PCSK9 Inhibitor Market Outlook:

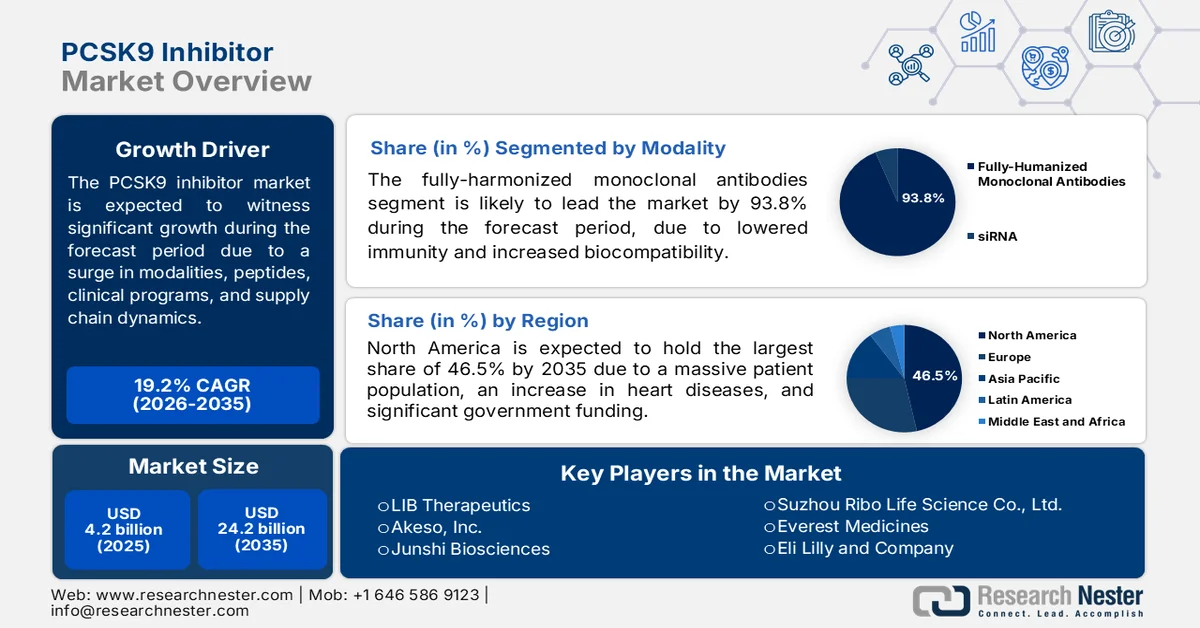

PCSK9 Inhibitor Market size was valued at USD 4.2 billion in 2025 and is expected to reach USD 24.2 billion by the end of 2035, registering around 19.2% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of PCSK9 inhibitor is estimated at USD 5 billion.

The worldwide PCSK9 inhibitor market is being significantly influenced by next-generation modalities, including oral peptides and small-molecule inhibitors that are escalating through clinical pipelines. In this regard, the August 2023 NLM article noted that peptides are polypeptide chains with less than 50 amino acids, along with a relative molecular mass not surpassing 5,000 Da. Besides, the industrial size of protein therapeutics and peptides is currently predicted to be more than USD 40 billion every year, readily contributing to an estimated 10% of the pharmaceutical franchise. Besides, an estimated 75% of therapeutic macromolecules, which include proteins and peptides, are delivered by parenteral methods, leading to increased expenses. Moreover, supply chain dynamics, an expansion into primary prevention settings, boosted by clinical programs, and the emergence of gene therapies are also positively impacting the market growth.

