Regenerative Medicine Market Outlook:

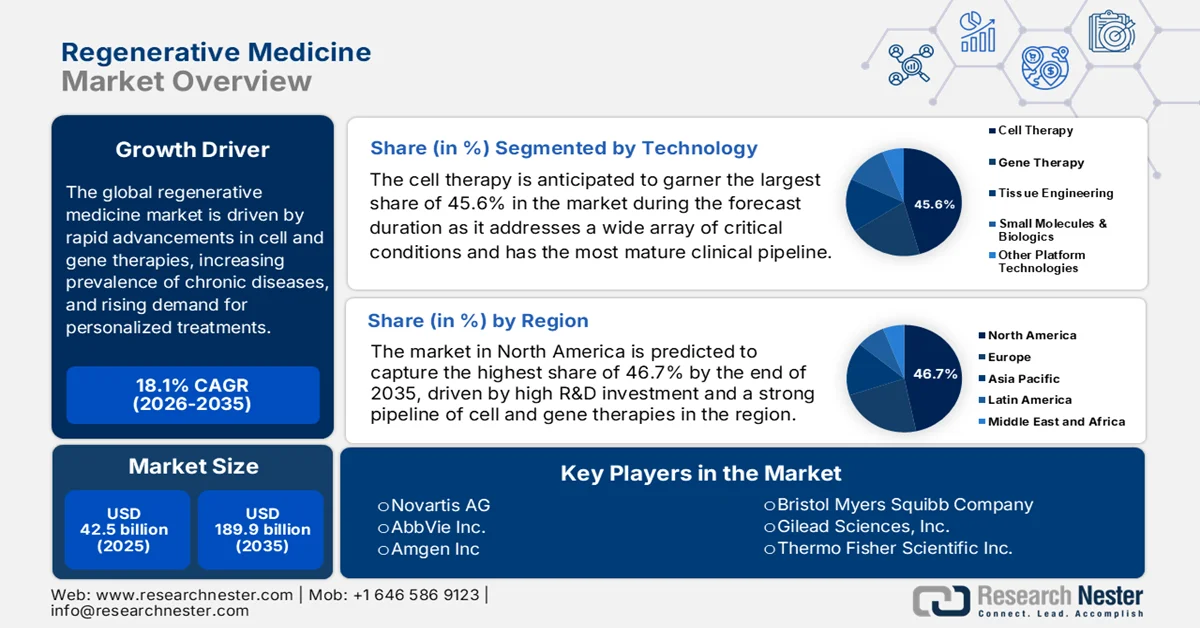

Regenerative Medicine Market size was USD 42.5 billion and is projected to surpass almost USD 189.9 billion by the end of 2035, rising at a CAGR of 18.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of regenerative medicine is evaluated at USD 50.2 billion.

The global regenerative medicine market is experiencing a transformative shift from experimental research to scalable therapies, which is fueled by the rising prevalence of chronic and neurodegenerative diseases and a growing aging population. In August 2024, the Centers for Disease Control and Prevention (CDC) revealed that dementia is a growing global health challenge, with 6.7 million older adults in the U.S. currently living with Alzheimer’s disease, the most common form. This number is projected to nearly double to 14 million by 2060, which reflects the urgent need for awareness and intervention. Alzheimer’s accounts for almost 60% to 80% of dementia cases, while vascular dementia makes up about 5% to10%. Importantly, the key context for understanding long‑term demand pressures on regenerative medicine therapies that target or intersect with neurodegenerative disease management and clinical research.

Key trends reshaping the future of the market are the shift toward personalized medicine and the integration of AI and 3D bioprinting for enhanced therapeutic production to improve patient access. In this context, as per the official release by Open Access Government in December 2025, regenerative medicine for osteoarthritis is entering a new phase with the discovery of small pluripotent stem cells, which are the naturally occurring cells that are found in peripheral blood that can be enriched without complex manipulation. Unlike mesenchymal stem cells, SPSCs fit within minimal-manipulation regulatory pathways, making them safer and more compliant for clinical use. A new device-based preparation platform, Stempheresis, is being developed to integrate SPSCs into established workflows. The research found that SPSCs may offer a transformative, accessible, and regulatorily robust approach to treating OA by harnessing the body’s own repair system, thus creating new growth opportunities for players in this field.

