Global Specialty Malt Market

- An Outline of the Global Specialty Malt Market

- Market Definition and Segmentation

- Study Assumptions and Abbreviations

- Research Methodology & Approach

- Primary Research

- Secondary Research

- Data Triangulation

- SPSS Methodology

- Executive Summary

- Growth Drivers

- Major Roadblocks

- Opportunities

- Prevalent Trends

- Government Regulation

- Growth Outlook

- Competitive White Space Analysis – Identifying Untapped Market Gaps

- Risk Overview

- SWOT

- Technological Advancement

- Technology Maturity Matrix for Specialty Malt Market Recent News

- Regional Demand

- Global Specialty Malt by Geography – Strategic Comparative Analysis

- Strategic Segment Analysis: Specialty Malt Demand Landscape

- Specialty Malt Demand Trends Driven by Sustainability, Strategic Collaborations, and Regulatory Compliance (2026-2036)

- Root Cause Analysis (RCA) for discovering problems of the Specialty Malt Market

- Porter Five Forces

- PESTLE

- Comparative Positioning

- Global Specialty Malt – Key Player Analysis (2036)

- Competitive Landscape: Key Suppliers/Players

- Competitive Model: A Detailed Inside View for Investors

- Company Market Share, 2036 (%)

- Barmalt

- Briess Malt & Ingredients

- Canada Malting Co. Limited,

- Castle Malting

- Crisp Malt

- Invivo (Soufflet Group Acquired By Group InVivo)

- IREKS GmbH

- Malteurop

- MÄLZEREI STEINBACH

- Mouterij Dingemans

- MunThousand Tons Plc

- RahrBSG

- Simpsons Malt

- Thomas Fawcett & Sons Ltd.

- Global Specialty Malt Market Outlook

- Market Overview

- Market Revenue by Value (USD Thousand), Volume (Thousand Tons), and Compound Annual Growth Rate (CAGR)

- Specialty Malt Market Segmentation Analysis (2026-2036)

- By Source

- Barley, Market Value (USD Thousand), and CAGR, 2026-2036F

- Wheat, Market Value (USD Thousand), and CAGR, 2026-2036F

- Rye, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Type

- Roasted Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Caramel Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Crystal Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Pale Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Munich Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Vienna Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Application

- Brewing, Market Value (USD Thousand), and CAGR, 2026-2036F

- Distilling, Market Value (USD Thousand), and CAGR, 2026-2036F

- Non-Alcoholic Malt Beverages, Market Value (USD Thousand), and CAGR, 2026-2036F

- Baking, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Extraction Rate

- Low Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Medium Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- High Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Form

- Dry Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Liquid Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Regional Synopsis, Value (USD Thousand), 2026-2036

- North America Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Europe Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Asia Pacific Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Latin America Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Middle East and Africa Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Source

- Market Overview

- North America Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Thousand), 2026-2036, By

- By Source

- Barley, Market Value (USD Thousand), and CAGR, 2026-2036F

- Wheat, Market Value (USD Thousand), and CAGR, 2026-2036F

- Rye, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Type

- Roasted Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Caramel Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Crystal Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Pale Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Munich Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Vienna Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Application

- Brewing, Market Value (USD Thousand), and CAGR, 2026-2036F

- Distilling, Market Value (USD Thousand), and CAGR, 2026-2036F

- Non-Alcoholic Malt Beverages, Market Value (USD Thousand), and CAGR, 2026-2036F

- Baking, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Extraction Rate

- Low Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Medium Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- High Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Form

- Dry Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Liquid Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Thousand)

- U.S. Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Canada Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Source

- Overview

- Europe Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Thousand), 2026-2036, By

- By Source

- Barley, Market Value (USD Thousand), and CAGR, 2026-2036F

- Wheat, Market Value (USD Thousand), and CAGR, 2026-2036F

- Rye, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Type

- Roasted Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Caramel Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Crystal Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Pale Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Munich Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Vienna Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Application

- Brewing, Market Value (USD Thousand), and CAGR, 2026-2036F

- Distilling, Market Value (USD Thousand), and CAGR, 2026-2036F

- Non-Alcoholic Malt Beverages, Market Value (USD Thousand), and CAGR, 2026-2036F

- Baking, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Extraction Rate

- Low Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Medium Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- High Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Form

- Dry Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Liquid Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Thousand)

