Retail Clinics Market Outlook:

Retail Clinics Market size was valued at USD 6.4 billion in 2025 and is projected to reach USD 14.3 billion by the end of 2035, rising at a CAGR of 8.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of retail clinics is estimated at USD 6.9 billion.

The global market is driven by the access gaps in the primary care vaccination demand and cost containment priorities documented by the public health agencies. According to the CDC, January 2026 data, there were nearly 1.0 billion physician office visits in the U.S., reflecting sustained outpatient demand across preventive and minor acute care services. Moreover, the 2026 Medical Professional Liability Association report indicates that over 10o million people in the U.S. live in designated Primary Care Health Professional Shortage Areas, indicating continued structural capacity constraints in the traditional care settings. Retail-based care delivery models are positioned within this broader outpatient ecosystem to absorb non-emergency cases, vaccinations, and routine screening. This trend is further supported by the decentralized care delivery across pharmacies and community-based retail locations.

Government expenditure patterns also support the continued integration of accessible outpatient channels. As per the CMS December 2023 data, the national health expenditure reached USD 4.5 trillion in 2022, representing 17.3% of GDP, with outpatient and physician services accounting for a significant share. Besides, the WHO December 2024 report shows that there is a global shortfall of 10 million health workers by 2030, concentrated in the primary care segment. This workforce imbalance has led health systems and payers to expand task shifting frameworks and alternative service sites to maintain coverage continuity. As governments prioritize vaccination preparedness, chronic disease screening, and minor illness management outside emergency departments, retail clinics are structurally aligned with national objectives focused on cost efficiency, geographic reach, and surge capacity management.

Key Retail Clinics Market Insights Summary:

Regional Highlights:

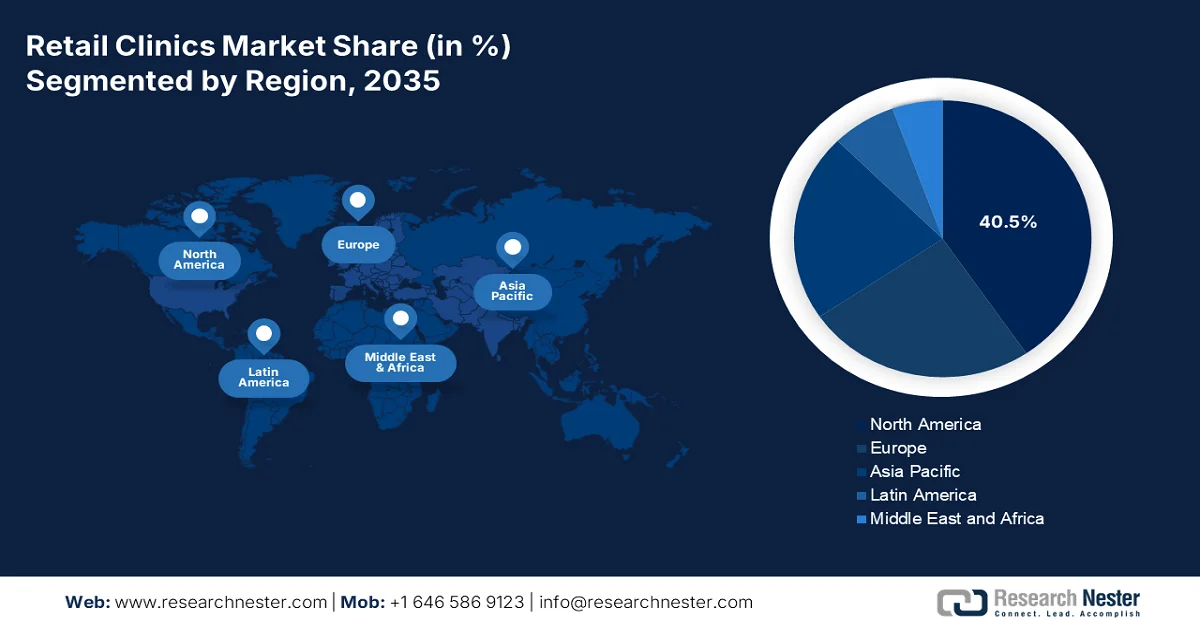

- The retail clinics market in North America is projected to command a 40.5% share by 2035, underpinned by a well-established retail healthcare ecosystem and rising preference for convenient walk-in care.

