Polycystic Kidney Disease Drugs Market Outlook:

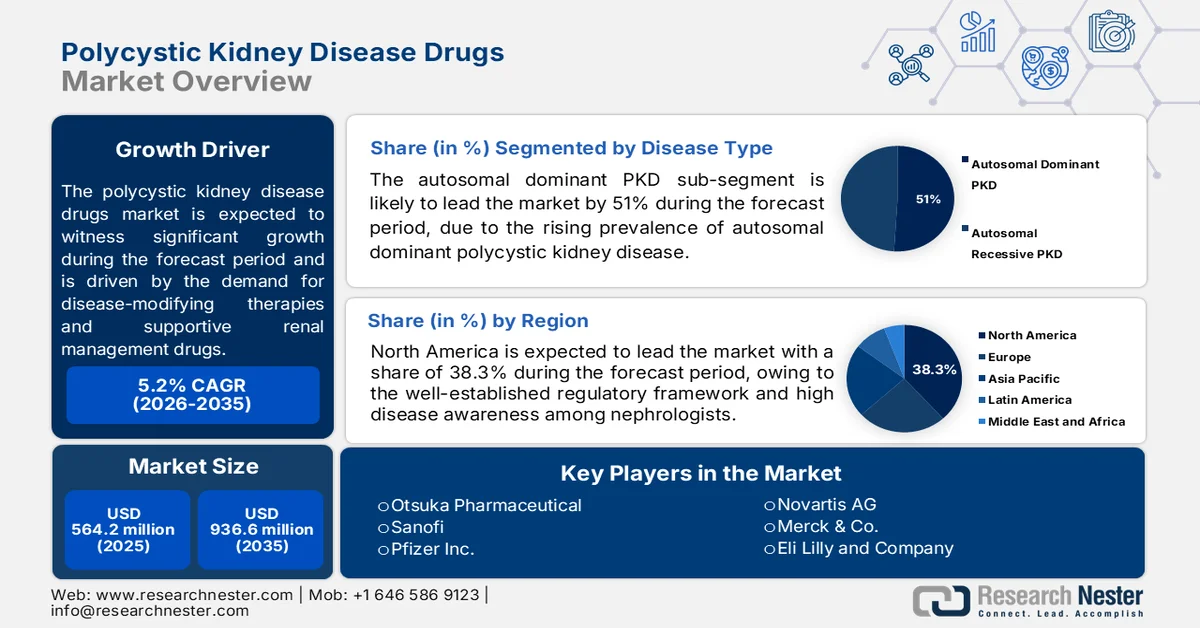

Polycystic Kidney Disease Drugs Market size was valued at USD 564.2 million in 2025 and is projected to account for USD 936.6 million by 2035, rising at a CAGR of 5.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of polycystic kidney disease drugs is evaluated at USD 593.5 million.

Polycystic kidney disease (PKD) continues to represent a significant long-term burden on renal care systems, creating sustained demand for disease-modifying therapies and supportive renal management drugs. According to the NLM March 2024 data, autosomal dominant PKD affects an estimated prevalence of 1 in 20,000 to 40,000 individuals globally, making it one of the most common inherited kidney disorders. Moreover, it estimates that more than 12.5 million people worldwide are affected by PKD, while nearly 500,000 people in the U.S. are living with the condition. The clinical progression of PKD toward chronic kidney disease and kidney failure is a key factor supporting pharmaceutical utilization, particularly in nephrology-focused treatment settings. Government-backed rare disease programs and nephrology research funding are also strengthening the commercial environment for PKD drug development, especially in North America and Europe.

Recent research funded by Kidney Research UK in July 2025 has strengthened the therapeutic development landscape for polycystic kidney disease by identifying ROCK2 inhibition as a potential treatment pathway. In laboratory and kidney organoid studies, researchers observed that drugs targeting the ROCK2 protein showed promising effects in reducing cyst-related disease activity associated with cilia dysfunction, a major contributor to PKD progression. The study focused on repurposing drugs already in development, an approach that may reduce clinical development timelines and support faster regulatory progression. Researchers at the University of Leeds and the University of Sheffield are advancing additional pre-clinical investigations before moving toward clinical trials. The findings highlight increasing institutional investment in targeted renal therapies and reflect growing pharmaceutical interest in mechanism-based treatment strategies for inherited kidney diseases such as PKD.

