Global Testing, Inspection, and Certification Market

1.An Outline of the Global Testing, Inspection, and Certification Market

1.1.Market Definition and Segmentation

1.2.Study Assumptions and Abbreviations

2.Research Methodology & Approach

2.1.Primary Research

2.2.Secondary Research

2.3.Data Triangulation

2.4.SPSS Methodology

3.Executive Summary

4.Growth Drivers

5.Major Roadblocks

6.Opportunities

7.Prevalent Trends

8.Government Regulation

9.Growth Outlook

10.Competitive White Space Analysis – Identifying Untapped Market Gaps

11.Risk Overview

12.SWOT

13.Technological Advancement

14.Technology Maturity Matrix for Testing, Inspection, and Certification Market Recent News

15.Regional Demand

16.Global Testing, Inspection, and Certification by Geography – Strategic Comparative Analysis

17.Strategic Segment Analysis: Testing, Inspection, and Certification Demand Landscape

18.Testing, Inspection, and Certification Demand Trends Driven by Rising Regulatory Compliance, Global Trade Expansion, and Digital Transformation Across Industries (2026-2037)

19.Root Cause Analysis (RCA) for discovering problems in the Testing, Inspection, and Certification Market

20.Porter Five Forces

21.PESTLE

22.Comparative Positioning

23.Global Testing, Inspection, and Certification – Key Player Analysis (2037)

24.Competitive Landscape: Key Suppliers/Players

25.Competitive Model: A Detailed Inside View for Investors

26.Company Market Share, 2037 (%)

26.1.Mistras Group Inc. (U.S.)

26.2.SGS Société Générale de Surveillance SA (Switzerland)

26.3.Bureau Veritas (France)

26.4.DEKRA Certification B.V. (Germany)

26.5.Intertek Group plc (UK)

26.6.Eurofins Scientific Group (Luxembourg)

26.7.TÜV SÜD AG (Germany)

26.8.DNV GL (Norway)

26.9.UL LLC (U.S.)

26.10.Applus+ (Spain)

26.11.TÜV Rheinland (Germany)

27.Global Testing, Inspection, and Certification Market Outlook

27.1.Market Overview

27.1.1.Market Revenue by Value (USD Million), Volume (Million), and Compound Annual Growth Rate (CAGR)

27.2.Testing, Inspection, and Certification Market Segmentation Analysis (2026-2037)

27.2.1.By Service Type

27.2.1.1.Testing and Inspection, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.2.Certification, Market Value (USD Million), and CAGR, 2026-2037F

27.2.2.By Source

27.2.2.1.In-House, Market Value (USD Million), and CAGR, 2026-2037F

27.2.2.2.Outsource, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.By End user

27.2.3.1.Consumer Goods & Retail, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.2.Manufacturing, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.3.Construction & Infrastructure, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.4.Energy & Utilities, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.5.Automotive, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.6.Agriculture and Food, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.7.Chemicals, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.8.Oil & Gas, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.9.Healthcare & Medical Sciences, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.10.Others, Market Value (USD Million), and CAGR, 2026-2037F

27.2.4.Regional Synopsis, Value (USD Million), 2026-2037

27.2.4.1.North America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

27.2.4.2.Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

27.2.4.3.Asia Pacific Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

27.2.4.4.Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

27.2.4.5.Middle East and Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

28.North America Market

28.1.Overview

28.1.1.Market Value (USD Million), Current and Future Projections, 2026-2037

28.1.2.Increment $ Opportunity Assessment, 2026-2037

28.2.Segmentation (USD Million), 2026-2037,

28.2.1.By Service Type

28.2.1.1.Testing and Inspection, Market Value (USD Million), and CAGR, 2026-2037F

28.2.1.2.Certification, Market Value (USD Million), and CAGR, 2026-2037F

28.2.2.By Source

28.2.2.1.In-House, Market Value (USD Million), and CAGR, 2026-2037F

28.2.2.2.Outsource, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.By End user

28.2.3.1.Consumer Goods & Retail, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.2.Manufacturing, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.3.Construction & Infrastructure, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.4.Energy & Utilities, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.5.Automotive, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.6.Agriculture and Food, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.7.Chemicals, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.8.Oil & Gas, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.9.Healthcare & Medical Sciences, Market Value (USD Million), and CAGR, 2026-2037F

28.2.3.10.Others, Market Value (USD Million), and CAGR, 2026-2037F

28.2.4.Country Level Analysis, Value (USD Million)

28.2.4.1.U.S. Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

28.2.4.2.Canada Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.Europe Market