- Asia Pacific is forecast to register the fastest growth at a CAGR of 9.3% during 2026–2035, stimulated by rising healthcare expenditure and expanding middle-class demand for accessible care.

Segment Insights:

- The retail clinics market retail-owned clinics sub-segment is projected to account for a 60.3% share by 2035, reinforced by the strategic integration of healthcare services within established retail infrastructures and extensive consumer foot traffic.

- The in-store clinics segment is anticipated to maintain its leading position through 2035, strengthened by its embedded presence within pharmacies and supermarkets and accelerated by the growing consumer preference for convenient, walk-in care access.

Key Growth Trends:

- Vaccination infrastructure and public immunization funding

- Cost containment and avoidable emergency department visits

Major Challenges:

- Profitability and sustainable business model challenges

- High competition from traditional healthcare providers:

Key Players: CVS Health (U.S.), Walgreens Boots Alliance (U.S.), The Kroger Co. (U.S.), Walmart Inc. (U.S.), Rite Aid Corp. (U.S.), Target Brands Inc. (U.S.), Kaiser Permanente (U.S.), Concentra Inc. (U.S.), FastMed Urgent Care (U.S.), Doctors Care (U.S.), NEXtCARE (U.S.), U.S. HealthWorks (U.S.), Sutter Health (U.S.), AFC Doctors Express (U.S.), Geisinger Health (U.S.), Baptist Medical Group (U.S.), Smile2impress (Spain), Terveystalo (Finland), Affidea (Portugal), AniCura (Sweden).

Global Retail Clinics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.4 billion

- 2026 Market Size: USD 6.9 billion

- Projected Market Size: USD 14.3 billion by 2035

- Growth Forecasts: 8.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Canada, Germany, Japan

- Emerging Countries: India, Vietnam, Singapore, South Korea, Brazil

Last updated on : 18 February, 2026

Retail Clinics Market - Growth Drivers and Challenges

Growth Drivers

- Vaccination infrastructure and public immunization funding: Mass immunization programs significantly drive the traffic to community-based clinics. According to the report stated in the WHO February 2024 data, it is registered that nearly 9 million doses of influenza vaccine were produced in 2023, and in total, 80 million doses of influenza vaccine were supplied by the manufacturer. Moreover, the funds in billions were allocated for COVID-19 vaccination to expand the decentralized immunization capacity. WHO continues to emphasize the life course immunization strategies in national budgets globally. Further, the retail clinics market is additionally benefitted from the government-backed procurement and public vaccination campaigns.

- Cost containment and avoidable emergency department visits: Governments are targeting non-urgent emergency department use as a cost burden. The U.S. Agency for Healthcare Research and Quality reports that millions of emergency department visits annually are for non-emergent conditions treatable in outpatient settings. Further, the value-based reimbursement models are tested continuously, which avoids hospital utilization. Moreover, the government analysis shows avoidable hospital admissions remain a persistent cost driver across the member countries. The market offers lower cost treatment for minor acute conditions aligning with these containment objectives. The policy reforms penalizing non-urgent emergency visit utilization often increase the insurer incentives to redirect patients toward retail-based outpatient models, supporting the demand expansion.