Furthermore, the growth of biosimilars, the successful integration of digital health and telemedicine, and the transition towards notable modalities and RNA-interface technologies are other trends that are responsible for bolstering the market globally. As per an article published by NLM in June 2024, the average payers’ pricing per dose of biologic product was lowered by USD 438 for trastuzumab, which is followed by USD 112 for infliximab and USD 110 for bevacizumab. Likewise, the persistent effect of biosimilars resulted in diminishing the price, such as USD 49 for adalimumab, USD 290 for filgrastim, USD 189 for trastuzumab, and USD 21 for infliximab. Based on this pricing strategy, the overall medical spending per person for biologic-based disease-modifying antirheumatic drugs amounted to an estimated USD 26,217, with out-of-pocket costs averaging USD 1,484, thus enhancing the worldwide market’s exposure.

Key PCSK9 Inhibitor Market Insights Summary:

Regional Highlights:

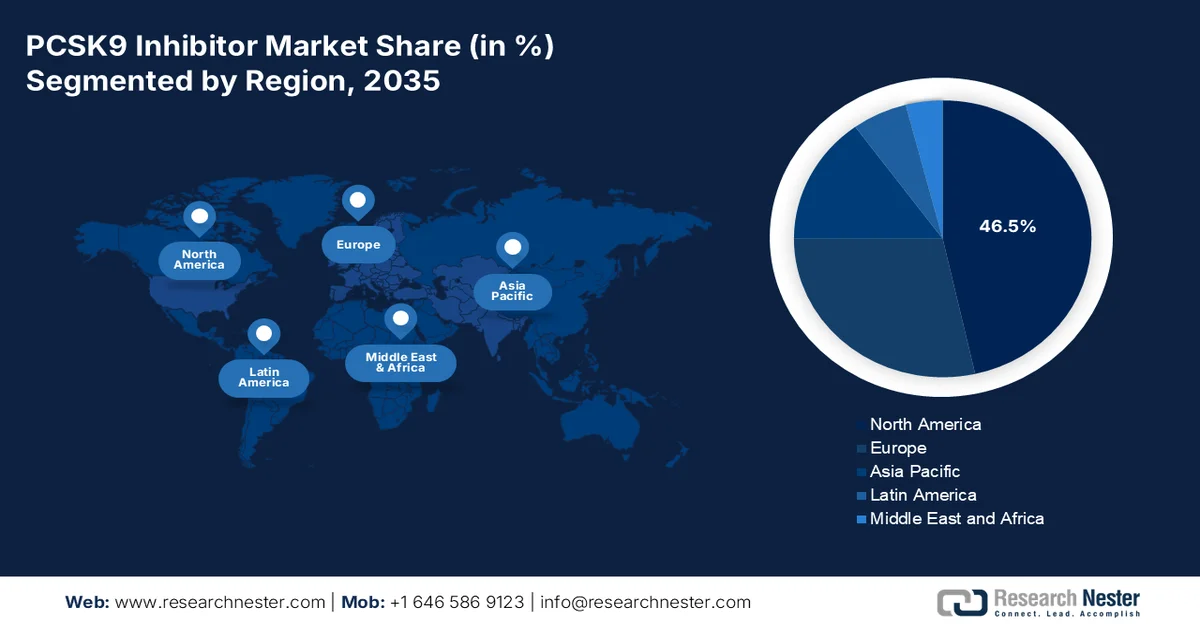

- North America PCSK9 inhibitor market is anticipated to command 46.5% of the market share by 2035, bolstered by a large patient pool, rising hypercholesterolemia prevalence, growing demand for advanced lipid-lowering therapies, and substantial government healthcare spending through Medicaid and Medicare

- Asia Pacific is poised to register the fastest growth in the market throughout 2026-2035, stimulated by accelerating urbanization, evolving dietary habits, increasing cardiovascular disease burden, and enhanced healthcare services across the region

Segment Insights:

- The fully-harmonized monoclonal antibodies segment in the PCSK9 inhibitor market is forecast to capture 93.8% share by 2035, supported by its ability to reduce immunogenicity, improve biological compatibility, and minimize side effects compared to animal-specific treatments

