Global Radiation Hardened Electronics Market

- An Outline of the Global Radiation Hardened Electronics Market

- Market Definition and Segmentation

- Study Assumptions and Abbreviations

- Research Methodology & Approach

- Primary Research

- Secondary Research

- Data Triangulation

- SPSS Methodology

- Executive Summary

- Growth Drivers

- Major Roadblocks

- Opportunities

- Prevalent Trends

- Government Regulation

- Growth Outlook

- Competitive White Space Analysis – Identifying Untapped Market Gaps

- Risk Overview

- SWOT

- Technological Advancement

- Technology Maturity Matrix for Radiation Hardened Electronics Market Recent News

- Regional Demand

- Global Radiation-Hardened Electronics by Geography – Strategic Comparative Analysis

- Strategic Segment Analysis: Radiation-Hardened Electronics Demand Landscape

- Radiation-Hardened Electronics Demand Trends Driven by rapid expansion of satellite deployments, deep-space exploration programs, and increasing complexity of space missions (2026-2036)

- Root Cause Analysis (RCA) for discovering problems of the Radiation Hardened Electronics Market

- Porter Five Forces

- PESTLE

- Comparative Positioning

- Global Radiation-Hardened Electronics – Key Player Analysis (2036)

- Competitive Landscape: Key Suppliers/Players

- Competitive Model: A Detailed Inside View for Investors

- Company Market Share, 2036 (%)

- BAE Systems (the UK)

- Honeywell International Inc. (U.S.)

- Microchip Technology Inc. (U.S.)

- STMicroelectronics (Switzerland)

- Infineon Technologies AG (Germany)

- Texas Instruments Incorporated (U.S.)

- Analog Devices Inc. (U.S.)

- Renesas Electronics Corporation (Japan)

- Teledyne Technologies Incorporated (U.S.)

- TTM Technologies Inc. (U.S.)

- Global Radiation Hardened Electronics Market Outlook

- Market Overview

- Market Revenue by Value (USD Thousand), Volume (Thousand Tons), and Compound Annual Growth Rate (CAGR)

- Radiation Hardened Electronics Market Segmentation Analysis (2026-2036)

- By Component

- Mixed Signals ICs, Market Value (USD Thousand), and CAGR, 2026-2036F

- Processors and Controllers, Market Value (USD Thousand), and CAGR, 2026-2036F

- Memory, Market Value (USD Thousand), and CAGR, 2026-2036F

- Power Management, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Manufacturing Technique

- Radiation Hardening by Design (RHBD), Market Value (USD Thousand), and CAGR, 2026- 2036F

- Radiation Hardening by Process (RHBP), Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Product Type

- Commercial Off-the-Shelf, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Custom Made, Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Application

- Aerospace & Defense, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Nuclear Power Plants, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Regional Synopsis, Value (USD Thousand), 2026-2036

- North America Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Europe Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Asia Pacific Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Latin America Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Middle East and Africa Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Market Overview

- North America Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Thousand), 2026-2036, By

- By Component

- Mixed Signals ICs, Market Value (USD Thousand), and CAGR, 2026-2036F

- Processors and Controllers, Market Value (USD Thousand), and CAGR, 2026-2036F

- Memory, Market Value (USD Thousand), and CAGR, 2026-2036F

- Power Management, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Manufacturing Technique

- Radiation Hardening by Design (RHBD), Market Value (USD Thousand), and CAGR, 2026- 2036F

- Radiation Hardening by Process (RHBP), Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Product Type

- Commercial Off-the-Shelf, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Custom Made, Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Application

- Aerospace & Defense, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Nuclear Power Plants, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Country Level Analysis, Value (USD Thousand)

- U.S. Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Canada Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Europe Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Thousand), 2026-2036, By

- By Component

- Mixed Signals ICs, Market Value (USD Thousand), and CAGR, 2026-2036F

- Processors and Controllers, Market Value (USD Thousand), and CAGR, 2026-2036F

- Memory, Market Value (USD Thousand), and CAGR, 2026-2036F

- Power Management, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Manufacturing Technique

- Radiation Hardening by Design (RHBD), Market Value (USD Thousand), and CAGR, 2026- 2036F

- Radiation Hardening by Process (RHBP), Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Product Type