- Convenience and accessibility: The fundamental driver for the retail clinics market growth remains the unparalleled convenience they offer via strategic locations in pharmacies, supermarkets, and shopping centers where consumers already spend time. This accessibility overcomes the traditional barriers to care, such as appointment scheduling, extended wait times, and limited operating hours. According to the Census.gov data in March 2023, 97% of the retail health clinics in the U.S. are located in metropolitan areas, positioning them precisely where population density ensures maximum utilization. For suppliers and manufacturers, this geographic concentration creates predictable demand patterns for point-of-care diagnostics and basic treatment supplies, as clinics in high-traffic urban locations require consistent inventory replenishment to serve steady patient volumes.

Challenges

- Profitability and sustainable business model challenges: The most significant roadblock in the market is achieving profitability in primary care delivery within retail settings. The retail clinics operate on thin margins and require high patient volumes to break even, unlike traditional healthcare providers that can offset losses with specialty producers and higher revenue services. Though the market is expected to grow, the major players continue to struggle with unsustainable economics. Manufacturers supplying specialized equipment to these clinics face demand volatility when operators suddenly contract or exit markets entirely.

- High competition from traditional healthcare providers: In the market, the suppliers must navigate intense competitive pressures from established healthcare systems that view retail entrants as threats. The traditional providers use their existing patient relationships, physician network, and integrated care models to compete effectively. This competition limits patient volume growth for retail clinics, constraining their purchasing capacity for new equipment and supplies.

Retail Clinics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.4% |

|

Base Year Market Size (2025) |

USD 6.4 billion |

|

Forecast Year Market Size (2035) |

USD 14.3 billion |

|

Regional Scope |

|

Retail Clinics Market Segmentation:

Ownership Segment Analysis

The retail-owned clinics sub-segment dominates and is expected to hold the share value of 60.3% by 2035. This leadership position is built upon the ability of major chains such as CVS Health, Walgreens, and Walmart to integrate healthcare delivery directly into their existing commercial infrastructure using significant foot traffic and established brand trust. According to the Association of American Medical Colleges' June 2021 data, it is estimated that there were 1,949 retail clinics in the U.S., demonstrating the scalable nature of this ownership model. This co-location strategy reduces the overhead costs while offering unparalleled patient convenience, creating a sustainable economic model that is difficult for hospital-owned counterparts to replicate without the operational expertise and real estate portfolio of a retail parent company.

Clinic Type Segment Analysis

In-store clinics represent the largest and most influential clinic type within the retail clinics market, distinguished by their physical integration within the pharmacies, supermarkets, and big box retail environments. These walk-in facilities are typically staffed by nurse practitioners or physician assistants and offer treatment for minor illnesses, diagnostic services, and immunizations, operating with extended hours that accommodate working adults. Moreover, the massive number of doses is administered via retail partners, proving the infrastructure’s capability for widespread public health deployment. This model’s dominance stems from its ability to transform routine shopping tips into healthcare visits, effectively capturing the demand from consumers seeking immediate attention for common ailments without the wait times and costs associated with traditional emergency departments or urgent care centers.

Location Segment Analysis

Retail pharmacy settings constitute the leading location sub-segment in the market. Pharmacies serve as natural healthcare touchpoints where patients already interact with medical professionals for prescriptions and advice. The strategic placement of clinics within or adjacent to pharmacies creates a seamless care continuum where the patients can receive a diagnosis and immediately fill the prescriptions, reducing the medication abandonment rates and improving the treatment adherence. According to the Urgent Care Association report in August 2023, nearly 78% of U.S. people live within a 10-minute drive of a retail clinic, highlighting the exceptional accessibility that pharmacy-based location provides. This proximity to consumers, combined with the trust associated with established pharmacy brands, positions retail pharmacy settings as the preferred location for delivering convenient, affordable primary care services to diverse populations across metropolitan and suburban areas.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Ownership |

|

|

Application |

|

|

Location Type |

|

|

Service Type |

|

|

Patient Type Demographics |

|

|

Payment Model |

|

|

Technology Integration |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Retail Clinics Market - Regional Analysis

North America Market Insights

North America is anticipated hold the largest share of 40.5% by the end of 2035. This dominance is driven by an established retail healthcare ecosystem, high healthcare expenditure, and increasing preference for convenient walk-in care. The major metropolitan areas in the U.S. and Canada lead the adoption, supported by the high foot traffic and diverse patient populations. The policy initiatives aimed at reducing healthcare costs and improving access in regions with primary care physician shortages further boost the market growth. The market in North America is also benefiting from the expansion of service offerings beyond minor illness treatment to include preventive screenings and chronic disease management, positioning retail clinics as integral components of the broader healthcare delivery system.