Key Regenerative Medicine Market Insights Summary:

Regional Highlights:

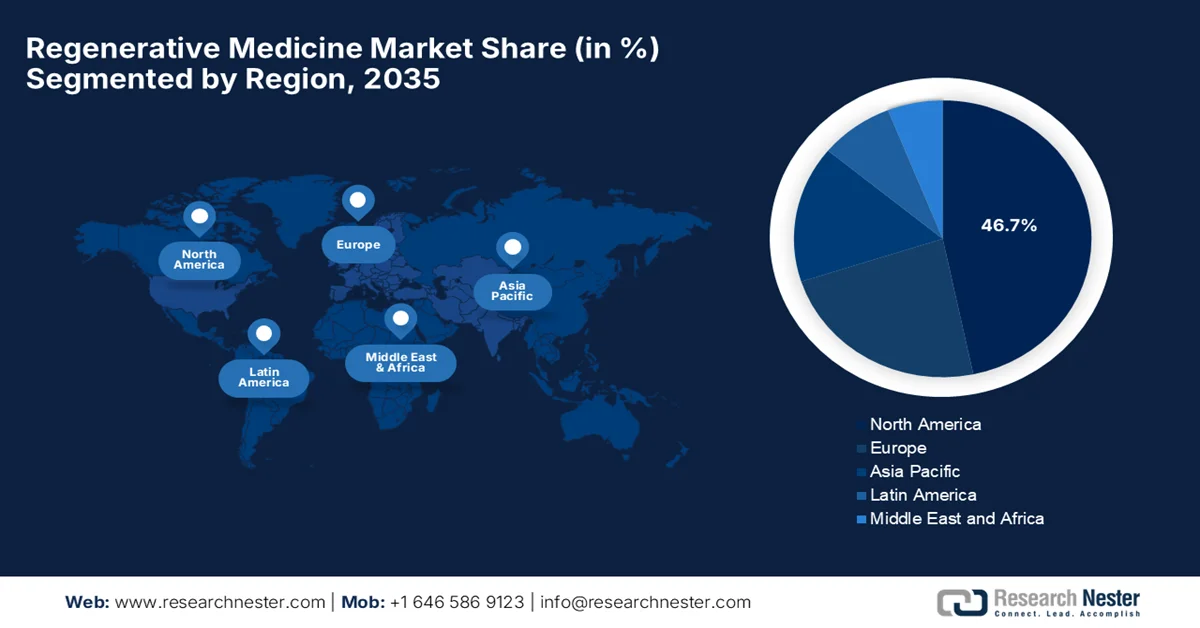

- North America in the regenerative medicine market is projected to command a 46.7% share by 2035, attributed to robust healthcare infrastructure, substantial R&D investments, and an enabling regulatory landscape fostering accelerated therapy approvals

- Asia Pacific is poised to witness the fastest growth over 2026–2035, fueled by supportive government initiatives and progressive regulatory reforms accelerating clinical development and investments

Segment Insights:

- Cell therapy segment in the regenerative medicine market is estimated to capture 45.6% share by 2035, propelled by its broad therapeutic applicability and the advancement of a highly mature clinical pipeline

- Orthopedics and musculoskeletal application segment is expected to expand significantly during 2026–2035, driven by the rising prevalence of musculoskeletal disorders and increasing adoption of stem cell-based therapies

Key Growth Trends:

- Advancements in technology

- Strong R&D pipeline and clinical trials

Major Challenges:

- Manufacturing complexity and scalability

- Regulatory and ethical barriers

Key Players: Novartis AG (Switzerland), AbbVie Inc. (U.S.), Amgen Inc. (U.S.), Bristol-Myers Squibb Company (U.S.), Gilead Sciences, Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), Smith & Nephew plc (UK), Medtronic plc (Ireland), Bluebird Bio, Inc. (U.S.), CRISPR Therapeutics (Switzerland), Takeda Pharmaceutical Company Limited (Japan), JCR Pharmaceuticals Co., Ltd. (Japan), Mesoblast Ltd (Australia), RACTHERA Co., Ltd. (Japan), Sumitomo Pharma (Japan), Sumitomo Chemical (Japan).

