Qualitative Platelet Disorders Treatment Market Outlook:

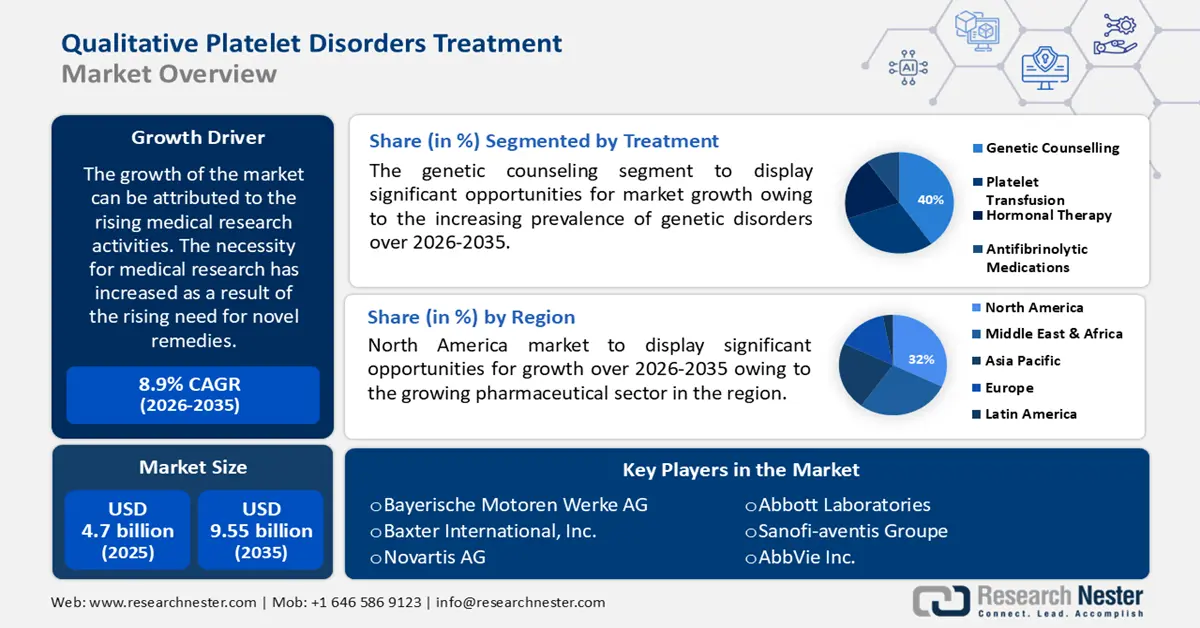

Qualitative Platelet Disorders Treatment Market size was valued at USD 4.07 billion in 2025 and is set to exceed USD 9.55 billion by 2035, registering over 8.9% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of qualitative platelet disorders treatment is evaluated at USD 4.4 billion.

The growth of the market can be attributed to the rising medical research activities. The necessity for medical research has increased as a result of the rising need for novel remedies. For instance, the diagnosis of qualitative platelet diseases, which were formerly underdiagnosed or incorrectly recognized, has grown with developments in medical research and technology. This has increased the need for these illnesses' diagnosis and treatment, which is expected to add to the market growth. India's clinical trials market accounted for around 8% of worldwide clinical research activity in 2020.

In addition to these, factors that are believed to fuel the market growth of qualitative platelet disorders treatment include the increasing development of new therapies and treatments. Further, infections such as dengue fever and malaria which are more common in some parts of the Middle East & Africa can induce platelet dysfunction, this as a result is anticipated to boost the market growth during the forecast period.

Key Qualitative Platelet Disorders Treatment Market Insights Summary:

Regional Highlights:

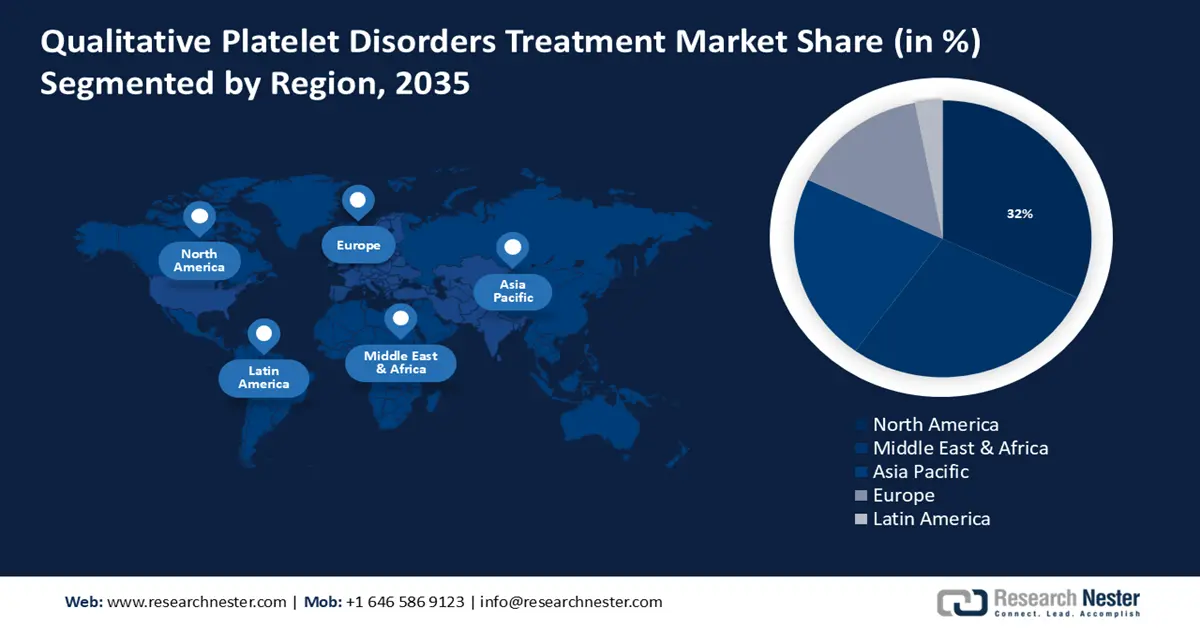

- North America is expected to hold a 32% share by 2035 in the Qualitative Platelet Disorders Treatment Market, owing to the expanding pharmaceutical sector.

- The Middle East & Africa region is anticipated to accelerate at the fastest pace by 2035, supported by the rising frequency of qualitative platelet disorders in specific populations.

Segment Insights:

- The genetic counseling segment is projected to capture the largest share by 2035, underpinned by the growing prevalence of genetic disorders.

- The specialty clinics segment is set to secure a substantial share by 2035, facilitated by the broader adoption of advanced diagnostic methodologies.

Key Growth Trends:

- Growing Changes in Lifestyle

- Rising Geriatric Population

Major Challenges:

- Exorbitant Cost of Treatment

- Insufficient Access to Appropriate Care in Middle and Low Income Countries

Key Players: Pfizer, Inc., Merck & Co., Inc., Siemens Healthcare GmbH, Boehringer Ingelheim International GmbH, Johnson & Johnson Services, Inc., Baxter International, Inc., Novartis AG, Abbott Laboratories, Sanofi-aventis Groupe, AbbVie Inc.

Global Qualitative Platelet Disorders Treatment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.07 billion

- 2026 Market Size: USD 4.4 billion

- Projected Market Size: USD 9.55 billion by 2035

- Growth Forecasts: 8.9%

Key Regional Dynamics:

- Largest Region: North America (32% Share by 2035)

- Fastest Growing Region: Middle East & Africa

- Dominating Countries: United States, Germany, United Kingdom, Japan, China

- Emerging Countries: India, Brazil, South Korea, Saudi Arabia, United Arab Emirates

Last updated on : 20 November, 2025

Qualitative Platelet Disorders Treatment Market - Growth Drivers and Challenges

Growth Drivers

- Growing Changes in Lifestyle – Changes in lifestyle and nutrition among people across the globe have led to a rise in the occurrence of illnesses including obesity, diabetes, and hypertension, which are risk factors for qualitative platelet disorders. As per data, over 600,000 fatalities in the United States occur as a result of unhealthy nutrition each year.

- Rising Geriatric Population – The elderly population is more prone to qualitative platelet abnormalities and the rising number of elderly populations across the globe is estimated to drive market growth. Lately, there are more than 40 million senior citizens in the United States who are 65 or older. It is predicted that this number is expected to rise by more than 80 million by 2050.

- Increasing Health Spending – To address qualitative platelet abnormalities, surgery may occasionally be required. Increasing healthcare spending improves access to competent doctors and specialized surgical facilities wich is further expected to contribute to the market growth. According to the most recent expenditure data, health spending in the US rose by over 9% in 2020.

- Surging Demand for Drugs – It is expected that consumption of several medications, including high-dose penicillin, as well as ethanol, can cause platelet dysfunction as a side effect, which in turn is anticipated to drive the market growth. It was discovered in the US the usage of medications prescribed by retail pharmacies increased by over 2% yearly.

Challenges

- Exorbitant Cost of Treatment - The high cost associated with the treatment of qualitative platelet disorders is one of the major factors predicted to slow down the market growth. For instance, the requirement for long-term care, regular monitoring, and the use of pricey drugs or procedures, treating qualitative platelet abnormalities can be expensive. In addition, in extreme situations of qualitative platelet abnormalities, platelet transfusions can be necessary. Depending on how severe the illness is, these transfusions may need to be repeated frequently and might increase the expenses.