The rising absorbing noncomplex primary care visits, reshaping outpatient service distribution, are driving the retail clinics market in U.S. According to the Association of American Medical Colleges June 2021 data, 39% of retail clinic visits substitute for physician office visits, 3% replace emergency department visits, and 58% represent new utilization, suggesting incremental demand expansion rather than full displacement of traditional providers. Besides 4,550 pediatric retail visits offsetting demand for one pediatrician, 5,430 adult retail visits offset one adult primary care physician, based on MGMA ambulatory encounter benchmarks. Further, the report has projected a shortfall of 102,400 physicians (13%) overall, including a 16% gap in Primary Care (35,500 physicians). These data are significant for the market because retail clinics predominantly manage low-acuity, noncomplex primary care conditions. Overall, these data show a rising demand for the U.S. market growth.

Health Care Utilization Equity Scenario

|

Specialty Group |

Current Supply |

Requirements Under Equity Scenario |

Current Gap (Physicians) |

% Gap |

Advanced Practice Nurses Required |

Physician Assistants Required |

|

Total |

808,400 |

910,800 |

102,400 |

13% |

18,100 |

9,500 |

|

Primary Care |

228,700 |

264,200 |

35,500 |

16% |

7,900 |

1,200 |

|

Non-Primary Care |

579,700 |

646,600 |

66,900 |

12% |

10,200 |

8,300 |

|

Medical Specialties |

137,900 |

156,500 |

18,600 |

13% |

3,800 |

1,800 |

|

Surgical Specialties |

152,700 |

166,600 |

13,900 |

9% |

1,600 |

3,400 |

|

Other Specialties |

255,800 |

288,300 |

32,500 |

13% |

4,000 |

2,900 |

|

Hospitalists |

33,300 |

35,200 |

1,900 |

6% |

800 |

200 |

Source: According to the Association of American Medical Colleges June 2021

Primary care access constraints, rising public health expenditure, and expanded scope of practice for pharmacists and nurse practitioners are driving the growth for market in Canada. According to the 2026 Canadian Medical Association data, the total health spending in Canada reached USD 344 billion, representing 12.1% of GDP, with continued growth in physician and community-based care spending. Besides, the access gaps remain a central issue. The Canadian Medical Association's December 2025 data reported that approximately 5.9 million adults did not have a regular healthcare provider, increasing reliance on walk-in and retail-based clinics. Further sustained national immunization programming, including seasonal influenza campaigns targeting millions annually. Moreover, the public spending growth, uninsured primary care demand, pharmacist scope expansion, and preventive health funding are reinforcing structural demand in Canada.

APAC Market Insights

The Asia Pacific retail clinics market is projected to be the fastest-growing region globally and is growing at a CAGR of 9.3% during the forecast period 2026 to 2035. The region's growth is fueled by rising healthcare expenditure, a growing middle-class population demanding accessible care, and supportive government policies towards private healthcare providers. China is expected to lead this expansion and is driven by the rapid urbanization, government healthcare reforms, and the increasing prevalence of chronic diseases. Moreover, the key trends include the integration of digital health technologies such as AI-powered diagnostics and telemedicine platforms, particularly in mature markets like South Korea and Singapore, alongside the expansion of retail clinic networks in high-growth countries like Vietnam and India.

