Semaglutide Market Outlook:

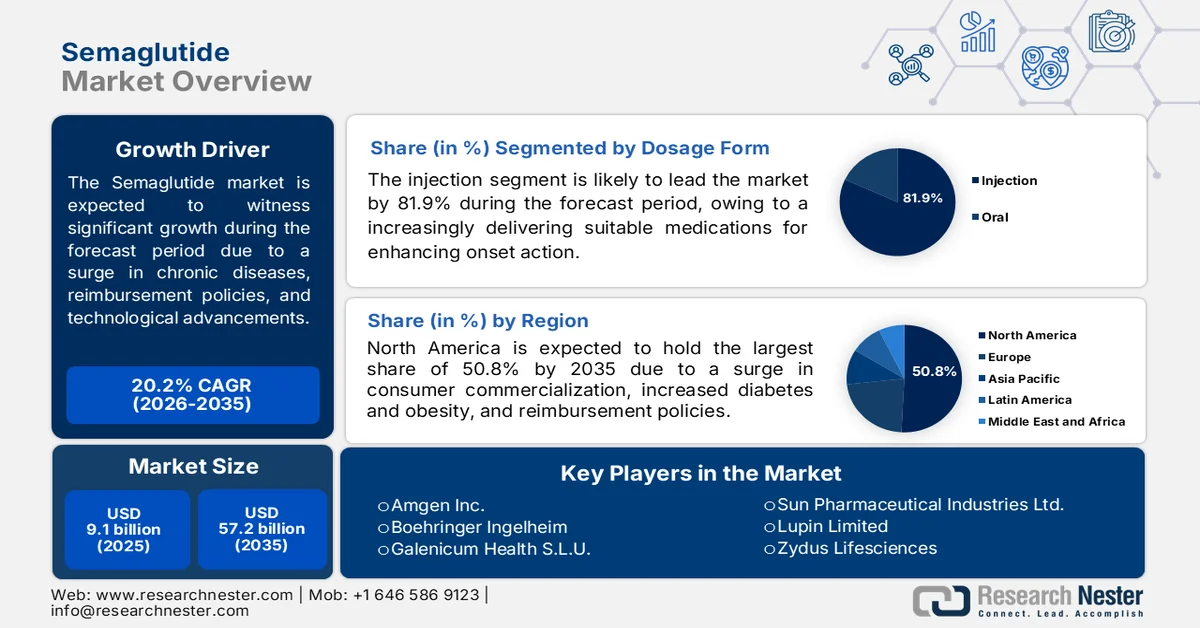

Semaglutide Market size was valued at USD 9.1 billion in 2025 and is projected to reach USD 57.2 billion by the end of 2035, registering around 20.2% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of semaglutide is assessed at USD 10.9 billion.

The global semaglutide market is continuously expanding, owing to patent expirations, competitive positioning, regional reimbursement policies, the rising prevalence of diabetes among the youth, technological innovations, growth in pharmacotherapy, and an expansion in telemedicine platforms. According to official statistics published by NLM in March 2023, the pharmacokinetic technique is adopted for ensuring drug development, for which the time-consuming process ranges between 10 and 12 years for reaching different economic utilization. Additionally, this also amounts to an estimated USD 2.6 billion as a generous investment and is also associated with the safety aspects of compounds. This particular opportunity eventually favors a few compounds in the overall developmental process, thereby making it suitable for bolstering the semaglutide market globally.

Furthermore, the shift towards preventive cardiometabolic care, the integration with wearable devices and digitalized health, the emergence of payer-based prior authorization and step therapy, along with direct-to-consumer advertising and social media influence, are certain trends that are responsible for driving the semaglutide market. As stated in an article published by the Journal of Medical Internet Research in February 2025, a survey-based study was conducted on 5,591 adults in the U.S. to examine wearable utilization and willingness. This study resulted in 36.3% wearable device adoption as of 2022. In addition, 78.4% are willing to adopt such devices, and 26.5% have readily adopted so far. Moreover, there was an increase in the utilization of wearables for higher income, ranging from USD 50,000 to USD 75,000, thus proliferating the market expansion.

