Optogenetics Market Outlook:

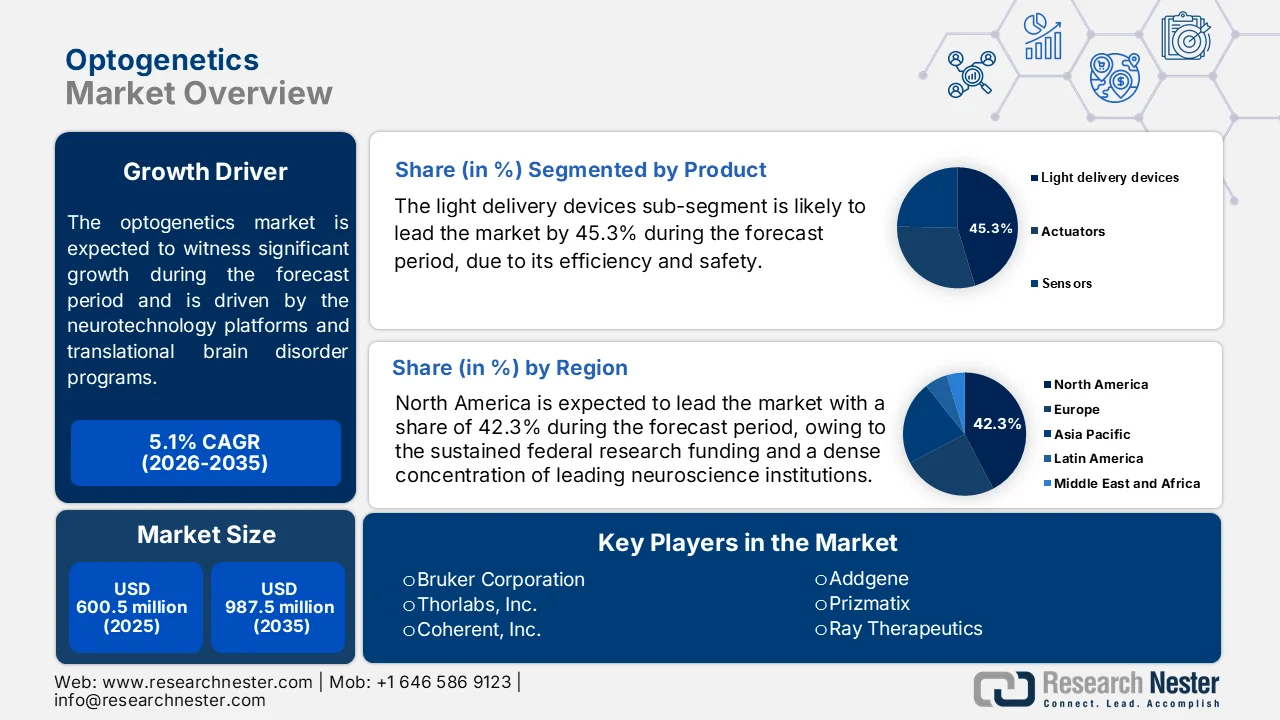

Optogenetics Market size was valued at USD 600.5 million in 2025 and is projected to reach USD 987.5 million by the end of 2035, registering around 5.1% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of optogenetics is estimated at USD 631.1 million.

The optogenetics market is shaped primarily by sustained public-sector investment in neuroscience research, neurotechnology platforms, and translational brain disorder programs. The IEC June 2024 data depicted that the NIH BRAIN Initiative has committed more than USD 5 billion in research support since its launch, funding large-scale tool development, neural circuit mapping, and next-generation intervention technologies that directly support optogenetics-related research ecosystems. Federal funding continues to expand the installed base of advanced optical systems, viral vector development programs, neural recording platforms, and specialized laboratory infrastructure across universities, medical centers, and research institutes. The National Institute of Neurological Disorders and Stroke (NINDS), National Institute of Mental Health (NIMH), and other NIH institutes continue to fund projects focused on neurological and psychiatric disorders, creating long-term demand for optogenetics-enabled preclinical research.

