Polycrystalline Solar Cell Market Outlook:

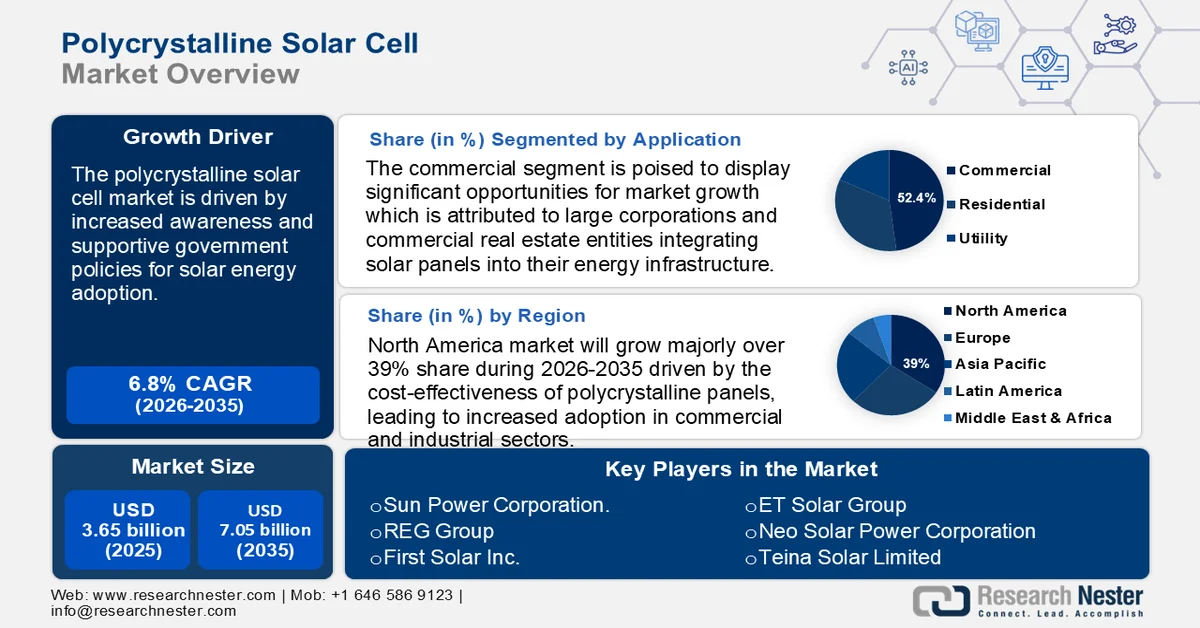

Polycrystalline Solar Cell Market size was valued at USD 3.65 billion in 2025 and is likely to cross USD 7.05 billion by 2035, registering more than 6.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of polycrystalline solar cell is assessed at USD 3.87 billion.

The global shift towards renewable energy has significantly propelled the polycrystalline solar cell market. Governments worldwide are enacting stringent regulations to reduce carbon emissions, leading to increased investments in solar power. Polycrystalline solar cells, known for their cost-effectiveness and straightforward manufacturing processes, make solar energy more accessible across residential, commercial, and industrial sectors. Technological enhancements have enhanced their efficiency and lifespan, narrowing the performance gap with monocrystalline alternatives. Innovations such as bifacial panels, which capture sunlight from both sides, further boost energy generation, increasing the appeal of polycrystalline technology.

As research and development continue, polycrystalline solar cells are expected to become even more efficient, reinforcing their role in diverse applications, from residential rooftops to large-scale utility installations. Studies have shown that bifacial panels can produce up to 30% more electricity than their monofacial counterparts. Additionally, data from the National Renewable Energy Laboratory (NREL) revealed up to a 9% gain in energy production using bifacial panels. These enhancements underscore the potential of bifacial technology to significantly boost solar energy production.

Furthermore, the polycrystalline solar cell market is witnessing strong growth, driven by increased awareness and supportive government policies for solar energy adoption. Many countries offer subsidies, tax rebates, and financial incentives to encourage solar energy system installation, reducing initial costs and enhancing long-term returns. For instance, India’s Production Linked Incentive (PLI) Scheme allocates approximately USD 2.2 billion to boost domestic solar module manufacturing, aiming to reduce reliance on imports and promote self-sufficiency. Polycrystalline modules, made from multiple silicon crystals, strike a balance between cost and efficiency. Their less energy-intensive manufacturing process results in lower production costs compared to monocrystalline panels, making them a cost-effective choice for residential and commercial installations. As technological advancements continue to improve their efficiency and durability, polycrystalline modules are solidifying their position in the global polycrystalline solar cell market.