29.1.Overview

29.1.1.Market Value (USD Million), Current and Future Projections, 2026-2037

29.1.2.Increment $ Opportunity Assessment, 2026-2037

29.2.Segmentation (USD Million), 2026-2037,

29.2.1.By Service Type

29.2.1.1.Testing and Inspection, Market Value (USD Million), and CAGR, 2026-2037F

29.2.1.2.Certification, Market Value (USD Million), and CAGR, 2026-2037F

29.2.2.By Source

29.2.2.1.In-House, Market Value (USD Million), and CAGR, 2026-2037F

29.2.2.2.Outsource, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.By End user

29.2.3.1.Consumer Goods & Retail, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.2.Manufacturing, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.3.Construction & Infrastructure, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.4.Energy & Utilities, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.5.Automotive, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.6.Agriculture and Food, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.7.Chemicals, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.8.Oil & Gas, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.9.Healthcare & Medical Sciences, Market Value (USD Million), and CAGR, 2026-2037F

29.2.3.10.Others, Market Value (USD Million), and CAGR, 2026-2037F

29.2.4.Country Level Analysis, Value (USD Million)

29.2.4.1.UK Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.2.Germany Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.3.France Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.4.Italy Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.5.Spain Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.6.Netherlands Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.7.Russia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.8.Switzerland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.9.Poland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.10.Belgium Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.2.4.11.Rest of Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.Asia Pacific, excluding Japan Market

30.1.Overview

30.1.1.Market Value (USD Million), Current and Future Projections, 2026-2037

30.1.2.Increment $ Opportunity Assessment, 2026-2037

30.2.Segmentation (USD Million), 2026-2037,

30.2.1.By Service Type

30.2.1.1.Testing and Inspection, Market Value (USD Million), and CAGR, 2026-2037F

30.2.1.2.Certification, Market Value (USD Million), and CAGR, 2026-2037F

30.2.2.By Source

30.2.2.1.In-House, Market Value (USD Million), and CAGR, 2026-2037F

30.2.2.2.Outsource, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.By End user

30.2.3.1.Consumer Goods & Retail, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.2.Manufacturing, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.3.Construction & Infrastructure, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.4.Energy & Utilities, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.5.Automotive, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.6.Agriculture and Food, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.7.Chemicals, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.8.Oil & Gas, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.9.Healthcare & Medical Sciences, Market Value (USD Million), and CAGR, 2026-2037F

30.2.3.10.Others, Market Value (USD Million), and CAGR, 2026-2037F

30.2.4.Country Level Analysis, Value (USD Million)

30.2.4.1.China Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.2.India Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.3.South Korea Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.4.Australia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.5.Indonesia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.6.Malaysia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.7.Vietnam Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.8.Thailand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.9.Singapore Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.10.New Zealand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.2.4.11.Rest of Asia Pacific Excluding Japan Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

31.Latin America Market

31.1.Overview

31.1.1.Market Value (USD Million), Current and Future Projections, 2026-2037

31.1.2.Increment $ Opportunity Assessment, 2026-2037

31.1.3.Year-on-Year Growth Forecast (%)

31.2.Segmentation (USD Million), 2026-2037, By

31.2.1.By Service Type

31.2.1.1.Testing and Inspection, Market Value (USD Million), and CAGR, 2026-2037F

31.2.1.2.Certification, Market Value (USD Million), and CAGR, 2026-2037F

31.2.2.By Source

31.2.2.1.In-House, Market Value (USD Million), and CAGR, 2026-2037F

31.2.2.2.Outsource, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.By End user

31.2.3.1.Consumer Goods & Retail, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.2.Manufacturing, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.3.Construction & Infrastructure, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.4.Energy & Utilities, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.5.Automotive, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.6.Agriculture and Food, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.7.Chemicals, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.8.Oil & Gas, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.9.Healthcare & Medical Sciences, Market Value (USD Million), and CAGR, 2026-2037F

31.2.3.10.Others, Market Value (USD Million), and CAGR, 2026-2037F

31.2.4.Country Level Analysis, Value (USD Million)

31.2.4.1.Brazil Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

31.2.4.2.Argentina Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

31.2.4.3.Mexico Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

31.2.4.4.Rest of Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.Middle East & Africa Market

32.1.Overview

32.1.1.Market Value (USD Million), Current and Future Projections, 2026-2037

32.1.2.Increment $ Opportunity Assessment, 2026-2037

32.1.3.Year-on-Year Growth Forecast (%)

32.2.Segmentation (USD Million), 2026-2037, By

32.2.1.By Service Type

32.2.1.1.Testing and Inspection, Market Value (USD Million), and CAGR, 2026-2037F