- Commercial Off-the-Shelf, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Custom Made, Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Application

- Aerospace & Defense, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Nuclear Power Plants, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Country Level Analysis, Value (USD Thousand)

- UK Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Germany Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- France Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Italy Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Spain Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Netherlands Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Russia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Switzerland Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Poland Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Belgium Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Europe Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Asia Pacific, Excluding Japan Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Thousand), 2026-2036, By

- By Component

- Mixed Signals ICs, Market Value (USD Thousand), and CAGR, 2026-2036F

- Processors and Controllers, Market Value (USD Thousand), and CAGR, 2026-2036F

- Memory, Market Value (USD Thousand), and CAGR, 2026-2036F

- Power Management, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Manufacturing Technique

- Radiation Hardening by Design (RHBD), Market Value (USD Thousand), and CAGR, 2026- 2036F

- Radiation Hardening by Process (RHBP), Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Product Type

- Commercial Off-the-Shelf, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Custom Made, Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Application

- Aerospace & Defense, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Nuclear Power Plants, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Country Level Analysis, Value (USD Thousand)

- China Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- India Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Korea Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Australia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Indonesia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Malaysia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Vietnam Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Thailand Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Singapore Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- New Zealand Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Asia Pacific Excluding Japan Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Latin America Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Thousand), 2026-2036, By

- By Component

- Mixed Signals ICs, Market Value (USD Thousand), and CAGR, 2026-2036F

- Processors and Controllers, Market Value (USD Thousand), and CAGR, 2026-2036F

- Memory, Market Value (USD Thousand), and CAGR, 2026-2036F

- Power Management, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Manufacturing Technique

- Radiation Hardening by Design (RHBD), Market Value (USD Thousand), and CAGR, 2026- 2036F

- Radiation Hardening by Process (RHBP), Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Product Type

- Commercial Off-the-Shelf, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Custom Made, Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Application

- Aerospace & Defense, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Nuclear Power Plants, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Country Level Analysis, Value (USD Thousand)

- Brazil Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Argentina Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Mexico Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Latin America Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Middle East & Africa Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Thousand), 2026-2036, By

- By Component

- Mixed Signals ICs, Market Value (USD Thousand), and CAGR, 2026-2036F

- Processors and Controllers, Market Value (USD Thousand), and CAGR, 2026-2036F

- Memory, Market Value (USD Thousand), and CAGR, 2026-2036F

- Power Management, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Manufacturing Technique

- Radiation Hardening by Design (RHBD), Market Value (USD Thousand), and CAGR, 2026- 2036F

- Radiation Hardening by Process (RHBP), Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Product Type

- Commercial Off-the-Shelf, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Custom Made, Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Application

- Aerospace & Defense, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Nuclear Power Plants, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Country Level Analysis, Value (USD Thousand)

- Saudi Arabia Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- UAE Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Israel Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Qatar Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Kuwait Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Oman Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Africa Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Middle East & Africa Market Value (USD Thousand) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Japan Market

- Overview

- Market Value (USD Thousand), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Thousand), 2026-2036, By

- By Component

- Mixed Signals ICs, Market Value (USD Thousand), and CAGR, 2026-2036F

- Processors and Controllers, Market Value (USD Thousand), and CAGR, 2026-2036F

- Memory, Market Value (USD Thousand), and CAGR, 2026-2036F

- Power Management, Market Value (USD Thousand), and CAGR, 2026-2036F

- By Manufacturing Technique

- Radiation Hardening by Design (RHBD), Market Value (USD Thousand), and CAGR, 2026- 2036F

- Radiation Hardening by Process (RHBP), Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Product Type

- Commercial Off-the-Shelf, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Custom Made, Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Application

- Aerospace & Defense, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Nuclear Power Plants, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026- 2036F

- Medical, Market Value (USD Thousand), and CAGR, 2026-2036F

- Others, Market Value (USD Thousand), and CAGR, 2026- 2036F

- By Component

- Overview

- Global Economic Scenario

- World Economic Outlook

- About Research Nester

- Our Global Clientele

- We Serve Clients Across World

Radiation Hardened Electronics Market Outlook:

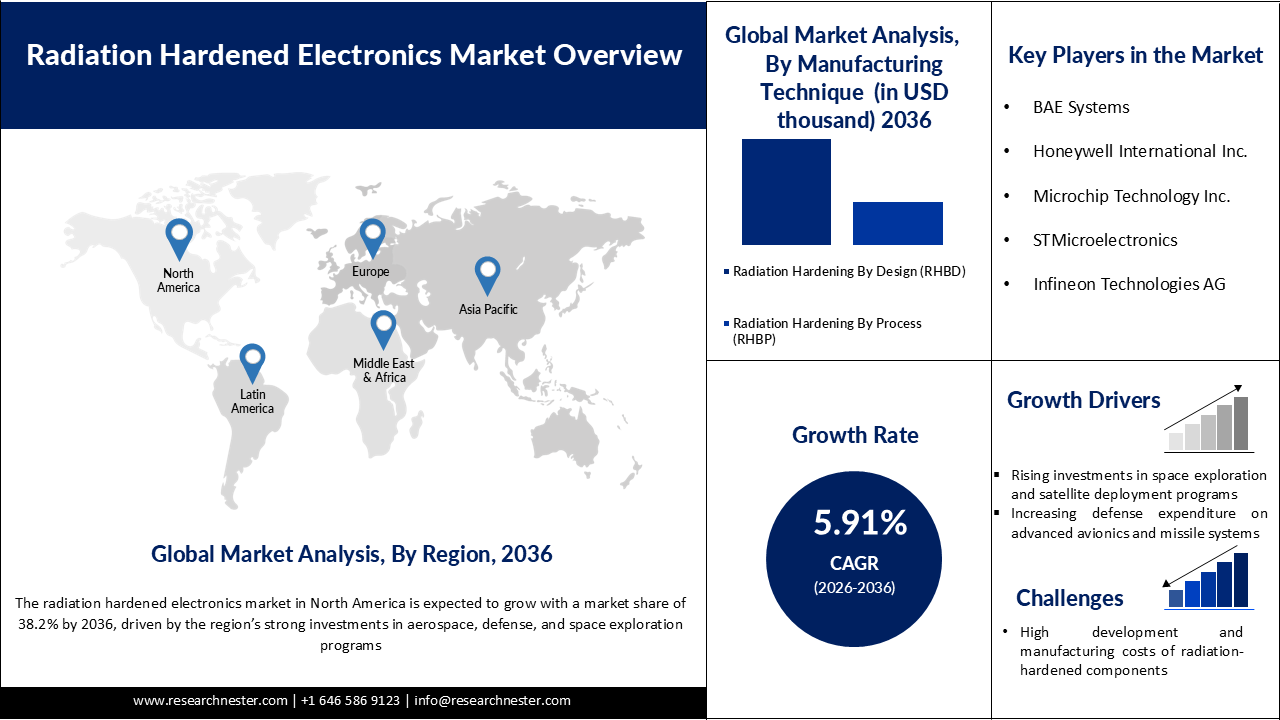

Radiation Hardened Electronics Market is valued at USD 1.82 billion in 2025 and is projected to reach USD 3.48 billion by 2036, growing at a CAGR of 5.91% during the forecast period, i.e., 2026-2036. In 2026, the industry size of radiation hardened electronics is estimated at USD 1.96 billion.

The primary growth driver of the radiation hardened electronics market is the rapid expansion of space and defense systems that require reliable performance in high-radiation environments. Space satellite launches have surged dramatically, driving demand for radiation hardened electronics. In 2024, a record 259 launches deployed 2,695 satellites into orbit, up from just 3,371 total satellites operating in 2020. This escalation, reaching over 11,539 satellites by the end of 2024, stems from mega-constellations like Starlink, necessitating rad-hard components to combat cosmic radiation. Additionally, NOAA operates critical satellite systems for Earth observation and space weather monitoring, further increasing demand for radiation-tolerant components. Defense modernization by the U.S. Department of Defense also emphasizes hardened electronics for secure and survivable systems. In parallel, nuclear infrastructure expansion supported by the International Atomic Energy Agency requires electronics that can function safely in high-radiation zones. This consistent growth in satellites, government missions, and high-reliability applications is the key factor driving the radiation hardened electronics market through 2030 and beyond.