Global Regenerative Medicine Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 42.5 billion

- 2026 Market Size: USD 50.2 billion

- Projected Market Size: USD 189.9 billion by 2035

- Growth Forecasts: 18.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (46.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Japan, Germany, United Kingdom, China

- Emerging Countries: South Korea, India, Singapore, Australia, Canada

Last updated on : 9 April, 2026

Regenerative Medicine Market - Growth Drivers and Challenges

Growth Drivers

- Advancements in technology: The improvements in terms of stem cell therapy, gene therapy, and tissue engineering are readily transforming treatment approaches in the market. Innovations such as gene editing, e.g., CRISPR, and biomaterials enable the repair or replacement of damaged tissues and organs, thus making regenerative medicine more effective. As stated by Press Information Bureau (PIB) in November 2025, India launched the country’s first-ever indigenous CRISPR-Cas9-based gene therapy, i.e., BIRSA 101, for sickle cell disease, particularly benefiting tribal populations. It was developed by CSIR-Institute of Genomics and Integrative Biology, and the therapy signals India’s decisive move toward a sickle cell–free future and affordable advanced healthcare. Therefore, such improvements strengthen public–private collaboration to scale low-cost gene therapies, thus positively impacting the market’s growth and exposure.

- Strong R&D pipeline and clinical trials: The burgeoning number of clinical trials and product pipelines in cell and gene therapies is also a major growth booster for the market. Remarkable investments by biotech and pharma companies to develop next-generation therapies are prompting a profitable business ecosystem, allowing continuous product launches and market expansion. According to the article published by the National Institute of Health (NIH) in November 2023, advanced genetic therapies, including gene, cell, and RNA approaches, are witnessing strong clinical expansion, with more than 5,500 active trials despite fewer in vivo gene editing studies when compared to the broader pipeline. Data from the American Society of Gene and Cell Therapy shows oncology dominating clinical research, especially in gene and cell therapies, whereas infectious diseases lead RNA-based trials, thus suitable for bolstering market expansion.

Global Advanced Genetic Therapies Clinical Trial Statistics (2021-2023): Gene, Cell & RNA Therapy Market Trends, Pipeline Growth, and Oncology Dominance

|

Category |

Value |

|

Total known clinical trials (all time) |

18,185 |

|

Active clinical trials |

5,572 (31%) |

|

Active cell therapy trials |

4,163 |

|

Active gene therapy trials |

2,233 |

|

Active RNA therapy trials |

930 |

|

Oncology share (gene therapy trials) |

80% (1,776 trials) |

|

Oncology share (cell therapy trials) |

68% |

|

Infectious disease shares (RNA therapies) |

53% |

|

Oncology share (RNA therapies) |

18% |

|

In vivo gene editing trials initiated (2022) |

13 |

|

Gene transfer trials initiated (2022) |

77 |

|

Gene transfer trials initiated (2021) |

97 |

|

Noncoding RNA trials initiated (2021) |

141 |

|

Noncoding RNA trials initiated (2022) |

119 |

|

mRNA trials for infectious diseases |

429 (384 for COVID-19) |

|

Noncoding RNA active trials |

421 |

|

mRNA active trials |

509 |

|

Cell therapy trials (autoimmune/inflammation) |

475 |

|

Cell therapy trials (CNS) |

257 |

|

Cell therapy trials (infectious diseases) |

213 |

Source: NIH

- Shift toward personalized medicine: Regenerative therapies are often patient-specific, i.e., autologous treatments. At the same time, there has been a heightened demand for targeted, precision-based therapies, which is accelerating adoption across healthcare systems. In June 2024, NIH revealed that personalized medicine is transforming healthcare by integrating molecular profiling, multi-omics technologies, and AI-based data analysis to deliver precise diagnostics and targeted therapies that are suitable for individual patients. Meanwhile, advances such as whole genome sequencing, liquid biopsy, and gene editing technologies such as CRISPR-Cas9 are enabling early disease detection, improved treatment outcomes, and breakthroughs in areas such as cancer and rare genetic disorders, hence indicating a positive outlook for the market’s upliftment globally.

