Agrochemicals Market Outlook:

Agrochemicals Market size is poised to grow from a valuation of USD 299.8 billion in 2025 to USD 502.2 billion by 2035, representing a compound annual growth rate of 5.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of agrochemicals is assessed at USD 317.5 billion.

The global agrochemicals market is all set to witness a steady expansion, fueled by the intensifying need to enhance crop yields on limited arable land. Government support across different nations for localized, efficient farming is positioning the industry toward a long-term growth trajectory. In March 2024, the U.S. Department of Agriculture (USDA) announced that it made a total investment of USD 124 million in renewable energy and fertilizer production projects across 44 states under the Inflation Reduction Act, with a prime focus to lower energy costs and creating new revenue streams for farmers and rural businesses. Funding through the Rural Energy for America Program and Fertilizer Production Expansion Program supports over 541 clean energy projects and 42 domestic fertilizer facilities, enhancing production capacity and efficiency, hence increasing the growth potential for the agrochemicals market.

Furthermore, there has been a shift towards sustainable agriculture influenced by an increased focus on bio-based alternatives, eco-friendly fertilizers, and precision farming technologies that effectively minimize environmental impact. In March 2023, India’s Standing Committee on Chemicals and Fertilizers reported that the development and promotion of nano-fertilizers, such as nano urea, improves crop productivity, reducing environmental impact and lowering input costs. Moreover, the field trials showed up to 8% higher yields and cost savings when compared to conventional fertilizers, with the higher potential to reduce urea imports and subsidies. In addition, it also recommends increased funding, commercial deployment, and support for drone-based applications to accelerate the adoption of nano-fertilizer technologies, hence benefiting the agrochemicals market growth.

Global Insecticide Exports 2023: Top 10 Countries by Retail Shipment Value and Volume

|

Country / Region |

Export Value (USD 1,000) |

Quantity (Kg) |

|

China |

1,955,652.75 |

467,238,000 |

|

European Union |

1,706,746.98 |

71,383,300 |

|

U.S. |

1,644,628.30 |

59,066,500 |

|

India |

1,546,883.83 |

164,454,000 |

|

France |

897,079.31 |

32,487,900 |

|

Germany |

730,880.71 |

23,672,700 |

|

Spain |

533,910.54 |

51,052,500 |

|

Korea, Rep. |

396,836.76 |

12,108,500 |

|

Japan |

363,449.56 |

11,141,800 |

|

Singapore |

341,985.66 |

8,432,200 |

Source: WITS

Key Agrochemicals Market Insights Summary:

Regional Highlights:

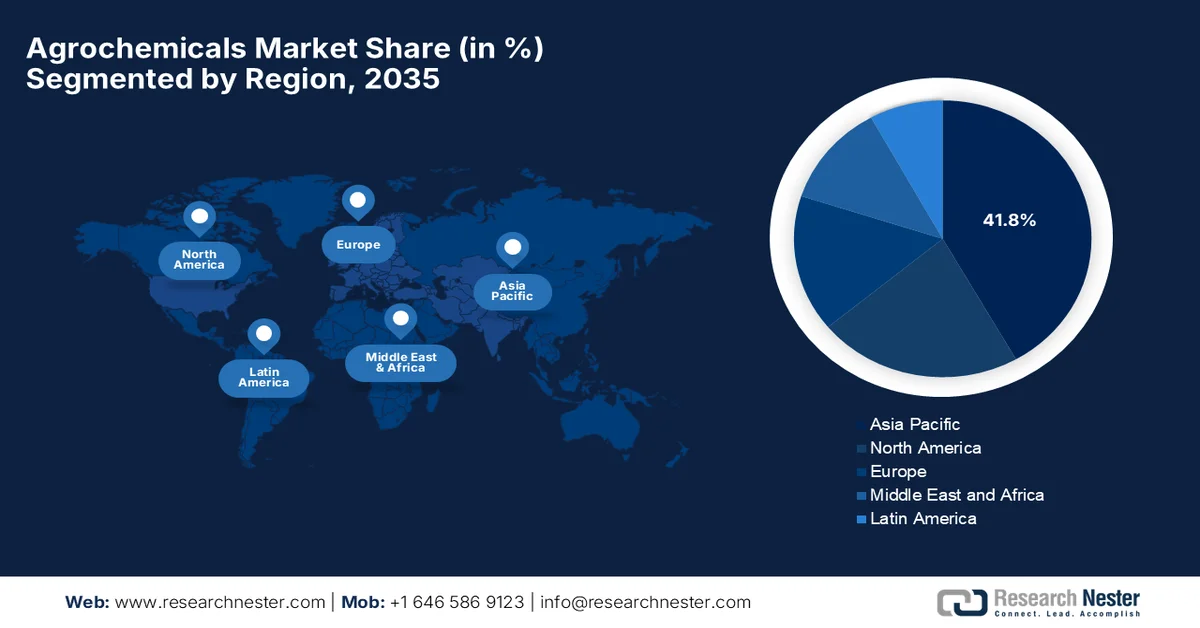

- Asia Pacific is expected to capture a 41.8% share of the agrochemicals market by 2035, propelled by expanding agricultural land and increasing adoption of sustainable farming techniques.

- North America is projected to retain a notable share of the market by 2035, supported by favorable regulatory frameworks encouraging development and adoption of advanced agrochemical formulations.

Segment Insights:

- Fertilizers segment is projected to command a 68.7% share of the agrochemicals market by 2035, driven by their critical role in crop nutrition and yield enhancement across staple and high-value crops.

- Cereals and grains segment is anticipated to witness a considerable share of the market by 2035, fueled by extensive cereal farming systems and rising demand for effective weed resistance management solutions.

Key Growth Trends:

- Rising global population & food demand

- Shrinking arable land

Major Challenges:

- Stringent regulatory frameworks

- Rising demand for organic farming

Key Players: Syngenta AG, Bayer Crop Science, BASF SE, Corteva Inc., FMC Corporation, UPL Limited, Insecticides India Limited (IIL), ADAMA Agricultural Solutions, Sumitomo Chemical Co., Ltd., Nufarm Ltd., Jiangsu Yangnong Chemical Co., Ltd., Rainbow Agro, Fertiglobe plc, Lianyungang Liben Crop Science, Wynca Chemicals, Lier Chemical Co., Ltd., Hubei Xingfa Chemicals, Nutrichem Company Limited, Fuhua Tongda Agrochemical Technology Co., Zhejiang Zhongshan Chemical Co., Ltd., Cheminova (FMC subsidiary), PI Industries Ltd..

Global Agrochemicals Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 299.8 billion

- 2026 Market Size: USD 317.5 billion

- Projected Market Size: USD 502.2 billion by 2035

- Growth Forecasts: 5.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.8% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, India, Brazil, Germany

- Emerging Countries: Vietnam, Thailand, Indonesia, Mexico, Turkey

Last updated on : 9 March, 2026

Agrochemicals Market - Growth Drivers and Challenges

Growth Drivers

- Rising global population & food demand: This rising population and the heightened demand for higher agricultural productivity are the major driving factors for the agrochemicals market. This pushes farmers to adopt agrochemicals to boost yields and ensure food security. According to the official statistics published by the USDA’s Economic Research Service in June 2024, the worldwide food consumption is projected to rise sharply by the end of 2050 as population growth and rising incomes drive demand for more calories. It also notes that low-income economies still spend about 40% of their budgets on food, whereas high-income economies spend around 10%, which is due to affordability differences. By 2050, crop calorie production will need to increase nearly 50% to 60% to meet demand, with diets shifting toward more oils, meat, and dairy, hence increasing the demand for agrochemicals to increase production.

- Shrinking arable land: The rising urbanization and industrialization are reducing the amount of available farmland, shrinking arable land across the world. This loss of cultivable area is consistently pushing farmers to produce more on smaller plots. As a result, many turn to agrochemicals to maximize crop yields per hectare. As stated by the Food and Agriculture Organization (FAO) in 2025, urban expansion and unsustainable land-use practices have degraded more than 1.6 billion hectares of land, with more than 60% of this on agricultural lands, shrinking arable areas. Therefore, farmers face increased pressure to boost production on smaller plots, which in turn drives greater demand for products such as pesticides, herbicides, and fertilizers in the agrochemicals market.