- UK Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Germany Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- France Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Italy Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Spain Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Netherlands Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Russia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Switzerland Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Poland Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Belgium Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Europe Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Source

- Overview

- Asia Pacific Market Excluding Japan

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Thousand), 2026-2036, By

- By Source

- Barley, Market Value (USD Thousand), and CAGR, 2026-2036F

- Wheat, Market Value (USD Thousand), and CAGR, 2026-2036F

- Rye, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Type

- Roasted Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Caramel Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Crystal Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Pale Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Munich Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Vienna Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Application

- Brewing, Market Value (USD Thousand), and CAGR, 2026-2036F

- Distilling, Market Value (USD Thousand), and CAGR, 2026-2036F

- Non-Alcoholic Malt Beverages, Market Value (USD Thousand), and CAGR, 2026-2036F

- Baking, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Extraction Rate

- Low Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Medium Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- High Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Form

- Dry Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Liquid Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Thousand)

- China Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- India Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Korea Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Australia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Indonesia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Malaysia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Vietnam Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Thailand Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Singapore Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- New Zealand Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Asia Pacific Excluding Japan Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Source

- Overview

- Japan Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Thousand), 2026-2036, By

- By Source

- Barley, Market Value (USD Thousand), and CAGR, 2026-2036F

- Wheat, Market Value (USD Thousand), and CAGR, 2026-2036F

- Rye, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Type

- Roasted Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Caramel Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Crystal Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Pale Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Munich Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Vienna Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Application

- Brewing, Market Value (USD Thousand), and CAGR, 2026-2036F

- Distilling, Market Value (USD Thousand), and CAGR, 2026-2036F

- Non-Alcoholic Malt Beverages, Market Value (USD Thousand), and CAGR, 2026-2036F

- Baking, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Extraction Rate

- Low Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Medium Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- High Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Form

- Dry Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Liquid Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Source

- Overview

- Latin America Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Thousand), 2026-2036, By

- By Source

- Barley, Market Value (USD Thousand), and CAGR, 2026-2036F

- Wheat, Market Value (USD Thousand), and CAGR, 2026-2036F

- Rye, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Type

- Roasted Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Caramel Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Crystal Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Pale Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Munich Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Vienna Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Application

- Brewing, Market Value (USD Thousand), and CAGR, 2026-2036F

- Distilling, Market Value (USD Thousand), and CAGR, 2026-2036F

- Non-Alcoholic Malt Beverages, Market Value (USD Thousand), and CAGR, 2026-2036F

- Baking, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Extraction Rate

- Low Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Medium Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- High Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Form

- Dry Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Liquid Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Thousand)

- Brazil Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Argentina Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Mexico Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Latin America Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Source

- Overview

- Middle East & Africa Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Thousand), 2026-2036, By

- By Source

- Barley, Market Value (USD Thousand), and CAGR, 2026-2036F

- Wheat, Market Value (USD Thousand), and CAGR, 2026-2036F

- Rye, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Type

- Roasted Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Caramel Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Crystal Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Pale Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Munich Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Vienna Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Application

- Brewing, Market Value (USD Thousand), and CAGR, 2026-2036F

- Distilling, Market Value (USD Thousand), and CAGR, 2026-2036F

- Non-Alcoholic Malt Beverages, Market Value (USD Thousand), and CAGR, 2026-2036F

- Baking, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Extraction Rate

- Low Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Medium Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- High Extraction Rate Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Form

- Dry Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Liquid Malt, Market Value (USD Thousand), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Thousand)

- Saudi Arabia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- UAE Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Israel Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Qatar Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Kuwait Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Oman Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Africa Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Middle East & Africa Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Source

- Overview

- Global Economic Scenario

- World Economic Outlook

- About Research Nester

- Our Global Clientele

- We Serve Clients Across World

Specialty Malt Market Outlook:

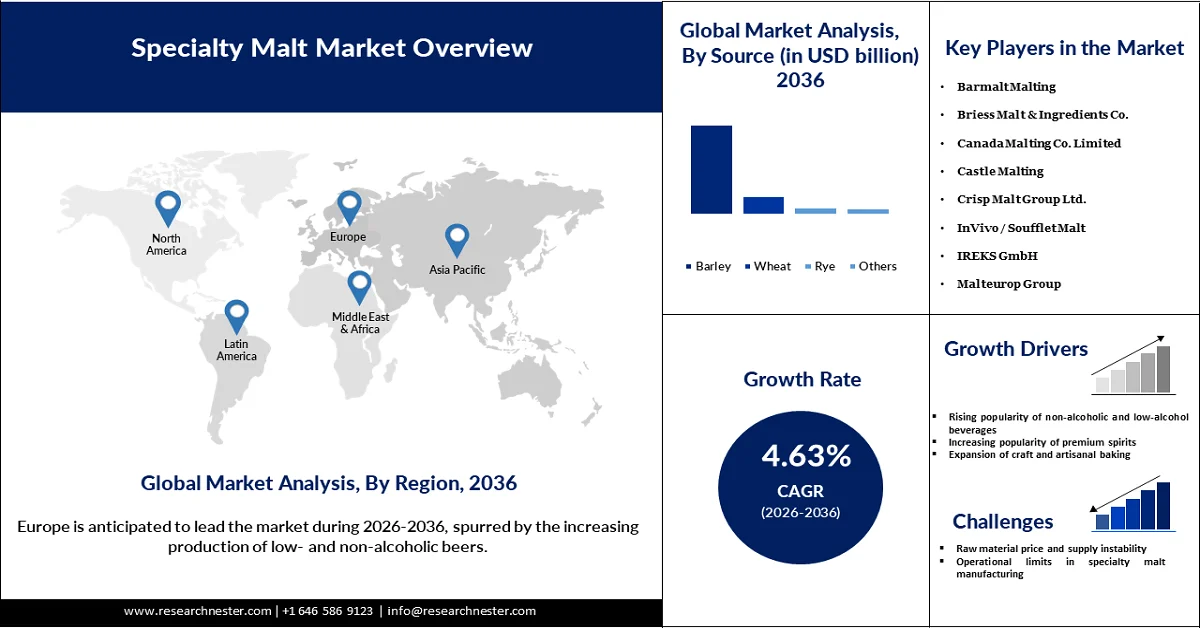

Specialty Malt Market is valued at USD 3.54 billion in 2025 and is anticipated to surpass USD 5.94 billion by 2036, expanding at a CAGR of 4.63% during the forecast period, i.e., 2026 to 2036. In 2026, the industry size of specialty malt is assessed at USD 3.78 billion.

The booming expansion of craft breweries and artisanal distilleries worldwide is fueling rapid growth in the specialty malt industry, as producers seek to create beverages with distinctive flavors, aromas, and visual appeal. In contrast to major commercial beverage producers, craft makers prioritize creativity and experimentation, prompting them to incorporate a wider variety of specialty malts, including caramelized, roasted, chocolate, and smoked types. Building on this, in September 2025, Weyermann, with its portfolio of over 100 malt types, demonstrated the impact of specialty malts on color, taste, and versatility across alcoholic and non-alcoholic drinks as well as culinary uses. The showcase featured three non-alcoholic beers, including a smoked option, catering to growing demand while preserving rich and complex flavors. The growing craft beverage movement in countries like the U.S., Germany, and the United Kingdom has further increased the need for premium and customized malt options. Simultaneously, increasing demand for local and upscale alcoholic drinks is promoting small-batch brewing and distilling, which requires high-quality specialty ingredients. To adapt, malt makers are enhancing their product lines and investing in practical innovation, ensuring they remain competitive and contribute to sustained growth in the sector.

At the same time, as more consumers seek high-quality, natural, and health-conscious options, manufacturers are increasingly turning to specialty malt market for their unique taste and exceptional ingredients. These malts contribute natural sweetness, rich color, and unique flavor without the need for artificial additives, fitting well with the clean-label movement. Food and beverage makers incorporate them into craft beers, artisanal spirits, and wholesome baked goods to create products that appeal to discerning customers. As a result, specialty malts are becoming an essential ingredient for producers aiming to meet rising expectations for flavor, quality, and healthier choices.