- Evolocumab is expected to secure a 71.7% market share by 2035, underpinned by its effectiveness in regressing and preventing arterial plaque formation while reducing the risk of strokes and heart attacks

Key Growth Trends:

- An escalation in cardiovascular morbidity

- Value-based contracting and favorable reimbursement policies

Major Challenges:

- Restrictive authorization hurdles

- Physician hesitancy and clinical inertia

Key Players: Amgen (U.S.),Sanofi/Regeneron (France/U.S.),Novartis (Switzerland),Merck & Co. (U.S.),LIB Therapeutics (U.S.),Akeso, Inc. (China),Junshi Biosciences (China),Innovent Biologics (China),Jiangsu Hengrui Medicine (China),Suzhou Ribo Life Science Co., Ltd. (China),Everest Medicines (China),Eli Lilly and Company (U.S.).

Global PCSK9 Inhibitor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.2 billion

- 2026 Market Size: USD 5 billion

- Projected Market Size: USD 24.2 billion by 2035

- Growth Forecasts: 19.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (46.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, United Kingdom, Canada

- Emerging Countries: China, India, South Korea, Australia, Singapore

Last updated on : 25 June, 2026

PCSK9 Inhibitor Market - Growth Drivers and Challenges

Growth Drivers

- An escalation in cardiovascular morbidity: The increased and high global burden of this particular disease is responsible for the maximum number of deaths every year, positively catering to the PCSK9 inhibitor market. According to an article published by NLM in January 2022, approximately 17.7 million people die from the disease, demonstrating 31% of total deaths and more than 75% of such deaths take place across low and middle-income nations. For instance, India constitutes the highest burden, with the World Health Organization (WHO) estimating non-communicable diseases to account for 60% of overall deaths. However, to ensure standard diagnosis, the country usually spends roughly USD 236 billion for managing the disease occurrence, thus proliferating the market expansion.

- Value-based contracting and favorable reimbursement policies: This is another growth driver for the market, significantly diminishing financial gaps for the global patient population. As stated in an article published by Clinical Nutrition Open Science in June 2025, curative care services usually constitute the majority of health spending, indicating 61% of overall healthcare expenses. Besides, medical goods and ancillary services account for 28% of the expenditure, and meanwhile, the cost of preventive care services tends to remain steady at 1%. Moreover, private insurance organizations generously allocated 36% of their overall health spending towards medical and ancillary services, thus positively driving the market expansion.

Challenges

- Restrictive authorization hurdles: Navigating the complex reimbursement landscape presents a formidable roadblock when patients are clinically eligible, which negatively impacts the PCSK9 inhibitor market. Payers across major markets have implemented stringent prior authorization protocols that demand extensive documentation of statin intolerance or failure, genetic testing for familial hypercholesterolemia, and proof of adherence to other lipid-lowering therapies. These administrative burdens delay treatment initiation and create substantial physician burnout. The criteria for approval vary significantly between insurers and regions, creating a confusing patchwork of requirements that complicates clinical workflows.

- Physician hesitancy and clinical inertia: Despite compelling clinical trial evidence, significant physician hesitancy persists regarding the adoption of PCSK9 inhibitors. Many clinicians remain comfortable with traditional statin therapy and are reluctant to adopt newer, more expensive agents. This therapeutic inertia is reinforced by historical skepticism about the safety of aggressively lowering LDL-C to very low levels, a concern that has only recently been dispelled through long-term safety data. The perception that these therapies are reserved for only the most difficult-to-treat patients further limits their use in broader populations, thus causing a hindrance in the market.