Approved Gene & Cell Therapy Products: Key Details, Companies, Indications, and Global Approvals

|

Product Name |

Generic Name |

Originator Company |

Diseases |

Year First Approved |

Locations Approved |

|

Vyjuvek |

Beremagene geperpavec |

Krystal Biotech |

Epidermolysis bullosa |

2023 |

U.S. |

|

Adstiladrin |

Nadofaragene firadenovec |

Merck |

Bladder cancer |

2022 |

U.S. |

|

Hemgenix |

Etranacogene dezaparvovec |

uniQure |

Hemophilia B |

2022 |

U.S., EU, UK |

|

Roctavian |

Valoctocogene roxaparvovec |

BioMarin |

Hemophilia A |

2022 |

EU, UK |

|

Upstaza |

Eladocagene exuparvovec |

PTC Therapeutics |

Aromatic L-amino acid decarboxylase deficiency |

2022 |

EU, UK |

|

Carvykti |

Ciltacabtagene autoleucel |

Legend Biotech |

Myeloma |

2022 |

U.S., EU, UK, Japan |

|

Skysona |

Elivaldogene autotemcel |

Bluebird Bio |

Adrenoleukodystrophy |

2021 |

U.S. |

|

Delytact |

Teserpaturev |

Daiichi Sankyo |

Brain cancer |

2021 |

Japan |

|

Benoda |

Relmacabtagene autoleucel |

JW Therapeutics |

B-cell lymphomas (DLBCL, follicular) |

2021 |

China |

Source: NIH

Challenges

- Manufacturing complexity and scalability: One of the biggest challenges in the regenerative medicine market is manufacturing at a commercial scale. In this context, producing living cell-based therapies, engineered tissues, or advanced therapy medicinal products requires highly specialized facilities, strict aseptic environments, and validated good manufacturing practice processes. Therefore, maintaining cell viability, potency, and uniformity through scaling up from laboratory to industrial production is both technically demanding and expensive. Also, the aspect of high costs, contamination risks, and technical failures can lead to compromises in terms of product quality and regulatory compliance. This lack of standardized processes ultimately slows down commercialization timelines and increases financial burden on manufacturers, negatively impacting the number of therapies that reach patients.

- Regulatory and ethical barriers: The market is operating under complex and evolving regulatory frameworks, as authorities across the globe struggle to classify and regulate novel therapies, i.e., biologicals, cell therapies, and gene editing in a unified way. At the same time, global regulatory frameworks keep changing, which can lead to inconsistent approval processes as well as long review times. Therefore, harmonizing regulations across different regions is considered to be difficult, and ethical issues such as the use of embryonic cells or gene editing technologies in turn complicate oversight. The existence of these regulatory ambiguities increases development risk for innovators and can delay patient access to new treatments. Furthermore, ethical debates around stem cells and genetic manipulation intensify public scrutiny, requiring more robust safety and governance mechanisms, negatively impacting the growth of the regenerative medicine industry.

Regenerative Medicine Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

18.1% |

|

Base Year Market Size (2025) |

USD 42.5 billion |

|

Forecast Year Market Size (2035) |

USD 189.9 billion |

|

Regional Scope |

|

Regenerative Medicine Market Segmentation:

Technology Segment Analysis

The cell therapy, which is a part of the technology segment, is anticipated to garner the largest share of 45.6% in the regenerative medicine market by the end of the forecast duration. The subtype addresses a wide array of critical conditions from hematologic malignancies to orthopedic and cardiovascular disorders and has the most mature clinical pipeline among regenerative modalities. In February 2026, Gilead Sciences announced the acquisition of Arcellx for a total amount of USD 7.8 billion, thereby gaining full control of anti-cel, a BCMA-directed CAR T-cell therapy for multiple myeloma. The U.S. Food & Drug Administration (FDA) has accepted the BLA for anito-cel, and the deal eliminates profit-sharing and royalties, accelerating development and commercialization while leveraging Arcellx’s D-Domain CAR technology for next-generation therapies, thus denoting a wider segment scope.

Application Segment Analysis

The orthopedics and musculoskeletal application segment is expected to grow at a noteworthy pace in the market during the stipulated timeframe. The growth of the segment is largely driven by the extensive global prevalence of musculoskeletal disorders and the growing adoption of stem cell–based therapies. In June 2024, the article published by NIH stated that tissue engineering and regenerative medicine offer promising strategies to restore function in musculoskeletal conditions, using stem cell therapies such as mesenchymal stem cells and adipose-derived stem cells, biomaterials such as scaffolds and hydrogels, and bioactive molecules, including growth factors and external stimuli. Therefore, the presence of such evidence-based studies indicates a strong and sustained potential for orthopedics and musculoskeletal applications in the years ahead.