Key Specialty Malt Market Insights Summary:

Regional Highlights:

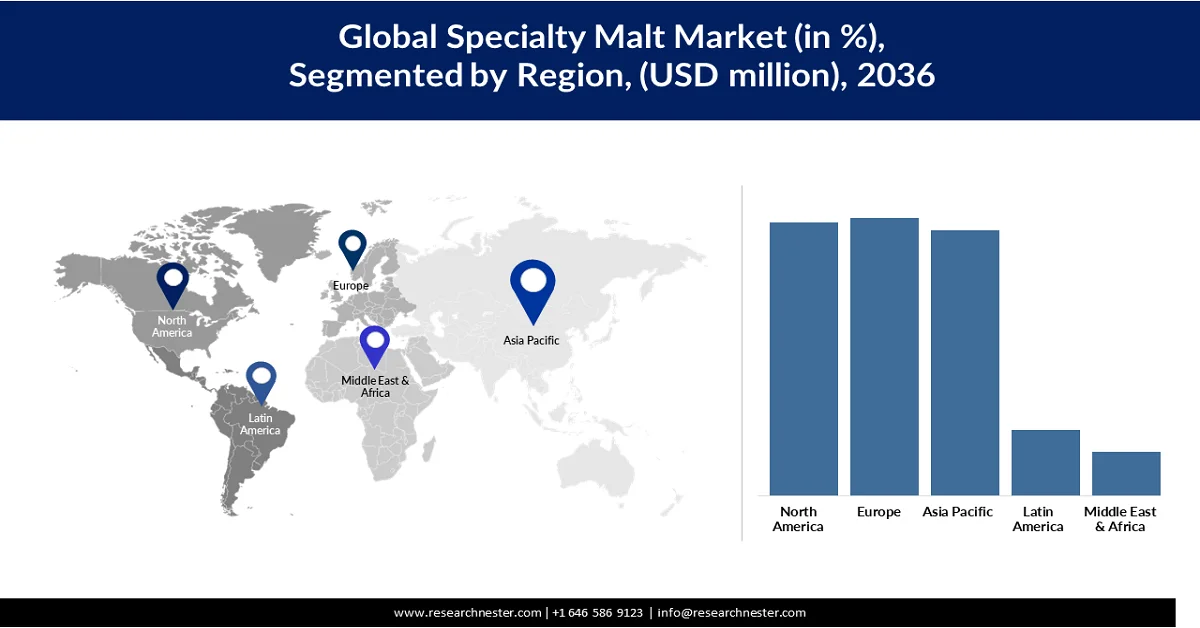

- Europe is projected to command a 30% share of the specialty malt market by 2036, supported by rising production of low- and non-alcoholic beers and expanding applications of specialty malts to enhance flavor, color, and mouthfeel.

- North America is estimated to capture 29% of the market by 2036, bolstered by continuous craft beer innovation and strong barley supply supporting premium malt product development.

Segment Insights:

- Barley is anticipated to secure a 73.41% share of the specialty malt market by 2036, attributed to its superior enzymatic strength and consistent fermentable sugar content supporting brewing, distilling, and baking applications.

- Roasted Malt is projected to represent 28.81% of the market by 2036, fueled by the rising popularity of craft beers, specialty stouts, dark ales, and porters requiring complex flavor and color profiles.

Key Growth Trends:

- Rising popularity of non-alcoholic and low-alcohol beverages

- Increasing popularity of premium spirits

Major Challenges:

- Raw material price and supply instability

- Operational limits in specialty malt manufacturing

Key Players: Barmalt Malting (India), Briess Malt & Ingredients Co. (U.S.), Canada Malting Co. Limited (Canada), Castle Malting (Belgium), Crisp Malt Group Ltd. (U.K.), InVivo / Soufflet Malt (France), IREKS GmbH (Germany), Malteurop Group (France), Mouterij Dingemans (Belgium), Muntons Plc (U.K.), Rahr Malting Co. / BSG (U.S.), Simpsons Malt Limited (U.K.), Thomas Fawcett & Sons Ltd (U.K.).