Key Semaglutide Market Insights Summary:

Regional Highlights:

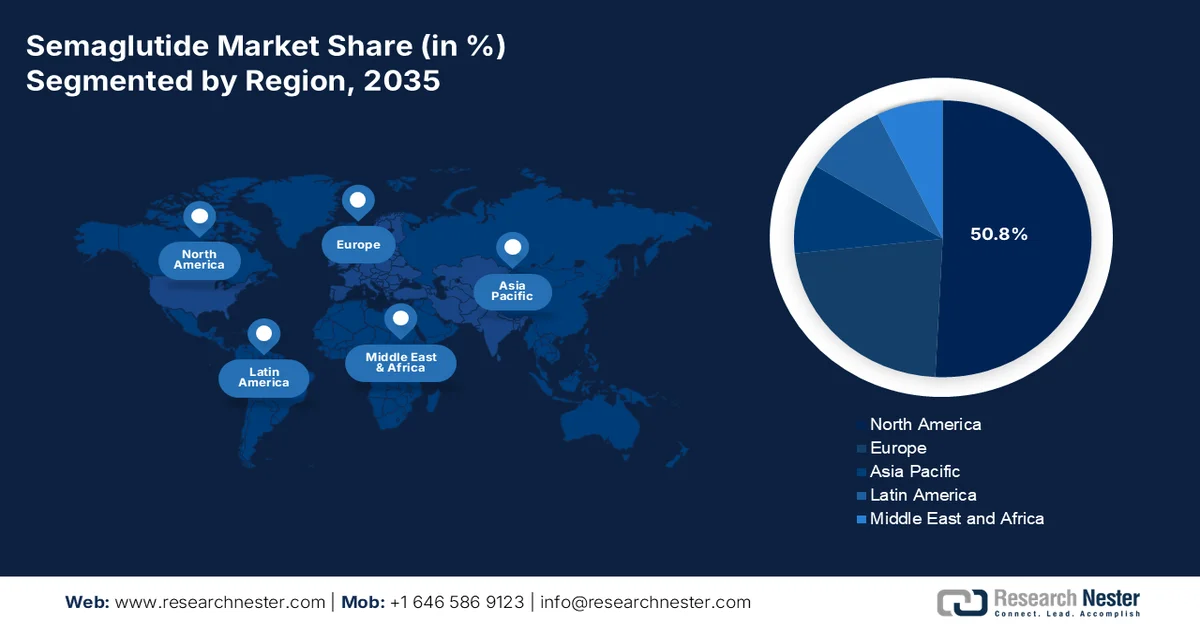

- North America in the semaglutide market is anticipated to secure a 50.8% share by 2035, with regional expansion being stimulated by strong direct-to-consumer commercialization, favorable reimbursement expansions, and high prevalence of diabetes and obesity

- Asia Pacific is poised to emerge as the fastest-growing regional market throughout 2026-2035, with momentum accelerated by expanding healthcare expenditure, rising GLP-1 receptor acceptance, increasing obesity and diabetes prevalence, and improved accessibility to generic and branded formulations

Segment Insights:

- The injection segment in the semaglutide market is projected to account for an 81.9% share by 2035, with segment progression being reinforced by delivering medications directly into the bloodstream, tissues, or muscles for enabling increased onset of action, treating uncooperative or unconscious patients, and bypassing the digestive tract to combat drug degradation

- The type 2 diabetes sub-segment is expected to capture the second-largest share during 2026-2035, with growth being energized by its recognition as a chronic condition wherein the body resists insulin or fails to produce sufficient insulin leading to high blood sugar levels

Key Growth Trends:

- Prevalence of dietary shifts

- Expansion in wellness programs

Major Challenges:

- Ethical concerns for off-label prescribing and cosmetic utilization

- Protein stability and cold chain requirements

Key Players: Novo Nordisk (Denmark), Eli Lilly and Company (U.S.), Pfizer Inc. (U.S.), F. Hoffmann-La Roche AG (Switzerland), AstraZeneca plc (UK), Amgen Inc. (U.S.), Boehringer Ingelheim (Germany), Galenicum Health S.L.U. (Spain), Abbott Laboratories (U.S.), Dr. Reddy's Laboratories (India), Sun Pharmaceutical Industries Ltd. (India), Lupin Limited (India), Zydus Lifesciences (India), Torrent Pharmaceuticals (India), Glenmark Pharmaceuticals (India), Alkem Laboratories (India), Natco Pharma (India), MSN Laboratories (India), Eris Lifesciences (India), Emcure Pharmaceuticals (India), Samsung Bioepis Co., Ltd. (South Korea), Epis NexLab Co., Ltd. (South Korea).