Key Polycystic Kidney Disease Drugs Market Insights Summary:

Regional Highlights:

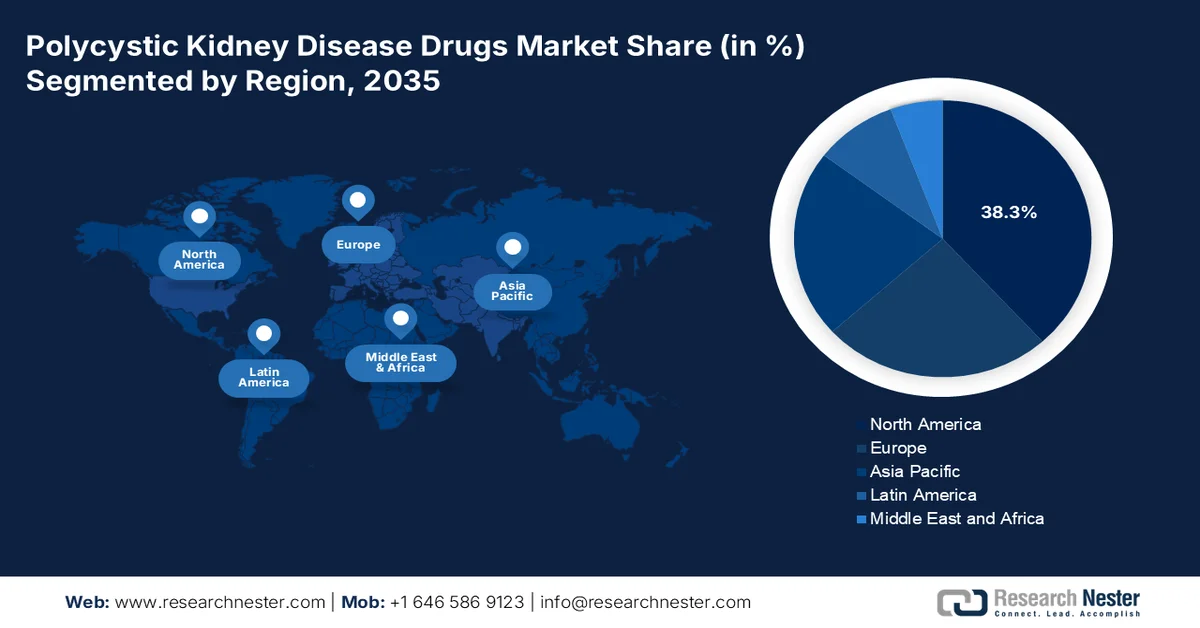

- North America polycystic kidney disease drugs market is anticipated to command 38.3% of the regional revenue share by 2035, propelled by well-established regulatory frameworks, proactive orphan drug policies, and high disease awareness among nephrologists

- Asia Pacific is forecast to witness a CAGR of 7.1% during 2026-2035, stimulated by expanding rare disease frameworks, improving reimbursement pathways, and evolving healthcare infrastructure across emerging economies

Segment Insights:

- The autosomal dominant PKD sub-segment in the polycystic kidney disease drugs market is projected to secure over 51% share by 2035, fueled by the high prevalence of autosomal dominant PKD and increasing pharmaceutical R&D focus on disease-modifying therapies

- Oral administration is expected to remain the leading route of administration segment in the market through 2035, bolstered by superior patient adherence, convenient lifelong home-based dosing, and growing development of oral formulations for chronic ADPKD management

Key Growth Trends:

- Rising chronic kidney disease

- Increasing dialysis and transplant expenditure

Major Challenges:

- High late-stage clinical trial failure rates

- Patient resistance and side effect profile

Key Players: Otsuka Pharmaceutical (Japan), Sanofi (France), Pfizer Inc. (The U.S.), Novartis AG (Switzerland), Merck & Co. (U.S.), Eli Lilly and Company (The U.S.), AstraZeneca (UK), Regulus Therapeutics (The U.S.), Palladio Biosciences (The U.S.), Reata Pharmaceuticals (The U.S.), Kadmon Corporation (The U.S.), ManRos Therapeutics (France), Galapagos NV (Belgium), Chinook Therapeutics (The U.S.), Daewoong Pharmaceutical (South Korea), Lupin Limited (India), Sun Pharmaceutical Industries (India), Calico Life Sciences LLC (The U.S.), Vertex Pharmaceuticals Incorporated (The U.S.), Rege Nephro Co., Ltd. (Japan).

Global Polycystic Kidney Disease Drugs Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 564.2 million

- 2026 Market Size: USD 593.5 million

- Projected Market Size: USD 936.6 million by 2035

- Growth Forecasts: 5.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Japan, Germany, China, United Kingdom

- Emerging Countries: China, India, South Korea, Australia, Brazil

Last updated on : 15 May, 2026

Polycystic Kidney Disease Drugs Market - Growth Drivers and Challenges

Growth Drivers

- Rising chronic kidney disease: The growing prevalence of chronic kidney disease and kidney failure is a major demand driver for the polycystic kidney disease drugs market because PKD is a leading inherited cause of renal decline. According to the 2026 National Kidney Foundation data, more than 35.5 million U.S. adults are estimated to have CKD, while many remain undiagnosed in early stages. PKD patients frequently progress toward dialysis or kidney transplantation, increasing the need for disease-modifying drugs that can delay renal deterioration. These rising treatment expenditures are encouraging healthcare systems to prioritize earlier intervention and long-term renal preservation therapies. Pharmaceutical companies are therefore increasing their investments in nephrology-focused drug pipelines that reduce hospitalization and dialysis dependence.

- Increasing dialysis and transplant expenditure: The increasing financial burden of chronic kidney disease treatment is driving demand for polycystic kidney disease therapeutics that can delay renal decline and reduce dialysis dependence. According to the NLM July 2023 data, the Inside CKD programme covering 31 countries and regions, annual direct healthcare costs rise substantially as CKD progresses, increasing from an average of USD 3,060 per patient in stage G3a to nearly USD 57,334 for haemodialysis and USD 49,490 for peritoneal dialysis. Kidney transplant procedures were associated with annual incident costs exceeding USD 75,000. Since PKD is a major inherited contributor to CKD and kidney failure, healthcare providers and public health systems are increasingly supporting early-stage therapeutic intervention to reduce long-term renal replacement expenses, strengthening demand for disease-modifying PKD drugs and nephrology-focused treatment programs.

- Expansion of clinical trials: The expansion of clinical research programs and international nephrology collaborations is stimulating innovation in polycystic kidney disease therapeutics. The NIH-supported kidney research centers and academic medical institutions are increasingly using organoids, biomarker analysis, and imaging technologies to evaluate new treatment pathways. Clinical trial expansion is helping pharmaceutical companies improve patient recruitment and generate evidence for long-term renal preservation strategies. In Europe, organizations such as the European Renal Association are supporting collaborative nephrology research and chronic kidney disease management initiatives. These research networks are improving data sharing, stimulating validation of therapeutic targets, and supporting multicenter studies for inherited renal diseases. Increasing collaboration between universities, nonprofit organizations, and biotechnology firms is also strengthening commercialization pathways for emerging PKD therapies. This environment is pushing greater investment in targeted renal drug development and expanding opportunities for precision nephrology products.

Challenges

- High late-stage clinical trial failure rates: The high failure rate in the late-stage clinical trials represents one of the most significant financial and developmental roadblocks in the polycystic kidney disease drugs market. Despite a strong scientific rationale, many promising candidates fail to demonstrate efficacy in Phase II/III trials, leading to substantial sunk costs and delayed market entry. This challenge is mainly acute given the slow disease progression of ADPKD, which requires lengthy and expensive trials with surrogate endpoints such as total kidney volume. Manufacturers must therefore invest heavily in robust preclinical models and biomarker development to de-risk their pipelines before committing to costly pivotal trials.