Global Specialty Malt Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.54 billion

- 2026 Market Size: USD 3.78 billion

- Projected Market Size: USD 5.94 billion by 2036

- Growth Forecasts: 4.63% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: Europe (30% Share by 2036)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, United Kingdom, Canada, Belgium

- Emerging Countries: China, India, Japan, South Korea, Australia

Last updated on : 10 March, 2026

Specialty Malt Market - Growth Drivers and Challenges

Growth Drivers

- Rising popularity of non-alcoholic and low-alcohol beverages: As non-alcoholic and low-alcohol beverages become more popular, specialty malts are finding increasing opportunities in the specialty malt market. For instance, in 2024, EU production of low- and no-alcohol beer increased by 11.1% to approximately 2 billion liters, surpassing the growth of conventional beer and signaling a structural change in consumer drinking habits. Craft brewers use specialty malts to create alcohol-free or low-alcohol beers that match traditional beers in color, flavor, and body. Roasted and smoked malt varieties help producers craft beverages that closely resemble standard beers while catering to the growing focus on health and wellness. The demand for flavorful non-alcoholic and low-alcohol drinks is rising worldwide, particularly in countries where mindful drinking is becoming more common. As consumers gradually seek tasty, alcohol-free alternatives, specialty malts are playing an essential role in developing these products.

- Increasing popularity of premium spirits: Increasing consumer preference for premium and craft spirits, such as whiskey and bourbon, is boosting the use of specialty malt market. In response, in August 2023, Beam Suntory and Frucor Suntory launched Suntory Oceania, an AU$3 billion multi-beverage partnership covering premium spirits and non-alcoholic drinks in Australia and New Zealand. The venture will combine the strengths of both companies to form the fourth-largest beverage group in the ANZ region, with full control over manufacturing, sales, and distribution. These malts enhance the taste, color, and body of distilled beverages, enabling producers to create distinctive and high-quality profiles. Craft and small-batch distillers frequently rely on specialty malts to differentiate their offerings and appeal to quality-focused consumers. With rising demand for premium spirits in North America and Europe, the specialty malt segment within this sector continues to grow steadily.

- Expansion of craft and artisanal baking: The rise of craft and artisanal baking has significantly boosted specialty malt market demand, as these bakers emphasize wholesome ingredients, rich taste, and appealing textures. The industry continued to gain strength in 2025. At CFIA Rennes in March, suppliers presented bakery-specific malt extracts as versatile, clean-label enhancers of flavor, color, and texture, emphasizing the shift of malt use from brewing into the bakery and craft food sectors. Enhancing baked goods with natural sweetness, vibrant color, and distinctive taste, specialty malts improve product quality without the need for artificial additives. Many small-scale and artisanal bakeries use these malts to create distinctive, signature products that differentiate them in competitive specialty malt markets and attract discerning, quality-focused consumers. With more people seeking premium, wholesome, and flavorful baked items, the demand for specialty malts in baking continues to rise. This trend is particularly strong in regions with a thriving artisanal food culture, highlighting the versatility of specialty malts beyond just beverages.

Challenges

- Raw material price and supply instability: Specialty malt production relies mainly on barley, a crop highly susceptible to weather fluctuations and damage from extreme events such as droughts and floods, which diminish yields and degrade malting quality. Declining global barley output and worsening quality have driven up barley prices and increased production expenses, putting pressure on malt producers’ profit margins. This persistent price fluctuation creates uncertainty across the specialty malt supply chain, leading to frequent price adjustments for brewers, distillers, and food producers, which slows down overall industry expansion.

- Operational limits in specialty malt manufacturing: Caramel, roasted, chocolate, and high-diastatic specialty malts face production constraints due to their dependence on small, carefully overseen batches and precise roasting processes. Expanding batch sizes often results in quality fluctuations and barley variability, limiting the potential for scaling up even as demand from craft brewers, artisan bakers, and specialty food makers increases. Scaling up is further hindered by the substantial investment required for roasting and kilning machinery, which contributes to longer delivery schedules and less adaptability in meeting large orders. This situation drives prices up and risks smaller maltsters losing customers to bigger suppliers, keeping specialty malts within a premium, supply-restricted specialty malt market segment.

Specialty Malt Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2036 |

|

CAGR |

4.63% |

|

Base Year Market Size 2025 |

USD 3.54 billion |

|

Forecast Year Market Size 2036 |

USD 5.94 billion |

|

Regional Scope |

|

Specialty Malt Market Segmentation:

Source Segment Analysis

The barley segment is expected to hold 73.41% of the specialty malt market share. Barley is the most widely used and versatile raw material for malt production. It is the leading and most versatile raw ingredient for malt production. In January 2026, Simpsons Malt Limited achieved a major sustainability milestone by obtaining 100% Farm Sustainability Assessment (FSA) Gold verification across its entire UK malting barley supply. This accomplishment reinforces Simpsons Malt’s commitment to sustainable sourcing, providing its brewing and distilling customers with verified, traceable barley while setting a new benchmark for sustainable malting practices in the UK. With its high enzyme levels, steady fermentable sugars, and consistent malting quality, it is well-suited for brewing, distilling, and baking. Barley malts are favored by craft brewers and artisanal bakers for their ability to enhance flavor, deepen color, and add body to drinks and baked products.