Global Semaglutide Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 9.1 billion

- 2026 Market Size: USD 10.9 billion

- Projected Market Size: USD 57.2 billion by 2035

- Growth Forecasts: 20.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (50.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, France

- Emerging Countries: India, South Korea, Brazil, Saudi Arabia, Indonesia

Last updated on : 27 May, 2026

Semaglutide Market - Growth Drivers and Challenges

Growth Drivers

- Prevalence of dietary shifts: The global transition toward increased consumption of high-calorie and processed food, reduced physical activity, and sedentary occupations, which is enhancing the semaglutide market. According to official statistics published by the USDA Government in June 2024, the aspect of spending on food constitutes an average expenditure share of 40%, particularly across low-income markets and 22% across middle-income nations. Besides, effectively focusing on income-based diets and the worldwide population growth of 39%, food calorie availability is expected to grow by 44% by the end of 2050, along with an increase in crop calories by 47%. Therefore, with the focus on these objectives, there is a huge growth opportunity for the semaglutide market across different regions.

- Expansion in wellness programs: An increase in employee numbers, especially in West Europe and North America, is significantly including semaglutide in employee assistance and workplace wellness programs. As stated in an article published by the Global Wellness Institute in 2025, the wellness economy has successfully doubled and effectively reached USD 6.8 trillion as of 2024. In addition, the economy is expected to witness a 7.6% growth in the upcoming 5 years and significantly reach approximately USD 9.8 trillion by the end of 2029. Besides, there has been suitable growth in long-lasting wellness by 6.5% yearly in 2024, while the worldwide gross domestic product (GDP) surged by 3.2% annually, thereby denoting a huge growth opportunity for the semaglutide market.

Global Wellness Economy Analysis, 2024

|

Categories |

Growth (USD) |

|

Traditional and Complementary Medicine |

606 billion |

|

Public Health, Prevention, & Personalized Medicine |

676 billion |

|

Healthy Eating, Nutrition, & Weight Loss |

1,148 billion |

|

Physical Activity |

1,144 billion |

|

Personal Care & Beauty |

1,350 billion |

|

Wellness Tourism |

894 billion |

|

Mental Wellness |

268 billion |

|

Wellness Real Estate |

548 billion |

|

Spas |

157 billion |

|

Springs |

72 billion |

|

Workplace Wellness |

53 billion |

Source: Global Wellness Institute

Challenges

- Ethical concerns for off-label prescribing and cosmetic utilization: The widespread public demand for semaglutide has led to significant off-label prescribing for patients who do not meet clinical criteria for diabetes or obesity treatment. This includes individuals seeking modest weight loss for cosmetic rather than medical reasons, such as bridal weight loss or beach body preparation. While physicians may legally prescribe approved medications for unapproved uses, this practice raises ethical concerns about resource allocation, particularly when supply shortages exist. Besides, patients with genuine medical needs for glycemic control or cardiovascular risk reduction may face medication delays or denials because manufacturing output is diverted to patients using semaglutide for aesthetic purposes, thus limiting the semaglutide market.

- Protein stability and cold chain requirements: Semaglutide is a peptide-based therapeutic that degrades rapidly when exposed to temperatures outside the narrow range. This thermal instability imposes strict cold chain requirements throughout the entire distribution pathway, from the manufacturing facility to the patient refrigerator. Besides, any break in the cold chain, whether during air transport, warehouse storage, local delivery, or patient handling, can render the medication ineffective or potentially unsafe. This requirement creates particular challenges in regions with unreliable electricity, hot climates, or limited access to medical-grade refrigeration. Moreover, rural pharmacies in developing countries may lack consistent power for vaccine coolers, let alone the monitored refrigerators required for pharmaceutical storage, thus negatively impacting the semaglutide market.

