Polycarbonate Sheets Market Outlook:

Polycarbonate Sheets Market size was over USD 4.17 billion in 2025 and is poised to exceed USD 7.06 billion by 2035, witnessing over 5.4% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of polycarbonate sheets is estimated at USD 4.37 billion.

The reason behind the growth is impelled by the growing demand for polycarbonates (PC) by end-use industries. As its peculiar features provide design freedom to product designers, engineers, and OEMs of various industries, PC becomes suitable for use in several applications such as appliances, automotive industry, consumer products, electrical & electronics, and other applications. It was found that in 2020, the total global demand for polycarbonates was little more than 4 million metric tons, whereas it reached 4.51 million metric tons in 2022.

The rise in research and development and collaboration between major key players to manufacture more sustainable thermoplastics such as polycarbonate are believed to fuel the market growth. For instance, a joint study proposal selected by Japan’s New Energy and Industrial Technology Development Organization (NEDO), joined by many stakeholders and managed by Tosoh Corporation and Mitsubishi Gas Chemical Company, Inc. collaborated to reduce CO2 emissions during the manufacture of polycarbonate and polyurethane. The aim is to eliminate the usage of conventional raw material phosgene from the process.

Key Polycarbonate Sheets Market Insights Summary:

Regional Highlights:

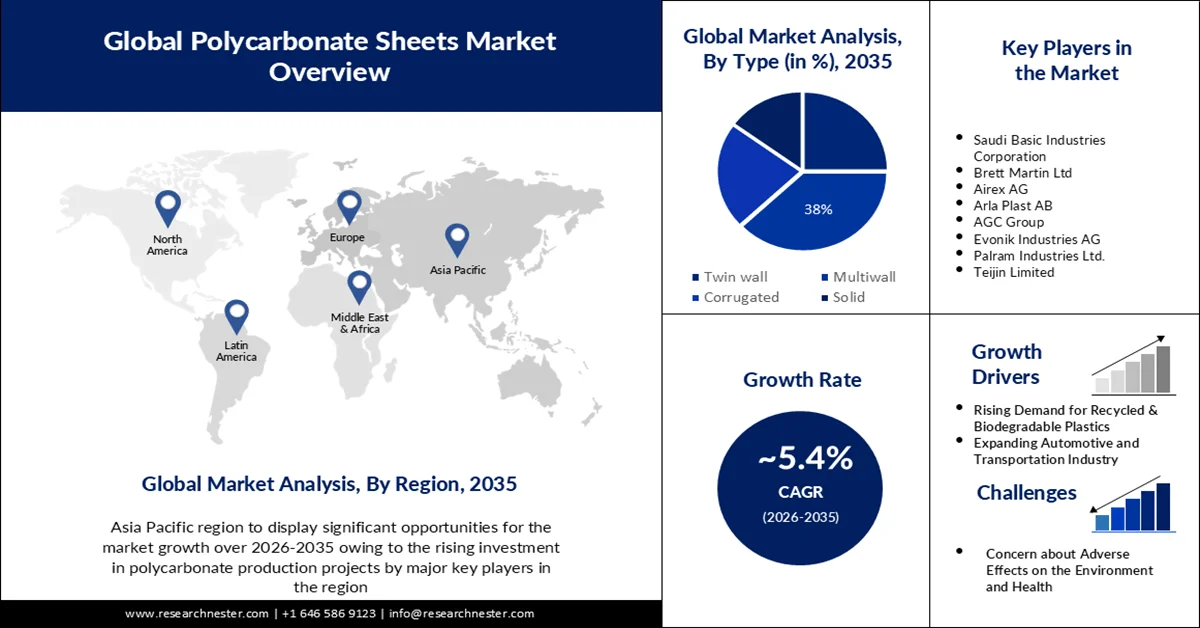

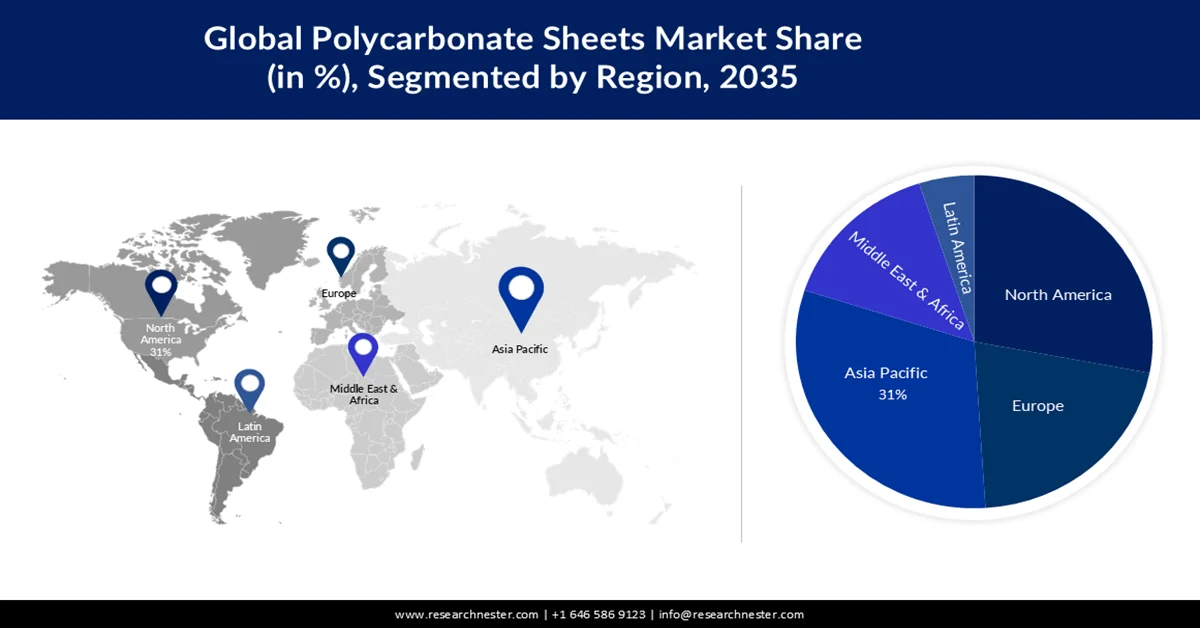

- Asia Pacific polycarbonate sheets market will secure around 31% share by 2035, driven by rising investment in polycarbonate production projects by key players.

- North America market will hold the second largest share by 2035, driven by rising urbanization and infrastructure development.

Segment Insights:

- The electrical & electronics segment in the polycarbonate sheets market is projected to hold a 46% share by 2035, fueled by increasing disposable income boosting demand for consumer electronics.

- The multiwall polycarbonate segment in the polycarbonate sheets market is expected to secure a 38% share by 2035, driven by its unique structure offering lightness and thermal insulation benefits.

Key Growth Trends:

- Rising Demand for Recycled & Biodegradable Plastics

- Expanding Automotive and Transportation Industry

Major Challenges:

- Concern about Adverse Effects on the Environment and Health

