Aerospace Composites Market Outlook:

Aerospace Composites Market size was valued at USD 35.1 billion in 2025 and is projected to reach USD 95.7 billion by the end of 2035, rising at a CAGR of 11.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of aerospace composites is estimated at USD 39.2 billion.

The market is poised for extensive growth in the upcoming years as the aviation industry is seeking lightweight, high-strength materials to enhance fuel efficiency, performance, and sustainability. Ongoing research and development efforts are the main assets for this landscape, thereby boosting consistent revenue. In November 2023, the U.S. Department of Defense (DOE) allocated a total of USD 3.7 million to Qarbon Aerospace under the Industrial Base Analysis and Sustainment program (IBAS) to develop advanced lightweight continuous fiber thermoplastic composite structures for defense aviation. This investment supports the design and manufacture of components with improved efficiency, durability, and ease of repair, including structures with icing protection, hence denoting a lucrative opportunity for the market’s growth and exposure.

Furthermore, the mutually profitable collaborations between aerospace companies and material scientists are accelerating the integration of improved composites into new-generation aircraft, highlighting their essential role in shaping the future of aerospace engineering. In March 2023, NASA reported that its Hi-Rate Composite Aircraft Manufacturing project awarded a total amount of USD 50 million to 14 organizations, including Boeing, Spirit AeroSystems, and Northrop Grumman, to develop advanced composite materials and manufacturing processes for aircraft structures. Therefore, with these public-private partnerships under the Advanced Composites Consortium, HiCAM accelerates technology development, evaluation, and full-scale demonstration of fuselage and wing components, thereby enhancing both sustainability and benefiting the market.

Key Aerospace Composites Market Insights Summary:

Regional Highlights:

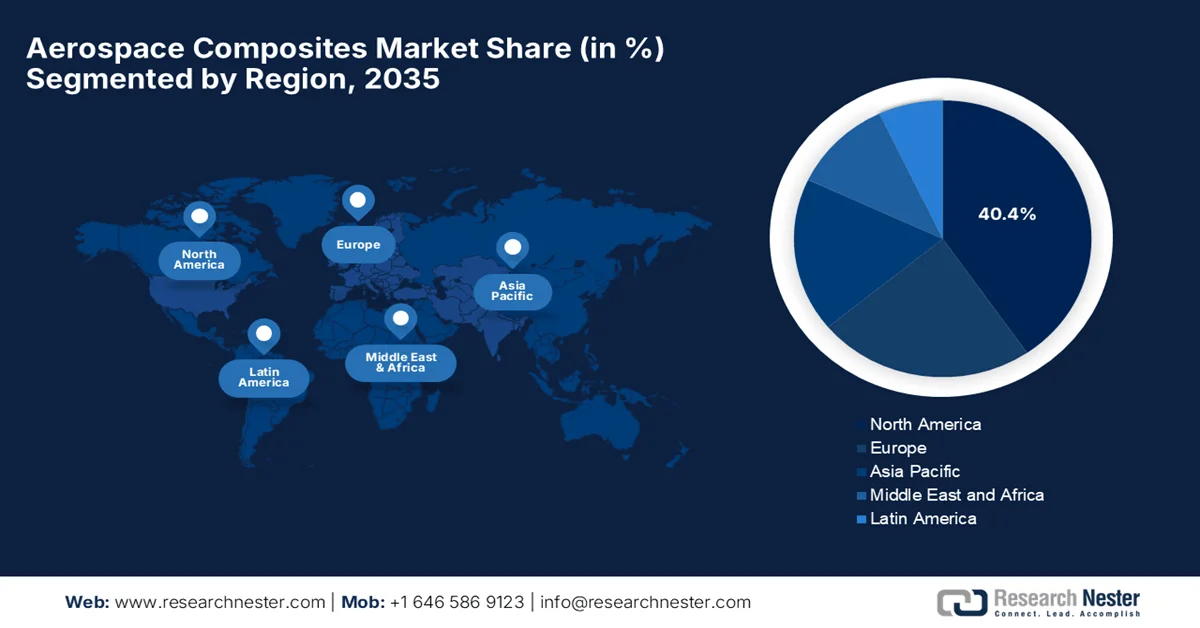

- The North America aerospace composites market is projected to command 40.4% share by 2035, impelled by well-established aerospace manufacturing infrastructure and supply chains