Semaglutide Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

20.2% |

|

Base Year Market Size (2025) |

USD 9.1 billion |

|

Forecast Year Market Size (2035) |

USD 57.2 billion |

|

Regional Scope |

|

Semaglutide Market Segmentation:

Dosage Form Segment Analysis

Based on the dosage form, the injection segment is anticipated to capture the largest share, at 81.9%, in the semaglutide market by the end of 2035. The segment’s upliftment is primarily driven by delivering medications directly into the bloodstream, tissues, or muscles for enabling increased onset of action, treating uncooperative or unconscious patients, and bypassing the digestive tract to combat drug degradation. According to official statistics published by NLM in August 2025, the aspect of one-to-one mapping analysis was conducted between the European Directorate for the Quality of Medicines & HealthCare (EDQM) pharmaceutical dose forms and those used by the U.S. FDA, Health Canada, Systematized Nomenclature of Medicine (SNOMED), and the Clinical Data Interchange Standards Consortium (CDISC). The pharmaceutical dosage form of Health Canada was 16%, and for the U.S. FDA, it was 22%, while CDISC was 20%, and SNOMED demonstrated a 45% match, thereby proliferating the segment’s growth.

Indication Segment Analysis

During the forecast period, the type 2 diabetes sub-segment, part of the indication segment, is projected to grab the second-largest share in the semaglutide market. The sub-segment’s growth is effectively fueled by its recognition as a chronic condition, wherein the body effectively resists insulin or is unable to produce enough of it, resulting in high blood sugar. As stated in an article published by the World Health Organization (WHO) in November 2024, globally, more than 95% of people impacted by diabetes suffer from type 2 diabetes. Besides, as per the May 2024 CDC Government article, over 40 million people in America have diabetes, which is almost 1 in 8. In addition, nearly 90% to 95% of the population in the region has type 2 diabetes, and it frequently develops among people aged more than 45 years, thereby enhancing the market growth and demand globally.

Distribution Channel Segment Analysis

The hospital pharmacies segment, which is part of the distribution channel, is expected to garner the third-largest share in the semaglutide market by the end of the stipulated period. The segment’s development is highly attributed to its role as a critical distribution channel for semaglutide, primarily serving as the initial point of prescribing and dispensing for newly diagnosed patients. Within a hospital setting, semaglutide is often initiated under direct physician supervision, particularly for patients with complex metabolic profiles, concurrent cardiovascular conditions, or those requiring careful dose titration. This channel is especially significant in markets where GLP-1 receptor agonists are first introduced during inpatient or specialty outpatient consultations. Moreover, hospital pharmacies benefit from robust inventory management systems, allowing for a consistent supply of temperature-sensitive formulations.

Our in-depth analysis of the semaglutide market includes the following segments:

|

Segment |

Subsegments |

|

Dosage Form |

|

|

Indication |

|

|

Distribution Channel |

|

|

End user |

|

|

Type |

|

|

Product |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Semaglutide Market - Regional Analysis

North America Market Insights

North America in the semaglutide market is anticipated to account for the highest share of 50.8% by the end of 2035. The market’s upliftment in the region is primarily attributed to strong direct-to-consumer commercialization, favorable reimbursement expansions, and the prevalence of high diabetes and obesity. According to official statistics published by the CDC Government in May 2024, the obesity prevalence among adults aged more than 20 years in the U.S. was 41.9%. Additionally, the prevalence of critical obesity among the population was 9.2%. This readily denotes that over 100 million adults are impacted by this disease, and more than 22 million suffer from severe obesity. Besides, there has been an increase in the occurrence from 30.5% in previous years and 4.7% surge in severe obesity, thereby making it suitable for enhancing the semaglutide market growth in the region.