Key Radiation Hardened Electronics Market Insights Summary:

Regional Highlights:

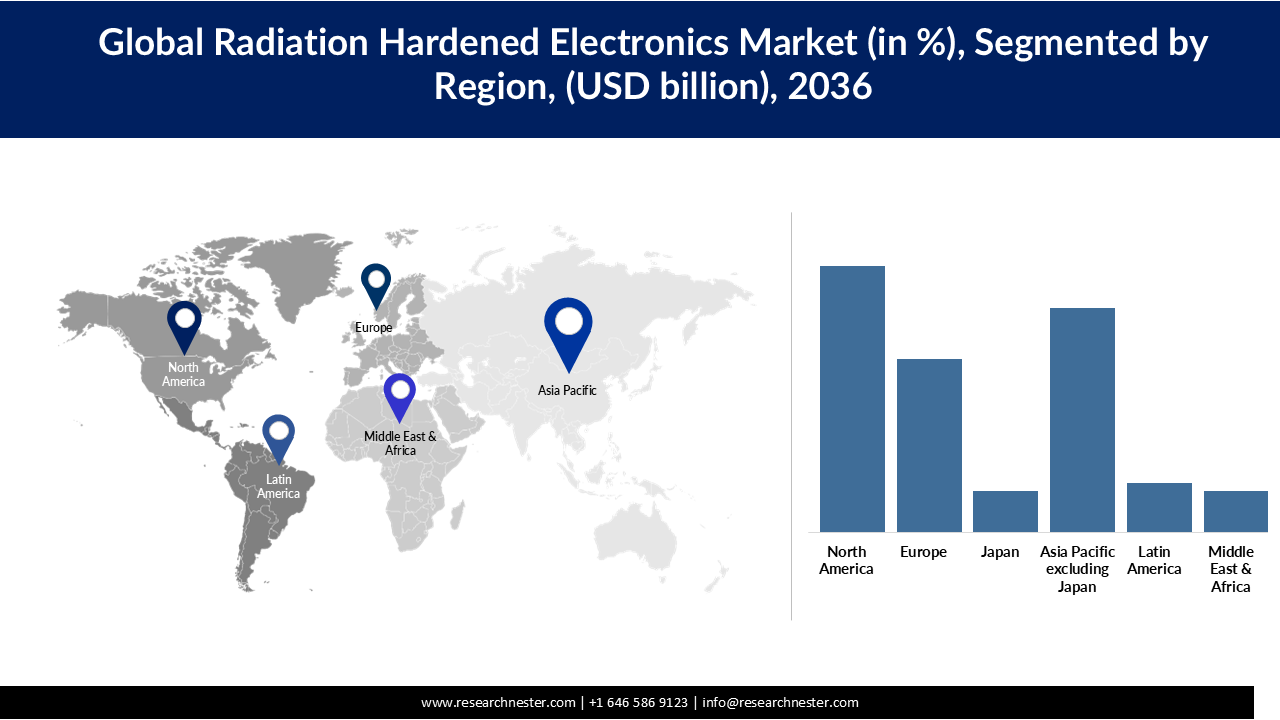

- North America radiation hardened electronics market is anticipated to capture 38.2% share by 2036, propelled by strong investments in aerospace, defense, and expanding space exploration initiatives

- Asia Pacific excluding Japan market is projected to witness robust growth through 2026–2036, fueled by rising military modernization programs and increasing focus on advanced defense technologies

Segment Insights:

- The processors and controllers segment in the radiation hardened electronics market is projected to account for 35% share by 2036, driven by increasing demand for high-performance, fault-tolerant computing in complex space and defense missions

- The radiation hardening by design (RHBD) segment is anticipated to dominate with a 56% share by 2036, owing to its cost-efficient scalability and enhanced radiation tolerance through advanced circuit design techniques

Key Growth Trends:

- Deep-Space & interplanetary missions

- Strategic missile & hypersonic systems

Major Challenges:

- Limited access to high-energy radiation test infrastructure

- Prolonged and expensive radiation qualification requirements

Key Players: BAE Systems (UK), Honeywell International Inc. (U.S.), Microchip Technology Inc. (U.S.), STMicroelectronics (Switzerland), Infineon Technologies AG (Germany), Texas Instruments Incorporated (U.S.), Analog Devices Inc. (U.S.), Renesas Electronics Corporation (Japan), Teledyne Technologies Incorporated (U.S.), TTM Technologies Inc. (U.S.).