32.2.1.2.Certification, Market Value (USD Million), and CAGR, 2026-2037F

32.2.2.By Source

32.2.2.1.In-House, Market Value (USD Million), and CAGR, 2026-2037F

32.2.2.2.Outsource, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.By End user

32.2.3.1.Consumer Goods & Retail, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.2.Manufacturing, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.3.Construction & Infrastructure, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.4.Energy & Utilities, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.5.Automotive, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.6.Agriculture and Food, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.7.Chemicals, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.8.Oil & Gas, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.9.Healthcare & Medical Sciences, Market Value (USD Million), and CAGR, 2026-2037F

32.2.3.10.Others, Market Value (USD Million), and CAGR, 2026-2037F

32.2.4.Country Level Analysis, Value (USD Million)

32.2.4.1.Saudi Arabia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.2.4.2.UAE Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.2.4.3.Israel Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.2.4.4.Qatar Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.2.4.5.Kuwait Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.2.4.6.Oman Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.2.4.7.South Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.2.4.8.Rest of Middle East & Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

33.Japan Market

33.1.Overview

33.1.1.Market Value (USD Million), Current and Future Projections, 2026-2037

33.1.2.Increment $ Opportunity Assessment, 2026-2037

33.1.3.Year-on-Year Growth Forecast (%)

33.2.Segmentation (USD Million), 2026-2037, By

33.2.1.By Service Type

33.2.1.1.Testing and Inspection, Market Value (USD Million), and CAGR, 2026-2037F

33.2.1.2.Certification, Market Value (USD Million), and CAGR, 2026-2037F

33.2.2.By Source

33.2.2.1.In-House, Market Value (USD Million), and CAGR, 2026-2037F

33.2.2.2.Outsource, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.By End user

33.2.3.1.Consumer Goods & Retail, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.2.Manufacturing, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.3.Construction & Infrastructure, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.4.Energy & Utilities, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.5.Automotive, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.6.Agriculture and Food, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.7.Chemicals, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.8.Oil & Gas, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.9.Healthcare & Medical Sciences, Market Value (USD Million), and CAGR, 2026-2037F

33.2.3.10.Others, Market Value (USD Million), and CAGR, 2026-2037F

34.Global Economic Scenario

34.1. World Economic Outlook

35.About Research Nester

35.1.Our Global Clientele

35.2.We Serve Clients Across World

Testing, Inspection, and Certification Market Outlook:

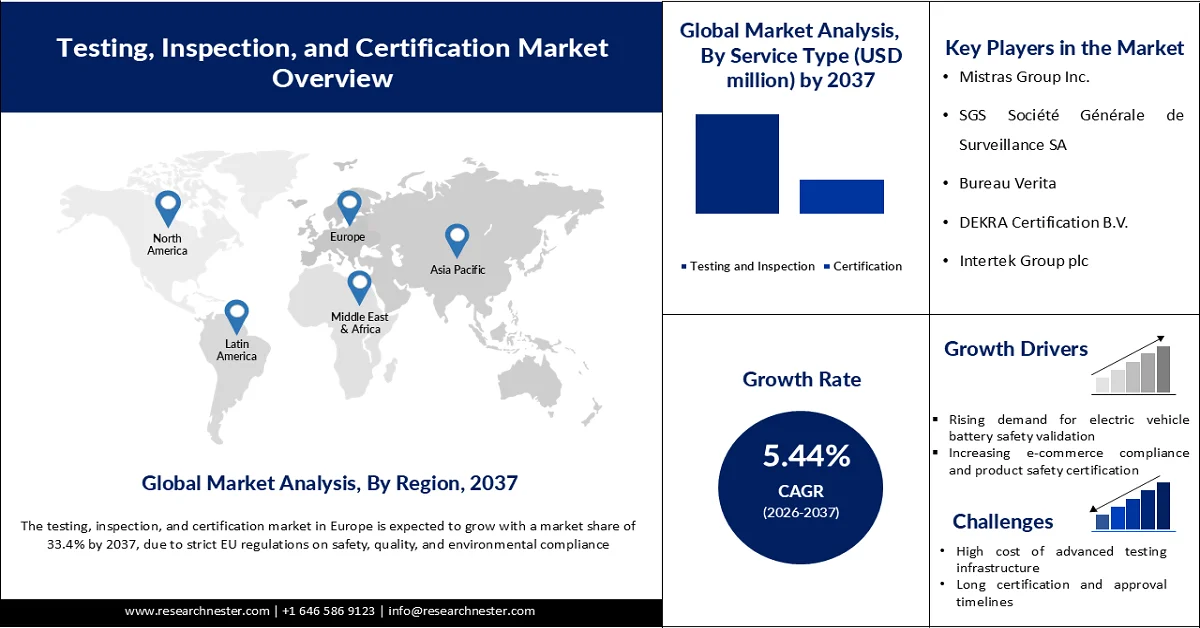

Testing, Inspection, and Certification Market is valued at USD 260.35 billion in 2025 and is projected to reach USD 502 billion by 2037, growing at a CAGR of 5.44% during the forecast period, i.e., 2026-2037. In 2026, the industry size of testing, inspection, and certification is assessed at USD 280.46 billion.