- Insufficient Access to Appropriate Care in Middle- and Low-Income Countries

- Absence of Reimbursement Policies

Qualitative Platelet Disorders Treatment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.9% |

|

Base Year Market Size (2025) |

USD 4.07 billion |

|

Forecast Year Market Size (2035) |

USD 9.55 billion |

|

Regional Scope |

|

Qualitative Platelet Disorders Treatment Market Segmentation:

Treatment Segment Analysis

The global qualitative platelet disorders treatment market is segmented and analyzed for demand and supply by treatment into platelet transfusion, hormonal therapy, anti-fibrinolytic medications, genetic counseling, and others. Out of the five types of treatment, the genetic counseling segment is estimated to gain the largest market share over the projected time frame. The growth of the segment can be attributed to the increasing prevalence of genetic disorders. The increasing number of genetic disorders across the globe has resulted in a growing demand for genetic counseling services. Individuals and families afflicted by these illnesses can receive advice and help from genetic counselors. For instance, those with a qualitative platelet abnormality, as well as their family members, are advised to seek genetic counseling. In addition, the purpose of genetic counseling is to assist people and families in better comprehending the inheritance pattern of the condition, the dangers to their children, and the many diagnostic and treatment choices. This, as a result, is anticipated to create numerous opportunities for the growth of the segment in the coming years. According to the World Health Organization (WHO), in developed nations, genetic illnesses and congenital anomalies account for up to 30% of pediatric hospital admissions, affect 2% to 5% of all live births, and account for roughly 50% of all infant fatalities.

End-user Segment Analysis

The global qualitative platelet disorders treatment market is also segmented and analyzed for demand and supply by end-user into hospitals, ambulatory surgical centers, specialty clinics, and others. Amongst these four segments, the specialty clinics segment is expected to garner a significant share. Accurately identifying and categorizing various forms of qualitative platelet diseases requires the use of cutting-edge diagnostic procedures, which are used in specialty clinics. Moreover, this can aid in choosing the optimal course of action and care alternatives for each patient. In addition, patients with qualitative platelet abnormalities have access to a variety of therapy, including prescription drugs, blood transfusion diagnostics, and other treatments, at specialty clinics. This, as a result, is anticipated to create numerous opportunities for the growth of the segment in the coming years.

Our in-depth analysis of the global market includes the following segments:

|

By Treatment |

|

|

By End User |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Qualitative Platelet Disorders Treatment Market - Regional Analysis

North American Market Insights

North America industry is likely to dominate majority revenue share of 32% by 2035. The growth of the market can be attributed majorly to the growing pharmaceutical sector. For instance, the pharmaceutical industry in the region has experienced fast growth as a result of the creation of several new products and treatments for a variety of illnesses, including platelet abnormalities. In addition, several innovative medications and therapies are being explored to address platelet problems. Further, gene therapy strategies that try to address genetic abnormalities leading to platelet problems are also being investigated, which as a result are also anticipated to contribute to the market growth in this region. More than 20% of the world's pharmaceutical manufacturing and over 40% of the market are both based in the US.

Middle East & Africa Market Insights

The Middle East & Africa qualitative platelet disorders treatment market, amongst the market in all the other regions, is projected to grow with the highest CAGR during the forecast period. The growth of the market can be attributed majorly to the increasing frequency of qualitative platelet disorders. For instance, QPD is a genetic disease, which is why, it is more common in communities that practice intermarriage. Qualitative platelet disorders are often caused by genetic mutations, and some of these mutations may be more common in certain populations. For instance, the prevalence of Glanzmann thrombasthenia, a rare inherited platelet disorder, is found to be higher in populations with consanguineous marriages, which are more common in some parts of the Middle East & Africa, as a result, anticipated to boost the market growth during the forecast period

Qualitative Platelet Disorders Treatment Market Players:

- Pfizer, Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Merck & Co., Inc.

- Siemens Healthcare GmbH

- Boehringer Ingelheim International GmbH

- Johnson & Johnson Services, Inc.

- Baxter International, Inc.

- Novartis AG

- Abbott Laboratories

- Sanofi-aventis Groupe

- AbbVie Inc.

Recent Developments

-

Sanofi-aventis Groupe acquired Provention Bio, Inc., to provide best-in-class medications, and to provide those at risk of developing Stage 3 type 1 diabetes with life-changing advantages. Further, the acquisition also advances the company's strategy to move towards pharmaceuticals with distinctive profiles.

- acquired cardiovascular Systems, Inc. (CSI), to enhance its industry-leading vascular device solutions with new innovations.

- Report ID: 3782

- Published Date: Nov 20, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.