The semaglutide market in the U.S. is growing significantly, owing to the presence of Medicare programs, private insurance coverage, cardiovascular risk reduction approvals by the FDA, intense brand competition, and oral formulation. As stated in an article published by the American Heart Association Journals in June 2024, cardiovascular diseases, such as stroke, atrial fibrillation, heart failure, and coronary heart disease, affect an estimated 9.9% of adults in the country, or approximately 28.6 million individuals. Besides, the demographic shift is yet another factor that affects people with stroke. For instance, 1 in 5 people will be aged more than 65 years by the end of 2030. Additionally, over 85 aged people is expected to be almost double by 2035, which is from 6.5 million to 11.8 million, and almost triple by 2060, which is 19 million, thereby bolstering the semaglutide market growth.

The single-payer public system, generic semaglutide approval, patent lapse due to missed maintenance fee, the presence of provincial supply protection laws, reimbursement models for obesity indication, and comprehensive societal value modeling are certain factors that are driving the semaglutide market in Canada. As per an article published by the Canadian Health Policy Journal in April 2026, the most-favored-nation (MFN) reference-specific drug pricing policy was launched by the government, demanding brand medicines without competitors to be set at the lowest pricing strategy, with a GDP per capita of nearly 60%. Based on this policy, the price conditions in the country have been expressed frequently as a suitable percentage reduction for achieving a low affordability threshold of USD 50,000 per quality-adjusted life-year, thus boosting the market upliftment.

APAC Market Insights

The Asia Pacific in the semaglutide market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by an expansion in healthcare expenditure, an increase in the acceptance of GLP-1 receptor, a rise in obesity and diabetes prevalence, a surge in the demand for effective glycemic control therapies, and improved accessibility to generic and branded formulations. According to official statistics published by NLM in July 2025, China is considered the largest economy in the region, which is followed by South Korea, India, and Japan, and these 4 countries readily control 70.8% of the regional economy and also significantly contribute to the top 15 GDPs. Moreover, doctors per 1,000 people are a notable indicator of the region’s health and medical spending, thus denoting an optimistic outlook for the semaglutide market’s growth.

The semaglutide market is gaining increased traction in Japan, owing to the existence of therapies, along with a rise in the remote work culture, the comprehensive adoption of sedentary lifestyles, an upsurge in chronic conditions, and the number of diabetic and obese patients. The Japan semaglutide market was valued at USD 242.7 million as of 2025, which is further projected to be worth USD 299.2 million by the end of 2026 and also increase to USD 1,955.5 million, along with a 23.2% growth rate by the end of 2035. As stated in an article published by NLM in March 2023, more than 90% of adults in the country aged more than 75 years have 1 chronic disease, and of these, an estimated 80% are impacted with multiple chronic diseases. Moreover, a clinical study was conducted on 2,481 internet users in the country, of which 24.5% suffered from hypertension, 10.1% from chronic lung disorder, 7.7% from anxiety disorder or depression, and 7.2% of cancer, thus enhancing the market demand.

The aspects of chronic weight management indications, governmental spending on diabetes care, a transformative development of biosimilars, national reimbursement strategies, improvement in patient accessibility, the growing awareness of innovative diabetes treatments, and provincial expansion are a few trends that are responsible for fueling the semaglutide market in China. As per an article published by NLM in February 2023, the diabetes prevalence in the country for adults aged between 20 and 79 years is predicted to increase from 8.2% to 9.7% by the end of 2030. Regarding this, the overall expenses of diabetes are also poised to surge from USD 250.2 billion to USD 460.4 billion, readily corresponding to a 6.3% yearly growth rate. In addition, the total expenses of diabetes in terms of GDP are also anticipated to increase from 1.5% to 1.6% by the same year, thus enhancing the market development.

Overall Projected Expenses of Diabetes (Direct and Indirect Costs in USD Billion) in China, 2019-2030

