6000, Global Express, Global Express XRS, Gulfstream G650, G550, G450, and GIV aircraft.

- In February 2024, Shadin Avionics unveiled the newest iteration of the DARALT Series of Radar Altimeter Converters, effectively enabling new radar altimeters to be installed in different kinds of fixed-wing and rotor aircraft.

- Report ID: 8463

- Published Date: Mar 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.