Global Radiation Hardened Electronics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.82 billion

- 2026 Market Size: USD 1.96 billion

- Projected Market Size: USD 3.48 billion by 2036

- Growth Forecasts: 5.91% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: North America (38.2% Share by 2036)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, France

- Emerging Countries: India, South Korea, Brazil, United Arab Emirates, Saudi Arabia

Last updated on : 13 April, 2026

Radiation Hardened Electronics Market - Growth Drivers and Challenges

Growth Drivers

- Deep-Space & interplanetary missions: The growth of deep-space and interplanetary missions is a major driver for radiation hardened electronics due to extreme cosmic radiation beyond Earth’s magnetosphere. Programs led by NASA, such as Artemis, mark a long-term exploration timeline extending through the 2020s–2030s, with Artemis I (launched November 16, 2022) traveling about 1.4 million miles over 25 days to validate deep-space systems. This mission alone carried multiple experiments to study radiation exposure effects on electronics and materials. Additionally, the number of operational satellites used as precursors and support systems for deep-space infrastructure grew from 2,218 in 2019 to 7,560 by 2023, according to the Union of Concerned Scientists. As missions extend farther (Moon, Mars, deep space), electronics must withstand prolonged radiation exposure, making rad-hard components essential.

- Strategic missile & hypersonic systems: Strategic missile and hypersonic system development is a major growth driver, as these platforms must operate reliably in extreme radiation, high-speed, and high-altitude environments, including potential nuclear scenarios. Organizations like the U.S. Department of Defense emphasize the need for resilient electronics in missile guidance, navigation, communication, and early-warning systems. According to the Congressional Budget Office, the United States planned to spend about USD 634 billion on nuclear forces between 2021 and 2030, reflecting sustained investment in strategic delivery systems that rely on hardened electronics.

- Additionally, hypersonic weapons capable of speeds above Mach 5 are being actively developed and tested through the 2020s, requiring advanced semiconductors that can withstand thermal and radiation stress. These systems must also remain functional under electromagnetic pulse (EMP) conditions, further increasing the need for radiation hardened designs. Over the 2020–2030 timeline, continuous modernization of missile and hypersonic capabilities is accelerating the adoption of rad-hard electronics to ensure mission reliability and survivability.

- High-energy physics & particle accelerator facilities: High-energy physics research and particle accelerator facilities are a significant but specialized growth driver for radiation hardened electronics due to intense radiation fields generated during experiments. Organizations like CERN operate large-scale accelerators such as the Large Hadron Collider, where detectors and electronics are exposed to continuous high radiation levels. These facilities require radiation-tolerant sensors, control systems, and data acquisition electronics to ensure accurate measurements over long operational lifetimes.

- Additionally, nuclear research and monitoring efforts supported by the International Atomic Energy Agency emphasize robust electronics for safe operation in high-radiation environments. Over the 2020s, upgrades to accelerator facilities (e.g., high-luminosity upgrades) are increasing radiation intensity, further boosting demand for advanced rad-hard components. This niche but critical application area continues to drive innovation and steady radiation hardened electronics market growth.

Challenges

- Limited access to high-energy radiation test infrastructure: A key restraint is the limited availability of specialized facilities required to test electronics under high-radiation conditions, such as particle accelerators and ion-beam labs. Institutions like CERN and a few national labs operate such infrastructure, but access is highly competitive and capacity-constrained. This creates bottlenecks in testing schedules, especially for smaller companies and new entrants. As demand grows through the 2020s, restricted access continues to slow development and validation cycles.

- Prolonged and expensive radiation qualification requirements: Radiation qualification involves rigorous, multi-stage testing to ensure reliability under extreme conditions, significantly increasing time-to-market and costs. Standards followed by agencies like NASA require extensive validation across total ionizing dose (TID) and single-event effects (SEE), often taking several months to years. The need for repeated testing, certification, and documentation adds a substantial financial burden, particularly for commercial manufacturers. This makes radiation hardened electronics far more expensive than conventional components, limiting widespread adoption.