Type Segment Analysis

The roasted malt segment is expected to hold a 28.81% specialty malt market share by 2036. The use of roasted malts is central to producing beers and beverages with rich hues, full-bodied aroma, and layered flavor complexity. Craft brewers and artisanal distillers often choose chocolate, black, and coffee malts to design products with unique and recognizable taste profiles. These malts enhance body, mouthfeel, and visual appeal, making them highly valued in premium and specialty drinks. The increasing popularity of craft beers, specialty stouts, dark ales, and porters, especially in European and North American specialty malt markets, is driving steady consumption of roasted malts. In January 2026, Lexington Brewing & Distilling Co. introduced the Kentucky Bourbon Barrel Toasted Stout, highlighting roasted malts, toasted oak, and bourbon barrel flavors, while extending distribution to Missouri. This launch reflects ongoing growth in high-ABV, malt-driven seasonal beers. Limited availability of some roasted malt types strengthens their specialty malt market significance.

Form Segment Analysis

The dry malt segment is expected to grow at a specialty malt market share of 65.81% by 2036 because of its easy handling, longer shelf stability, and versatility across brewing, distilling, and baking applications. Dry malts provide consistent enzyme activity and fermentable sugars, allowing brewers and distillers to achieve dependable fermentation and high-quality finished products. For example, Briess CBW Dry Malt Extracts, including Golden Light DME, Sparkling Amber DME, and Traditional Dark DME, offer rich malt character, precise color control, and fermentable sugars, allowing brewers to perform extract brewing without preparing fresh wort. In contrast to liquid malts, dry malts are easier to store and ship, making them ideal for large-scale production and global distribution. Furthermore, craft brewers and artisanal bakers appreciate dry malts for the unique flavors, rich color, and full-bodied texture they bring to drinks and baked goods, fueling demand in premium and specialty markets worldwide.

Our in-depth analysis of the global specialty malt includes the following segments:

|

Segments |

Subsegments |

|

Source |

|

|

Form |

|

|

Type |

|

|

Extraction Rate |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Specialty Malt Market - Regional Analysis

Europe Market Insights

Europe is expected to dominate the specialty malt market, accounting for 30% of the total share by 2036. As the production of low- and non-alcoholic beers increases, brewers are increasingly using specialty malts to enhance color, intensify flavor, and improve mouthfeel. As stated by the European Commission, in 2024, European Union countries produced a total of 34.7 billion litres of beer, comprising 32.7 billion litres of beer with more than 0.5% alcohol and 2 billion litres of low- or non-alcoholic beer containing 0.5% alcohol or less. Meanwhile, long-standing brewing traditions in Germany, Belgium, the Czech Republic, Poland, and Spain continue to support steady demand for roasted and caramel malts. At the same time, stable barley production, reinforced by the EU Common Agricultural Policy (CAP), guarantees a consistent supply of top-quality raw materials. Furthermore, as specialty malts are used more widely in baked goods, cereals, and malt-based foods, overall demand grows, cementing Europe’s standing as a mature specialty malt market with a strong focus on specialty malt innovation.

The specialty malt sector in Germany is expanding steadily, fueled by the nation’s craft brewing legacy and consumers’ growing preference for unique flavors, vibrant colors, and textured profiles. The continuing trend towards premium and artisanal beverages, as well as more frequent use of baked goods and food manufactured with malt, is further contributing to the industry’s growth. As Germany has a stable barley supply and a well-known reputation for producing high-class beer, malt supplies will be guaranteed, and this will support continued specialty malt market growth.

