PAN-based Carbon Fiber Precursor Market Outlook:

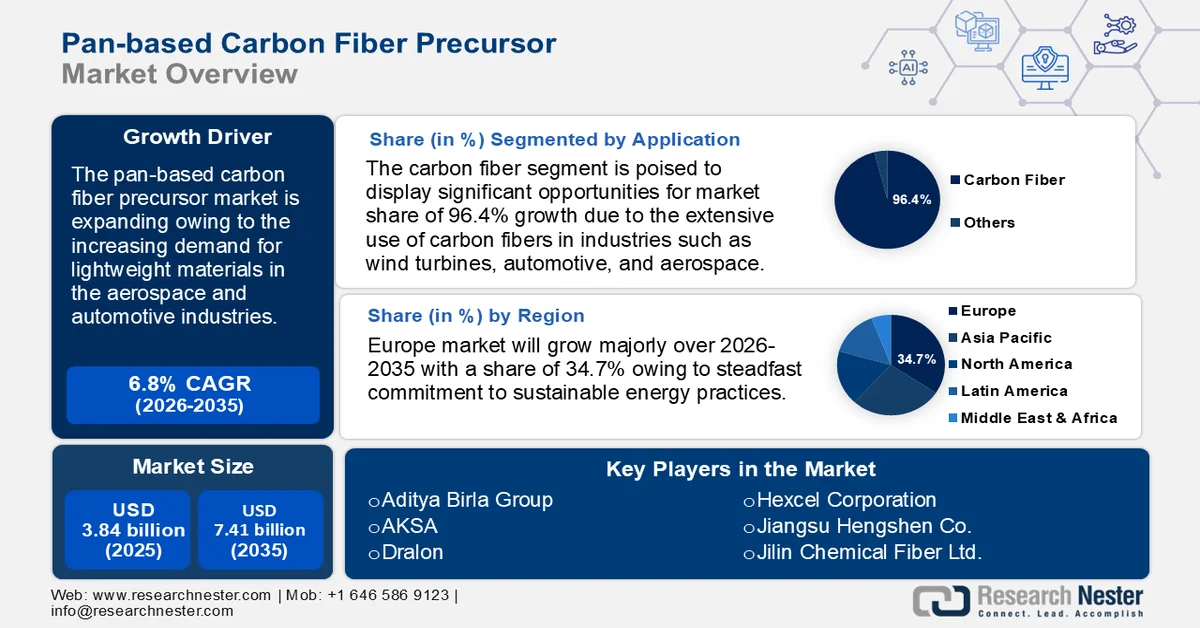

PAN-based Carbon Fiber Precursor Market size was valued at USD 3.84 billion in 2025 and is expected to reach USD 7.41 billion by 2035, expanding at around 6.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of PAN-based carbon fiber precursor is evaluated at USD 4.08 billion.

The global PAN-based carbon fiber precursor market is anticipated to grow due to the increasing demand for lightweight materials in the aerospace and automotive industries. There has been a notable trend towards materials that can offer strength without adding extra weight as a result of these industries' unrelenting quest for performance improvements and fuel efficiency. Carbon fibers, which are made from PAN-based precursors, are leading this change because of their remarkable strength-to-weight ratio.

In the aerospace industry, lowering aircraft weight is essential for increasing operational costs and fuel efficiency. The manufacture of airplane parts, including wings, propulsion systems, and fuselages, heavily relies on carbon fibers. In addition to being lighter than conventional materials like steel and aluminum, these materials also provide better stiffness and corrosion resistance, both of which are essential for preserving the structural integrity of airplanes under the strain of high altitudes and fluctuating temperatures.

In a similar vein, the automotive sector is constantly under pressure to adhere to strict international pollution regulations, which has increased interest in lightening vehicles. Metal parts of automobiles, such as the chassis, engine parts, and body panels, are increasingly being replaced with carbon fibers.