Product Type Segment Analysis

Based on product type, the stem cell therapy is predicted to attain a significant revenue share in the regenerative medicine market by the end of 2025. The segment’s upliftment is effectively propelled by its unique self‑renewal and differentiation capabilities, enabling treatment of conditions previously deemed intractable. In March 2026, the Ministry of Health, Labour and Welfare (MHLW) approved the world’s first iPS cell-based regenerative medicine products, i.e., RiHEART for ischemic cardiomyopathy and AMCHEPRY for Parkinson’s disease. It was developed by Cuorips Inc. and Sumitomo Pharma, and these therapies build on decades of pioneering research at Osaka and Kyoto Universities. The approvals were granted under Japan’s conditional scheme, requiring post-marketing confirmation of safety and efficacy, hence denoting a positive market outlook.

Our in-depth analysis of the global regenerative medicine market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Application |

|

|

Product Type |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Regenerative Medicine Market - Regional Analysis

North America Market Insights

The North America regenerative medicine market is anticipated to attain the largest revenue share of 46.7% by the conclusion of the forecast period. The region’s leadership originates from its advanced healthcare infrastructure, high R&D investment, and a strong pipeline of cell and gene therapies. At the same time, a supportive regulatory environment facilitates faster development and review of cell and gene therapies for serious conditions. As of April 2025, data from the U.S. FDA under the 21st Century Cures Act, regenerative medicine therapies such as cell and gene therapies can qualify for RMAT designation if they target serious or life-threatening conditions and show preliminary evidence of addressing unmet medical needs. In this context, the FDA’s Office of Tissues and Advanced Therapies reviews applications within 60 days, granting or denying designation with a rationale provided. Hence, such a pathway offers expedited development and review, thereby supporting innovation in regenerative medicine for critical patient needs.

The presence of an aging population facing chronic degenerative conditions and a surge in oncological breakthroughs, particularly in cell and gene therapies, are the main factors responsible for uplifting the regenerative medicine market in the U.S. Key industry leaders and specialized biotech firms are opting for artificial intelligence and 3D bioprinting to accelerate drug discovery and tissue engineering. U.S. Centers for Medicare & Medicaid Services stated that its Cell and Gene Therapy (CGT) Access Model, which was launched between January 2025 and 2026, is a multi‑year voluntary program especially designed to expand Medicaid access to transformative treatments for rare and severe diseases. Besides, its first focus is gene therapy for sickle cell disease, with 34 states and 2 manufacturers participating. It also mentioned that by using outcomes‑based agreements that tie payment to patient results, the model aims to lower costs, improve health outcomes, and reduce the financial burden on state Medicaid programs, thereby accelerating access to innovative therapies.

A primary emphasis on research and development, supported by a network of prominent academic institutions and public-private partnerships, is bolstering the regenerative medicine market in Canada. At the same time, collaboration between federal health agencies and biotech innovators is identified as a major factor in advancing clinical trials and bringing transformative treatments to the country’s patient population. In April 2026, the government of Canada made a generous investment of USD 127 million in Vancouver’s Aspect Biosystems and Providence Health Care to strengthen the country’s life sciences and biomanufacturing ecosystem. The government is contributing almost USD 79 million to Aspect Biosystems to advance its AI-powered bioprinted tissue therapeutics platform for treating serious metabolic and endocrine diseases, in partnership with Novo Nordisk, supporting clinical development, biomanufacturing, and commercialization. Hence, such investments aim to solidify the country’s position in regenerative medicine, AI-enabled health research, and life sciences innovation.

APAC Market Insights

The Asia Pacific regenerative medicine market is forecasted to represent the fastest growth from 2026 to 2035. The region’s leadership is largely attributable to government initiatives and favorable regulatory reforms, which are accelerating clinical trial approvals and attracting substantial foreign investment. The region is a global leader in stem cell research and is increasingly adopting advanced gene therapies and tissue engineering to address unmet medical needs. In March 2025, an NIH article reported that Japan’s Act on the Safety of Regenerative Medicine (RM Act) was designed to ensure the safe and appropriate provision of regenerative medicine. The Act was partially amended in June 2024 to expand its scope to include gene therapy and related technologies, establish on-site inspections, and set grounds for the disqualification of certified committees for regenerative medicine. The RM Act now classifies regenerative technologies into three risk categories and mandates CRM committee review of clinical plans, ensuring safety, scientific validity, and regulatory compliance, thus positively impacting the market’s growth.