- Asia Pacific poised to register the fastest growth during 2026–2035, catalyzed by expanding aviation industries and increasing regional manufacturing capacities

Segment Insights:

- Carbon fiber composites sub-type is projected to account for 56.4% share by 2035 in the aerospace composites market, propelled by their outstanding strength-to-weight ratio and reliable performance in essential aerospace components

- Exterior components segment is expected to secure a considerable share by 2035, fueled by their ability to reduce aircraft weight while enhancing fuel efficiency and structural durability

Key Growth Trends:

- Weight reduction & fuel efficiency

- Emission control & sustainability initiatives

Major Challenges:

- Technical complexity in manufacturing

- Sustainability and recycling challenges

Key Players: Toray Industries, Inc., Hexcel Corporation, Solvay S.A., SGL Carbon SE, Teijin Limited, Mitsubishi Chemical Holdings Corporation, Owens Corning, Gurit Holding AG, Huntsman Corporation.

Global Aerospace Composites Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 35.1 billion

- 2026 Market Size: USD 39.2 billion

- Projected Market Size: USD 95.7 billion by 2035

- Growth Forecasts: 11.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, France, United Kingdom

- Emerging Countries: China, India, Japan, South Korea, Brazil

Last updated on : 25 February, 2026

Aerospace Composites Market - Growth Drivers and Challenges

Growth Drivers

- Weight reduction & fuel efficiency: Aerospace composites are low in weight when compared to aluminum, which in turn reduces fuel consumption and operating costs. These structures also improve aircraft range and payload efficiency, thereby driving huge adoption in the market. In this regard, in April 2023, the U.S. Department of Energy renewed funding for the Institute for Advanced Composites Manufacturing Innovation (IACMI), allocating a total amount of USD 6 million in the first year to advance composite research, commercialization, and domestic manufacturing. This investment will readily accelerate research on composites, which are durable and cost-effective when compared to traditional materials. Hence, such factors will boost the market growth by strengthening manufacturing capabilities and expanding the adoption of composites across aerospace applications.

- Emission control & sustainability initiatives: The worldwide aviation industry is mainly focused on achieving net-zero emissions, which is accelerating the use of these materials. In this context, composites contribute to long-term sustainability goals by readily enhancing aerodynamic efficiency and supporting propulsion technologies. In October 2025, as stated by the International Civil Aviation Organization, it has strengthened the global framework to achieve net-zero carbon emissions from the international aviation sector by 2050, wherein all of the Member States support environmental resolutions without reservations. Besides, the Assembly also recommends cleaner energy adoption by including sustainable aviation fuels and reinforcing the carbon offsetting and reduction scheme for international aviation to accelerate decarbonization efforts, benefiting the overall aerospace composites market.

- Rising global aircraft demand: The rebound in air passenger traffic, especially in the emerging nations, has led to significant aircraft order backlogs. In this context, major OEMs are increasing production rates of fuel-efficient aircraft, many of which incorporate high composite content in fuselage, wings, and structural components. According to the official statistics published by the IEA Organization in January 2025, the global commercial air passenger traffic rebounded to nearly 95% of pre-pandemic levels in 2023, driven largely by the Asia Pacific, where international travel demand surged more than 120% year-on-year following China’s reopening. It also notes that domestic aviation grew by 30%, whereas international flights expanded by more than 40%, reflecting a strong recovery in air travel, hence increasing the growth potential of the market.

Challenges

- Technical complexity in manufacturing: Aerospace composites manufacturing is quite a complex process, which needs special equipment and expert knowledge. Techniques such as automated fiber placement, resin transfer molding, and thermoplastic composite consolidation need proper temperature, pressure controls, and curing cycles to make sure consistent material performance. Any deviation can result in structural defects, reducing the safety and reliability of products in the aerospace composites market. In addition, integrating these composites into large aircraft structures often involves joining with metal components, which is challenging in bonding and thermal expansion. Therefore, this complexity increase may result in production delays, quality control issues, and even higher operational costs, making it challenging for smaller players.