The testing, inspection, and certification market is fundamentally driven by the rising stringency and global harmonization of regulatory standards, which compel organizations to continuously validate product quality, safety, and compliance. Governments and international standard-setting bodies mandate adherence to structured certification systems, making TIC services a critical operational requirement rather than an optional activity. For instance, according to the International Organization for Standardization, there were over 1.47 million active ISO 9001 certificates across 189 economies in 2023, reflecting the widespread adoption of formal quality management systems globally. Additionally, occupational health and safety standards such as ISO 45001 recorded nearly 398,000 certifications with +22% annual growth, indicating increasing regulatory focus on workplace compliance. The expansion of such standardized frameworks across industries ranging from manufacturing to food safety forces companies to rely on third-party testing and certification to meet both domestic and export requirements. Moreover, global supply chains require uniform compliance across multiple jurisdictions, further intensifying demand for TIC services. As regulatory frameworks continue to evolve and enforcement tightens, compliance-driven verification remains the single most significant and sustained growth driver for the testing, inspection, and certification market.

Key Testing Inspection and Certification Market Insights Summary:

Regional Highlights:

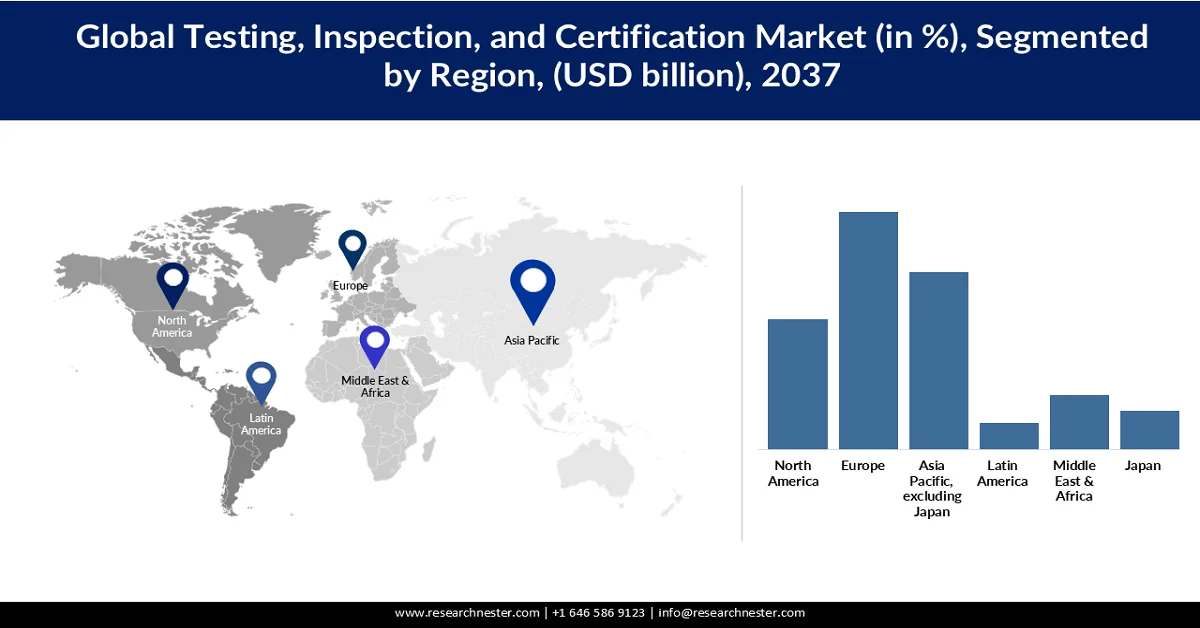

- Europe testing, inspection, and certification market is projected to hold a 33.4% share by 2037, supported by stringent regulatory frameworks and sustainability mandates across industries

- Asia Pacific excluding Japan market is set to witness the fastest growth through 2037, fueled by rapid industrialization and export-driven manufacturing expansion

Segment Insights:

- The testing and inspection segment in the testing, inspection, and certification market is anticipated to expand at a CAGR of 5.59% during 2026–2037, propelled by increasing demand for quality assurance and regulatory compliance across industries

