Residential Energy Management Market Outlook:

Residential Energy Management Market size was valued at USD 5.6 billion in 2025 and is projected to reach USD 27.4 billion by the end of 2035, rising at a CAGR of 19.3% during the forecast period, i.e., 2026-2035. In 2026, the industry size of residential energy management is estimated at USD 6.6 billion.

There is a huge opportunity for the residential energy management market to grow, mainly driven by homeowners adopting improved home technologies and energy analytics platforms to monitor and optimize their energy usage. According to the official statistics by the U.S. Energy Information Administration as of December 2023, in U.S. homes, more than half of annual energy consumption is used for space heating and air conditioning, whereas water heating, lighting, and refrigeration account for about a quarter, and the remaining energy powers appliances and electronics. It also underscored that electricity and natural gas are the primary energy sources, contributing around 44% and 43% of residential energy use in a particular year. Meanwhile, petroleum, renewables, and other fuels are also used considerably at lower rates. Since the energy use varies by home type, size, location, household members, and equipment efficiency, there is a huge potential for residential energy management systems to capitalize on.

Furthermore, the aspects of supportive government programs, rising demand for efficient energy use, and cost savings are efficiently stimulating the growth of the residential energy management market. For instance, the data from the U.S. Environmental Protection Agency, which was published in January 2023, shows that its ENERGY STAR program has certified the first mass-market smart home energy management system by enabling homeowners to track, control, and automate energy use across lighting, appliances, thermostats, EV chargers, and solar panels. Certified systems, such as Samsung SmartThings, offer energy-saving features such as occupancy-based optimization, standby limits, demand response capabilities, and integration with utility time-of-use pricing, making energy management simple and efficient. Moreover, this initiative promotes nationwide energy savings, cost reduction, and reduced carbon footprints by enhancing the smart home experience.

Key Residential Energy Management Market Insights Summary:

Regional Highlights:

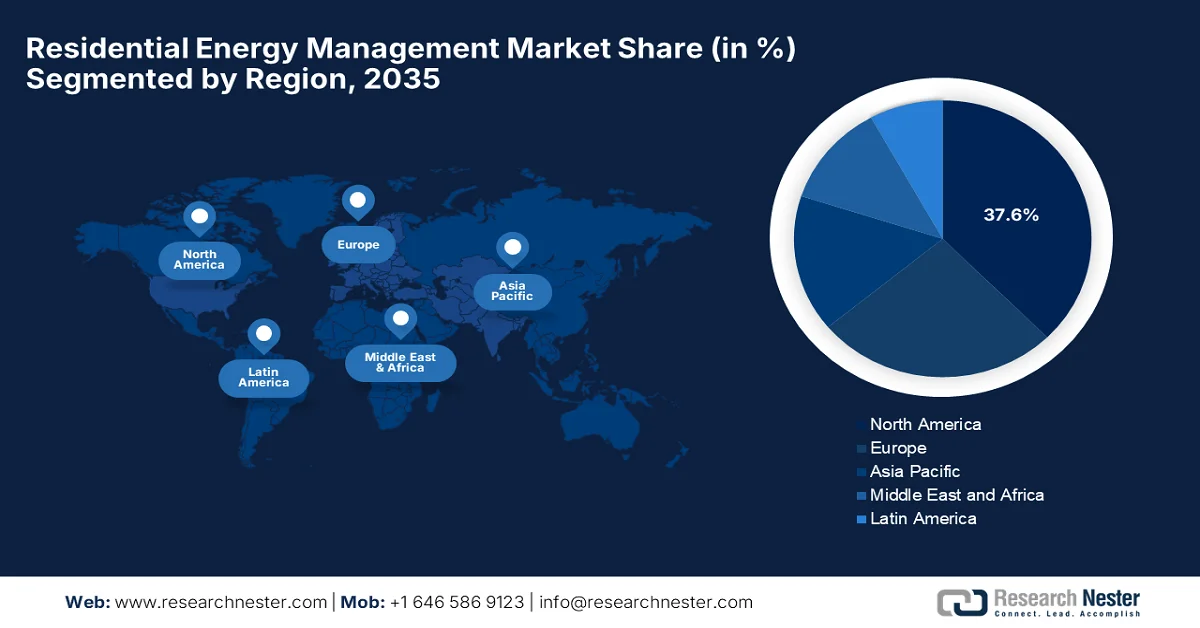

- The North America residential energy management market is projected to capture 37.6% of revenue share by 2035, impelled by rising consumer awareness of power efficiency and sustainability supported by strong government incentives for renewable energy integration and residential upgrades.