PCSK9 Inhibitor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

19.2% |

|

Base Year Market Size (2025) |

USD 4.2 billion |

|

Forecast Year Market Size (2035) |

USD 24.2 billion |

|

Regional Scope |

|

PCSK9 Inhibitor Market Segmentation:

Modality Segment Analysis

Based on the modality segment, the fully-harmonized monoclonal antibodies sub-segment is projected to account for the highest share of 93.8% in the PCKS9 inhibitor market by the end of 2035. The sub-segment’s upliftment is primarily driven by its importance in reducing immunogenicity, increasing biological compatibility, and effectively lowering side effects, in comparison to animal-specific treatments. According to an article published by NLM in June 2024, monoclonal antibodies have effectively garnered suitable clinical acclaim, with more than 20 mAbs presently in clinical utilization, and were valued at USD 300 billion as of 2025. Besides, as per the 2026 SEAIR report, the import shipment of these antibodies accounted for 4,258 tons for cholera and typhoid. Therefore, with the continuous expansion and an increase in supply dynamics, there is a huge growth opportunity for the sub-segment globally.

Drug Segment Analysis

During the forecast period, the Evolocumab sub-segment under the drug segment is projected to garner the second-highest share of 71.7% in the market. The sub-segment’s growth is effectively fueled by its importance as a groundbreaking medication for regressing and preventing plaque development in arteries and diminishing the risk of strokes and heart attacks. As per the 2024 NCBI data report, the payer’s pricing of evolocumab amounts to USD 271.2 per 150 mg/mL based on a single-use prefilled autoinjector, as well as USD 587.7 per 120 mg/mL based on a single-use automated mini-dozer. In addition, the yearly per-patient expense of the drug amounted to USD 7,053, with a lifetime duration of 52 years, which constitutes moderate and high-intensity statin therapy, thus positively driving the sub-segment’s demand.

Indication Segment Analysis

The familial hyper cholesterolemia sub-segment, which is part of the indication segment, is expected to grab the third-highest share of 42.8% in the market by the end of the stipulated timeline. This genetic disorder, characterized by markedly elevated LDL cholesterol from birth due to mutations in the LDL receptor pathway, creates an urgent and compelling medical need that conventional statins cannot adequately address. Heterozygous FH patients, despite maximally tolerated statin and ezetimibe therapy, frequently fail to achieve recommended LDL-C targets, while homozygous FH patients, lacking functional LDL receptors, derive minimal benefit from standard oral therapies. PCSK9 inhibitors, by blocking the PCSK9 protein and preventing LDL receptor degradation, uniquely enhance hepatic clearance of circulating LDL, offering a targeted therapeutic intervention for this specific pathophysiology.

Our in-depth analysis of the PCSK9 inhibitor includes the following segments:

|

Segment |

Subsegments |

|

Modality |

|

|

Drug |

|

|

Indication |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

PCSK9 Inhibitor Market – Regional Analysis

North America Market Insights

The North America PCSK9 inhibitor market is anticipated to grab the largest share of 46.5% by the end of 2035. The market’s upliftment is primarily attributed to the presence of a massive patient population, an increase in hypercholesterolemia, the demand for advanced lipid-lowering agents, and generous government expenditure through Medicaid and Medicare. According to a December 2023 NCBI article, the U.S. population increased by 7.4% over the past 10 years, to 331,449,281 people. In addition, the U.S. Census Bureau estimated that the 65-and-older population has risen from 12.7% to 16.1%. Additionally, 1 in 8 people in the country are aged more than 65 years, and presently, 1 in 6 people fall under this category. Therefore, with this increase in the elderly population, disease incidence is also increasing, thus making it suitable for expanding the market in the overall region.

The PCSK9 inhibitor market in the U.S. is growing rapidly, owing to an increase in cardiovascular disease, government funding, continued efforts for optimizing patient accessibility, and an upsurge in the need for inhibitors. According to the January 2026 AHA Journals Organization article, hypertension is one of the most common risk factors of cardiovascular disease, leading to roughly 664,00 deaths in the country. As of 2023, there was no modification in the total age-standardized hypertension prevalence among the adult population, ranging between 32.4% and 36.1%. In addition, this pattern among men and women accounted for 35.2% and 33.4%, while 13.5% to 14.5% for young adults aged from 20 years to 44 years. Meanwhile, in the case of middle-aged adults from 45 to 6 years, the incidence rate was 44.3% to 45.8%, and it was 63.3% to 69.7% for old adults aged more than 65 years. Therefore, with these increased incidences, there is a huge demand for PCSK inhibitors in the overall country.