The expanding public insurance coverage, rapid urbanization, workforce constraints, and large-scale preventive health programs are propelling the market in India. As per the PIB September 2024, under the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana, more than 55 crore beneficiaries are eligible for the cashless secondary and tertiary care coverage, increasing the formal healthcare utilization across low and middle-income populations. At the primary care level, the government has operationalized over 1,81,873 Ayushman Arogya Mandirs to strengthen community-based service delivery, expanding screening and basic treatment access, based on the PIB January 2026 report. Additionally, rapid urban population growth is increasing demand for convenient, walk-in care formats, thereby making a suitable place for market upliftment.

The retail clinics market in China is shaped by the primary care system reform, urbanization, aging demographics, and expansion of the community-level medical institutions. According to the NLM June 2024 study, China had 1,032,918 medical and health institutions nationwide, including 979,768 grassroots institutions and 36,976 hospitals, reflecting the continued expansion of community-level care infrastructure. While the number of rural township health clinics declined to 33,917 and village health centers to 587,749, overall system capacity strengthened, with total national bed capacity reaching 9.75 million, including 1.744 million beds in grassroots institutions. Notably, rural township health clinics increased their bed capacity to 1,455,876 beds despite a decline in the facility count, indicating the consolidation and scaling of the service capability. Hospital beds rose to 7.663 million, reinforcing outpatient referral integration. These dynamics signal the growing opportunities in the market in China.

Europe Market Insights

The market's development is driven by the increasing consumer preference for accessible and affordable healthcare, mainly among the aging populations and those managing chronic diseases. The market in Europe is expanding significantly, and the key trends include the integration of digital health solutions such as telemedicine and electronic health records to enhance operational efficiency and patient experience. Besides the service expansion into preventive care, chronic disease management, and mental health, alongside partnerships between the retailers and healthcare providers, are also shaping the competitive landscape of the market in the region. Further, the growth is supported by the established infrastructure and investment capabilities.

The retail clinics market in Germany is influenced by statutory health insurance expansion, outpatient cost management, and physician workforce constraints. According to the Federal Ministry of Health, April 2025 data, Germany operates under a statutory health insurance system covering 90% of the population and ensuring broad reimbursement eligibility for the ambulatory services. However, in rural regions, where physician shortages have been documented by the Federal Ministry of Health, policy support for alternative outpatient delivery models. Demographic trends further reinforce demand. As per the NLM study, September 2023 reports that over 18.6 million of Germany’s population was aged 65 or older in 2022, increasing the need for routine monitoring, vaccination, and minor acute care services, hence driving the market growth.

The National Health Service capacity constraints, rising outpatient demand, and expanded community pharmacy services are fueling the market in the UK. Primary care access pressures are an important driver for the market growth. According to the NHS, October 2023 data, over 362 million general practice appointments were delivered in 2023, indicating the record utilization levels and ongoing strain on the general practice capacity. Besides, the workforce shortages are also influencing demand redistribution, with the British Medical Association reporting persistent general practice staffing gaps across regions. To address these constraints, the UK government expanded the Pharmacy First initiative in 2024, enabling community pharmacists to manage seven common conditions without GP referral, supported by NHS funding allocations. This accelerates community-based care delivery and patient access, driving a positive market impact.

NHS Primary Care Appointment Activity and Delivery Metrics

|

Category |

Metric |

September 2023 Data |

|

GP Practice Appointment Systems |

Total Appointments Delivered |

32.6 million |

|

Of which: COVID-19 Vaccinations |

1.5 million |

|

|

Primary Care Network (PCN) Appointment Systems |

Additional Appointments Delivered |

791,000 |

|

PCNs Reporting Separate System Data |

67.5% of PCNs |

|

|

Same Day Appointments |

Appointments Occurring Same Day as Booking |

39.7% |

|

Appointment Status |

Appointments Attended |

88.7% |

|

Appointments by Clinician Type |

Conducted by GP |

43.9% |

|

|

Conducted by Nurses |

22.1% |

|

Appointment Mode |

Face-to-Face Appointments |

70.7% |

Source: According to the NHS, October 2023

Key Retail Clinics Market Players:

- CVS Health (U.S.)