- Asia Pacific is anticipated to register the fastest growth during 2026–2035, stimulated by rapid urbanization, surging electricity demand, and proactive government-backed green building and energy-efficiency initiatives.

Segment Insights:

- The Hardware segment is projected to account for a 48.8% revenue share by 2035 in the residential energy management market, propelled by the expanding deployment of smart meters, thermostats, inverters, and load control devices.

- The HVAC Control segment is expected to secure a considerable share by 2035, driven by the high electricity consumption associated with residential space heating and cooling.

Key Growth Trends:

- Rising energy costs

- Smart home technology adoption

Major Challenges:

- Interoperability and lack of standardization

- Limited consumer awareness and engagement

Key Players: Schneider Electric SE (France), Honeywell International Inc. (U.S.), Siemens AG (Germany), General Electric Company (U.S.), Johnson Controls International plc (Ireland), Eaton Corporation plc (Ireland), ABB Ltd. (Switzerland), Panasonic Holdings Corporation (Japan), Samsung Electronics Co., Ltd. (South Korea), LG Electronics Inc. (South Korea), Ecobee Inc. (Canada), Vivint Smart Home, Inc. (U.S.), Comcast Cable Communications, LLC (U.S.), Alphabet Inc. (Google Nest, U.S.), EnergyHub, Inc. (U.S.), Itron Inc. (U.S.), Landis+Gyr (Switzerland), Tata Power (India), NeoSilica (India), TeraHive (Australia).

Global Residential Energy Management Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.6 billion

- 2026 Market Size: USD 6.6 billion

- Projected Market Size: USD 27.4 billion by 2035

- Growth Forecasts: 19.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (37.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, Brazil, South Korea, Australia, Canada

Last updated on : 17 February, 2026

Residential Energy Management Market - Growth Drivers and Challenges

Growth Drivers

- Rising energy costs: The residential energy management market is crucial to sustain rising utility and electricity expenses, which are encouraging homeowners to optimize their spending. These solutions help to reduce bills, thereby boosting demand across established and emerging regions. According to the official statistics by Ofgem in February 2025, there was a 6.4% increase in the UK energy price cap for April to June 2025, raising typical annual bills for dual-fuel households by £111 (approximately USD 136) to £1,849 (approximately USD 270) due to higher wholesale prices and inflationary pressures. This rise indicates that there is a growing financial burden on consumers, making energy conservation and residential energy management solutions important in such instances. It also stated that the government-backed measures, such as the Warm Home Discount expansion and debt relief initiatives, aim to support households in managing these higher electricity costs.

- Smart home technology adoption: The rise in smart home trend is an influential factor boosting adoption in the residential energy management market. There has been a surging uptake of smart devices, enabling proper monitoring and automated control, making energy management more accessible and useful for consumers across the world. According to the article published by NIH in October 2023, observed that smart homes integrate various sorts of automation technologies, allowing residents to monitor and control household appliances on a remote basis, which supports energy management. It also notes that adoption is influenced by certain benefits, social impact, cost, and security concerns, which shape user acceptance over the years. Therefore, based on this, smart homes play an essential role in enhancing residential power efficiency, thereby enabling more effective energy management solutions for households.

- Advanced metering infrastructure: This is a major growth driver for the residential energy management market since it provides real-time visibility into household energy consumption. By collecting detailed usage data, AMI enables both consumers and utilities to make suitable decisions. In this context Ministry of Power in February 2026 revealed that under India’s revamped distribution sector scheme, as of December 2025, more than 5.28 crore smart meters have been installed in the country, providing consumers with near real-time visibility of electricity consumption through mobile applications. These smart meters help households monitor usage, optimize energy consumption, and enable prepaid billing, while also improving utilities’ revenue collection and reducing losses. Hence, this is an indication that there is a huge opportunity for players to capitalize on this field.