|

Province |

2019 |

2020 |

2025 |

2030 |

Yearly Growth Rate % during 2020-2030 |

|

Northeast |

|

|

|

|

|

|

Heilongjiang |

4.8 (3.8 and 0.9) |

5.1 (4.1 and 1.1) |

6.9 (5.5 and 1.4) |

8.5 (7.0 and 1.5) |

5.2 (5.6 and 3.5) |

|

Jilin |

4.4 (3.3 and 1.1) |

4.8 (3.6 and 1.2) |

6.6 (4.7 and 1.9) |

8.2 (5.9 and 2.3) |

5.6 (5.2 and 6.7) |

|

Liaoning |

9.7 (7.4 and 2.3) |

10.5 (8.0 and 2.6) |

14.5 (10.7 and 3.7) |

17.9 (13.8 and 4.1) |

5.4 (5.7 and 4.5) |

|

North |

|

|

|

|

|

|

Beijing |

17.8 (15.6 and 2.3) |

19.1 (16.6 and 2.5) |

26.1 (21.9 and 4.3) |

33.5 (27.8 and 5.7) |

5.8 (5.3 and 8.3) |

|

Hebei |

10.6 (8.6 and 2.0) |

11.5 (9.2 and 2.3) |

16.0 (12.6 and 3.4) |

20.4 (16.5 and 3.9) |

5.9 (6.0 and 5.4) |

|

Inner Mongolia |

5.8 (4.5 and 1.3) |

6.3 (4.9 and 1.4) |

9.1 (6.6 and 2.5) |

12.3 (8.7 and 3.7) |

7.0 (6.0 and 9.9) |

|

Shanxi |

6.0 (5.0 and 1.0) |

6.5 (5.3 and 1.2) |

9.1 (7.2 and 1.9) |

11.8 (9.4 and 2.5) |

6.2 (5.8 and 7.6) |

|

Tianjin |

5.3 (3.9 and 1.7) |

5.8 (4.2 and 1.6) |

8.1 (5.5 and 2.7) |

10.6 (7.0 and 3.6) |

6.2 (5.3 and 8.3) |

Source: NLM

Europe Market Insights

Europe in the semaglutide market is projected to witness considerable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively driven by suitable cross-country variation in reimbursement policies, rapid transformation, the existence of a decentralized healthcare system, generous NHS expenditure, and the regional health data space approach. According to official statistics published by the Frontiers Organization in March 2026, the average share of health expenditure in regional GDP surged significantly by 1 percentage point to 9.2%. Besides, in 2023, Switzerland was considered the biggest spender in the region, significantly accounting for USD 6,894.1 per person, which is followed by USD 6,608.6 in Norway and USD 6,301.5 in Germany. Meanwhile, the spending level in Finland, Denmark, Ireland, France, Luxembourg, Belgium, Sweden, the Netherlands, and Austria is above the average of USD 3,814, thus enhancing the market exposure.

Health Expenditure Analysis in Europe, 2023

|

Countries |

USD PPP (Million) |

USD PPP (per capita) |

GDP% |

|

Austria |

52,087.4 |

5,704.4 |

11.2 |

|

Belgium |

62,657.2 |

5,319.2 |

10.8 |

|

Bulgaria |

15,641.0 |

1,426.8 |

7.9 |

|

Croatia |

9,122.0 |

2,365.2 |

7.1 |

|

Cyprus |

3,104.0P |

3,253P |

8.1P |

|

Czechia |

36,988.3 |

3,404.3 |

8.4 |

|

Denmark |

28,886.5 |

5,485.4 |

9.5 |

Source: Frontiers Organization

The semaglutide market is gaining increased exposure in Germany, owing to structural benefits in the domestic healthcare system, the existence of the decentralized statutory health insurance, a strong private insurance sector, a pharmaceutical manufacturing base, and an expansion in continued label. As stated in an article published by the German Trade & Invest (GTAI) in 2026, the country’s pharmaceutical industrial revenue was worth USD 69.6 billion, along with a 6.4% yearly growth rate, and more than 600 pharma organizations. Besides, as of 2022, pharmaceutical companies in the country generously invested USD 11.1 billion in research and development, along with the registration of 613 patents within the regional patent office in terms of the pharma sector. Therefore, with all such developments in the domestic industry, the market is gradually growing in the country.

The healthcare technological appraisal, governmental strategies, the proactive formulary inclusion of weight management, an expansion in accessible volumes, and premium-priced next-generation therapies are certain trends that are boosting the semaglutide market in the UK. As per an article published by NLM in March 2026, 29% of adults in England resided with obesity, which is aggressively associated with increased cardiovascular risks as of 2022. Therefore, in terms of health management, the Government of England introduced a National Enhanced Service (NES) that readily reimburses USD 15.5 for each patient, recognized as suffering from obesity. Simultaneously, the National Health Service (NHS) Digital Weight Management Programme (DWMP) was also unveiled for people aged 18 years and above, thus fueling the market’s expansion.