- Sustainability and recycling challenges: The composites offer superior strength-to-weight ratios, but the concerns of environmental impact and recyclability are considerable obstacles hindering the market growth. Most aerospace-grade composites, especially thermoset-based materials, are difficult to recycle, and end-of-life aircraft generate more volumes of composite waste. In this context, the regulatory pressures and growing sustainability expectations from airlines and governments are pushing manufacturers to look for eco-friendly alternatives and closed-loop recycling systems. On the other hand, developing recyclable thermoplastic composites or chemical recycling methods requires substantial R&D investment and new manufacturing infrastructure, creating hurdles for the market’s expansion.

Aerospace Composites Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

11.8% |

|

Base Year Market Size (2025) |

USD 35.1 billion |

|

Forecast Year Market Size (2035) |

USD 95.7 billion |

|

Regional Scope |

|

Aerospace Composites Market Segmentation:

Fiber Type Segment Analysis

Carbon fiber composites sub-type is expected to lead the aerospace composites market, accounting for 56.4% share by 2035, due to their outstanding strength-to-weight ratio and reliable performance in essential aerospace components. For instance, in June 2024, Airbus announced that it had developed a proof-of-concept nose panel for the H145 PioneerLab helicopter by using bio-derived carbon fiber composites, which are made from sustainable acrylonitrile sourced from atmospheric CO₂ and other renewable feedstocks. This panel was flight-tested in May 2024, and it demonstrated performance equivalent to conventional composites with’ low-carbon material initiatives hence denoting a wider segment scope. Moreover, increasing investments in sustainable aviation technologies are further expected to accelerate the adoption of advanced carbon fiber composites across aerospace applications.

Application Segment Analysis

Exterior components are predicted to grow with a considerable share in the market over the forecasted years. The growth of the subtype is mainly due to its capability in covering critical elements such as wings, fuselage sections, and tail assemblies. The use of composites in these areas is mainly influenced by their ability to reduce overall aircraft weight, directly improving fuel efficiency and operational performance. Primary structural elements such as wing boxes and fuselage panels mainly benefit from the suitable strength properties of composites, which allow engineers to optimize load-bearing capabilities along specific directions. In addition, the inherent corrosion resistance of composite materials enhances durability and reduces maintenance requirements over the aircraft’s service life, hence supporting both commercial and defense sectors.

Manufacturing Process Segment Analysis

The lay-up is expected to lead the aerospace composites market with a significant share during the stipulated timeframe. It includes both manual and automated methods that enable the production of intricate geometries and prototypes. The laying technologies are also expanding at a rapid pace, since they are offering high precision, consistent quality, and greater production efficiency when compared to traditional methods. These automated approaches allow manufacturers to reduce material waste, improve repeatability, and accelerate production timelines for complex aerospace components. As a result, layup processes are being adopted for critical structures such as fuselage sections, wing skins, and other high-performance parts, solidifying their role as key enablers of improved composite manufacturing in modern aircraft production.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Fiber Type |

|

|

Application |

|

|

Manufacturing Process |

|

|

Matrix Type |

|

|

Aircraft Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Aerospace Composites Market - Regional Analysis

North America Market Insights

The North America aerospace composites market is forecasted to hold the largest share of 40.4% in the global industry by the end of 2035. The leadership of the region is mainly propelled by well-established aerospace manufacturing infrastructure and supply chains. The presence of major OEMs and manufacturers is promoting a favorable business ecosystem in the region. For instance, in January 2026, Continuous Composites reported that it received a total of USD 1.25 million contract through the AFWERX Manufacturing Challenge to advance next-generation joining and stiffening methods for aerospace structures using its CF3D digitally driven manufacturing process. CF3D enables automated, scalable production of continuous fiber composites, and it supports the Department of the Air Force’s goal of accelerating innovative manufacturing technologies for lighter aerospace and defense platforms, hence positively impacting market growth.

The burgeoning investments in low-weight structural innovations for both commercial and military aircraft drive adoption in the U.S. aerospace composites market, including hybrid and multifunctional materials. Federal laboratories and military R&D programs in the country are allocating significant funding grants, encouraging more players to establish their footprint in the country. In October 2023, as stated by the U.S. Economic Development Association, the Department of Commerce has designated the American Aerospace Materials Manufacturing Tech Hub in Spokane, Washington, as one of the inaugural 31 Tech Hubs under the CHIPS and Science Act. It was led by Gonzaga University, and the hub will develop high-rate thermoplastic composite manufacturing for lightweight aircraft, leveraging regional research institutions, aerospace suppliers, and workforce expertise, denoting a positive market outlook.