Key PAN-based Carbon Fiber Precursor Market Insights Summary:

Regional Highlights:

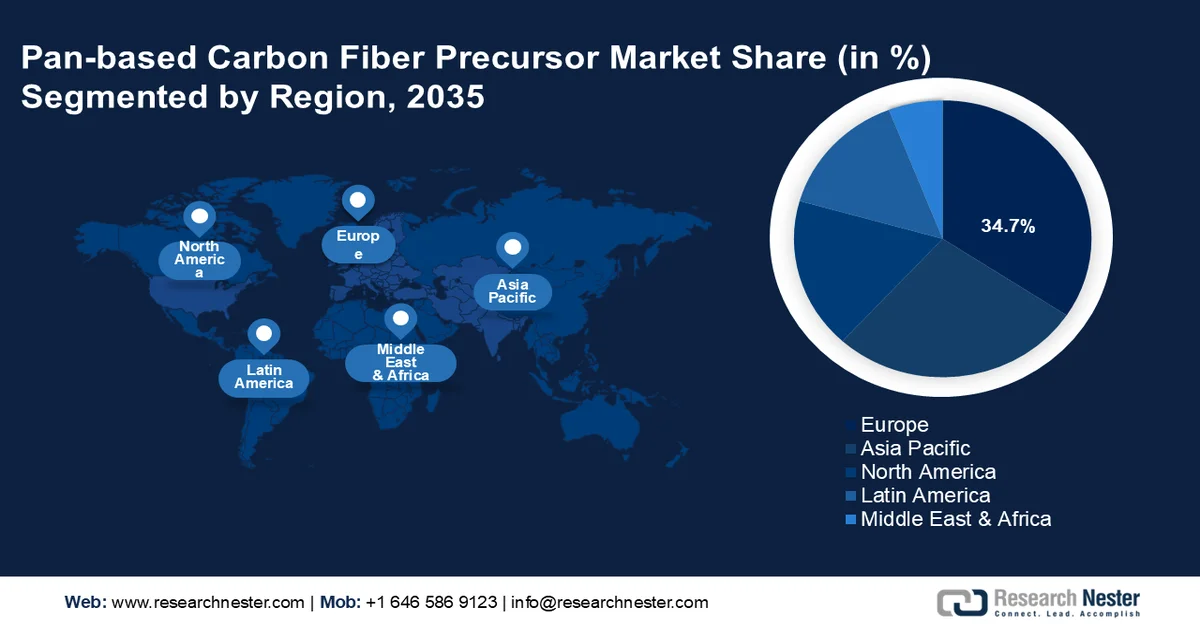

- The Europe PAN-based carbon fiber precursor market is projected to dominate with over 34.7% revenue share by 2035, attributed to stringent environmental regulations and strong governmental backing for sustainable energy and carbon emission reduction initiatives

- Asia Pacific is anticipated to witness significant growth by 2035, fueled by rapid industrialization and expanding demand from aerospace, automotive, military, and renewable energy sectors including wind energy applications

Segment Insights:

- The carbon fiber segment in the PAN-based carbon fiber precursor market is projected to command approximately 96.4% revenue share by 2035, propelled by the escalating demand for high-strength, lightweight materials across wind energy, automotive, aerospace, and sports equipment industries

- The big tow segment is expected to secure a substantial share by 2035, stimulated by its cost-effectiveness and growing preference in aerospace and automotive sectors requiring lightweight and high-structural-stability materials

Key Growth Trends:

- Recent innovations in recycling technologies for carbon fibers

- Rapid transition to renewable energy and infrastructure sectors

Major Challenges:

- Higher production costs

- Lack of awareness

Key Players: Novartis AG, Teva Pharmaceutical Industries Limited, Eli Lilly and Company, Dr. Reddy's Laboratories Ltd., Sun Pharmaceutical Industries Limited, Torrent Group, Apotex Inc., Aurobindo Pharma Ltd, Viatris, Alkermes, Inc.