- Patient resistance and side effect profile: Patient resistance to initiating therapy represents a significant polycystic kidney disease drugs market access barrier. Nephrologists report that patients are often reluctant to start tolvaptan because ideal candidates are frequently asymptomatic, cannot tolerate the required high-water intake, and are hesitant to commit to long-term treatment with monitoring requirements. The drug’s side effects, such as polyuria, polydipsia, and hepatotoxicity, further limit compliance. New players must develop therapies with better tolerability profiles or formulate strategies to manage these side effects to improve patient acceptance and adherence rates in the polycystic kidney disease drugs market.

Polycystic Kidney Disease Drugs Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.2% |

|

Base Year Market Size (2025) |

USD 564.2 million |

|

Forecast Year Market Size (2035) |

USD 936.6 million |

|

Regional Scope |

|

Polycystic Kidney Disease Drugs Market Segmentation:

Disease Type Segment Analysis

Under the disease type segment, the autosomal dominant PKD is the dominant subsegment in the polycystic kidney disease drugs market and is poised to capture the share value of over 51% by 2035. The segment is driven by the high prevalence of autosomal dominant PKD. As per the NLM March 2024 data, the prevalence of ADPKD is 1 in 400 to 1,000 people who are affected. This high prevalence translates into a large patient pool requiring chronic disease management, creating sustained demand for disease-modifying therapies. Moreover, the pharmaceutical R&D investments remain heavily skewed toward the ADPKD, with many clinical trial enrollments targeting this sub-segment. The substantial polycystic kidney disease drugs market share also attracts the favorable reimbursement policies and orphan drug designations, further reinforcing the ADPKD's financial and clinical dominance.

Route of Administration Segment Analysis

Oral administration is the leading route of administration sub-segment in the polycystic kidney disease drugs market. The segment is driven by the superior patient adherence and chronic disease management convenience. The oral small molecules allow lifelong home-based dosing without hospital visits. According to the Clinical Trial December 2025 data, Tolvaptan (Tol), the only FDA-approved drug for treatment of ADPKD, has some benefit in slowing kidney disease progression when formulated as oral tablets or capsules. This oral formulation eliminates the need for intravenous infusions or subcutaneous injections, which are impractical for lifelong management of a chronic condition like ADPKD. As a result, all late-stage pipeline candidates, including next-generation vasopressin antagonists and AMPK activators, are being developed exclusively as oral formulations to replicate tolvaptan's commercial success.

Molecule Type Segment Analysis

Small molecules are the leading molecule type in the polycystic kidney disease drugs market, primarily due to their oral bioavailability, favorable pharmacokinetic profiles, and established safety records in chronic disease management. Small molecules can penetrate intracellular targets, modulating key signaling pathways such as cAMP, mTOR, and AMPK that drive cystogenesis. Their relatively low manufacturing complexity and room temperature stability simplify global distribution and long-term storage, making them practical for lifelong administration in outpatient settings. Furthermore, small molecules offer greater formulation flexibility, allowing once or twice daily oral dosing that enhances patient adherence. The extensive experience with small molecule development also accelerates regulatory approvals through well-defined generic and reformulation pathways. As a result, pharmaceutical companies continue to prioritize small-molecule candidates over larger, more costly biologic entities for PKD therapeutics.

Our in-depth analysis of the polycystic kidney disease drugs market includes the following segments:

|

Segment |

Subsegments |

|

Drug Class |

|

|

Disease Type |

|

|

Route of Administration |

|

|

Distribution Channel |

|

|

Treatment Phase |

|

|

Molecule Type |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Polycystic Kidney Disease Drugs Market - Regional Analysis

North America Market Insights

North America is dominating the polycystic kidney disease drugs market and is projected to hold the regional revenue share of 38.3% by the end of 2035. The market is driven by the well-established regulatory framework, proactive orphan drug policies, and high disease awareness among nephrologists. The U.S. and Canada share a collaborative approach to rare disease management with streamlined reimbursement pathways and government-funded research initiatives that support clinical innovation. The key trends include the shift toward early-stage chronic treatment protocols, increased utilization of biomarker-driven patient stratification, and growing real-world evidence requirement for post-market surveillance. Manufacturers benefit from integrated cross-border clinical trial networks and harmonized regulatory guidance. The region’s focus on preventative pharmacotherapy to delay dialysis initiation continues to shape demand, pushing pipeline diversification into oral small molecules and combination regimens.