Steady growth in the UK specialty malt market is being supported by the thriving craft beer sector and strong demand for premium, flavorful drinks. Brewers are adopting specialty malts to enrich flavor profiles, deepen color, and add body to both alcoholic and low-alcohol beers. Meanwhile, the burgeoning use of these malts in artisanal baking and malt-based foods is expanding their applications, further encouraging market expansion. Supported by a reliable barley supply and established malting infrastructure, these factors are fostering steady and sustained growth in the UK specialty malt market.

North America Market Insights

The specialty malt market in North America is expected to hold a share of 29% by 2036. The market is largely shaped by innovation in craft and premium beers, where brewers prioritize rich flavors, unique colors, and a satisfying texture. In April 2025, Blue Ox Malthouse introduced seven new roasted specialty malts, including Chocolate Rye, Crystal 90/120, and Roasted Oats, enhancing both product innovation and regional supply for craft brewers and distillers across the US. This development is further supported by the strong quality of the 2025 malting barley crop in western Canada, where high test weights and plump kernels are ideal for producing specialty malts. Increased low and non-alcoholic beer production has led to greater use of specialty malts because of the fermentation process's reduced volume. Strong barley supply, supportive agricultural policies, and sophisticated malting infrastructure ensure consistent quality and promote product innovation.

In the U.S., the specialty malt market is growing as craft and premium beers continue to gain popularity, with brewers focusing on distinctive flavors, colors, and textures. The rising production of low- and non-alcoholic beers has driven the use of specialty malts to improve taste and mouthfeel. Beyond brewing, malt is being used more in natural-label baked goods, cereals, and malted drinks. Stable barley availability, strong farming support, and state-of-the-art malting facilities ensure quality consistency while promoting continuous product development, fueling market expansion.

The specialty malt market in Canada is expanding as craft and premium brewers look for unique flavors, colors, and textures in their products. The rise in the production of low-alcohol and non-alcoholic beers has also contributed to the use of specialty malts to enhance the taste and character of those beverages as well. Additionally, specialty grains are used in the production of natural-label baked goods, breakfast cereals, and processed malted beverages. In the past few years, there have been consistent barley harvests, government policies that favour the agricultural industry, and the establishment of new modern malt facilities, which contribute to the consistency and quality of malts produced and the continuing development of new and innovative malt products.

Asia Pacific Market Insights

Asia Pacific specialty malt market will grow with a market share of 28.7% by 2036, propelled by the surge in premium ready-to-drink (RTD) cocktails, where producers are using smoked or peat-roasted malts to imitate the flavor of Scotch whisky, or employing caramel malts to enhance color and richness without actually labeling the product as whisky, thereby avoiding excise taxes. This type of flavor innovation across categories is generating a large-scale demand separate from the beer industry. At the same time, dependable barley harvests, favorable agricultural policies, and modern malting facilities help maintain high-quality standards and support continuous product development throughout the region.

The specialty malt market in China is steadily expanding as craft and premium brewers place greater emphasis on rich flavors, vibrant colors, and unique textures. The growing production of low- and non-alcoholic beers has increased the use of specialty malts to improve taste and mouthfeel. Malt is also seeing rising demand in baked goods, cereals, malted beverages, and premium RTD cocktails, creating new opportunities for growth. As global craft breweries establish operations in China, local production must meet exacting technical requirements, boosting quality benchmarks and technical know-how.

The specialty malt market in India continues to grow as craft and premium breweries concentrate on distinctive taste profiles, rich colors, and unique textures. The rising production of low- and non-alcoholic beers, combined with increasing use of malt in baked goods, cereals, malted beverages, and premium RTD cocktails, is fueling demand. The entry of international craft breweries into India requires local production that meets precise technical standards, helping to raise quality benchmarks. Steady barley harvests, supportive agricultural policies, and modern malting facilities ensure consistent quality and support continuous product development across the country.

Key Specialty Malt Market Players:

- Barmalt Malting (India)

- Briess Malt & Ingredients Co. (U.S.)

- Canada Malting Co. Limited (Canada)

- Castle Malting (Belgium)

- Crisp Malt Group Ltd. (U.K.)

- InVivo / Soufflet Malt (France)

- IREKS GmbH (Germany)

- Malteurop Group (France)

- Mouterij Dingemans (Belgium)

- Muntons Plc (U.K.)

- Rahr Malting Co. / BSG (U.S.)

