Preeclampsia Diagnostics Market Outlook:

Preeclampsia Diagnostics Market size was valued at USD 2.27 Billion in 2025 and is expected to reach USD 6 Billion by 2035, registering around 10.2% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of preeclampsia diagnostics is evaluated at USD 2.48 Billion.

The growth of this market can be propelled by the increasing prevalence of preterm births. In least-developed countries such as Bangladesh, Afghanistan and Central Africa, infections, malaria, and high teenage pregnancy rates are the main causes of premature births. As per a report of World Health Organization, 14 million births were pre-termed in 2020 with 1 million of death out of complications.

The main trend of the market is being recognized as an increasing need for companion diagnostics. With the growing need for an understanding of patient needs and the provision of personalized medicinal products, there is increasing demand for companion diagnostics. This trend will be more widespread and is expected to allow the entry of POC products including laboratory tests for preeclampsia into new markets. This further leads to disease management, patient satisfaction, and treatment adherence. All these, factors are expected to boost the market growth of preeclampsia diagnostics in the estimated period.

Key Preeclampsia Diagnostics Market Market Insights Summary:

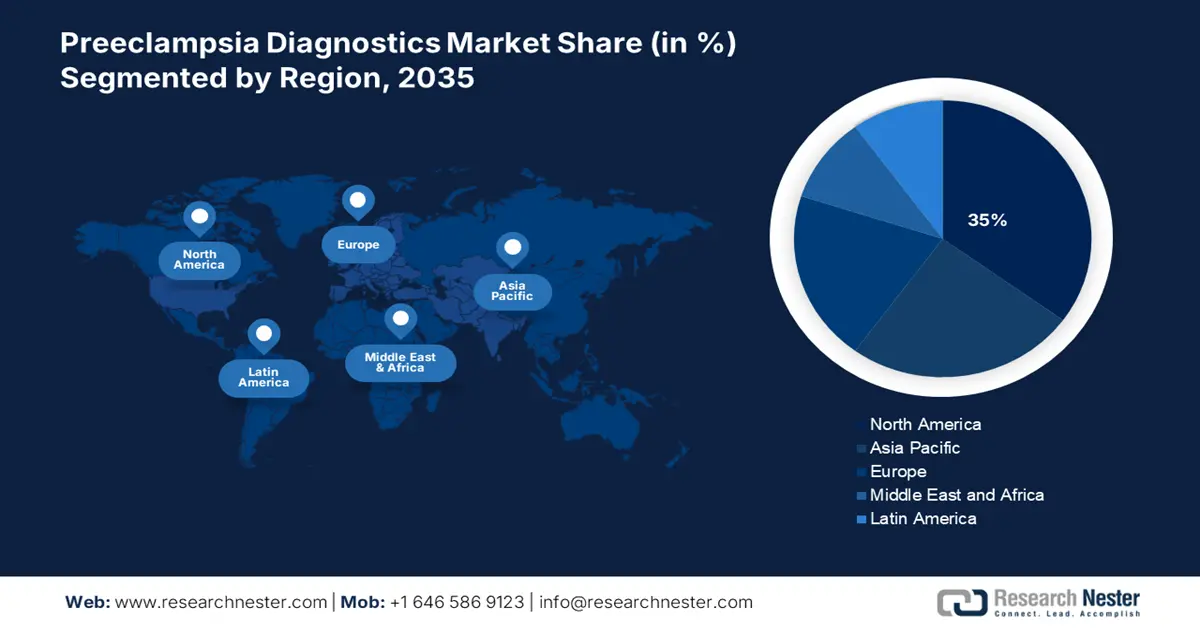

Regional Highlights:

- The North America preeclampsia diagnostics market will secure around 35% share by 2035, fueled by a focus on drug delivery, vaccine development, advancements in biotechnology, and maternal health awareness.

- The Asia Pacific market will achieve substantial CAGR from 2026 to 2035, attributed to the increasing population of women in reproductive age, escalating research activities, and technological advancements in biotechnology.

Segment Insights:

- The consumables segment in the preeclampsia diagnostics market is expected to hold a 60% share by 2035, attributed to low cost, increased usage, and the critical role of consumables in diagnostic tests for preeclampsia.

- The hospitals segment in the preeclampsia diagnostics market is anticipated to exhibit substantial growth from 2026-2035, driven by hospitals being the primary centers for preeclampsia diagnosis and care.

Key Growth Trends:

- Market Expansion in Emerging Economies

- Development of Innovative Tests

Major Challenges:

- Lack of Reimbursement

- Lack of Skilled Professionals is Estimated to Restrict the Market Expansion in Future Time.

Key Players: of Cardinal Health Inc., Diabetomics Inc., F. Hoffmann La Roche Ltd., Thermo Fisher Inc., Biora Therapeutics Inc.

Global Preeclampsia Diagnostics Market Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.27 Billion

- 2026 Market Size: USD 2.48 Billion

- Projected Market Size: USD 6 Billion by 2035

- Growth Forecasts: 10.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, United Kingdom, Japan, China

- Emerging Countries: China, India, Japan, South Korea, Brazil

Last updated on : 9 September, 2025

Preeclampsia Diagnostics Market Growth Drivers and Challenges:

Growth Drivers

-

Market Expansion in Emerging Economies – The preeclampsia diagnostics market is growing rapidly in emerging economies such as India and China. This is due to several factors such as rising incomes, increasing access to healthcare and increasing awareness about preeclampsia. This factor is anticipated to drive the growth of the preeclampsia diagnostics market in the anticipated time period.