Radiation Hardened Electronics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2036 |

|

CAGR |

5.91% |

|

Base Year Market Size (2025) |

USD 1.82 billion |

|

Forecast Year Market Size (2036) |

USD 3.48 billion |

|

Regional Scope |

|

Radiation Hardened Electronics Market Segmentation:

Component Segment Analysis

The processors and controllers segment is expected to hold 35% of the radiation hardened electronics market share by 2036. Processors and controllers are a key segment driving growth in the market as they function as the core intelligence of systems operating in high-radiation environments such as space, nuclear facilities, and defense platforms. These components ensure reliable execution of commands, data handling, and system control despite exposure to ionizing radiation that can induce errors or damage. Increasing mission complexity, including advanced satellites, deep-space exploration, and autonomous defense systems, is raising demand for high-performance, fault-tolerant processing units. Ongoing advancements in radiation-hardening techniques, such as silicon-on-insulator (SOI) and built-in error correction, are improving reliability and efficiency. The emergence of AI-enabled edge computing in space applications is further intensifying the need for robust, powerful processors and controllers, thereby supporting continued segment growth.

Manufacturing Technique Segment Analysis

The radiation hardening by design (RHBD) segment is expected to dominate the radiation hardened electronics market with a share of 56% by 2036, driven by its ability to enhance radiation tolerance through advanced circuit design and layout techniques. This approach supports the use of standard semiconductor manufacturing processes, enabling cost efficiency and scalability compared to process-based hardening methods. RHBD facilitates faster development cycles and design flexibility, which aligns with the growing need for customized solutions in space, defense, and nuclear applications. Increasing system complexity is also encouraging the integration of error detection and correction features at the design level. Continuous advancements in design tools and architectures are further strengthening RHBD adoption, thereby driving growth in the manufacturing techniques segment.

Product Type Segment Analysis

The commercial off-the-shelf (COTS) segment is playing a significant role in driving the growth of the product type segment in the radiation hardened electronics market by offering readily available and cost-efficient alternatives to fully customized components. These products are increasingly being adapted with radiation-tolerant features, making them suitable for less critical or short-duration missions in space and defense applications. Their lower development time and faster deployment capabilities support rapid system integration and scalability. Growing demand for small satellites and commercial space missions is further accelerating the adoption of COTS-based solutions. Continuous improvements in screening, testing, and shielding techniques are enhancing their reliability in radiation-prone environments. This trend is encouraging broader product diversification and expansion within the radiation hardened electronics market.

Our in-depth analysis of the radiation hardened electronics market includes the following segments:

|

Segments |

Subsegments |

|

Component |

|

|

Manufacturing Technique |

|

|

Product Type |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Radiation Hardened Electronics Market - Regional Analysis

North America Market Insights

North America is witnessing steady growth in the radiation hardened electronics market and is expected to hold a share of 38.2% by 2036. The region benefits from strong investments in aerospace, defense, and space exploration programs, particularly in the U.S., which drives consistent demand for reliable radiation-resistant components. Increasing satellite launches, deep-space missions, and commercial space initiatives are further accelerating adoption across applications. Additionally, the presence of major industry players and continuous technological innovation strengthens regional market expansion. Government funding and focus on real-time data processing and operational efficiency also contribute to sustained growth in North America.

The U.S. radiation hardened electronics market is experiencing steady growth driven by expanding space exploration programs, defense modernization, and commercial satellite deployment. NASA's Goddard Space Flight Center tested candidate electronics for space from 2019-2020, confirming the need for TID tolerance up to 1 Mrad(Si) and SEE thresholds like LETth >85 MeV-cm²/mg for MRAM and NAND flash in satellite applications. Communications satellite deployments in 2020 grew 477% from 2019's 175 satellites, primarily from broadband constellations like OneWeb and SpaceX, heightening rad-hard demands. An October 2020 Oak Ridge National Laboratory report (ORNL/TM-2020/1776) details rad-hard advancements for reactor/space environments, noting NASA RHA processes and commercial offerings tolerant to >100 MGy gamma TID in some cables/devices amid U.S. DOE investments. DoD's Trusted & Assured Microelectronics program (post-2020 updates) sustains funding for rad-hard ICs in defense systems.