Key Polycrystalline Solar Cell Market Insights Summary:

Regional Highlights:

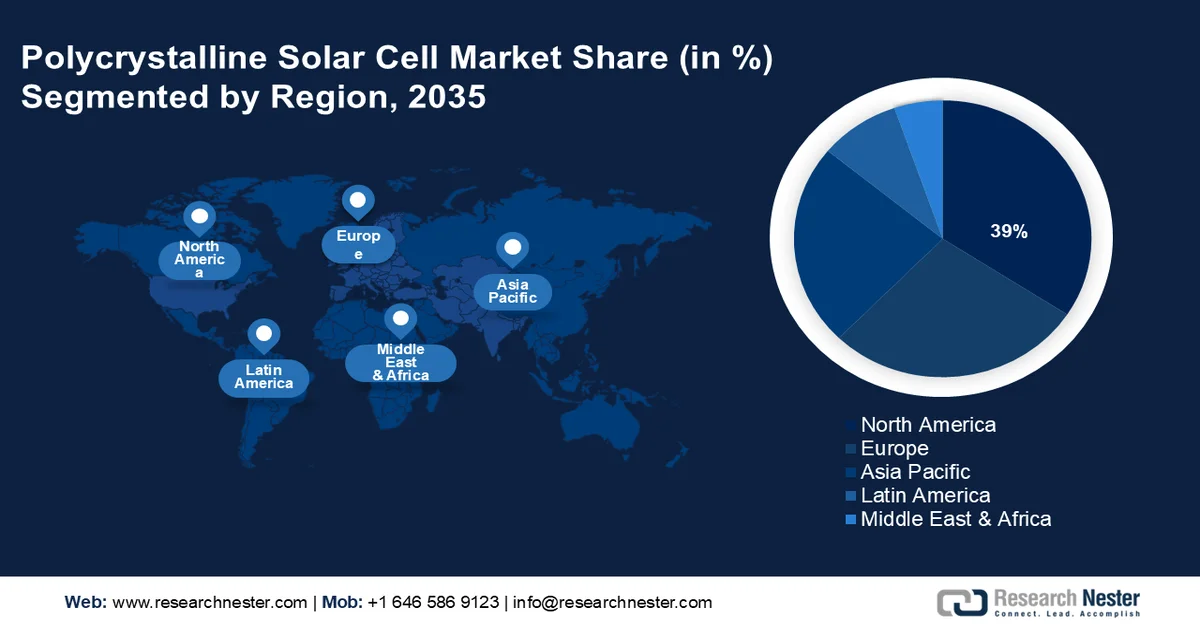

- North America in the polycrystalline solar cell market is anticipated to command over 39% revenue share by 2035, attributed to the cost-effectiveness of polycrystalline panels accelerating their uptake across commercial and industrial sectors.

- Europe is set to register the fastest growth through 2035, buoyed by supportive government incentives and regulatory frameworks encouraging broader solar energy adoption across residential and commercial applications.

Segment Insights:

- The Commercial segment in the polycrystalline solar cell market is expected to capture over 52.4% revenue share by 2035, impelled by growing corporate adoption of solar systems to reduce operational costs and meet sustainability targets.

- The Crystalline silicon cells segment is projected to secure a substantial share by 2035, owing to continuous improvements in silicon wafer quality and manufacturing efficiency enhancing performance and cost-effectiveness.

Key Growth Trends:

- Increasing solar adoption and technological advancements

- Increasing energy demand

Major Challenges:

- Lower efficiency and space requirements

- Disposal and recycling challenges

Key Players: Koninklijke Philips N.V., Headsense Medical Ltd., Braun Melsungen, Minnetronix, Ingehlium GmbH, Vesalio, LLC, Actellion Pharmaceuticals Ltd., GE Healthcare, Teva Pharmaceutical Industries Ltd., Edge Therapeutics Inc., Bristol-Myers Squibb Company, Siemens AG, Aritria Medical.

Global Polycrystalline Solar Cell Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.65 billion

- 2026 Market Size: USD 3.87 billion

- Projected Market Size: USD 7.05 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (39% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: China, United States, Japan, Germany, South Korea

- Emerging Countries: China, India, United States, Japan, Germany

Last updated on : 25 February, 2026

Polycrystalline Solar Cell Market - Growth Drivers and Challenges

Growth Drivers

- Increasing solar adoption and technological advancements: The increasing adoption of solar energy are driven by several key issues, including the urgent need to reduce carbon emissions, rising electricity costs, depleting fossil fuel reserves, government incentives and policies promoting renewable energy, advancements in energy storage solutions, growing consumer awareness of sustainability, improvements in solar panel efficiency and durability, declining manufacturing costs, and the demand for decentralized energy solutions. Additionally, changes in concerns, energy security, and innovations in materials such as perovskite and bifacial solar panels further accelerate the shift towards polycrystalline solar cells.