The growing burden of chronic kidney disease, increasing dialysis dependence, and rising federal healthcare spending on renal care are shaping the polycystic kidney disease drugs market in the U.S. According to the CDC's March 2026 data, chronic kidney disease affects 34% of individuals aged 65 years and older compared with 13% among adults aged 45 to 64 years. Nearly 800,000 U.S. people, including 10,000 children and adolescents, currently receive treatment for kidney failure, and projections indicate that more than 1 million people could require kidney replacement therapy by 2030, without stronger disease prevention measures. In addition, the NLM December 2023 study showed Medicare spending for CKD patients now exceeds USD 130 billion annually, encouraging healthcare systems to prioritize therapies that delay disease progression, reduce dialysis dependence, and support long-term renal preservation strategies. Moreover, the Kidney Fund's February 2026 data indicated that H.R. 7148 allocated USD 2.33 billion to NIDDK, supporting ongoing kidney disease research and therapeutic development. These data show an active polycystic kidney disease drugs market expansion in the U.S.

Reported Cause of End Stage Kidney Disease, 2026

|

Cause |

Percentage |

|

Diabetes |

37 |

|

High Blood Pressure |

27 |

|

Glomerulonephritis |

14 |

|

Cystic Kidney |

5 |

|

Other Causes |

10 |

|

Unknown Cause |

7 |

Source: CDC March 2026

The early regulatory adoption of disease-modifying therapies and increasing clinical focus on advanced renal treatments are driving the polycystic kidney disease drugs market in Canada. According to the NLM January 2026 study, Canada is the second country after Japan to approve tolvaptan for slowing kidney enlargement and kidney function decline in patients with autosomal dominant polycystic kidney disease, strengthening the country’s position in targeted PKD therapy adoption. The NLM December 2025 study shows that ADPKD is currently the fourth leading cause of kidney failure in Canada, increasing demand for long-term nephrology treatment and renal preservation therapies. Clinical management strategies increasingly combine renin angiotensin system inhibitors, sodium restriction, and high-water intake with vasopressin antagonist therapies such as tolvaptan. Moreover, the ongoing evaluation of sodium glucose cotransporter-2 inhibitors as potential renal protective therapies reflects continued therapeutic innovation and expanding pharmaceutical research activity within Canada’s nephrology sector.

APAC Market Insights

Asia Pacific is projected to expand at a CAGR of 7.1% during the assessed period, 2026 to 2035. The region is driven by the rapidly evolving environment characterized by varying levels of disease awareness, healthcare infrastructure, and regulatory maturity across countries. Japan leads with a well-established intractable disease support system that subsidizes treatment costs, followed by South Korea and Australia with structured rare disease frameworks. Emerging markets such as China and India are stimulating the regulatory approvals and expanding reimbursement listings for orphan drugs, improving patient access. The key trends include increasing adoption of oral small molecules, growing participation in global clinical trials, and government initiatives to reduce dialysis burden via early pharmacotherapy.

Large autosomal dominant polycystic kidney disease patient population and the expanding nephrology research activity are fueling the polycystic kidney disease drugs market in China. According to the NLM October 2024 data, the ADPKD prevalence in China is estimated at 1/400 to 1/1,000, representing 1.4–3.5 million patients, while nearly 50% of affected individuals progress to end-stage kidney disease by age 60. Tolvaptan, the only approved disease-modifying therapy for rapidly progressing ADPKD, is increasingly evaluated in China’s clinical settings for its ability to slow estimated glomerular filtration rate decline and reduce kidney volume growth. In addition, the NLM March 2026 study highlights the multicenter studies conducted across major China hospitals between 2018 and 2023, which screened more than 1,230 ADPKD patients, reflecting growing investment in targeted renal therapies. Expanding clinical research and biomarker-based monitoring are supporting long-term PKD treatment demand in China.