- Fluctuating prices of raw materials Affects the Pricing of Polycarbonate Sheets

Key Players: Saudi Basic Industries Corporation, Brett Martin Ltd, Airex AG, Arla Plast AB, AGC Group, Evonik Industries AG, Palram Industries Ltd., Teijin Limited.

Global Polycarbonate Sheets Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.17 billion

- 2026 Market Size: USD 4.37 billion

- Projected Market Size: USD 7.06 billion by 2035

- Growth Forecasts: 5.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (31% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: China, United States, Germany, Japan, India

- Emerging Countries: China, India, Japan, South Korea, Thailand

Last updated on : 10 September, 2025

Polycarbonate Sheets Market Growth Drivers and Challenges:

Growth Drivers

- Rising Demand for Recycled & Biodegradable Plastics - As polycarbonate is fully recyclable and based on advanced recycling, besides providing an excellent yield for plastic recycling facilities, the demand for it is anticipated to increase in the upcoming years.

- Expanding Automotive and Transportation Industry - Modified polycarbonate is widely being used for exterior and interior parts in automobiles owing to its high mechanical properties and good appearance which is expected to boost its demand in the automotive sector.

In 2022, the global market for Automotive Manufacturing was estimated to be worth over USD 2 trillion.

- Rising Aerospace Sector - Polycarbonate and acrylic are common materials found in aircraft windows and cockpit canopies as they are capable of surviving dramatic climatic changes and exceptional resilience to harsh conditions. Moreover, polycarbonate is used in the aerospace and defense industries owing to its excellent transparency, softness, and ductility even at thick ranges. Polycarbonate sheets offer remarkable clarity, impact resilience, and lightweight nature, therefore it is commonly employed in the manufacture of airplane windows given that aircraft are frequently exposed to severe temperatures.

In 2023, worldwide commercial aerospace revenues are predicted to increase by 14% year on year.

- Growing Trend of Do it Yourself (DIY) Projects- Polycarbonate plastic sheets can be used for various crafts and hobbies, such as laser engraved signage, hobby display cases, art protectors, photo frames, temporary outdoor signs, or as school project backgrounds as they are available in a variety of colors, thicknesses, and cellular structures.