The aggressive government backing through strategic national development plans and a massive, aging patient population are certain factors expanding the market in China. At the same time, major biotech hubs are emerging in specialized industrial parks, fostering a competitive landscape of domestic innovators and international partnerships focused on stem cell technology and tissue engineering. In this context, the National Natural Science Foundation of China, in August 2023, released guidelines for its major research program on tissue and organ regeneration and repair. It also mentioned that the program aims to decode multi-dimensional information on regeneration, uncover regulatory mechanisms, and develop new models, technologies, and strategies to overcome barriers in organ repair. This funding will support projects in areas such as new regenerative models, multidimensional information decoding, mechanisms of repair disorders, and intervention strategies, with a specific focus on liver regeneration, hence making it suitable for standard market growth.

India regenerative medicine market is positioned for phenomenal growth, which is facilitated by rising pharmaceutical manufacturing infrastructure and a rising number of specialized biotech startups. Besides, the presence of suitable government initiatives to promote indigenous research is fostering a more conducive environment for clinical trials and public-private collaborations. In this context, the India Brand Equity Foundation (IBEF) in October 2025, noted that the country is rapidly advancing in regenerative medicine by using cell-based therapies, gene editing, and tissue engineering to treat various health conditions. Meanwhile, the government support through initiatives such as the Biotechnology Ignition Grant Scheme and BIRAC, along with investments such as the USD 54 million stem cell manufacturing hub in Hyderabad, is accelerating R&D and clinical trials, including India’s first human gene therapy trial for haemophilia A. Hence, with the presence of these factors, the country is positioned to become a predominant leader in regenerative medicine, thereby offering improved patient outcomes and economic growth.

Europe Market Insights

Europe regenerative medicine market maintains a strong position in the global dynamics, majorly propelled by a highly collaborative research ecosystem and a sophisticated regulatory framework. The region's growth is also supported by both public funding and private investment, along with the presence of key market players. In April 2025, CUTISS reported the closure of a USD 62 million Series C round, thereby bringing total funds raised to over USD 138 million. The financing will support Phase 3 trials and commercialization of denovoSkin, which is a personalized bioengineered skin graft for burn and reconstructive patients. In addition, CUTISS signed an agreement with Rode Kruis Ziekenhuis in the Netherlands to establish its first international production facility, strengthening its global expansion in skin tissue therapies. Therefore, such a business ecosystem will position Europe as a predominant leader in the regenerative medicine category.

The central network of academic research institutions and specialized biotechnology clusters is responsible for driving growth in the regenerative medicine market in Germany. The sector is driven by continued innovations in cell therapy and tissue engineering. The country’s market is also fueled by manufacturing infrastructure and a strong emphasis on translational medicine. In this context, the Medical Research Act (MFG), which came into force in October 2024, aims to strengthen Germany as a hub for innovative medical research. Besides, it readily streamlines clinical trial approvals, reduces administrative burdens, and enhances overall access to research data. At the same time, the Federal Institute for Drugs and Medical Devices and the Paul-Ehrlich-Institut provide coordinated guidance and faster regulatory pathways, thus accelerating medical innovation and facilitating translational research, including regenerative therapies.

The UK regenerative medicine market is exponentially growing on account of a highly integrated life sciences ecosystem. The country’s market is remarkably bolstered by government-backed initiatives and specialized manufacturing centers, which are especially designed to accelerate the journey from laboratory discovery to patient bedside. In August 2025, the UK government announced a total of USD 37 million investment with the main goal of establishing the UK RNA Biofoundry in Darlington. Besides, this facility will accelerate the development of RNA therapies, which are faster, more adaptable, and more precise than traditional drugs, with the potential to treat cancer, heart disease, and infectious conditions. The biofundry is positioned at CPI’s RNA Centre of Excellence, and it will provide affordable, clinical-grade RNA manufacturing for early trials and pandemic resilience, thus positively impacting the market’s expansion.

Key Regenerative Medicine Market Players:

- Novartis AG (Switzerland)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Bristol‑Myers Squibb Company (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Smith & Nephew plc (UK)

- Medtronic plc (Ireland)

- Bluebird Bio, Inc. (U.S.)