The Canada radiation hardened electronics market is also growing steadily, supported by government-led space and defense initiatives and increasing participation in international space programs. The Canadian Space Agency (CSA) continues to fund missions focused on Earth observation, satellite communication, and deep-space research, which require reliable radiation-resistant electronics, with CSA's RADARSAT Constellation Mission (RCM) launched in 2019 needing rad-hard components to handle >30 krad(Si) TID in LEO. Growing collaboration with NASA and participation in programs such as the Lunar Gateway are increasing demand for advanced radiation-hardened components, as Canada's contribution includes avionics tested to 100 krad(Si) levels per CSA-NASA agreements post-2020. In addition, Canada’s defense modernization initiatives and investments in Arctic surveillance are also accelerating adoption, with the Department of National Defence’s NORAD modernization plan (as of 2022) allocating CAD 38.6 billion over 20 years for resilient electronics against radiation in northern orbits. Ongoing government support for aerospace innovation and partnerships with global semiconductor firms are expected to sustain long-term radiation hardened electronics market growth.

Asia Pacific excluding Japan Market Insights

The Asia Pacific region, excluding Japan is experiencing strong growth in the defense market, driven by increasing security concerns and ongoing military modernization programs. Countries across the region are actively upgrading their defense capabilities with a focus on advanced surveillance, naval strength, and air defense systems. There is also a clear shift toward adopting next-generation technologies such as unmanned systems, cyber defense, and integrated command-and-control platforms. Additionally, growing emphasis on self-reliance in defense production is further accelerating market expansion across the region.

The radiation hardened electronics market in China is growing steadily, supported by rapid expansion in space exploration, satellite deployment, and advanced defense systems. Increasing use of satellites for communication, navigation, and earth observation is driving strong demand for reliable components that can operate in high-radiation environments. The country’s focus on deep-space missions and long-term space infrastructure development is further strengthening the adoption of rad-hard semiconductors. At the same time, modernization of aerospace and defense platforms is increasing the integration of high-reliability electronics. Domestic efforts to enhance semiconductor self-sufficiency are also improving supply capabilities for these specialized components. Overall, sustained investment in space and defense technologies is positioning China as a key growth radiation hardened electronics market for radiation hardened electronics.

Moreover, rising military expenditure in China is directly boosting demand for radiation hardened electronics as defense modernization programs expand. Increased spending on satellites, missile systems, and advanced C4ISR platforms is driving the need for reliable components that can operate in high-radiation environments. Upgrades to space-based surveillance and communication networks are further accelerating the adoption of rad-hard semiconductors. At the same time, stronger investment in indigenous defense technologies is supporting local development and procurement of these specialized electronics.

Military Spending (USD Billion)

Source: defensebudget.org

In India, the radiation hardened electronics market growth is primarily supported by increasing satellite launches, deep-space missions, and the rising use of radiation-tolerant systems in navigation, communication, and remote sensing applications. The country’s long-term space exploration roadmap and defense electronics modernization are further boosting demand for rad-hard processors, memory devices, and power management ICs. Government-backed initiatives focused on indigenous electronics manufacturing and strategic autonomy are also strengthening domestic capability development in this segment. Overall, India’s growth is being driven by sustained mission-critical demand and gradual ecosystem development in advanced semiconductor design and radiation-tolerant technologies.

Europe Market Insights

The Europe radiation hardened electronics market is growing steadily, driven by strong expansion in space exploration, satellite deployment, and defense modernization programs across the region. The presence of major institutions such as the European Space Agency (ESA) and initiatives like Horizon Europe is increasing investments in advanced semiconductor technologies for harsh space environments. Rising satellite launches for communication, Earth observation, and navigation are significantly boosting demand for radiation-hardened processors, memory, and power systems. Defense applications, including military satellites, drones, and secure communication systems, are also contributing to market expansion. In addition, increasing collaboration between European governments and private space-tech companies is accelerating innovation in radiation-tolerant design and manufacturing. Continued funding for R&D and next-generation missions like deep-space exploration further supports long-term growth in the region.