- The in-house sourcing segment is expected to reach a valuation of USD 326.86 billion by 2037, driven by organizations seeking greater control over quality assurance and operational efficiency

Key Growth Trends:

- Rising demand for electric vehicle battery safety validation

- Increasing e-commerce compliance and product safety certification requirements

Major Challenges:

- High cost of advanced testing infrastructure

- Long certification and approval timelines

Key Players: Mistras Group Inc. (U.S.), SGS Société Générale de Surveillance SA (Switzerland), Bureau Veritas (France), DEKRA Certification B.V. (Germany), Intertek Group plc (UK), Eurofins Scientific Group (Luxembourg), TÜV SÜD AG (Germany), DNV GL (Norway), UL LLC (U.S.), Applus+ (Spain), TÜV Rheinland (Germany).

Global Testing Inspection and Certification Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 260.35 billion

- 2026 Market Size: USD 280.46 billion

- Projected Market Size: USD 502 billion by 2037

- Growth Forecasts: 5.44% CAGR (2026-2037)

Key Regional Dynamics:

- Largest Region: Europe (33.4% Share by 2037)

- Fastest Growing Region: Asia Pacific excluding Japan

- Dominating Countries: United States, Germany, China, United Kingdom, Japan

- Emerging Countries: India, Vietnam, Indonesia, Brazil, Mexico

Last updated on : 20 April, 2026

Testing, Inspection, and Certification Market - Growth Drivers and Challenges

Growth Drivers

- Rising demand for electric vehicle battery safety validation: The accelerating adoption of electric vehicles since 2020 has intensified the need for rigorous battery safety validation, directly boosting demand for TIC services. EV batteries pose unique risks such as thermal runaway, fire, and high-voltage hazards, prompting governments to strengthen safety regulations and testing protocols. For instance, the U.S. National Highway Traffic Safety Administration (NHTSA) has implemented standards such as FMVSS No. 305a and launched a dedicated Battery Safety Initiative to investigate defects, conduct research, and enforce compliance for EV batteries. The initiative also includes ongoing investigations and recalls linked to battery-related fire risks, highlighting the critical need for continuous validation. Additionally, global frameworks like the UN’s Global Technical Regulation No. 20 mandate testing for battery durability, crash safety, and fire resistance. As EV deployment scales rapidly worldwide, manufacturers increasingly depend on third-party TIC providers to ensure compliance across design, production, and post-market stages, making battery safety validation a key growth driver.

- Increasing e-commerce compliance and product safety certification requirements: The expansion of e-commerce since the COVID-19 pandemic has significantly increased the need for testing and certification to ensure product safety across global digital marketplaces. According to a 2023 OECD report based on a 2021 international safety sweep, 79% of products sold online were found to be non-compliant or potentially non-compliant with safety standards, while 87% of banned or recalled products were still available for purchase online. These findings highlight substantial regulatory gaps in cross-border online trade and have led governments to tighten surveillance and compliance requirements for digital platforms. As a result, e-commerce companies, sellers, and manufacturers increasingly rely on TIC providers for product testing, certification, and conformity assessment to meet regulatory expectations and avoid recalls or penalties. The growing complexity of global supply chains and cross-border transactions further amplifies the need for standardized certification, positioning e-commerce compliance as a major driver of testing, inspection, and certification market growth.

- Digital platforms enhancing efficiency and workflow in the TIC market: Digital transformation is reshaping the testing, inspection, and certification market by improving efficiency, traceability, and real-time compliance monitoring across industries. Governments and regulatory organizations are increasingly leveraging digital data systems to track product safety and enforce standards more effectively. For instance, the OECD highlights that modern digital marketplaces require continuous monitoring due to high levels of unsafe or non-compliant products circulating globally, reinforcing the need for advanced data-driven oversight systems. Digital tools such as IoT-enabled sensors, AI-based inspection systems, and cloud-based certification platforms enable remote audits, automated testing, and predictive maintenance, significantly reducing inspection time and operational costs. These technologies also enhance transparency and documentation across complex global supply chains, ensuring continuous compliance rather than one-time certification. As regulatory environments become more stringent and globalized, the integration of digital platforms into TIC operations is becoming essential, driving both service innovation and market expansion.

Challenges

- High cost of advanced testing infrastructure: The testing, inspection, and certification market faces a significant restraint in the form of high capital investment required for advanced testing infrastructure. Modern testing facilities, especially for sectors like electric vehicles, aerospace, and pharmaceuticals, require sophisticated equipment, specialized laboratories, and highly skilled personnel. Establishing and maintaining such infrastructure involves substantial upfront and operational costs, which can be prohibitive for small and mid-sized TIC providers. This cost barrier limits market entry, reduces competition, and can slow the expansion of testing capabilities in emerging markets.