- Rising Application in Outdoor Recreational Projects- Polycarbonate sheet roofing is an excellent choice for a variety of exterior projects such as garages, sheds, greenhouses, sunporches, carports, pergolas, or covered patios as it helps lessen sun glare while also reducing sunlight, and is a robust thermoplastic material that is lightweight and can tolerate extremely low and high temperatures.

- Increasing Adoption of Solar Panels- Polycarbonate solar sheets are one of the most popular solar panels as they are used to harness the sun's energy because they can collect sunlight, convert it into heat energy, and release that heat on overcast days.

Solar PV contributed over 4% of worldwide electricity generation in 2021.

Challenges

- Concern about Adverse Effects on the Environment and Health - Raw materials utilized in the manufacturing of polycarbonate sheets primarily involve bisphenol A (BPA) phosgene and other petroleum-based products. These chemicals are considered toxic to the environment and human health. As per findings, long-term exposure to BPA has possible health effects on the brains of fetuses, infants, and children, and its widespread use is possibly linked with increased blood pressure, type 2 diabetes, and cardiovascular disease. Moreover, plastic pollution is a global threat to aquatic animals and other species of the ecosystem. Hence, these factors are majorly anticipated to hamper the market growth.

- Fluctuating prices of raw materials Affects the Pricing of Polycarbonate Sheets

- Stringent Government Regulatory Policies Regarding the Use of Bisphenol A (BPA)

Polycarbonate Sheets Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

5.4% |

|

Base Year Market Size (2025) |

USD 4.17 billion |

|

Forecast Year Market Size (2035) |

USD 7.06 billion |

|

Regional Scope |

|

Polycarbonate Sheets Market Segmentation:

Type Segment Analyis

The multiwall segment is estimated to account for 38% share of the global polycarbonate sheets market in the coming years. Multiwall polycarbonate sheet with hollow and cellular polycarbonate sheets- the most versatile polycarbonate glazing system is made from high-quality bayer polycarbonate resin that has at least two walls and connective ribbing, and offers great impact strength, clarity, and superb transparency. Owing to their unique structure and design, hollow and cellular sheets can be highly light, ensuring lightness and boosting thermal insulation.

End-User Segment Analysis

The electrical & electronics segment in the polycarbonate sheets market is set to garner a notable share of 46% on the account of increasing disposable income. As a result, more and more people across the globe are spending on consumer electronics such as laptops, printers, copiers, and mobile chargers for smartphones, among others. This may drive the demand for polycarbonate sheets as they are clear, impact-resistant sheets formed of thermoplastic polymers that are used to make a variety of electrical and hardware accessories. Moreover, these sheets are excellent electrical insulators which makes them apt for several electrical components.

Our in-depth analysis of the global market includes the following segments:

|

Type |

|

|

End-User |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Polycarbonate Sheets Market Regional Analysis:

APAC Market Insights

Polycarbonate Sheets market in Asia Pacific is predicted to account for the largest share of 31% by 2035 impelled by the rising investment in polycarbonate production projects by major key players. For instance, it was found that a major player Covestro AG invested in the production of more sustainable polycarbonates in the Asia Pacific. The delivery capability of recycled polycarbonates of the company’s first dedicated mechanical recycling production line in Shanghai is anticipated to be more than 60,000 tons per year annually by 2026.

North American Market Insights

The North America polycarbonate sheets market is estimated to hold the second largest, during the forecast timeframe led by rising urbanization. This has led to an increase in infrastructure development in the region which may increase demand for polycarbonate sheets as they are used for several applications in construction projects. According to estimates, in 2021, the United States' urbanization rate was over 0.24%.

Polycarbonate Sheets Market Players:

- Covestro AG

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Saudi Basic Industries Corporation

- Brett Martin Ltd.

- Airex AG

- Arla Plast AB

- AGC Group

- Evonik Industries AG

- Palram Industries Ltd.

Recent Developments

- Covestro AG one of the world’s leading manufacturers of high-quality polymer materials and their components shipped the first climate-neutral polycarbonate from its Uerdingen, Germany site, in 2021. This polycarbonate is climate neutral from cradle to the factory gate, according to a verified life cycle analysis.

- Saudi Basic Industries Corporation (SABIC), a global leader in the chemical industry, launched its certified circular polycarbonate (PC) resin and blends made from the upcycling of post-consumer mixed plastic.

- Report ID: 4835

- Published Date: Sep 10, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.