Smart Meter Installation Progress in India 2023-2026: State-wise Data on Consumer, DT, and Feeder Meters Under RDSS

|

State/UTs |

Consumer Meters (Nos.) Sanctioned |

Consumer Meters (Nos.) Installed |

DT Meters (Nos.) Sanctioned |

DT Meters (Nos.) Installed |

Feeder Meters (Nos.) Sanctioned |

Feeder Meters (Nos.) Installed |

Total Meters (Nos.) Sanctioned |

Total Meters (Nos.) Installed |

|

Andaman & Nicobar |

83,573 |

- |

1,148 |

- |

114 |

- |

84,835 |

- |

|

Andhra Pradesh |

56,08,846 |

21,56,269 |

2,93,140 |

74,389 |

17,358 |

8,192 |

59,19,344 |

22,38,850 |

|

Arunachal Pradesh |

2,87,446 |

47,941 |

10,116 |

311 |

688 |

263 |

2,98,250 |

48,515 |

|

Assam |

63,64,798 |

46,72,329 |

77,547 |

57,731 |

2,782 |

2,879 |

64,45,127 |

47,32,939 |

|

Bihar |

23,50,000 |

19,74,061 |

2,50,726 |

1,82,145 |

6,427 |

5,775 |

26,07,153 |

21,61,981 |

|

Chhattisgarh |

59,62,115 |

32,32,660 |

2,10,644 |

66,023 |

6,720 |

5,936 |

61,79,479 |

33,04,619 |

|

Delhi |

- |

- |

766 |

- |

2,755 |

- |

3,521 |

- |

|

Goa |

7,41,160 |

- |

8,369 |

- |

827 |

- |

7,50,356 |

- |

|

Gujarat |

1,64,87,100 |

34,42,740 |

3,00,487 |

1,28,600 |

- |

- |

1,67,87,587 |

35,71,340 |

|

Himachal Pradesh |

28,00,945 |

7,02,046 |

39,012 |

22,054 |

1,951 |

1,603 |

28,41,908 |

7,25,703 |

Source: Ministry of Power

Challenges

- Interoperability and lack of standardization: This is a major barrier, causing hindrance to the residential energy management market progression. Devices from different manufacturers need to operate in terms of proprietary platforms and communication protocols that can cause compatibility challenges. The existence of this fragmentation makes it difficult for homeowners to integrate multiple smart devices into a unified and efficient system. Also, the absence of universal standards increases the risk of technological obsolescence, thereby negatively impacting long-term investments in this field. In this context, integration with older wiring systems or conventional meters can be technically complex as well as expensive. Furthermore, for service providers and utilities, inconsistent standards lead to complicated, large-scale deployment and grid integration.

- Limited consumer awareness and engagement: The absence of consumer awareness about the benefits offered by the residential energy management systems is also a considerable bottleneck for the industry to grow over the forecasted years. Most of the homeowners are not so familiar with how these systems operate and their role in reducing energy costs and environmental impact. Also, the misconceptions around the complexity, reliability, and maintenance requirements are hampering adoption in the residential energy management market. Even when systems are installed, user engagement is low due to complicated interfaces or insufficient education. In addition, without proper communication regarding cost savings and environmental advantages, consumers may not opt for these solutions, in turn requiring coordinated efforts from manufacturers, utilities, and policymakers.

Residential Energy Management Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

19.3% |

|

Base Year Market Size (2025) |

USD 5.6 billion |

|

Forecast Year Market Size (2035) |

USD 27.4 billion |

|

Regional Scope |

|

Residential Energy Management Market Segmentation:

Component Segment Analysis

Hardware is expected to dominate, capturing the largest revenue share of 48.8% in the residential energy management market. The leadership of the segment is highly propelled by smart meters, thermostats, inverters, and load control devices. In February 2026, Adani Energy Solutions Limited (AESL) reported that it had become the first company in India to deliver 1 crore smart meters across discoms, thereby supporting India’s smart metering rollout under the government’s Revamped Distribution Sector Scheme. In addition, the company’s advanced metering infrastructure provides real-time consumer insights, enhances billing transparency, and strengthens grid operations, allowing an increased uptake. Therefore, from a strategic perspective, the dominance of hardware will accelerate digital transformation and enable smarter, more efficient energy consumption.

Application Segment Analysis

By the conclusion of the forecast period, the HVAC control is expected to attain a considerable share in the residential energy management market. The growth of the segment is mainly driven by space heating and cooling, which represent the biggest residential electricity consumption category. In May 2025, Generac announced that it had officially launched the ecobee smart thermostat enhanced with home energy management by integrating smart HVAC control with Generac’s standby generators and PWRcell 2 solar battery systems. It also stated that the device intelligently optimizes heating and cooling based on occupancy, reducing energy consumption and improving efficiency, with reported savings of up to 26% on annual HVAC bills. Such developments from the leading pioneers will efficiently boost energy management by targeting the largest electricity end-use category, space heating and cooling.