A strong regional cluster of suppliers and academic partnerships, which has an emphasis on extreme weather performance, is the main driver boosting Canada market. Materials are being developed to remain strong in terms of harsh cold climates and high-altitude operations, supporting both commercial and specialized aerospace platforms, including surveillance aircraft and regional jets. In February 2026, the country’s Economic Development for Quebec Regions announced support for 28 projects in Quebec’s defense sector. In this, the Composites Development Center of Quebec (Cégep de Saint-Jérôme) in Laurentides received a total amount of USD 400,000 in non-repayable funding to enhance its equipment and infrastructure. The project mainly aims to strengthen the center’s capabilities in supporting businesses with innovation and technology transfer in the composites sector.

APAC Market Insights

The Asia Pacific aerospace composites market is expected to record the fastest growth rate from 2026 to 2035. The region’s growth is highly attributable to expanding aviation industries and increasing manufacturing capacities across China, Japan, India, and Australia. Governments in this region are strengthening in-country production of advanced composite components through supportive initiatives, thereby increasing the region’s self-reliance in aircraft materials. The Japan Science and Technology Agency managed the Critical Technology Development Program for Economic Security for the financial year 2025, which supports aerospace materials research focused on innovative adhesion technologies for composite materials. This program mainly aims to advance elemental technologies that contribute to the establishment of robust composite adhesion methods, enhancing Japan’s aerospace materials capabilities. The funding was available up to 300 million JPY (approximately USD 2.1 million) for more than five years.

The government-backed commercial and military aerospace programs are driving strong demand in the aerospace composites market in China, thereby bolstering local supply chains. The aspects such as rapid industrialization of production lines and the integration of advanced automation for large-scale airframe structures are also propelling the growth of the country’s market. Based on the government data, which was published in December 2025, the Shenyang Aviation and Aerospace City completed the core structures of the Shenyang Aircraft's new factory, with full-scale production of aerospace components, which also includes composite materials. The Shenyang Aircraft composite materials project will significantly increase the local supply of fuselage and structural parts from 50% to 80%, integrating advanced production lines and expanding upstream and midstream supply chains.

The emphasis on modular composite component manufacturing for both civil and defense aerospace sectors is the main fueling factor that is responsible for uplifting India market. The country is emerging as one of the crucial growth markets, supported by government policies and private investments that efficiently enhance aircraft manufacturing, maintenance, and technical capabilities. In November 2023, Airbus notified new contracts with the domestic suppliers Aequs, Dynamatic, Gardner, and Mahindra Aerospace to manufacture airframe and wing components for the A320neo, A330neo, and A350 programs, thereby supporting the government’s AatmaNirbhar Bharat initiative. These contracts strengthen the country’s aerospace ecosystem across sheet metal, machining, and extrusion profiles, denoting a huge growth potential for modular and composite components in both civil and defense aircraft.

Europe Market Insights

Europe aerospace composites market is solidifying its position in the global landscape, effectively fueled by its circular economy goals and advanced R&D infrastructure. Germany, the UK, France, and Spain lead the sector, and the regulatory framework in the region ensures smooth global supply chain integration. In March 2025, the European Composites Industry Association (EuCIA), in partnership with JEC and supported by the European Commission, introduced the European Circular Composites Alliance with a prime goal to promote a circular economy for composite materials in Europe. In addition, the alliance aims to set targets for recycling, reuse, and repurposing of composites, develop circular product design standards, and create a collaborative forum for industry stakeholders, hence making it suitable for bolstering the market in Europe.

Germany aerospace composites market has gained enhanced traction owing to its capacity in the development of multifunctional composites that combine structural performance with embedded thermal management properties. There has been a heightened demand for stronger and more sustainable aircraft components, and government-backed research and innovation programs also propel adoption in this field. In May 2024, the Fraunhofer Institute for Material and Beam Technology (IWS) Dresden, within the EU Clean Sky 2 program, showcased the CO2 laser-based CONTIjoin process for joining large carbon fiber-reinforced thermoplastic aircraft fuselage sections without autoclaves. The institute also notes that this innovative method enables significant weight, material, and labor savings by also producing full-size fuselage components, hence denoting a huge opportunity for the market’s growth and exposure.