- Simpsons Malt Limited (U.K.)

- Thomas Fawcett & Sons Ltd (U.K.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Briess Malt & Ingredients Co. is one of the foremost producers of specialty malts worldwide due to its extensive portfolio of innovative malt varieties that cater to craft, premium, and low-/non-alcoholic beverages. The company invests heavily in research and development to create malts with unique flavors, colors, and functional properties that meet evolving brewer and consumer preferences. Briess maintains a strong global supply chain, ensuring consistent quality and timely delivery to breweries and beverage producers across different regions. Its close collaboration with brewers and beverage makers to define technical specifications and quality standards further strengthens its position as a trusted, high-quality specialty malt supplier worldwide.

- Canada Malting Co. Limited is recognized as one of the leading producers of specialty malts globally, offering a wide range of malt varieties tailored for craft, premium, and low- or non-alcoholic beverages. The company focuses on high-quality production, using advanced malting techniques and precise quality control to ensure consistency and flavor integrity. By maintaining strong regional and international supply chains, Canada Malting serves breweries and beverage producers worldwide, delivering malts that meet strict technical specifications.

- Crisp Malt Group Ltd. is a key player in the specialty malts worldwide, offering a broad portfolio of innovative malts for craft, premium, and low-/non-alcoholic beverages. The company emphasizes consistent quality through advanced malting processes and strict quality control, ensuring its products meet precise flavor, color, and functional requirements. By maintaining strong partnerships with brewers globally and supporting technical specifications for specialty malts, Crisp Malt Group has established itself as a trusted supplier that drives innovation and meets the evolving needs of the global brewing and beverage industry.

- Thomas Fawcett & Sons Ltd is a leading global supplier of specialty malts, supplying a wide range of high-quality malts for craft, premium, and specialty beverages. The company focuses on traditional malting expertise combined with modern production techniques to ensure consistent flavor, color, and performance. By working closely with brewers to meet precise technical specifications, Thomas Fawcett & Sons has built a reputation for reliability and innovation.

- Malteurop Group specializes in specialty malts, offering a wide range of high-quality malts for craft, premium, and low- or non-alcoholic beverages. The company emphasizes innovation and consistency, using advanced malting processes to deliver malts with precise flavors, colors, and functional properties. By maintaining strong global supply chains and partnering closely with brewers, Malteurop ensures that its malts meet strict technical specifications and quality standards.

Below is the list of the key players operating in the global specialty malt market:

Leading companies in the global specialty malt market are broadening their product lines with new malt varieties that provide distinctive flavors, colors, and functional qualities, catering to the changing tastes of craft and premium beverage consumers. They are focusing on research and development to produce malts specifically for low- and non-alcoholic beers, premium RTD cocktails, and other applications beyond traditional brewing, including baked goods and malted drinks. These firms are also enhancing regional supply by setting up local production or forming partnerships in key specialty malt markets, which allows faster delivery and better alignment with brewer requirements. Additionally, they collaborate closely with brewers and beverage makers to define technical standards and quality benchmarks, helping to improve overall product quality throughout the industry.

Corporate Landscape of the Global Specialty Malt Market:

Recent Developments

- In March 2025, Muntons introduced its Climate Positive Malt, claimed to be the UK’s lowest‑carbon malt for the craft brewing industry, offering up to 30 % lower CO₂ emissions per tonne compared with the UK malt average and helping brewers reduce their environmental impact while maintaining quality. The launch, timed with BeerX 2025 in Liverpool, reflects Muntons’ long‑standing focus on regenerative agriculture and sustainable barley farming to cut on‑farm emissions, support soil health, and meet rising demand for eco‑conscious products.

- In August 2024, Malteurop Malting Company (MMC) unveiled its new Pot Still Malt, designed for all-malt and high-malt distillation applications. The malt is crafted from AMBA-approved non-GN barley to ensure consistent performance, high spirits yield, and reduced ethyl carbamate formation. MMC Pot Still Malt builds on Malteurop’s more than 60 years of expertise in the distilling industry and supports today’s generation of distillers in producing premium all-malt and high-malt spirits.

- Report ID: 8303

- Published Date: Mar 10, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2036

Copyright @ 2026 Research Nester. All Rights Reserved.