The Japan polycystic kidney disease drugs market is expanding rapidly and reached USD 37.8 million in 2025 and is poised to reach USD 75 million by the end of 2035 at a CAGR of 7.1% during the forecast period of 2026–2035. The market is further projected to reach USD 40.4 million in 2026. The polycystic kidney disease drugs market is driven by its early adoption of disease-modifying therapies and a strong clinical research ecosystem. Autosomal dominant polycystic kidney disease, one of the leading hereditary kidney disorders globally, has an estimated prevalence of 1 in 4,000 people in Japan, as per the NLM February 2025 study. The country became the first worldwide to approve tolvaptan for ADPKD treatment following the positive TEMPO 3:4 clinical trial involving 1,445 patients, where the therapy reduced total kidney volume growth and slowed estimated glomerular filtration rate decline. Japan’s PKD guidelines further recommend tolvaptan as a Grade 1A therapy for rapidly progressing patients, supporting broader adoption. In addition, the ongoing SLOW-PKD post-marketing surveillance program strengthens long-term confidence in safety and efficacy, accelerating demand for innovative renal therapies across Japan’s nephrology market.

Europe Market Insights

Europe represents a mature and well-structured polycystic kidney disease drugs market underpinned by centralized regulatory mechanisms via the European Medicines Agency and national health technology assessment bodies. The region benefits from the EU Orphan Regulation, which provides market exclusivity and protocol assistance for rare disease therapies. The key trends of the polycystic kidney disease drugs market growth include increasing adoption of biomarker-based patient selection, standardization of treatment guidelines across member states, and emphasis on the pharmacoeconomic evidence for reimbursement decisions. Manufacturers navigate diverse pricing and access frameworks across countries, with early engagement in the joint clinical assessments becoming essential. The growing focus on clinical trials for early chronic management drives the demand alongside collaborative research networks that facilitate the multinational clinical trials. Pipeline activity centers on oral small molecules and repurposed candidates with established safety profiles.

Clinical Trials and Therapeutic Development Programs for Polycystic Kidney Disease in Europe, 2020–2025

|

Year |

Organization |

Trial |

Study Focus |

Countries |

Status |

|

2021 |

Sanofi-Aventis Recherche & Développement |

Venglustat Extension Study |

Long-term efficacy and safety evaluation of venglustat in rapidly progressing cystic kidney disease |

France, Netherlands, Belgium, Germany, Portugal, Italy, Romania |

Mixed Completed / Prematurely Ended |

|

2021 |

Palladio Biosciences, Inc. |

Lixivaptan Phase 3 (PA-ADPKD-301) |

Evaluation of efficacy and safety of lixivaptan in ADPKD patients |

Italy, Spain, Hungary, Slovakia, Poland, Bulgaria |

Prematurely Ended |

|

2021 |

Aarhus University |

HP-CKDPKD MRI Study |

MRI-based imaging of metabolic abnormalities in chronic kidney disease and PKD |

Denmark |

Trial Transitioned |

|

2021 |

Erasmus University Medical Centre Rotterdam |

Vascular Stiffness Study |

Assessment of vascular stiffness treatment in ADPKD patients |

Netherlands |

Trial Transitioned |

|

2022 |

Aarhus University |

HP-CKDPKD |

Advanced MRI imaging study for chronic kidney disease and PKD progression analysis |