One of the notable developments involves the integration of 2D periodic nanopatterns into thin-film polycrystalline silicon solar cells using nanoimprint lithography. This technique has demonstrated a 6% increase in light absorption, leading to an enhancement in short-circuit current from 20.6 mA/cm2 to 23.8 mA/cm2. However, the overall efficiency gain was modest, rising from 6.4% to 6.7% due to increased series resistance attributed to changes in surface topography affecting the antireflection coating layer and contact resistance.

These cells are composed of multiple silicon crystals and offer a balance between affordability and performance, making them suitable for several applications. Technological innovations have improved the efficiency and lifespan of polycrystalline solar cells, narrowing the performance gap with monocrystalline alternatives. For instance, advancements in manufacturing processes have led to higher efficiency rates, boosting their appeal in various installations. This growth underscores the pivotal role of polycrystalline solar cells in the global transition towards sustainable energy solutions.

- Increasing energy demand: The escalating global energy demand, driven by population growth, industrialization, and technological advancements, has intensified the search for sustainable energy solutions. Polycrystalline solar cells have emerged as a cost-effective and efficient option to meet the increasing energy needs. Their affordability and relatively simple manufacturing process make them accessible for widespread adoption in various sectors.

In 2024, the National Energy Administration reports that China's installed capacity of solar power and wind power climbed by 45.2% and 18%, underscoring the expansion of solar infrastructure. As the global community strives to minimize carbon emissions and transition towards cleaner energy sources, the need for polycrystalline solar cells is expected to continue its upward trajectory, reinforcing their significance in the renewable energy landscape.

Challenges

- Lower efficiency and space requirements: The polycrystalline solar cell market addresses challenges related to lower efficiency and space requirements, impacting its competitiveness. Compared to monocrystalline cells, polycrystalline solar cells have slightly lower energy conversion efficiency, limiting their ability to maximize electricity generation in constrained spaces. While enhancements have improved efficiency levels, this gap remains a consideration in high-performance applications. Additionally, their lower efficiency necessitates a larger surface area to produce the same power output, making them less suitable for space-constrained environments like residential rooftops.

- Disposal and recycling challenges: Solar panels have a lifespan of 25 to 30 years, after which they require replacement. The panels contain materials such as silicon, glass, and metals, which require specialized recycling processes to recover valuable components efficiently. However, the lack of widespread recycling infrastructure and standardized procedures increases disposal costs and environmental risks. Over time, aging solar panels contribute to electronic waste, raising concerns about landfill accumulation and resource depletion. While more efforts and research have been done to improve recycling technologies and regulations, the industries must develop more sustainable end-of-life solutions to minimize waste and maximize material recovery for long-term environmental benefits of solar adoption.

Polycrystalline Solar Cell Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 3.65 billion |

|

Forecast Year Market Size (2035) |

USD 7.05 billion |

|

Regional Scope |

|

Polycrystalline Solar Cell Market Segmentation:

Application Segment Analysis

In polycrystalline solar cell market, commercial segment is expected to hold more than 52.4% revenue share by 2035. This prominence is attributed to large corporations and commercial real estate entities integrating solar panels into their energy infrastructure. Motivations include reducing operational energy costs, aligning sustainability objectives by minimizing carbon emissions, and achieving environmental goals. Companies also recognize the financial benefits of solar investments, such as generating revenue through feeding excess energy back into the grid or via power purchase agreements (PPAs).

For instance, in South Australia, eligible small businesses can receive grants ranging from USD 25,00 to USD 50,000 for investments in energy-saving technologies, including solar panels and battery storage systems. The businesses installing polycrystalline solar panels can capitalize on government incentives and subsidies, enhancing their return on investment. This combination of environmental responsibility and economic advantage drives the increased adoption of polycrystalline solar cells in the commercial sector. Consequently, the residential segment is projected to experience the fastest growth during the forecast period.

Homeowners are increasingly adopting solar energy due to factors like government incentives, decreasing solar panel costs, and heightened environmental awareness. The affordability of polycrystalline solar cells makes them a popular choice for residential installations. This reflects the broader movements towards sustainable living, with more households leveraging clean, renewable energy sources to meet their electric needs.