The strong focus on repairable and maintainable composite solutions for legacy as well as next-generation platforms is responsible for boosting the market in the UK. Research centers and manufacturers are mainly concentrated on modular designs that allow rapid replacement of damaged panels, minimizing aircraft downtime and reducing lifecycle costs. In June 2025, the National Composites Centre (NCC) announced the establishment of the country’s first-ever Carbon Fibre Development Facility at Cygnet Texkimp’s site in Northwich, Cheshire West, which was funded by the Department for Science, Innovation and Technology (DSIT). The facility will feature two digitally-enabled production lines to advance carbon fiber manufacturing, supporting the UK’s industrial strategy in the aerospace, defense, and energy sectors. From a strategic perspective, such expansions will boost the market by improving domestic supply chains and accelerating the adoption of aerospace composites.

Key Aerospace Composites Market Players:

- Toray Industries, Inc. (Japan)

- Hexcel Corporation (U.S.)

- Solvay S.A. (Belgium)

- SGL Carbon SE (Germany)

- Teijin Limited (Japan)

- Mitsubishi Chemical Holdings Corporation (Japan)

- Owens Corning (U.S.)

- Gurit Holding AG (Switzerland)

- Huntsman Corporation (U.S.)

- Victrex plc (UK)

- Spirit AeroSystems Holdings, Inc. (U.S.)

- Park Aerospace Corp. (U.S.)

- Collins Aerospace (U.S.)

- Aernnova Aerospace S.A. (Spain)

- Kineco Limited (India)

- Aerospace Composites Malaysia Sdn Bhd (Malaysia)

- Hyosung Advanced Materials (South Korea)

- Rock West Composites, Inc. (U.S.)

- Teijin Carbon Europe (Europe)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Toray Industries, Inc. has registered itself predominant leader in this field, especially for carbon fiber and prepregs, which are used in aerospace applications. Besides, the company has decades of experience in this field, and it supplies lightweight, high-strength materials to commercial aircraft manufacturers, defense programs, and space missions.

- Hexcel Corporation is a central player in this field, which is a major supplier of carbon fiber, advanced composites, and reinforcements for various applications. The company’s product portfolio includes prepregs, honeycomb structures, and structural adhesives that support both commercial as well as military aircraft programs.

- Solvay S.A. is headquartered in Belgium and has a significant presence in aerospace composites. The company produces high-performance resins, polymers, and composite solutions that are especially for commercial aircraft, helicopters, and spacecraft, which allows it to maintain a leading position in this field.

- SGL Carbon SE is yet another prominent player in this field that is supplying the aerospace, automotive, and industrial sectors. In aerospace, the company provides carbon fiber reinforcements, prepregs, and carbon-carbon composites for structural as well as thermal applications.

- Teijin Limited is based in Japan and is considered to be a major provider of high-performance fibers, carbon composites, and resin systems for aerospace, automotive, and industrial applications. The company is mainly focused on innovation in lightweighting, high-temperature resistance, and manufacturing efficiency to meet stringent aerospace standards.

Below is the list of some prominent players operating in the global market:

Leading players in the market are Toray Industries, Hexcel, Solvay, and Mitsubishi Chemical, which maintain strong positions through vertical integration, international manufacturing presence, and long-term OEM contracts. Companies are making investments in innovation, such as recyclable resins, automated manufacturing, and thermoplastic composites, to meet sustainability and efficiency goals. Joint ventures, capacity expansions in the emerging economies, and R&D collaborations are tactical strategies adopted by the key players in this sector. In December 2025, Cambium Biomaterials Inc. acquired SHD Group, with the main goal of enhancing growth and innovation in the high-performance aerospace composites sector. The acquisition combines SHD’s knowledge in composite prepregs and resin production with Cambium’s improved material development capabilities, positively impacting market growth.

Corporate Landscape of the Aerospace Composites Market:

Recent Developments

- In January 2026, Cambium announced that it secured a total of USD 100 million in Series B financing, which was led by 8VC with participation from multiple investors, to accelerate the innovation and scaling of materials for aerospace, defense, and other high-performance sectors.

- In December 2025, Syensqo and Vertical Aerospace announced that they entered into a long-term supplier partnership to provide high-performance composite and adhesive materials for the VX4 electric aircraft, targeting certification in 2028.

- Report ID: 3822

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.