End user Segment Analysis

The single-family homes, which are a part of end use segment, will grow at a significant rate in the residential energy management market during the stipulated timeframe. These homes have higher per-unit energy loads, rooftop solar adoption, and EV charging integration, increasing REM deployment, necessitating a proper energy management solution. There has been an increased adoption of rooftop solar panels, which allows homeowners to generate their own electricity, whereas the rising integration of electric vehicle chargers elevates household energy demands. As a result, single-family residences are looking for advanced REM solutions to optimize electricity use, manage peak loads, and coordinate distributed energy resources. Therefore, this combination of higher energy loads and evolving clean energy technologies positions this segment as a key driver of REM deployment in the residential sector.

Our in-depth analysis of the residential energy management market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Application |

|

|

End user |

|

|

Technology |

|

|

Communication Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Residential Energy Management Market - Regional Analysis

North America Market Insights

The North America residential energy management market is forecasted to be the largest regional landscape, capturing 37.6% of revenue share by 2035. The region’s augmentation is mainly propelled by rising consumer awareness of power efficiency and sustainability. The market benefits from supportive government initiatives that are proactively promoting renewable energy integration, coupled with incentives for reducing residential energy consumption. Based on the government data that has been put forth by Energy Star through December 31, 2025, U.S. homeowners can claim up to USD 3,200 in federal tax credits for energy-efficient home improvements by covering upgrades such as windows, doors, insulation, and heating/cooling systems. It was also mentioned that the residential clean energy credit offers 30% of costs for solar panels, wind turbines, geothermal heat pumps, fuel cells, and battery storage, hence denoting a positive residential energy management market outlook.

2025 Federal Tax Credits for Energy-Efficient Home Upgrades and Residential Clean Energy Equipment

|

Upgrade / Equipment |

Maximum Credit |

Credit Rate |

|

Heat Pumps, Water Heaters, Biomass Stoves |

USD 2,000 |

30% |

|

Windows & Skylights, Doors, Insulation |

USD 1,200 |

30% |

|

Residential Clean Energy Equipment (solar, wind, geothermal, fuel cells, battery storage) |

- |

30% |

Source: Energy Star.gov

The rapid technological innovation and high consumer penetration of smart energy devices are the main drivers which are responsible for the U.S. residential energy management market growth. Urban areas in the country are the main adopters of residential solar paired with energy management platforms, which are enhancing grid stability. On the other hand, regional policies that are focused on carbon reduction and clean energy also encourage the implementation of these energy monitoring systems in households. In October 2024, Schneider Electric announced that it had launched Schneider Home, which is a fully integrated residential energy management solution that combines solar, battery storage, EV charging, and utility power, all controlled through a single app. It is efficiently supported by financial incentives such as the Inflation Reduction Act, thereby making energy management more accessible for U.S. residents.

The need for efficient heating and cooling solutions due to the country’s varying climate conditions is the key fueling factor boosting the residential energy management market in Canada. Smart grids and integration with renewable energy sources, such as residential solar, are gaining momentum, increasing the uptake of the market. As of the January 2026 data from the country’s government, the Canada Greener Homes Initiative helps homeowners and tenants make their homes more energy efficient, save on energy bills, create jobs, and combat climate change. Programs such as the oil-to-heat-pump affordability program provide grants up to USD 25,000 for eligible households to switch from oil heating to heat pumps. Energy advisors, service organizations, and HVAC professionals play a key role in delivering these initiatives, which are available through federal and provincial partnerships, hence contributing to a wider residential energy management market expansion.

APAC Market Insights

The Asia Pacific residential energy management market is anticipated to register the fastest growth from 2026 to 2035. The region’s market is highly driven by urbanization, rising electricity demand, and increasing awareness of energy efficiency. Governments across the region are proactively promoting green building standards, supporting market growth in the years ahead. In this context, METI in November 2025 revealed that Japan’s Cabinet has approved the FY2025 supplementary budget to strengthen support for energy-efficient residential buildings under the Home Energy Conservation 2026 campaign. It also stated that the Ministries of Economy, Trade and Industry, Environment, and Land, Infrastructure, Transport and Tourism jointly provide subsidies for energy-saving renovations, which include high-efficiency water heaters, insulated windows, and EcoJozu appliance replacements. The program also supports new construction of GX-oriented, long-term quality, and ZEH-standard homes, prioritizing households with children and young couples, hence creating an optimistic residential energy management market opportunity.