- Long certification and approval timelines: Lengthy certification and approval processes pose another key challenge for the testing, inspection, and certification market, as they can delay product launches and increase time-to-market for manufacturers. Many industries must comply with complex, multi-stage regulatory procedures that involve extensive documentation, repeated testing, and audits across different jurisdictions. These prolonged timelines can create bottlenecks, particularly in fast-evolving sectors like electronics and medical devices. As a result, companies may face increased costs and reduced agility, which can discourage innovation and slow overall market growth.

Testing, Inspection, and Certification Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2037 |

|

CAGR |

5.44% |

|

Base Year Market Size (2025) |

USD 260.35 billion |

|

Forecast Year Market Size (2037) |

USD 502 billion |

|

Regional Scope |

|

Testing, Inspection, and Certification Market Segmentation:

Service Type Segment Analysis

The testing and inspection segment is expected to grow at a CAGR of 5.59% between 2026 and 2037, due to its critical role in ensuring product quality, safety, and regulatory compliance across industries. As manufacturing processes become more complex and globalized, companies increasingly rely on independent testing and inspection to detect defects, verify specifications, and maintain consistent standards throughout production and supply chains. Regulatory authorities mandate frequent inspections and pre-market testing in sectors such as food, pharmaceuticals, construction, and electronics, making these services essential rather than optional. Additionally, rising concerns around product recalls, safety incidents, and brand reputation are pushing organizations to adopt continuous inspection and quality assurance practices. The growth of cross-border trade further amplifies demand, as exporters must meet diverse regulatory requirements across multiple regions. Moreover, the integration of advanced technologies such as automation, IoT-based monitoring, and non-destructive testing techniques is enhancing the efficiency and scope of testing and inspection services, further accelerating segment growth.

Source Segment Analysis

The in-house sourcing segment is projected to be valued at USD 326.86 billion by 2037. The segment is contributing to the growth of the market by enabling companies to maintain greater control over quality assurance and compliance processes. Large organizations, particularly in sectors like automotive, pharmaceuticals, and electronics, are increasingly investing in internal testing and inspection capabilities to reduce dependency on third-party providers and shorten turnaround times. This approach allows for real-time monitoring, faster decision-making, and early detection of defects during production, ultimately improving operational efficiency. Additionally, in-house capabilities help firms protect proprietary technologies and sensitive data, which is especially critical in innovation-driven industries. While external certification remains required for regulatory approval, integrating in-house testing with third-party validation creates a hybrid model that strengthens overall demand for TIC-related solutions, including equipment, software, and specialized expertise.

End user Segment Analysis

The consumer goods & retail segment is expected to grow, with a market share of 21.15% by 2037, driven by high product volumes, strict safety regulations, and increasing scrutiny in global and digital marketplaces. Governments and international organizations emphasize the scale of safety risks in this sector. For instance, the OECD has highlighted that unsafe consumer products contribute to thousands of preventable injuries each year across member countries, underscoring the public health importance of strong oversight and compliance systems (OECD consumer product safety work, 2020–2023). This growing concern has led to stricter regulatory frameworks and stronger enforcement of product safety standards across consumer goods categories. As retail supply chains become increasingly global and complex, manufacturers and retailers face greater pressure to ensure consistent compliance with labeling, safety, and quality requirements across multiple jurisdictions. The rapid expansion of e-commerce further amplifies these challenges, as products move quickly across borders and reach consumers through diverse digital platforms. Consequently, companies rely more heavily on TIC services for rigorous testing, inspection, and certification market to reduce risk, maintain regulatory compliance, and protect brand reputation.

Our in-depth analysis of testing, inspection, and certification market includes the following segments:

|

Segments |

Subsegments |

|

Service Type |

|

|

Source |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Testing, Inspection, and Certification Market - Regional Analysis

Europe Market Insights

The testing, inspection, and certification market in Europe is projected to hold a share of 33.4% by 2037. The growth of the market has been steady due to strict EU regulations on safety, quality, and environmental compliance. Strong industrial bases in Germany, France, and the UK, especially in automotive, manufacturing, and energy, are driving consistent demand for certification and conformity assessment services. Sustainability requirements and the EU’s focus on carbon neutrality are increasing the demand for environmental and green certifications. Cross-border trade within the EU further supports standardized testing and inspection services across supply chains. However, high compliance costs and fragmented national regulations slightly constrain faster expansion.