- Walgreens Boots Alliance (U.S.)

- The Kroger Co. (U.S.)

- Walmart Inc. (U.S.)

- Rite Aid Corp. (U.S.)

- Target Brands Inc. (U.S.)

- Kaiser Permanente (U.S.)

- Concentra Inc. (U.S.)

- FastMed Urgent Care (U.S.)

- Doctors Care (U.S.)

- NEXtCARE (U.S.)

- U.S. HealthWorks (U.S.)

- Sutter Health (U.S.)

- AFC Doctors Express (U.S.)

- Geisinger Health (U.S.)

- Baptist Medical Group (U.S.)

- Smile2impress (Spain)

- Terveystalo (Finland)

- Affidea (Portugal)

- AniCura (Sweden)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- CVS Health is executing a transformative strategy to integrate its vast network with the primary care providers. This approach aims to create a seamless healthcare ecosystem by connecting pharmacists and physicians to deliver more comprehensive value-based care within the market. According to the 2024 annual report, more than 36 million people were served from the CVS Health.

- Walgreens' strategy in the retail clinics market has been centered on a major investment in primary care via its partnership with VillageMD. The company invested to become the majority owner and committed to opening hundreds of co-located clinics to transform the stores into comprehensive health destinations. In 2024, 300,000 people were accessing pharmacies first initiative.

- The Kroger Co. leads in the retail clinics market, and the grocery chain operates the Little Clinic locations inside its stores, offering walk-in medical services alongside pharmacies and dietitians. The company’s pharmacy business has been a key driver of the sales growth, fueled by the strong prescription volumes.

- Walmart Inc is another global leader in the retail clinics market. After a significant retreat from physical operations in the retail clinics market, Walmart has pivoted to a new digital strategy. The company has launched a digital health marketplace that connects customers to third-party telehealth providers such as Doctor on Demand.

- Rite Aid Corp.'s approach to the retail clinics market has evolved via partnerships and operational structuring. The company previously partnered with RediClinic to open in store clinitcs, aiming to provide convenient and affordable healthcare access. These efforts unfold against a backdrop of significant financial distress, as the company navigates its second bankruptcy in recent years.

Here is a list of key players operating in the global market:

The global retail clinics market is very competitive, featuring a mix of large retail corporations and healthcare providers primarily from the U.S. The competitive landscape is characterized by strategic initiatives focused on integrating technology, such as telemedicine and AI-driven diagnostics, to enhance the patient experience and expand the service reach. The key players are also pursuing partnerships with insurers and health systems to develop integrated care models and tap into value-based reimbursement. For example, in January 2023, Carlyle backed VLCC to ramp retail clinics to 175 by the end of the year. However, the market is leading to a strategic pivot towards more sustainable partnership-based models and a focus on understanding local population needs.

Corporate Landscape of the Retail Clinics Market:

Recent Developments

- In June 2025, Amazon launched a service called Clinic in India that allows users to consult with doctors online. With Amazon Diagnostics, customers in 6 cities across 450+ PIN codes can easily book from over 800 diagnostic tests, get doorstep sample collection in under 60 minutes, and digital reports in as little as 6 hours, for routine tests.

- In April 2025, Walmart Canada announced the opening of its first pharmacy clinic in St. Catharines, Ontario, with additional clinics opening later this year. The new in-store clinic space will enhance our licensed pharmacists' ability to provide direct consultations and healthcare services within their expanded scope of practice to our St. Catharines patients, beyond dispensing medication via the pharmacy.

- In May 2024, Sumitomo Corporation will make a full-scale entry into the fast-growing private clinic business in Southeast Asia through investment in CareClinics Healthcare Services, which operates private medical clinics in Malaysia.

- Report ID: 4411

- Published Date: Feb 18, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.