Japan FY2025 Residential Energy Efficiency Subsidies and Incentives for Homes (JPY & USD)

|

Initiative |

Implementing Ministry |

FY2025 Budget (JPY Billion) |

Key Subsidy Details |

|

High-efficiency water heaters |

METI |

57 (approximately USD 427.5 million) |

Fixed subsidy per unit; additional support for replacing old heaters in cold regions |

|

EcoJozu appliance replacement (rental apartments) |

METI |

3.5 (approximately USD 26.3 million) |

¥50,000–¥70,000 per unit (approximately USD 375-USD525) depending on reheating function |

|

Insulated window retrofits |

Ministry of Environment |

112.5 (approximately USD 843.8 million) |

Up to ¥1,000,000 per household (approximately USD 7,500), depending on insulation work |

|

Energy-saving renovation (openings, framework, etc.) |

MLIT |

30 (approximately USD 225 million) |

Subsidy up to ¥1,000,000 per home (approximately USD 7,500), depending on pre/post renovation standards |

|

New energy-efficient homes (GX-oriented, long-term, ZEH) |

MLIT & Environment |

175 (approximately USD 1.31 billion) |

Subsidy range ¥350,000–¥1,250,000 per unit (approximately USD 2,625–USD 9,375) based on home type and household category |

Source: METI

The government’s push for smart city initiatives and energy saving programs is a factor that is responsible for fueling growth in the China residential energy management market. The proliferation of IoT-enabled smart devices in residential settings allows for the management of energy usage. Regional energy policies deliberately emphasize demand-side management, making smart energy systems an attractive option for homeowners. In November 2024, the Ministry of Industry and Information Technology of China released the guidelines for the construction of a comprehensive standardization system for smart homes and began taking public feedback. The guidelines aim to establish a proper framework for smart home development, including intelligent energy management, device interoperability, and IoT integration; hence, there is a lucrative opportunity for the residential energy management market to grow.

Rising urbanization, increasing electricity demand, and rising awareness of energy conservation are identified as the foundational factors driving the residential energy management market in India. Intelligent meters along with energy monitoring devices have gained enhanced adoption among middle- and upper-income households, allowing a steady cash flow in this sector. Government initiatives are mainly focused on incentives for power-efficient appliances, which support the deployment of residential energy management solutions. PIB in January 2026 stated that India is undergoing huge transformations in its energy transition, facilitated by improved clean energy infrastructure, policy reforms, and households' adoption of cleaner fuels. It also highlighted that by the published timeline, the initiatives such as the Pradhan Mantri Ujjwala Yojana reached around 10.41 crore households, supporting emissions reduction and energy security.

Europe Market Insights

Europe residential energy management market is reaping advantages from strong regulatory support for energy conservation and carbon reduction. The region’s market also benefits from smart grid infrastructure and home automation technologies. In addition, consumer interest in sustainability and energy cost savings drives adoption, creating encouraging opportunities for both domestic and foreign players operating in the region. In April 2024, the European Commission reported that its joint research centre has launched the code of conduct for energy smart appliances to ensure cross-brand interoperability of connected home devices, which allows households to shift electricity use based on grid conditions. The initiative is backed by 10 major manufacturers, and it covers appliances such as washing machines, dishwashers, heat pumps, and HVAC systems, promoting demand-side flexibility and grid stability, hence enhancing the environmental performance of residential energy use.

The high importance of lower energy consumption and renewable integration is responsibly uplifting the residential energy management market in Germany. The market is also witnessing the integration of electric vehicle charging with home energy management platforms, increasing demand for energy optimization. Based on the government data from Germany, which was published in March 2025, stated that there has been an accelerated rollout of smart meters as a key part of its energy transition. It also mentioned that since the May 2023 legal reforms, more than 1.15 million intelligent metering systems have been installed, thereby allowing households in the country to monitor and manage electricity use more efficiently. Furrhermore these intelligent meters integrate renewable energy and controllable devices, thus denoting an optimistic outlook for the residential energy management market’s exposure.