The structured healthcare system, drug approvals, the presence of both renewal and initial medical coverages, provincial funding, and the existence of pharmaceutical associations and organizations are a few factors that are responsible for bolstering the market in Canada. As stated in an article published by the Government of Canada in June 2025, there will be ongoing support provision with the intention of transforming the domestic healthcare system by generously investing approximately USD 200 billion for more than 10 years. This is poised to be suitable through the Working Together to Improve Health Care for Canadians Plan, which comprises direct support solutions to territories and provinces through bilateral deals. Therefore, based on this initiative, the country consists of sustainable and modernized healthcare systems that cater to generous spending and suitable results, thus driving the market upliftment.

Modern and Sustainable Healthcare Systems of Canada, 2026

|

Department Indicators |

Results |

Target |

Target Date |

|

National Health Spending as a GDP% |

2021-2022: 13.1% |

Between 11.0% and 13.4% |

March 2026 |

|

2022-2023: 12.0% |

|||

|

2023-2024: 12.1% |

|||

|

Real Per Capita Health Expenditure |

2021-2022: USD 4,998 |

Between USD 5,995 and USD 7,328 |

March 2026 |

|

2022-2023: USD 4,802 |

|||

|

2023-2024: USD 4,777 |

|||

|

Drug Spending as a GDP% |

2021-2024: 1.7% |

Between 1.0% and 2.0% |

March 2026 |

|

Family Physicians' Percentage Utilizing Electronic Medical Records |

2021-2022: 86.0% |

Almost 95.0% |

March 2026 |

|

2022-2024: 92.6% |

Source: Government of Canada

APAC Market Insights

The Asia Pacific is expected to emerge as the fastest-growing region in the market during the forecast period. The market’s development in the region is highly propelled by increased urbanization, dietary modifications, a rise in heart disease burden, and optimized healthcare services across the majority of economies. As stated in an article published by NLM in June 2024, the incorporation of high-quality dietary patterns in the region has led to lower cardiac risks, accounting for 16% to 22%. Besides, the quality indices of the regional diet ranged between 0.79 and 0.90, while quality indices for the international diet intake ranged from 0.69 to 0.88. Therefore, it can be indicated that there is a huge demand for present dietary guidelines in both the region and diet quality indices, which are further poised to improve in reflecting updated dietary suggestions for cardiovascular diseases.

The PCSK9 inhibitor market in China is gaining increased traction, owing to reduced physical activities, the heightened demand for innovative cholesterol-lowering therapies, robust domestic research and developmental efforts, and governmental support for biologics. As per the April 2025 Mercator Institute for China Studies report, the aspect of public funding for in-depth research in the biotechnology field has been generous and consistent, amounting to nearly USD 2.9 billion (CNY 20 billion) as of 2023. Based on this fund, the country’s innovation and research capabilities are ahead of its national needs in healthcare. Besides, the country successfully unveiled a 5-year plan for the bioeconomy to excel in bio-manufacturing, bio-security, bio-agriculture, and biopharmacy, thereby making it suitable for boosting the market development.

The aspects of the aging population, the existence of the national healthcare system, the regulation of the pharmaceutical pricing system for controlling expenses, cost-effectiveness models, and contributions from the Agency for Medical Research and Development (AMED) for ensuring innovation in therapies are certain trends that are responsible for fueling the PCSK9 inhibitor market in Japan. As per the June 2025 Cabinet Office Japan data report, the overall population of the country accounted for 123.8 million people as of October 2024, with the more than 65 years old category catering to 36.2 million, which is 29.3% of the total population. Simultaneously, the number of people aged between 65 and 74 years is 15.4 million, which is 12.5% of the overall population, thereby making it suitable for enhancing the market demand in the nation.