Global Pesticides Use and Trade in 2023: FAOSTAT Official Statistics on Consumption, Exports, and Regional Insights

|

Indicator |

2023 Value |

|

Total pesticide use (active ingredients) |

3.73 million tonnes (Mt) |

|

Pesticide use per cropland area |

2.40 kg/ha |

|

Total pesticides exports (formulated products) |

6.7 Mt |

|

Total export value |

USD 42.8 billion |

|

Top importing region |

Americas: 1.97 Mt |

|

Top exporting region |

Asia: 2.4 Mt |

|

Africa |

Mostly imports from outside the region. |

|

Europe - use per hectare |

1.59 kg/ha |

|

Europe - use per person |

0.65 kg/cap |

|

Oceania - use per hectare |

5.64 kg/ha |

|

Oceania - use per person |

2.44 kg/cap |

|

Azole-based antimicrobial fungicides |

9% of total fungicides & bactericides |

Source: FAO

- Technological innovation & advanced formulations: Both the public and private entities are mostly focused on innovations in terms of formulation, such as controlled-release fertilizers, nano-formulations, and modern biopesticides. These are known to improve efficiency and lower environmental impacts, wherein integration with precision agriculture technologies enhances the overall targeted application and reduces waste. As per the article published by the U.S. Government Accountability Office (GAO) in January 2024, it has analyzed precision agriculture, which uses technologies, i.e., GPS, drones, sensors, and automation to optimize farming efficiency. It notes that these technologies can increase profits, reduce input use, and provide environmental benefits. The report also underscored that federal support programs, research investments, and policy options encourage adoption, innovation, and hence increase the growth potential of the agrochemicals market.

Challenges

- Stringent regulatory frameworks: The agrochemicals market faces severe challenges in terms of regulatory scrutiny across different nations. Both the governments and regulatory bodies are imposing strict guidelines on pesticide approval, usage limits, residue levels, and environmental impact. In this context, obtaining product registration is time-consuming and expensive, which can also take many years of toxicology and environmental testing. On the other hand, the aspect of policy changes and bans on a few active ingredients results in uncertainty for manufacturers. Therefore, to address these challenges, companies need to make investments in compliance, documentation, and reformulation, which raises operational costs. Also, smaller players, particularly, struggle with these regulatory burdens, leading to market consolidation.

- Rising demand for organic farming: There has been a major shift towards organic farming, which poses a structural challenge to the agrochemicals market. Consumers across the globe are opting for chemical-free food products owing to health and environmental concerns. Besides, retailers and governments are supporting organic certification programs by reducing reliance on synthetic fertilizers and pesticides. As organic farming expands, demand for agrochemicals declines in certain regions. Therefore, this shift forces companies to diversify into bio-based pesticides, biofertilizers, and integrated pest management solutions, in turn necessitating new expertise and research capabilities. Furthermore, the established chemical manufacturers need to compete with biological input companies, which may cause disruptions to traditional agrochemicals market dominance and profit margins.

Agrochemicals Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.9% |

|

Base Year Market Size (2025) |

USD 299.8 billion |

|

Forecast Year Market Size (2035) |

USD 502.2 billion |

|

Regional Scope |

|

Agrochemicals Market Segmentation:

Product Type Segment Analysis

The fertilizers, which are a part of the product type segment is anticipated to lead with the largest revenue share of 68.7% in the agrochemicals market by the end of the forecast duration. Their importance in crop nutrition and yield enhancement across staple and high-value crops is the main fueling factor behind this leadership. In 2023, the government of India approved the market development assistance scheme under the GOBARdhan initiative to promote organic fertilizers by providing USD 16.4 per MT and allocating a total outlay of USD 159.5 million for the financial year 2023‑24 to 2025‑26, which also includes USD 39.56 million for research funding. The program integrates multiple schemes such as SATAT, Waste to Energy, and Swachh Bharat Mission with a collective goal to support biogas and biofertilizer production. In addition, the Ministry of Chemicals and Fertilizers is improving the innovations, including green ammonia, nano‑fertilizers, drone-based application, and drafting new legislation to regulate fertilizer production, quality, distribution, and pricing.

Crop Type Segment Analysis

The cereals and grains are expected to grow with a considerable share in the agrochemicals market. The growth of the subtype is highly attributable to large-scale cereal and row crop farming systems, where weed competition significantly impacts yields. Weed resistance management and conservation tillage practices are also driving the adoption of herbicides across both established and emerging economies. In June 2025, Syngenta announced a major innovation with metproxybicyclone, which is a new fourth-generation ACCase inhibitor especially designed to control resistant grass weeds that are affecting cereals, soybeans, and other row crops. The herbicide addresses global challenges of weed competition and resistance, which impact yields and crop sustainability, and is expected to launch in Argentina in 2026, pending regulatory approvals. Hence, with such continued developments, the market is set to witness unprecedented growth in the years ahead.