- CRISPR Therapeutics (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- JCR Pharmaceuticals Co., Ltd. (Japan)

- Mesoblast Ltd (Australia)

- RACTHERA Co., Ltd. (Japan)

- Sumitomo Pharma (Japan)

- Sumitomo Chemical (Japan)

- Minaris Regenerative Medicine (Germany)

- WuXi Advanced Therapies (China)

- Minaris Advanced Therapies (U.S.)

- Avita Medical, Inc. (Australia)

- MEDIPOST Co., Ltd. (South Korea)

- Celltrion, Inc. (South Korea)

- Advancells (India)

- Pandorum Technologies (India)

- REGEN HealthCare Sdn Bhd (Malaysia)

- StemFinityCord Malaysia (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Novartis AG is identified as a global leader in regenerative medicine and cell therapies, particularly in CAR‑T and gene therapy platforms. Besides, the firm has proactively made investments in expanding biomedical research centers and next‑generation gene and cell therapy capabilities to accelerate breakthroughs in personalized medicine.

- Gilead Sciences, Inc., through its Kite unit, is yet another dominant player in cell‑based regenerative therapies, especially CAR T‑cell treatments for oncology. Meanwhile, Kite has obtained regenerative medicine advanced therapy designations and generated positive clinical data for investigational agents, thereby solidifying its focus on curative cellular immunotherapies.

- AbbVie Inc. is identified as a major biopharmaceutical company that has a growing interest in regenerative modalities, especially through advanced biologics and cell therapy research. The firm makes heavy investments in technologies that intersect regenerative medicine with novel therapeutic modalities.

- Amgen Inc. is highly focused on developing pioneering human therapeutics that include novel biologics and regenerative processes targeting serious conditions such as cancer and autoimmune diseases. The company integrates strong R&D with scalable manufacturing to bring transformative therapies forward.

- Medtronic plc is a central player in this field that stands out for its convergence of regenerative devices and biologics, especially in orthobiologics and surgical solutions that promote tissue regeneration. In addition, the firm combines advanced hardware with regenerative science, and it drives innovation in musculoskeletal repair and trauma care.

Below is the list of some prominent players operating in the global market:

The regenerative medicine market is considered to be a blend of large multinational pharmaceutical and biotech firms, i.e., Novartis, AbbVie, Gilead, with specialized innovators in cell and gene therapies such as Bluebird Bio, CRISPR Therapeutics, and advanced biologics & devices such as Medtronic, Thermo Fisher. Strategic initiatives adopted by the leading players are heavy R&D investments, mergers & acquisitions, and partnerships to accelerate the commercialization of cell, gene treatments, and tissue engineering solutions. At the same time, regional players in the Asia Pacific, such as MEDIPOST in South Korea and Advancells in India, are strengthening innovation through collaborations and localized clinical adoption, expanding global reach. In December 2024, Sumitomo Chemical and Sumitomo Pharma announced the creation of RACTHERA Co., Ltd., which is a joint venture highly focused on regenerative medicine and cell therapy. Besides this particular partnership, Sumitomo Pharma’s expertise in iPS cell-derived therapies and Sumitomo Chemical’s industrial engineering and quality management strengths.

Corporate Landscape of the Regenerative Medicine Market:

Recent Developments

- In March 2026, the U.S. FDA granted accelerated approval to Kresladi (marnetegragene autotemcel), which is the first gene therapy for severe leukocyte adhesion deficiency type I (LAD-I). This treatment uses a patient’s own stem cells, genetically modified to restore immune function by introducing functional ITGB2 genes.

- In November 2025, CRISPR Therapeutics announced positive Phase 1 results for CTX310, its in vivo CRISPR/Cas9 therapy targeting ANGPTL3. A single IV infusion showed durable, dose-dependent reductions in ANGPTL3, triglycerides, and LDL cholesterol at the highest dose.

- In May 2025, Minaris Regenerative Medicine and WuXi Advanced Therapies merged to form Minaris Advanced Therapies, which is a global cell therapy CDMO headquartered in Philadelphia. The new company consists of 42 clean rooms and extensive infrastructure, and it aims to accelerate the next wave of commercial cell therapies.

- Report ID: 1884

- Published Date: Apr 09, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Regenerative Medicine Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.