The radiation hardened electronics market in Germany is growing steadily, supported by strong aerospace, defense, and nuclear technology capabilities. Germany’s participation in European Space Agency (ESA) programs and international missions is increasing demand for radiation-resistant semiconductors used in satellites, spacecraft, and scientific instruments. The country also benefits from a strong industrial base, with companies like Siemens and Infineon Technologies driving innovation in high-reliability electronics for harsh environments. In addition, government-backed space investments and defense modernization initiatives are encouraging the adoption of advanced rad-hard components. Growing focus on sustainable energy and nuclear safety applications further supports market expansion in the country. Overall, Germany is positioned as one of the leading contributors to Europe’s radiation hardened electronics growth

The UK radiation hardened electronics market is expanding steadily due to rising activity in space exploration, defense systems, and satellite-based communication programs. Strong support from the UK Space Agency (UKSA) and participation in ESA missions are driving demand for reliable electronics capable of operating in high-radiation environments. The country’s advanced aerospace and defense sector, including firms such as BAE Systems, is also contributing significantly to adoption. Increasing investment in small satellite constellations and space-based services is further boosting market growth. In addition, integration of advanced technologies such as AI-enabled space systems and secure military communications is increasing the need for radiation hardened processors and components. The UK is expected to maintain consistent growth supported by innovation and government funding.

Key Radiation Hardened Electronics Market Players:

- BAE Systems (the UK)

- Honeywell International Inc. (U.S.)

- Microchip Technology Inc. (U.S.)

- STMicroelectronics (Switzerland)

- Infineon Technologies AG (Germany)

- Texas Instruments Incorporated (U.S.)

- Analog Devices Inc. (U.S.)

- Renesas Electronics Corporation (Japan)

- Teledyne Technologies Incorporated (U.S.)

- TTM Technologies Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BAE Systems plays a leading role in designing and supplying radiation hardened microelectronics for space, defense, and nuclear applications. The company focuses on highly reliable ASICs and processors used in satellites and military systems, with strong collaboration with government space and defense agencies.

- Honeywell International Inc. is a major supplier of radiation-hardened avionics, sensors, and electronic systems for spacecraft and defense platforms. It contributes significantly through integrated system-level solutions used in navigation, communication, and control systems in extreme environments.

- Microchip Technology Inc. provides radiation-tolerant microcontrollers, FPGAs, and memory devices widely used in satellites and space missions. The company supports cost-effective space electronics through its expanding portfolio of space-grade and rad-hard semiconductor products.

- STMicroelectronics plays a key role in manufacturing radiation-hardened power management ICs, sensors, and microcontrollers for satellite and aerospace applications. It leverages advanced semiconductor processes to deliver reliable performance in harsh radiation environments.

- Texas Instruments Incorporated contributes by developing radiation-hardened analog and mixed-signal devices, including data converters and power management chips. These components are essential for ensuring the stable operation of spacecraft, satellites, and defense electronics systems.

Below is the list of the key players operating in the global radiation hardened electronics market:

Key players in the radiation hardened electronics market are driving growth through continuous innovation in high-reliability semiconductors designed for space, defense, and nuclear applications. They are investing heavily in advanced fabrication techniques, radiation-tolerant architectures, and testing standards to improve performance under extreme conditions. Strategic partnerships with space agencies and defense organizations are accelerating product development and deployment in critical missions. In addition, expansion of product portfolios, including rad-hard processors, memory, and power management devices, is strengthening overall radiation hardened electronics market adoption and scalability.

Corporate Landscape of the Global Radiation Hardened Electronics Market:

Recent Developments

- In February 2026, Honeywell and ForwardEdge ASIC LLC, a subsidiary of Lockheed Martin Corporation, announced a strategic collaboration focused on advancing high-reliability space microelectronics. Under this partnership, Honeywell will serve as the preferred semiconductor foundry, supporting ForwardEdge ASIC’s efforts to develop innovative solutions for space applications, including satellite technologies.

- In September 2025, BAE Systems announced the successful launch of the Carruthers Geocorona Observatory and SWFO-L1 spacecraft, developed for NASA and NOAA. These missions focus on studying space weather and solar radiation effects on Earth’s exosphere, requiring highly reliable space-grade electronics and radiation-tolerant systems to ensure accurate data collection in harsh orbital conditions. The mission strengthens understanding of radiation environments that directly influence satellite and spacecraft design requirements.

- Report ID: 3314

- Published Date: Apr 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2036

Copyright @ 2026 Research Nester. All Rights Reserved.