India Cereal Production and Major Export Destinations 2024-25: Rice, Wheat, Maize & Bajra Statistics

|

Aspect |

Details (2024-25) |

|

India’s global rank in cereal production |

2nd largest producer |

|

Cereal production share |

Rice: 25.79% |

|

Wheat: 13.84% |

|

|

Maize: 3.07% |

|

|

Major cereals |

Wheat, Paddy (Rice), Sorghum, Millet (Bajra), Barley, Maize |

|

Production of major cereals (million tonnes) |

Rice: 150.18 |

|

Wheat: 117.95 |

|

|

Maize: 43.41 |

|

|

Bajra: 11.21 |

|

|

Total cereals production |

332.05 million tonnes |

|

Major export destinations |

Saudi Arabia, Benin, Iraq, Iran, Guinea, Cote D’Ivoire |

Source: APEDA

Formulation Segment Analysis

The liquid subtype is predicted to grow with a considerable share in the agrochemicals market during the stipulated timeframe. The growth of the subtype is highly propelled by aspects such as ease of application, uniform distribution, and faster absorption by crops, which enhances operational efficiency for farmers. Besides, liquid-type formulations are highly suitable for large-scale cereal, row crop, and high-value crop systems, wherein the precise nutrient delivery and effective pest control are needed for maintaining consistent yields. In addition, the liquid agrochemicals facilitate integration with technologies such as fertigation systems and drone-based spraying, thereby enabling necessary input use, reduced wastage, and better environmental compliance. Furthermore, the convenience and adaptability across crop types efficiently fuel the sustained growth of the liquid formulation sub-segment.

Our in-depth analysis of the agrochemicals market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Crop Type |

|

|

Formulation |

|

|

Fertilizer Type |

|

|

Crop Protection Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Agrochemicals Market - Regional Analysis

APAC Market Insights

The Asia Pacific agrochemicals market is projected to hold the largest revenue share of 41.8% during the discussed timeframe. The region’s upliftment is mainly attributable to the expansion of agricultural land and the growing adoption of sustainable farming techniques. The rising pest pressures, high demand for herbicides and insecticides, also prompt a favorable business environment for players operating in the region. In March 2024, the governments of Ecuador, India, Kenya, Laos, the Philippines, Uruguay, and Vietnam launched the FARM programme, with a total investment of USD 379 million. The initiative is led by the UN Environment Programme (UNEP) with support from the Global Environment Facility (GEF and is aimed at reducing pollution from pesticides and agricultural plastics. The programme addresses the environmental and health risks of highly hazardous agrochemicals and mismanaged plastics, promoting safer, low-chemical alternatives, creating demand for innovative, sustainable crop protection products.

The strategic policies that support self-sufficiency in certain staple crops are responsible for uplifting the agrochemicals market in China. The demand profile reflects extensive use across paddy, wheat, and vegetables. Based on the government data, which was published in February 2025, the country’s No. 1 central document has reaffirmed the government’s dedication to grain security, mainly prioritizing self-sufficiency by increasing per-unit yields of grain and oil crops and enhancing disaster resilience. It also stated that by the end of 2024, China had developed more than 66.7 million hectares of high-standard farmland and built irrigation networks stretching over 10 million kilometers, thereby supporting successive bumper harvests. In 2024, the country achieved a record grain output of 706.5 million tonnes, which is a 1.6% increase from 2023, denoting a lucrative growth potential for the agrochemicals industry in the country.

The agrochemicals market in India supports the extensive cropping intensity and multiple growing seasons, wherein farmers are dependent on a variety of protective and plant nutrition products. Besides the government agricultural extension programs, market infrastructure improvements also contribute to the increased availability and utilization of these crop inputs. In this context Farmer's Welfare through Press Information Bureau (PIB) in August 2025 reported that the country’s Amrit Kaal fertilizer strategy focuses on self-reliance, sustainability, and technological innovation to empower farmers. It also states that between 2018 and 2025, six new urea plants were commissioned, which added 76.2 LMT to domestic capacity, helping India achieve its highest-ever urea production of 314 LMT in 2023-24. In addition, the long-term agreements with Saudi Arabia, Bhutan, Nepal, and Sri Lanka are focused on stable fertilizer supplies, supporting both domestic production and strategic imports, hence denoting a positive market outlook.