Denmark |

Ongoing / Transitioned |

|

2022 |

Otsuka Pharmaceutical Development & Commercialization |

Pediatric Tolvaptan Study |

Safety and efficacy assessment of tolvaptan in pediatric ADPKD patients |

Germany, Italy, Belgium, UK |

Completed |

|

2022 |

University Medical Center Groningen |

GnRH Agonist Study |

Treatment of severe polycystic liver disease associated with ADPKD |

Netherlands, Germany |

Ongoing |

|

2023 |

European Multicenter Registries |

Tolvaptan Real-world Monitoring |

Long-term renal function and kidney volume monitoring in ADPKD patients |

Germany, Italy, Netherlands, Denmark |

Ongoing |

|

2024 |

European Nephrology Research Networks |

Precision Imaging & Biomarker Programs |

Biomarker identification and disease progression monitoring in ADPKD |

Germany, Denmark, Netherlands |

Ongoing |

|

2025 |

Multiple European Academic Centers & Pharmaceutical Sponsors |

Targeted PKD Therapeutic Expansion |

Development of vasopressin antagonists and targeted metabolic pathway therapies for ADPKD |

Europe-wide |

Ongoing Clinical Development |

Source: EU Clinical Trials Register

The rising chronic kidney disease prevalence and expanding real-world monitoring of autosomal dominant polycystic kidney disease therapies are fueling the growth of the polycystic kidney disease drugs market in Germany. As per the NLM April 2025 data, a large German population-based cohort study reported CKD prevalence at 11.2%, emphasizing the growing burden of renal disorders and the need for long-term disease management strategies. On the other hand, Clinical Trials April 2026 data indicated that the Germany ADPKD Tolvaptan Treatment Registry is strengthening clinical adoption of tolvaptan through multicenter observational monitoring involving 500 patients annually. The registry collects real-world data on kidney volume, renal function decline, treatment dosing, and adverse effects, supporting evidence-based nephrology care. Increasing collaboration between nephrology centers, research institutions, and patient advocacy organizations such as PKDCure is further accelerating therapeutic research, patient identification, and demand for targeted PKD treatments across Germany’s renal care market.

The polycystic kidney disease drugs market in UK is supported by the increasing adoption of disease-modifying therapies and rising healthcare focus on reducing chronic kidney disease (CKD) progression costs. Data from the MedRxiv April 2026 data over 3,609 patients with autosomal dominant polycystic kidney disease (ADPKD) across 72 NHS kidney centres, highlighting growing clinical demand for tolvaptan, the only approved disease-modifying therapy for rapidly progressing ADPKD in the UK. Healthcare cost pressures are also accelerating interest in early renal intervention. The Kidney Research UK June 2023 report shows that as CKD stages 1 to 5 are projected to cost the NHS USD 3.13 billion annually by 2033, while dialysis costs may rise to USD 1.57 billion under constrained models. Increasing concerns regarding equitable therapy access, dialysis dependence, and long-term renal care expenditure are supporting continued investment in targeted PKD treatment strategies.

Cost of Kidney Disease and Renal Care in the UK, 2023

|

Cost Category |

2023 Cost (USD) |

2033 Projection (USD) |

|

CKD Stages 1–5 |

USD 2.63 billion |

USD 3.13 billion |

|

Dialysis Costs |

USD 1.42 billion |

USD 1.57 billion |

|

Dialysis Transport Costs |

USD 304 million |

USD 339 million |

|

Kidney Transplant Costs |

USD 396 million |

USD 564 million |

|

AKI Costs to NHS |

USD 4.23 billion |

USD 4.37 billion |

|

Productivity Loss from Dialysis & Transplantation |

USD 502 million |

USD 563 million – USD 2.70 billion |

Source: Kidney Research UK June 2023

Key Polycystic Kidney Disease Drugs Market Players:

- Otsuka Pharmaceutical (Japan)

- Sanofi (France)

- Pfizer Inc. (The U.S.)

- Novartis AG (Switzerland)

- Merck & Co. (U.S.)

- Eli Lilly and Company (The U.S.)

- AstraZeneca (UK)

- Regulus Therapeutics (The U.S.)

- Palladio Biosciences (The U.S.)

- Reata Pharmaceuticals (The U.S.)

- Kadmon Corporation (The U.S.)

- ManRos Therapeutics (France)

- Galapagos NV (Belgium)

- Chinook Therapeutics (The U.S.)