-

Development of Innovative Tests - The development of early diagnostic tests for preeclampsia will help reduce maternal and neonatal mortality. Awareness of pre-eclampsia has increased recently, mainly due to campaigns by patient advocacy groups and welfare associations. This remains an important factor providing profitable growth opportunities for innovative test development given the significant unmet need for diagnosing pre-eclampsia worldwide.

Challenges

-

Lack of Reimbursement - The lack of reimbursement will limit the market growth during the forecast period. Most health insurance policies do not cover reimbursement for preeclampsia tests. Lack of reimbursement policy and high cost pose barriers to adoption of preeclampsia testing. Some state and federal officials as well as health officials have publicly encouraged payers to review their insurance policies for Diagnostics for preeclampsia. However, the market still lacks reimbursement services for preeclampsia testing. Such factors limit the growth of the market. Therefore, these factors are expected to restrict the market growth of preeclampsia diagnostics market in the projected timeframe.

-

High Cost of Preeclampsia Diagnostics is Expected to Hamper the Market Growth in Upcoming Period.

- Lack of Skilled Professionals is Estimated to Restrict the Market Expansion in Future Time.

Preeclampsia Diagnostics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

10.2% |

|

Base Year Market Size (2025) |

USD 2.27 Billion |

|

Forecast Year Market Size (2035) |

USD 6 Billion |

|

Regional Scope |

|

Preeclampsia Diagnostics Market Segmentation:

Product (Instrument, Consumables)

Based on product, the consumables segment is estimated to hold the highest market share of 60% by the end of 2035. The selection and enrichment of laboratory tests for preeclampsia must be performed with the aid of consumables. Reagents used in laboratory studies for preeclampsia are chemical substances or mixtures. The growth in the consumables sector has been driven by factors like low costs and increasing consumption frequency. Various growth strategies such as the launch of new products, Strategic Alliances, and M&As are adopted by market players in order to maintain their competitiveness. New players are being encouraged to enter the market on the grounds of moderate market growth potential and access to distribution channels.

End User (Hospitals, Clinics, Diagnostic Centers)

Based on end user, the hospital segment is estimated to grow substantially during the time period. Hospitals have the most comprehensive range of Diagnostics services available comprising those for preeclampsia. They are the primary location where pregnant women are cared for so they are most likely places where preeclampsia will be diagnosed and managed. Furthermore, the increasing prevalence of preeclampsia is estimated to drive the growth of the the segment in the projected period. Around 2-8% of pregnant women experience preeclampsia during their pregnancy worldwide.

Our in-depth analysis of the global market includes the following segments:

|

Product |

|

|

End User

|

|

|

Test |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Preeclampsia Diagnostics Market Regional Analysis:

North American Market Forecast

The North America preeclampsia laboratory market is predicted to hold the largest market share of 35% during the forecast period. The growth of the market in the country is due to factors such as increasing focus on drug delivery services and vaccine discovery and development, recent advancements in biotechnology and pharmaceutical research as well as the presence of many suppliers. In Canada, growing awareness of maternal and fetal health care through the Canadian Fetal Health Surveillance Program and the Canadian Premature Babies Foundation (CPBF) has led to rapid adoption of screening productand s, pre-eclampsia testing in the laboratory at obstetrics departments.

Asia Pacific Market Statistics

The market in the Asia Pacific region is expected to grow substantially during 2026-2035. The growth of this market can be attributed owing to increasing population of women in reproductive age in the region. Besides this, escalating research and development activities, growing technological advancements and presence of biotechnology companies in the region is boosting the market expansion of preeclampsia diagnostics market on the forecast period.

Preeclampsia Diagnostics Market Players:

- ACON Laboratories Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Bio Rad Laboratories Inc.

- BioCheck Inc.

- bioMerieux SA

- Cardinal Health Inc.

- Diabetomics Inc.

- F. Hoffmann La Roche Ltd.

- Thermo Fisher Inc.

- Biora Therapeutics Inc

- Sysmex Corporation

- Hitachi Ltd.

- Fujirebio Diagnostics

- Siemens Healthineers AG

- Fujifilm Corporation

Recent Developments

- Thermo Fisher Scientific Inc., a world leader in serving science, announced in May 2023 that the U.S. Food and Drug Administration approved Thermo Scientific B·R·A·H· M·S PlGF plus KRYPTOR and B ·R·A·H . ·M·S sFlt-1 KRYPTOR novel biomarker, the first and only immunoassay to receive breakthrough designation and be validated for risk assessment and clinical management of preeclampsia, a serious complications of pregnancy.

- Biora Therapeutics, Inc., a biotechnology company that reimagines therapy delivery, has entered into an agreement to license Avero Diagnostics' Preeclampsia Ruleout test previously carried out at Northwest Pathology Company for commercial development of the product.

- Report ID: 4412

- Published Date: Sep 09, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.