Global PAN-based Carbon Fiber Precursor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.84 billion

- 2026 Market Size: USD 4.08 billion

- Projected Market Size: USD 7.41 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Europe (34.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Japan, China, Germany, South Korea

- Emerging Countries: China, India, Japan, South Korea, Taiwan

Last updated on : 25 February, 2026

PAN-based Carbon Fiber Precursor Market - Growth Drivers and Challenges

Growth Drivers

- Recent innovations in recycling technologies for carbon fibers: Pyrolysis represents a method whereby used carbon fiber composites are subjected to heating in an oxygen-free environment, facilitating the decomposition of the resin matrix and the extraction of the fibers. Recycled fibers, while potentially lacking some of the mechanical properties of virgin fibers, remain suitable for various applications, including consumer goods, construction panels, and non-structural vehicle components. These recycling processes not only contribute to environmental sustainability but also provide a more cost-effective source of carbon fibers compared to the production of new fibers. By minimizing waste and diminishing the need for raw materials, recycling effectively reduces manufacturing costs and mitigates the environmental impact associated with the extraction and processing of new resources. This consideration is particularly vital as environmental regulations continue to tighten and businesses across multiple sectors face increased pressure to demonstrate their commitment to sustainable practices.

- Rapid transition to renewable energy and infrastructure sectors: The design and composition of turbine blades have a significant impact on wind turbine efficiency in the renewable energy sector, especially wind energy. Longer, more effective blades that can produce more power without sacrificing structural integrity are made possible by carbon fibers, which provide the strength and fatigue resistance required. Because carbon fibers are lightweight, they lessen the strain on turbine systems, enabling the construction of larger rotors and taller towers that are better able to harvest wind energy.

The need for carbon fibers in this application is anticipated to increase dramatically as nations continue to make investments to increase their capacity for renewable energy in order to achieve climate goals. Carbon fibers can also significantly improve the longevity and durability of important structures in the infrastructure industry. Carbon fiber reinforcements can be advantageous for applications like buildings, bridges, and tunnels, particularly in seismically active regions. Traditional steel rebar, which corrodes over time, can be replaced with carbon fibers for reinforcement in concrete. This promotes safety, lowers maintenance costs, and prolongs the life of structures.

Challenges

- Higher production costs: There are several steps involved in producing carbon fibers from PAN-based precursors, and each one calls for exact control and premium inputs. It takes a lot of energy to stabilize the PAN polymer in the first place, and regulated heating under strain is necessary to prevent melting. The next step is carbonization, which involves heating the stabilized fibers to extremely high temperatures in an inert atmosphere in order to eliminate non-carbon components. In order to improve the ordering of the carbon atoms, fibers may need to undergo an extra graphitization stage, which involves heating them to even higher temperatures. These procedures increase the capital expenses because they not only use a lot of energy but also call for sophisticated equipment that can maintain exact environmental conditions.

- Lack of awareness: Because they lessen rutting, cracking, and stripping, asphalt additives can greatly extend the service life of asphalt pavements. As a result, asphalt road surfaces require less upkeep. However, because they are focused on lowering the cost of materials and construction, contractors and road builders in emerging nations do not take these considerations into account. Many road builders and contractors may not be aware of the various types of asphalt additives that are available, their benefits, and the proper way to include them in asphalt mixtures. This ignorance could lead to the inappropriate application or underuse of asphalt additives, which would impair the pavement's performance.

PAN-based Carbon Fiber Precursor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 3.84 billion |

|

Forecast Year Market Size (2035) |

USD 7.41 billion |

|

Regional Scope |

|

PAN-based Carbon Fiber Precursor Market Segmentation:

Application Segment Analysis

In PAN-based carbon fiber precursor market, carbon fiber segment is set to account for revenue share of around 96.4% by 2035. The conversion of pan-based precursors into carbon fibers, which are crucial parts of numerous high-value applications in diverse industries, is driving the segment’s growth. The significant market share of this segment is driven by the extensive use of carbon fibers in industries like wind turbines, sports equipment, automotive, and aerospace. The requirement for materials with high strength and low weight that improve performance and efficiency is driving the demand.