Aging Population Trend in Japan, 2024-2070

|

Year |

Aging Population in Numbers |

|

2024 |

12,360 |

|

2025 |

12,326 |

|

2030 |

12,012 |

|

2035 |

11,684 |

|

2040 |

11,254 |

|

2045 |

10,880 |

|

2050 |

12,469 |

|

2055 |

10,061 |

|

2060 |

9,615 |

|

2065 |

9,159 |

|

2070 |

8,700 |

Source: Cabinet Office Japan

Europe Market Insights

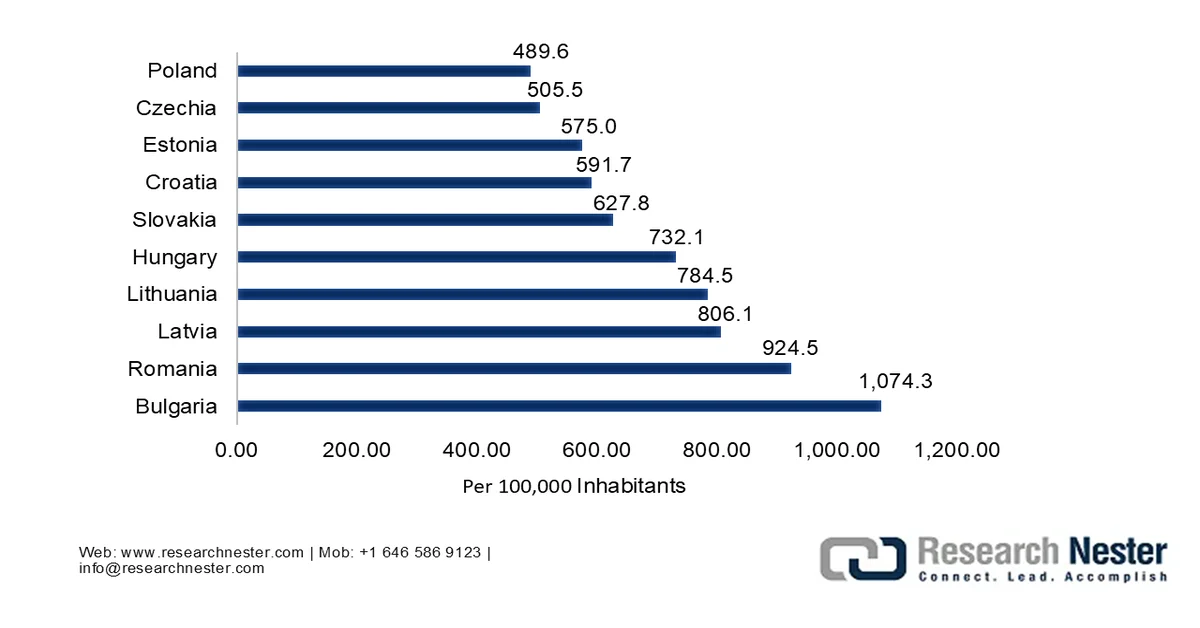

The Europe market is predicted to account for lucrative growth and expansion by the end of the stipulated period. The market’s growth in the region is highly driven by established health and medical facilities, the presence of favorable reimbursements, and an increase in the prevalence of heart diseases. According to a data report published by the Eurostat in July 2025, the standardized death rate for diseases of the circulatory system, especially in Bulgaria, was 6.3 times higher than in France as of 2022. Besides, there was a decrease in the number of heart bypasses per 100,000 inhabitants across 4 countries as of 2023. Overall, there are 1.6 million deaths in the region from diseases that are associated with the circulatory system, which is equivalent to 32.7% deaths, thereby demonstrating an optimistic outlook for the market’s expansion.