Germany is the largest testing, inspection, and certification market in Europe, supported by its highly regulated industrial ecosystem and strong manufacturing base, especially in the automotive and machinery sectors. EU-wide regulations such as CE marking, REACH, and the upcoming Machinery Regulation are significantly increasing the scope of mandatory testing and certification. Germany’s Industry 4.0 transformation is driving demand for advanced testing of robotics, IoT systems, batteries, and AI-enabled industrial equipment. Digital inspection, remote auditing, and AI-based quality control are increasingly being adopted to improve efficiency and traceability. However, capacity bottlenecks in accredited labs and a shortage of skilled experts are creating delays, further increasing reliance on external TIC providers.

France testing, inspection, and certification market is expanding due to strict EU and national regulatory enforcement across aerospace, nuclear energy, pharmaceuticals, and food safety sectors. Regulatory frameworks such as NIS2, CSRD (Corporate Sustainability Reporting Directive), MDR/IVDR, and ESG disclosure rules are increasing demand for independent certification and compliance verification. Large French TIC players like Bureau Veritas conduct tens of millions of inspections and tests annually, showing strong service penetration in industrial compliance.

Sustainability verification and ESG assurance are major growth drivers, particularly in carbon reporting and supply-chain transparency requirements. France is also seeing rising demand from cybersecurity testing, hydrogen infrastructure, and EV/battery ecosystems, especially in industrial regions like Île-de-France and Auvergne-Rhône-Alpes. However, the limited availability of accredited auditors and laboratories is constraining the faster scaling of services.

Asia Pacific excluding Japan Market Insights

Asia Pacific excluding Japan is the fastest-growing testing, inspection, and certification market globally, driven by rapid industrialization and export-oriented manufacturing in countries like China, India, Vietnam, and Indonesia. Expanding electronics, automotive (especially EVs), and renewable energy sectors are significantly increasing testing and certification needs. Strong regulatory tightening and rising quality expectations from global buyers are pushing companies toward third-party TIC services. Digital inspection technologies and automation are accelerating efficiency and scalability across the region. Despite strong growth, uneven regulatory enforcement and price sensitivity among smaller firms remain key challenges.

In China, the TIC ecosystem is expanding under a strong state-led quality infrastructure. The Certification and Accreditation Administration of China administers the China Compulsory Certification (CCC) system, which covers a wide range of industrial and consumer products, indicating broad regulatory penetration. China has also continued to increase the number of accredited certification bodies and laboratories under its national system, reflecting steady growth in conformity assessment capacity and demand. Government data highlights ongoing expansion in certified organizations and inspection activities, driven by stricter enforcement of product quality, safety, and environmental standards across sectors.

In India, the testing, inspection, and certification market is growing rapidly due to expanding regulatory coverage and the formalization of industries. The Bureau of Indian Standards has developed over 20,000 Indian Standards and continues to widen its product certification schemes. The Food Safety and Standards Authority of India oversees millions of registered and licensed food businesses, significantly increasing inspection and compliance requirements. Additionally, the Quality Council of India reports growth in accredited laboratories, certification, and inspection bodies, indicating rising demand for quality assurance services. Together, these trends show sustained testing, inspection, and certification market expansion supported by regulatory strengthening and increasing compliance needs.

North America Market Insights

North America represents a mature but steadily growing testing, inspection, and certification market, supported by stringent regulatory frameworks across healthcare, automotive, aerospace, and energy sectors. The U.S. leads demand due to its advanced manufacturing base and high compliance requirements for safety and product quality. Increasing adoption of technologies like AI-based inspection, IoT monitoring, and data analytics is improving testing efficiency and traceability. Certification demand is also rising due to a strong focus on sustainability, ESG compliance, and supply chain transparency. Growth is stable but slightly constrained by high service costs and saturation in some industrial segments.

In the U.S., the TIC ecosystem is supported by a large and highly structured conformity assessment network. The U.S. has a vast and complex standards ecosystem, with the federal government alone responsible for over 44,000 statutes, technical regulations, and procurement specifications. In addition, the private sector contributes more than 50,000 standards, bringing the total number in use close to 100,000 nationwide. These standards are developed and maintained by nearly 600 organizations, including over 200 accredited by the American National Standards Institute as official developers of American National Standards (ANS). While individual federal agencies decide which standards to adopt, there is a growing shift toward using voluntary consensus standards from both national and international bodies, reflecting increased alignment and efficiency in regulatory practices. In addition, the U.S. Food and Drug Administration regulates products accounting for about 20% of all U.S. consumer spending, requiring extensive testing and certification. Workplace safety enforcement by the Occupational Safety and Health Administration covers over 130 million workers across more than 8 million workplaces. These figures highlight a large, mature testing, inspection, and certification market with sustained demand driven by regulatory scale and enforcement.