The UK residential energy management market maintains a prominent position in the regional landscape, propelled by the focus on lowering power use across households. Consumers in the country are opting for platforms that provide real-time feedback on energy usage and help manage peak demand. For instance, in January 2026, the country’s government announced that it had launched the Warm Homes Plan to upgrade up to 5 million homes with heat pumps, solar panels, batteries, insulation, etc. helping families reduce energy bills and combat fuel poverty. The public investment amounted to a total of £15 billion (approximately USD 18.3 billion), and the initiative concentrates on low-income households, renters, and social housing, by also offering government-backed loans for all homeowners to adopt clean energy technologies. Hence, with continued investments, the residential energy management market will grow at a significant rate in the country.

Key Residential Energy Management Market Players:

- Schneider Electric SE (France)

- Honeywell International Inc. (U.S.)

- Siemens AG (Germany)

- General Electric Company (U.S.)

- Johnson Controls International plc (Ireland)

- Eaton Corporation plc (Ireland)

- ABB Ltd. (Switzerland)

- Panasonic Holdings Corporation (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- LG Electronics Inc. (South Korea)

- Ecobee Inc. (Canada)

- Vivint Smart Home, Inc. (U.S.)

- Comcast Cable Communications, LLC (U.S.)

- Alphabet Inc. (Google Nest, U.S.)

- EnergyHub, Inc. (U.S.)

- Itron Inc. (U.S.)

- Landis+Gyr (Switzerland)

- Tata Power (India)

- NeoSilica (India)

- TeraHive (Australia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Schneider Electric SE has registered itself as one of the most important international leaders in energy management and automation solutions, which has an enhanced portfolio of products in residential energy systems and smart home platforms. The firm majorly benefits from strong global presence, rising R&D investments, and strategic acquisitions, which are suitable to bolster its leadership in REM solutions worldwide.

- Honeywell International Inc. is based in the U.S. and has a remarkable presence in building and residential energy automation. The company is best known for delivering integrated energy monitoring and management solutions, which include connected thermostats, HVAC controls, and software packages.

- Siemens AG is yet another prominent player in this field that has deeper knowledge in digitalization and smart infrastructure in the residential space. In addition, the firm is recognized for its smart grid technologies, and it has expanded into home energy optimization products for improved comfort and reduced costs.

- Alphabet Inc., through its Google Nest brand, is identified as a major innovator in this field. The company is mainly focused on intelligent thermostats that learn occupant patterns to optimize heating and cooling for energy efficiency, which is making it a key player in residential energy management appliances.

- ecobee Inc. is a specialized player that is mainly focused on smart thermostats, occupancy sensors, and connected devices that enhance residential energy efficiency. Besides the company’s acquisition by Generac has readily expanded its strategic potential into integrated energy solutions.

Below is the list of some prominent players operating in the global residential energy management market:

The residential energy management market hosts both long-established industrial pioneers and technology-driven firms. Global leaders such as Schneider Electric, Honeywell, and Siemens are leveraging extensive product portfolios and international distribution networks to maintain scale. The U.S.-specific players are focused on smart thermostats and analytics platforms, which efficiently boost consumer-centric innovation. Growth strategies across the sector are partnerships with utilities, AI-enabled energy analytics, acquisitions to broaden software capabilities, and regionally localized smart home solutions. In January 2025, ABB announced that it had acquired Lumin to integrate Lumin’s flexible platform for electrification, solar, and storage solutions, enabling smarter, more efficient home energy use, hence positively impacting the residential energy management market’s growth and exposure.

Corporate Landscape of the Residential Energy Management Market:

Recent Developments

- In February 2026, FranklinWH reported that it had partnered with Origin Energy to offer its first virtual power plant program in Australia. The collaboration allows FranklinWH customers to participate in Origin’s Loop VPP, maximizing the value of their home energy systems.

- In February 2026, Hoymiles notified that it had launched its all-in-one residential battery energy storage system, HiOne, in Amsterdam. The company also signed agreements with leading distributors in Europe to support the product’s rollout across the region.

- In January 2026, ABB announced that it had launched ReliaHome Flex, which is a modular residential energy management system that allows homeowners to add appliances such as EV chargers, water heaters, and HVAC systems without costly service upgrades.

- Report ID: 3658

- Published Date: Feb 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.