Standardized Death Rates in Europe from Disease of the Circulatory System, 2022

Source: Eurostat

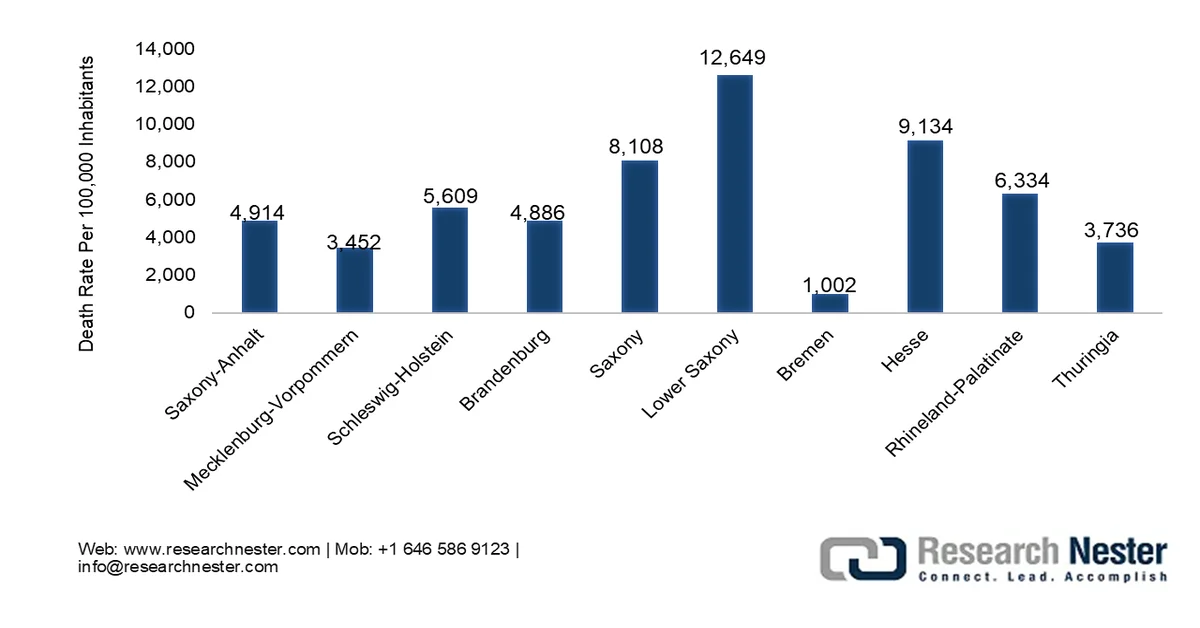

Germany in the PCSK9 inhibitor market is projected to witness suitable exposure due to the increased prevalence of coronary heart disorder, the massive patient pool, a surge in governmental healthcare expenditure, and reimbursement services and solutions. As per an article published by RKI in December 2025, coronary heart disorder is considered the leading cause of mortality and death in the country, resulting in 119,795 deaths as of 2023. In this regard, myocardial infarction is one of the life-threatening acute complications of the disorder, leading to permanent damage to the myocardial tissue in particular. Besides, the population in the country readily considers cardiac arrhythmia and heart failure as severe complications that eventually contribute to the increased mortality rate of the disorder, thereby enabling the increased demand for the market.

Coronary Heart Disorder Death Rate Across Different Cities in Germany, 2023

Source: RKI

The increased prevalence of obesity, awareness regarding cholesterol management, regulating drug pricing strategies, the demand for prescription medications, the shift to personalized treatment services, and the promotion of generic drugs by the government are certain factors that are contributing to the importance of the PCSK9 inhibitor market in France. As stated in an article published by the C3 Health Organization in 2024, a survey-based clinical study was conducted on 12,000 French participants to evaluate pediatric obesity. The study demonstrated that a body mass index (BMI) below 18.5 is usually considered underweight, above 25 is overweight, and more than 30 is obese. Therefore, based on the survey, 1 adult in 6 usually resides with obesity in the country. In addition, 17% of the population is obese, in comparison to 15% 8 years ago, which accounted for almost 8,567,128 patients, thereby enhancing the market exposure.