Key Semaglutide Market Players:

- Novo Nordisk (Denmark)

- Eli Lilly and Company (U.S.)

- Pfizer Inc. (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- AstraZeneca plc (UK)

- Amgen Inc. (U.S.)

- Boehringer Ingelheim (Germany)

- Galenicum Health S.L.U. (Spain)

- Abbott Laboratories (U.S.)

- Dr. Reddy's Laboratories (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Zydus Lifesciences (India)

- Torrent Pharmaceuticals (India)

- Glenmark Pharmaceuticals (India)

- Alkem Laboratories (India)

- Natco Pharma (India)

- MSN Laboratories (India)

- Eris Lifesciences (India)

- Emcure Pharmaceuticals (India)

- Samsung Bioepis Co., Ltd. (South Korea)

- Epis NexLab Co., Ltd. (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Novo Nordisk readily dominates the global market with its branded products Ozempic, Wegovy, and Rybelsus. The company continues to defend its market leadership through aggressive capacity expansion, label extension studies, and next-generation pipeline development.

- Eli Lilly and Company leveraged its dual GIP/GLP-1 agonist tirzepatide (Mounjaro/Zepbound) to capture significant market share across diabetes and obesity indications. The company’s aggressive direct-to-consumer marketing and competitive pricing strategies have intensified rivalry in the branded GLP-1 space.

- Pfizer Inc. has strategically pivoted toward the oral GLP-1 segment, developing danuglipron as a potential once-daily pill to compete directly with Rybelsus. The company’s focus on small-molecule oral agents aims to overcome the manufacturing complexity and cold-chain requirements of injectable peptides.

- F. Hoffmann-La Roche AG has successfully adopted a partnership-driven approach, entering the GLP-1 arena through strategic licensing and co-development agreements rather than internal proprietary programs. The company is leveraging its diagnostics and digital health expertise to create integrated metabolic disease management solutions around GLP-1 therapies.

- AstraZeneca plc maintains a presence in the incretin-based therapy market through its established portfolio of DPP-4 inhibitors, while actively evaluating pipeline opportunities in next-generation GLP-1 multi-agonist molecules. The company’s strategy emphasizes cardiometabolic combination therapies that incorporate GLP-1 mechanisms alongside other cardiovascular protective agents.

Here is a list of key players operating in the global semaglutide market:

The global semaglutide market is characterized by a dominant innovator, Novo Nordisk in Denmark, which holds approximately the majority of the global supply through its patented products Ozempic, Wegovy, and Rybelsus. The competitive landscape is rapidly transforming following the March 2026 patent expiry in India, which triggered a wave of generic launches from over a dozen Indian manufacturers. Key strategic initiatives include licensing and supply agreements, such as Lupin's partnership with Spain's Galenicum for distribution across 23 countries, and Dr. Reddy's receiving regulatory approval in Canada through CDMO partner OneSource. Besides, in March 2026, Samsung Bioepis Co., Ltd., and Epis NexLab Co., Ltd., proclaimed a research collaboration and license agreement with G2GBIO for developing suitable assets, leading to propelling the semaglutide industry’s growth.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, Novo Nordisk declared that the Committee for Medicinal Products for Human Use (CHMP) under the European Medicines Agency (EMA) implemented the marketing commercialization of Wegovy® 7.2 mg, along with once-weekly injectable semaglutide 7.2 mg, in a single-dose pen for people living with obesity.

- In February 2026, Eli Lily and Company notified that the U.S. FDA accepted the label expansion for Zepbound® (tirzepatide) for effectively including the four-dose single-patient use KwikPen® that delivers a full month of treatment in one device.

- In March 2025, Roche entered into an outstanding licensing agreement and collaboration with Zealand Pharma for co-commercializing and co-developing petrelintide as a standalone therapy and a fixed-dose combination with Roche’s lead incretin asset CT-388.

- Report ID: 8588

- Published Date: May 27, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.