In Canada, the testing, inspection, and certification market is expanding through a well-established accreditation and standards framework. The Standards Council of Canada supports a network of over 400 accredited organizations, including testing laboratories, inspection bodies, and certification bodies. Canada also participates in multiple international accreditation systems, enabling global recognition of its conformity assessments and increasing cross-border certification demand. Health Canada regulates a wide range of products, including pharmaceuticals, biologics, and medical devices, all requiring rigorous testing and inspection. Additionally, thousands of Canadian businesses operate under certified management system standards, reflecting the growing adoption of formal certification processes. These numerical indicators demonstrate steady testing, inspection, and certification market growth supported by regulatory oversight, accreditation expansion, and international integration.

Key Testing, Inspection, and Certification Market Players:

- Mistras Group Inc. (U.S.)

- SGS Société Générale de Surveillance SA (Switzerland)

- Bureau Veritas (France)

- DEKRA Certification B.V. (Germany)

- Intertek Group plc (UK)

- Eurofins Scientific Group (Luxembourg)

- TÜV SÜD AG (Germany)

- DNV GL (Norway)

- UL LLC (U.S.)

- Applus+ (Spain)

- TÜV Rheinland (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- SGS operates one of the largest TIC networks globally, with a presence in over 140 countries and more than 2,600 offices and laboratories. The company delivers a full suite of testing, inspection, and certification market services across industries such as minerals, agriculture, life sciences, and consumer goods. It holds tens of thousands of active certifications and accreditations, reflecting strong regulatory alignment and market trust. SGS is also advancing digital inspection and sustainability assurance services, positioning itself in high-growth TIC segments.

- Bureau Veritas maintains a strong global footprint with operations in more than 140 countries and over 1,500 sites. The company provides TIC services across sectors like infrastructure, marine, agri-food, and consumer products, ensuring end-to-end compliance. It manages over 100,000 certifications and thousands of accreditations, supporting a broad client base. Its strategy focuses on digital transformation and sustainability services, strengthening its competitive position in the testing, inspection, and certification market.

- Intertek operates a global network of over 1,000 laboratories and offices in more than 100 countries. The company delivers assurance, testing, inspection, and certification market services across sectors such as energy, chemicals, and consumer products. It supports thousands of clients with quality assurance programs and certification schemes aligned with international standards. Intertek is increasingly investing in Total Quality Assurance (TQA) solutions and digital tools to enhance service delivery.

- TÜV SÜD has a presence in over 1,000 locations worldwide and employs more than 25,000 people. The company provides TIC services across industrial, mobility, and certification segments, with a strong focus on safety and risk management. It conducts millions of inspections and audits annually, reflecting large-scale operational capacity. TÜV SÜD is also expanding in areas such as renewable energy, smart infrastructure, and digital certification services.

- DNV operates in over 100 countries and delivers TIC services focused on energy, maritime, healthcare, and digital assurance. The company performs thousands of certifications and risk assessments annually, supporting safety and compliance across critical industries. It is a leader in classification and certification for the maritime and energy sectors. DNV is also investing in digital assurance, cybersecurity, and sustainability services, aligning with evolving global TIC demands.

Below is the list of the key players operating in the global testing, inspection, and certification market:

Key players in the testing, inspection, and certification market are driving growth through strategic expansion, technological adoption, and service diversification. Companies such as SGS, Bureau Veritas, and Intertek are expanding their global footprint through acquisitions and partnerships, strengthening their presence in emerging markets. Firms like TÜV SÜD, DNV, and UL are investing in advanced technologies such as digital inspection, automation, and data analytics to enhance efficiency and accuracy. Many players are also broadening their portfolios to include high-growth areas like sustainability certification, renewable energy testing, and cybersecurity assurance. Additionally, continuous alignment with evolving international standards and regulatory requirements enables these companies to capture increasing demand for compliance and quality assurance services across industries.

Corporate Landscape of the Global Testing, Inspection, and Certification Market:

Recent Developments

- In July 2024, UL Solutions Inc., a global leader in applied safety science, inaugurated its North America Advanced Battery Laboratory in Auburn Hills, Michigan, one of the largest and most advanced facilities in the U.S. dedicated to testing electric, hybrid vehicle, and industrial batteries.

- In December 2025, Intertek, a global Total Quality Assurance provider, expanded its testing and certification capabilities in Bangladesh by launching advanced Hardlines, Toys, and Calibration laboratories at its facility in Gazipur, strengthening its support for product compliance and quality assurance.

- Report ID: 4738

- Published Date: Apr 20, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Testing Inspection and Certification Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.