India Fertilizer Production & Usage Statistics 2023-25: Nano, Urea, and Global Supply Insights

|

Parameter |

Value |

|

Total Fertilizer Production (2023-24) |

503.35 LMT |

|

Domestic Urea Production (2023-24) |

314 LMT |

|

Total Fertilizer Consumption (2023-24) |

601 LMT |

|

Budget Allocation for Department of Fertilizers (2024-25) |

USD 23.9 billion |

|

Nano/Neem Fertilizer Promotion |

Ongoing in 100+ districts, 15 agro-climatic zones |

|

DAP Supply from Saudi Arabia (2025-26) |

3.1 million MT annually |

Source: PIB

North America Market Insights

The supportive regulatory frameworks that encourage the development and adoption of new formulation drives consistent revenue for the agrochemicals market in North America. These safely formulated products support intensive row crop cultivation and high-yield agricultural systems, wherein farmers are leveraging targeted crop protection and nutrient solutions to safeguard staple commodities. In February 2026, as stated by the White House government, the U.S. president issued an order to make sure that the country maintains an optimum supply of elemental phosphorus and glyphosate-based herbicides, which are essential for both national defense and agricultural productivity. The order highlights glyphosate’s importance in maintaining high crop yields and food security, and it delegates authority to the Secretary of Agriculture to prioritize production, allocation, and regulations to boost the domestic supply and national security.

The U.S. agrochemicals market is characterized by a strong focus on innovation in active ingredients and formulations, which are suited to major crops such as corn, soybeans, and cotton. The primary focus on pest management solutions to address crop loss concerns also accelerates the use of agrochemicals in the country. The Agricultural Research Service USDA in 2023 revealed that more than a quarter-billion acres of the country’s agricultural production were valued at more than USD 115 billion. Besides, the program includes cultural, biological, physical, and chemical methods, addressing challenges such as pest resistance, regulatory changes, and invasive species threats. Its research is highly focused on sustainable, environmentally safe practices to enhance crop productivity, protect natural ecosystems, and reduce economic losses, including USD 2.5 billion in postharvest losses for corn and wheat, hence denoting a positive outlook for the agrochemicals market’s growth and exposure.

Strategic shift toward increased productivity and the integration of precision agriculture technologies are certain drivers responsible for uplifting the agrochemicals market in Canada. The logistics and supply chain considerations ensure products are suitable for broader grain and oilseed farming systems across prairie provinces in the country. In February 2026 country’s government reported that it had launched two new Market Diversification streams under the AgriMarketing Program, by investing a total amount of USD 75 million over five years to help farmers, processors, and exporters access new global markets and strengthen interprovincial trade. The initiative targets all agricultural sectors, and it has a higher priority for industries that are affected by trade barriers. From a strategic perspective, such government backing in the country boosts the market growth by increasing the adoption of crop protection solutions and expanding the demand for agrochemicals.

Europe Market Insights

Europe agrochemicals market maintains a strong position in the global landscape, propelled by stringent regulatory oversight and a growing orientation toward sustainability. This, in turn, prompts the sector to prioritize formulations that are compatible with integrated farming practices and have lower environmental effects. In this context European Commission in December 2025 revealed that its Member States approved a draft regulation to revise pesticide labelling, updating rules from 2011 to provide clearer guidance on safe handling, disposal, hazard indications, and risk mitigation for human, animal, and environmental health. The regulation allows Member States to adapt labels to local agro-environmental conditions and introduces digital labelling for easier access to information, hence making it suitable for standard market growth.

The agrochemicals market in Germany benefits from a long history of chemical research and improved agricultural technologies, with supply chains focused on both domestic crop protection needs and export sectors. The country’s market is currently making a profound structural evolution by shifting away from traditional chemical-intensive practices toward a high-tech, bio-based future. In this context, Kwizda Agro in January 2025, notified that it has launched the plant protection products called Botector, Blossom Protect, and Weintec, which are suitable for both organic and conventional growers. These products provide sustainable alternatives to synthetic pesticides by helping to comply with stricter environmental regulations. Hence, with such conscious developments from the country’s pioneers, the market is all set to witness tremendous growth in the upcoming years.