Technology Segment Analysis

The crystalline silicon cells segment is estimated to hold a substantial share in the polycrystalline solar cell market. These cells utilize high-purity silicon wafers, offering well-established and efficient technology. Continuous enhancements in silicon wafer quality and manufacturing processes have enhanced their efficiency and affordability, solidifying their position as the preferred choice for numerous solar installations due to their proven performance and cost-effectiveness. Conversely, the thin film solar cells segment is expected to experience robust growth during the forecast period. Thin film technology employs a thinner semiconductor material layer, resulting in lightweight and flexible solar cells.

This flexibility enables integration into various surfaces such as building facades and portable devices, making them suitable for applications like building-integrated photovoltaics (BIP) and wearable technology. Ongoing research focuses on enhancing the efficiency and durability of thin film cells to improve their competitiveness in the polycrystalline solar cell market. For instance, advancements in Cadmium Telluride (CdTe) technology have made it particularly well-suited for large-scale solar farms due to its cost advantages and efficiency. These developments underscore the dynamic nature of the solar cell market, with both crystalline silicon and thin film technologies evolving to meet diverse energy needs.

Our in-depth analysis of the global polycrystalline solar cell market includes the following segments:

|

Technology |

|

|

Technology |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Polycrystalline Solar Cell Market - Regional Analysis

North America Market Insights

North America in polycrystalline solar cell market is expected to hold over 39% revenue share by the end of 2035, driven by the cost-effectiveness of polycrystalline panels, leading to increased adoption in commercial and industrial sectors. The U.S. played a pivotal role, with the solar industry installing nearly 50 GW direct current (GWdc) of capacity, a 21% increase from 2023, making it the second consecutive year of record-breaking installations.

Residential solar installations also saw significant growth, as homeowners sought to reduce energy costs and minimize carbon footprints. Companies such as Sunrun contributed to this expansion by surpassing 1 million customers and integrating the reliability of solar energy for residential use. Advances in energy storage technologies further bolstered the market, ensuring a dependable energy supply even during periods of low sunlight.

These factors collectively propelled the steady expansion of the polycrystalline solar cell market in this region. Similarly, Canada’s polycrystalline solar cell market is expanding, driven by technological enhancements and a commitment to renewable energy. Canadian Solar Inc., a key player, has delivered over 125 GW of photovoltaic modules globally. The nation’s focus on sustainable practices and energy efficiency further supports this growth.

Europe Market Insights

Europe rapidly emerged as the fastest-growing polycrystalline solar cell market, driven by government incentives, instrumental in promoting solar energy adoption across both residential and commercial sectors. For instance, Germany’s Renewable Energy Sources Act (EEG) offers fixed payments for generated electricity over 20 years, providing investment security for solar installations. Additionally, in November 2024, Germany’s cabinet approved plans requiring most operators of new wind and solar power plants to sell their electricity independently on the open polycrystalline solar cell market. Technological advancements have further improved the efficiency and affordability of polycrystalline panels, making them a viable option for widespread deployment.

Companies such as Menlo Electric, a Warsaw-based photovoltaic panel supplier, exemplify this trend. Between 2020 and 2030, Menlo Electric achieved an annual growth rate of 830.8%, reflecting surging demand for solar products in Europe. Additionally, initiatives like the UK’s USD 270 million investment in solar panels for schools and hospitals demonstrate a commitment to integrating solar energy into public infrastructure.

Polycrystalline Solar Cell Market Players:

- JinkoSolar Holding Co., Ltd.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Trina Solar Limited

- Canadian Solar Inc.

- JA Solar Holdings Co., Ltd.

- LONGi Green Energy Technology Co., Ltd.

- Hanwha Q CELLS Co., Ltd.

- Risen Energy Co., Ltd.

- GCL System Integration Technology Co., Ltd.

- SunPower Corporation

- REC Group

- First Solar, Inc.

- Yingli Green Energy Holding Company Limited

- ET Solar Group

- Neo Solar Power Corporation

- Hareon Solar Technology Co., Ltd.

Leading companies maintain their market leadership by adopting enhanced technologies such as Tunnel Oxide Passivated Contact (TOPCon) and heterojunction (HJT) cells, enhancing efficiency and reducing costs. Additionally, innovations like integrating perovskite tandem cells and transitioning from silver to more abundant copper in solar cells further bolster their competitive edge.

Recent Developments

- In November 2023, LONGi Green Energy Technology Co., Ltd. declared that it has achieved a new global record by reaching an efficiency of 33.9% for crystalline silicon-perovskite tandem solar cells.

- In January 2022, during the Abu Dhabi World Future Energy Summit, TrinaTracker, a subsidiary of Trina Solar based in China, unveiled the Vanguard 1P single-row tracker. This innovative Vanguard 1P series is designed to work with ultra-high-power modules that range from 400W to over 670W, thereby expanding the potential applications for TrinaTracker technologies.

- Report ID: 7496

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.