Key PCSK9 Inhibitor Market Players:

- Amgen (U.S.)

- Sanofi/Regeneron (France/U.S.)

- Novartis (Switzerland)

- Merck & Co. (U.S.)

- LIB Therapeutics (U.S.)

- Akeso, Inc. (China)

- Junshi Biosciences (China)

- Innovent Biologics (China)

- Jiangsu Hengrui Medicine (China)

- Suzhou Ribo Life Science Co., Ltd. (China)

- Everest Medicines (China)

- Eli Lilly and Company (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Amgen is a pioneer in the PCSK9 inhibitor space with its first-in-class monoclonal antibody therapy. The company has established a strong commercial footprint across North America and Europe, leveraging extensive cardiovascular clinical trial data to support its market position. Amgen's focus on patient access programs and value-based contracting has been central to its competitive strategy.

- Sanofi/Regeneron markets a well-established monoclonal antibody PCSK9 inhibitor that competes directly in the same indication space. The companies have differentiated themselves through a robust clinical trial program and strategic pricing initiatives. Their combined global commercial infrastructure provides broad market coverage, particularly in secondary prevention settings.

- Novartis’ first-in-class siRNA therapy that offers a distinctly convenient twice-yearly dosing schedule. This innovative modality positions the company as a leader in shifting patient adherence paradigms. Novartis leverages its strong cardiovascular franchise and global supply chain capabilities to drive adoption across multiple regions.

- Merck & Co. is advancing a novel oral peptide PCSK9 inhibitor through late-stage clinical development. This oral formulation, if approved, could fundamentally transform the market by overcoming injection-related barriers. Merck's deep expertise in cardiovascular medicine and extensive primary care sales force position it as a formidable future competitor.

- Akeso, Inc. has developed an innovative PCSK9 monoclonal antibody for the domestic market. The company is focused on addressing the large and growing cardiovascular patient population in China. Its regulatory approvals and commercial partnerships are enabling expansion within the rapidly evolving the Asia Pacific region.

Here is a list of key players operating in the global market:

The PCSK9 inhibitor market is moderately consolidated, dominated by large multinational pharmaceutical companies with established cardiovascular portfolios. Amgen, Sanofi/Regeneron, and Novartis are the key leaders, with their respective marketed products, such as Repatha, Praluent, and Leqvio. The competitive dynamics are shifting with the entry of novel oral and long-acting candidates, as well as regional players like China's Akeso and Junshi Biosciences gaining ground. Besides, in June 2025, Eli Lilly and Company significantly acquired Verve Therapeutics, Inc. for a purchase price of USD 10.5 per share in cash, and readily expanded its PCSK9 inhibitor portfolio for aiding atherosclerotic cardiovascular disease through standard treatments.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, LIB Therapeutics Inc. proclaimed the U.S.-based commercial launch of LEROCHOL® Injection 300 mg/1.2 mL, which is a once-monthly, self-administered third-generation Proprotein Convertase Subtilisin/Kexin type 9 (PCSK9) inhibitor.

- In March 2026, Suzhou Ribo Life Science Co., Ltd.’s PCSK9-targeting siRNA drug RBD7022 / QLC7401, unveiled by collaborating with Qilu Pharmaceutical Co., Ltd., accomplished the Phase III clinical trial registration.

- In December 2025, Everest Medicines denoted that its subsidiary, Everest Medicines Co., Ltd., entered into a tactical agreement with Hasten Biopharmaceutical Cp., Ltd. for leveraging the commercialization of Lerodalcibep, which is a small protein-binding, novel, and third-generation PCSK9 inhibitor.

- Report ID: 8634

- Published Date: Jun 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

PCSK9 Inhibitor Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.