The need to manage both arable and horticultural systems, with a strong emphasis on aligning product use with environmental regulations, is the major fueling factor for the agrochemicals market in the UK. The government initiatives and research collaborations promote responsible application methods that help manage pest pressure in the country. Based on the government data, which was published in October 2025, the country’s pesticides national action plan 2025 was focused on sustainable crop protection by promoting integrated pest management by setting clear reduction targets, and strengthening compliance. It highlights the aim to cut pesticide risk indicators by 10% by 2030, and supports innovation and precision farming. This particular plan balances environmental sustainability with the need for effective crop protection, thereby denoting a huge growth opportunity for the agrochemicals market in the country.

Key Agrochemicals Market Players:

- Syngenta AG (Switzerland)

- Bayer Crop Science (Germany)

- BASF SE (Germany)

- Corteva, Inc. (U.S.)

- FMC Corporation (U.S.)

- UPL Limited (India)

- Insecticides (India) Limited (IIL) (India)

- ADAMA Agricultural Solutions (Israel)

- Sumitomo Chemical Co., Ltd. (Japan)

- Nufarm Ltd. (Australia)

- Jiangsu Yangnong Chemical Co., Ltd. (China)

- Rainbow Agro (China)

- Fertiglobe plc (UAE)

- Lianyungang Liben Crop Science (China)

- Wynca Chemicals (China)

- Lier Chemical Co., Ltd. (China)

- Hubei Xingfa Chemicals (China)

- Nutrichem Company Limited (China)

- Fuhua Tongda Agrochemical Technology Co. (China)

- Zhejiang Zhongshan Chemical Co., Ltd. (China)

- Cheminova (FMC subsidiary) (Denmark)

- PI Industries Ltd. (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Syngenta AG is a leading player in the Asia Pacific and Latin America, where it offers suitable products for local crop conditions. The company has pioneered in terms of digital farming platforms that integrate weather data, soil analytics, and crop protection recommendations.

- Bayer Crop Science is a prominent player that is best known for its vertical integration with seeds and traits. The company makes strong investments in climate-smart solutions, including nitrogen-use efficiency products and stress-tolerant seeds, by targeting environmental regulations in different economies.

- BASF SE is a central player in this field that has strong chemical manufacturing knowledge to produce agrochemicals with suitable formulations. In addition, the company is notable amongst other players due to the development of carbon-smart solutions such as urease inhibitors and other emission-reducing technologies.

- Corteva, Inc. is a multinational player that integrates biologicals with generally used chemical solutions by offering products that enhance soil health while controlling pests. Besides, the firm is mainly focused on farmer education and field-level demonstrations, thereby increasing the adoption of new technologies such as dual-mode fungicides.

- FMC Corporation is a well-recognized player for its specialty crop focus targeting high-value segments such as fruits, vegetables, and nuts. The company’s strategy mainly relies on rapid product innovation to address concerns as pest resistance, including the development of new classes of insecticides.

Below is the list of some prominent players operating in the global agrochemicals market:

The global agrochemicals market is dominated by multinational giants that benefit from strong R&D capabilities and portfolios of products, including herbicides, insecticides, fungicides, and biological solutions. Key players such as Syngenta AG, Bayer Crop Science, BASF SE, and Corteva, Inc. lead the market through innovation, acquisitions, and broad geographic reach to bolster product portfolios. Players from emerging nations are mainly focused on affordable manufacturing procedures and regional distribution. In October 2025, Fertiglobe, a leading player in terms of nitrogen fertilizers, reported that it had completed the acquisition of Wengfu Australia’s distribution assets by establishing Fertiglobe Australia Pty Ltd. to operate the network across five ports and eight warehouses. The move strengthens supply chain efficiency, hence contributing to a wider agrochemicals market expansion.

Corporate Landscape of the Agrochemicals Market:

Recent Developments

- In January 2026, Corteva Agriscience announced that it had launched Telbek PRO, which is the first Group 21 fungicide for cereals, especially designed to combat FU.S. rium Head Blight and late-season leaf diseases in Canada.

- In May 2025, Insecticides (India) Limited (IIL) reported that it has launched Altair, which is a patented pre-emergent herbicide for paddy developed by Nissan Chemical Corporation, Japan, and the product protects against tough weeds when applied shortly after transplanting.

- Report ID: 8419

- Published Date: Mar 09, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.