- Daewoong Pharmaceutical (South Korea)

- Lupin Limited (India)

- Sun Pharmaceutical Industries (India)

- Calico Life Sciences LLC (The U.S.)

- Vertex Pharmaceuticals Incorporated (The U.S.)

- Rege Nephro Co., Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Otsuka Pharmaceutical is the dominant leader in the polycystic kidney disease drugs market primarily due to its first-in-class vasopressin V2 receptor antagonist tolvaptan. The company has focused on securing regulatory approvals worldwide for slowing kidney function decline in autosomal dominant PKD. The company includes extensive post-marketing surveillance studies and patient support programs to manage the drug’s aquaretic side effects.

- Sanofi plays a significant role in the polycystic kidney disease drugs market by exploring repurposed and combination therapies targeting the mTOR and cAMP pathways. The French pharmaceutical giant has leveraged its expertise in rare kidney diseases to initiate early-stage clinical trials for PKD. In 2025, the company made a revenue of USD 220.8 million.

- Pfizer Inc. has made targeted investments in the polycystic kidney disease drugs market via its rare disease division, focusing on small-molecule inhibitors that interrupt cystic signaling pathways. The company's strategy involves licensing promising preclinical assets and utilizing its global clinical trial infrastructure to stimulate the proof-of-concept studies. In 2025, the company made a revenue of USD 62,579 million.

- Novartis AG has actively contributed to the polycystic kidney disease drugs market by investing in the potential of its existing portfolio, including mTOR inhibitors like everolimus and newer agents targeting cystic fibrosis transmembrane conductance regulator pathways. Novartis continues strategic initiatives such as gene silencing partnerships and real-world evidence generation to identify effective combination regimens.

- Merck & Co. approaches the polycystic kidney disease drugs market with a focus on the molecular targets, including SGLT2 inhibitors and epigenetic modulators. The company’s strategic initiatives include leveraging its robust R&D platforms for drug repurposing screenings and collaborating with nephrology-focused biotechs.

Here is a list of key players operating in the global polycystic kidney disease drugs market:

The competitive landscape of the polycystic kidney disease drugs market is concentrated with a mix of the large pharma and specialized biotech firms. The key players focus on vasopressin V2 receptor antagonists and mTOR inhibitors via tolvaptan, which remains the dominant therapy. The strategic initiatives include advanced gene therapy, RNA interference, and repositioning of existing drugs to slow cyst progression. Partnerships with academic research centers and orphan drug designations are common to accelerate pipelines. Emerging companies from Asia are increasingly investing in novel small molecules, while Europe and U.S. firms lead late-stage clinical trials for disease-modifying therapies. Moreover, the acquisition of the leading companies is expanding the polycystic kidney disease drugs market growth. For example, in April 2025, Novartis announced that it had agreed to acquire Regulus Therapeutics, a San Diego-based, publicly traded clinical-stage biopharmaceutical company focused on developing microRNA therapeutics.

Corporate Landscape of the Polycystic Kidney Disease Drugs Market:

Recent Developments

- In October 2025, Calico Life Sciences LLC (Calico), a biotechnology organization focused on aging and age-related diseases and founded by Alphabet Inc. and Arthur D. Levinson, announced the U.S. Food and Drug Administration (FDA) granted Fast Track Designation for ABBV-CLS-628, an investigational therapy for the treatment of Autosomal Dominant Polycystic Kidney Disease (ADPKD).

- In September 2025, Vertex Pharmaceuticals Incorporated announced several important advancements across its programs in immunoglobulin A Nephropathy (IgAN), APOL1-mediated kidney disease (AMKD), and autosomal dominant polycystic kidney disease (ADPKD). These updates represent significant progress toward achieving the Company’s goal of advancing first-in-class or best-in-class therapies that target the underlying causes of these serious kidney diseases.

- In October 2024, Rege Nephro Co., Ltd. announced that the company had successfully developed a funding plan of approximately USD 17 million (JPY 2.5 billion) in new Series B funding and raised USD 15 million with the first payment. This significant investment brings the company’s total funding to USD 30 million.

- Report ID: 4323

- Published Date: May 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.