Type Segment Analysis

The big tow segment is anticipated to garner a significant PAN-based carbon fiber precursor market share during the assessed period. Its extensive use in sectors like aerospace and automotive that demand lightweight, high-strength materials greatly benefits this segment. Big Tow carbon fibers are favored for their cost-effectiveness in large-scale manufacturing setups and provide higher structural stability because to their enormous number of filaments. The market for Big Tow carbon fibers is still being driven by the continuous push for performance and fuel efficiency in these industries.

Our in-depth analysis of the global PAN-based carbon fiber precursor market includes the following segments:

|

Type |

|

|

Application |

|

|

End use |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

PAN-based Carbon Fiber Precursor Market - Regional Analysis

European Market Insights

Europe PAN-based carbon fiber precursor market is expected to dominate revenue share of over 34.7% by 2035. Europe's aggressive enforcement of strict environmental laws and steadfast commitment to sustainable energy practices are the main drivers of this dominance. European governments have been instrumental in supporting efforts to reduce carbon emissions and improve energy efficiency in a variety of industries, including the maritime sector. In addition to setting a precedent for international norms, these initiatives highlight how crucial Pan-based carbon fiber precursor technologies are to achieving challenging environmental goals. The demand for Pan-based carbon fiber precursor solutions has been significantly increased by the strong regulatory support from European authorities, establishing them as essential tools in Europe's effort to reduce emissions across all industries.

Additionally, significant advancements in research and development within the PAN-based carbon fiber precursor market have been sparked by Europe's unwavering dedication to sustainability. These developments have produced Pan-based carbon fiber precursor solutions that are more effective, safe, and environmentally friendly, reaffirming Europe's position as a global leader in advancing cleaner energy sources. In addition to improving the effectiveness of Pan-based Carbon Fiber Precursor technologies, the region's innovative projects establish Europe as a leading innovator and a global benchmark for best practices in the sector.

APAC Market Insights

Asia Pacific PAN-based carbon fiber precursor market is expected to grow at a significant rate during the projected period. End-use industries like aerospace and military, automotive, and renewable energy are rising as a result of the region's rapid industrialization driven by its expanding economy. Additionally, the wind energy sector’s growth in the region contributes to the rising demand for Pan-based carbon fibers, as they are essential for manufacturing durable and efficient win turbine blades.

PAN-based Carbon Fiber Precursor Market Players:

- Aditya Birla Group

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- AKSA

- Dralon

- Farmosa Plastics Corporation

- Hexcel Corporation

- Hyosung Advanced Materials Corporation

- Jiangsu Henghsen Co.

- Jilin Chemical Fiber Ltd.

- ZeroAvia

- Airbus SE

The PAN-based carbon fiber precursor market is defined by the existence of well-established competitors who compete based on technological breakthroughs, product quality, and innovation. Key market players frequently use strategic moves like mergers, acquisitions, and expansions to increase PAN-based carbon fiber precursor market presence and effectively fulfill the growing demand.

Recent Developments

- In March 2025, during the 2025 Airbus Summit, Airbus delivered an update on its plans to lead the future of commercial aviation in the coming decades. The company detailed prospective technology bricks for a next-generation single-aisle aircraft that might enter service in the second half of the 2030s, as well as a revised timeline for maturing hydrogen-powered flying technologies.

- In February 2025, ZeroAvia announced that it has agreed to sell its 600kW electric propulsion system (EPS) to Jetcruzer International for electric flight testing to help refine the design of its Jetcruzer 500E. The development unit EPS is planned to be delivered this spring.

- Report ID: 7507

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.