Market activity is also supported by the growing burden of neurological disease. According to the World Health Organization (WHO) March 2024 data, neurological conditions affect more than 3 billion people globally, making them one of the leading causes of illness and disability worldwide. This disease burden is encouraging governments, academic institutions, and nonprofit organizations to invest in advanced brain research tools capable of improving understanding of neural circuits and therapeutic targets. As a result, procurement demand for light-delivery systems, optical components, viral vectors, laboratory services, and integrated neurotechnology platforms continues to expand across research-focused end users.

Key Optogenetics Market Insights Summary:

Regional Highlights:

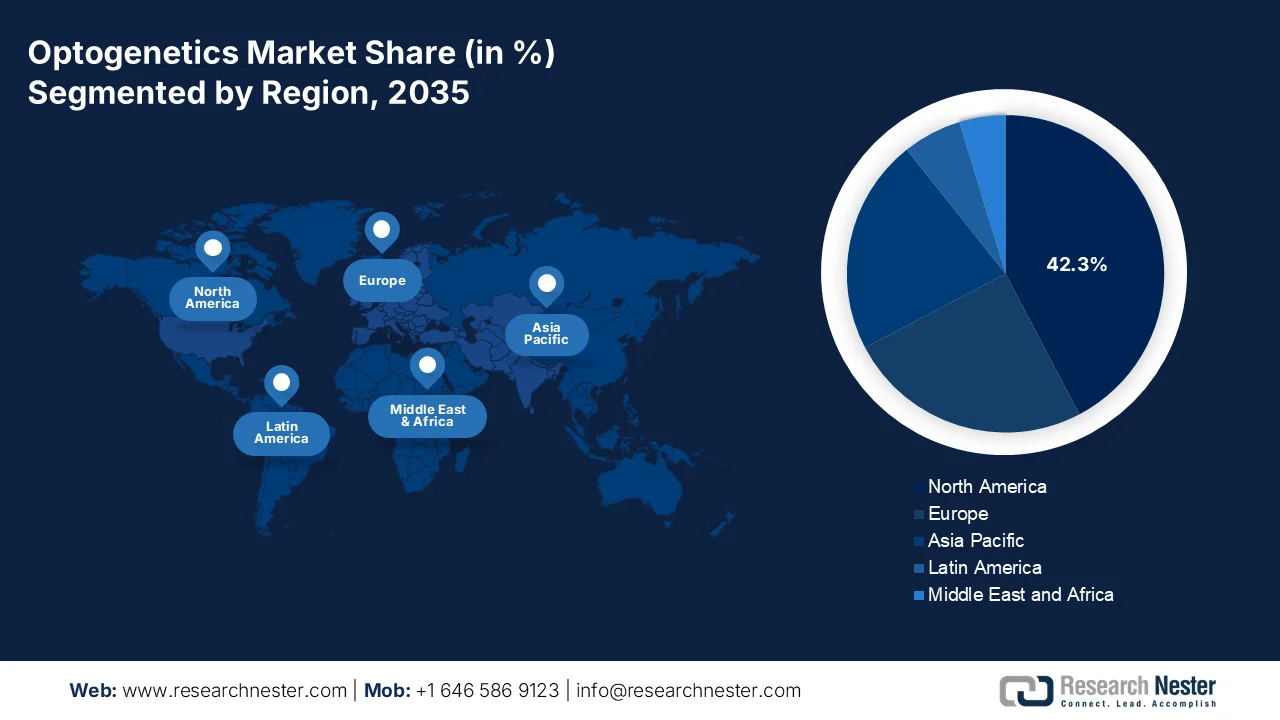

- North America is anticipated to secure 42.3% revenue share by 2035 in the optogenetics market, supported by sustained federal research funding and a dense concentration of leading neuroscience institutions

- Asia Pacific is projected to witness accelerated expansion across 2026-2035, fueled by rapid infrastructure development, government-backed neuroscience programs, and rising adoption of cost-effective LED-based systems

Segment Insights:

- In the optogenetics market, the light delivery devices segment is forecast to capture 45.3% share by 2035, propelled by their efficiency and safety

- The neuroscience (behavioral and neural circuit mapping) application segment is expected to maintain market leadership through 2035, attributed to expanding neuroscience research infrastructure investments and increasing deployment of optogenetic stimulation and recording platforms

Key Growth Trends:

- Increasing public investment in vision restoration research

- Expansion of academic research infrastructure

Major Challenges:

- High R&D costs and long development cycles

- Regulatory hurdles for therapeutic applications

Key Players: Bruker Corporation (U.S.), Thorlabs, Inc. (U.S.), Coherent, Inc. (U.S.), Addgene (U.S.), Prizmatix (Israel), Ray Therapeutics (U.S.), Nanoscope Therapeutics Inc. (U.S.), AviadoBio Ltd. (UK).

Global Optogenetics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 600.5 million

- 2026 Market Size: USD 631.1 million

- Projected Market Size: USD 987.5 million by 2035

- Growth Forecasts: 5.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Australia, France, United Kingdom, Canada

Last updated on : 23 June, 2026

Optogenetics Market - Growth Drivers and Challenges

Growth Drivers

- Increasing public investment in vision restoration research: Vision restoration programs are emerging as an important growth area supporting optogenetics demand. Government-funded institutions are actively exploring optogenetic approaches for retinal disorders and blindness. The U.S. National Eye Institute (NEI) has highlighted optogenetic strategies designed to restore visual responses in patients with retinal degeneration. According to the WHO February 2026 data, at least 2.2 billion people globally live with near or distance vision impairment, creating a substantial need for innovative treatment approaches. As governments increase spending on vision research and disability reduction programs, demand for optogenetics-compatible gene delivery technologies, optical devices, and translational research services is expected to rise. These investments are encouraging partnerships between academic institutions, hospitals, and technology developers, further strengthening the market landscape.

- Expansion of academic research infrastructure: Universities and public research institutions remain the largest users of optogenetics technologies. Government-funded grants are enabling laboratories to acquire sophisticated imaging systems, optical stimulation devices, electrophysiology equipment, and genetic engineering tools. In the United States, NIH April 2025 data states that the funding exceeded USD 47 billion annually, supporting biomedical research programs across thousands of institutions. Public-sector investments also support training programs that increase the number of scientists using advanced neurotechnology tools. As universities continue to receive funding for neuroscience, neurodegeneration, psychiatric disorders, and brain-machine interface research, procurement demand for optogenetics platforms and associated consumables is expected to increase.

Challenges

- High R&D costs and long development cycles: Developing new opsins, viral vectors, or integrated light delivery systems requires years of preclinical validation and substantial capital investment. Small manufacturers struggle to fund iterative prototyping and in vivo testing. Companies mitigate this by forming co-development partnerships with academic research labs, sharing intellectual property and reducing internal R&D expenses while accelerating time-to-market for novel optogenetic platforms.

- Regulatory hurdles for therapeutic applications: Optogenetic products intended for human therapy face complex regulatory pathways as combination gene-and-device products. Manufacturers must navigate overlapping agency requirements for viral vector safety and implantable light sources. Companies tackled this by securing orphan drug designation early, streamlining clinical development and gaining regulatory guidance for their vision restoration optogenetic therapy.

Optogenetics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.1% |

|

Base Year Market Size (2025) |

USD 600.5 million |

|

Forecast Year Market Size (2035) |

USD 987.5 million |

|

Regional Scope |

|

Optogenetics Market Segmentation:

Product Segment Analysis

Under the product segment, the light delivery devices are dominating and is poised to hold the share value of 45.3% by the end of 2035. The segment is driving due to their efficiency and safety. According to the DZHK July 2025 data, demonstrates an ultra-sensitive light-activated protein that requires only minimal light intensity to control cell activity. This innovation is directly relevant to LED-based systems because LEDs can deliver precise, low-level, and chronic illumination without thermal damage—ideal for restoring sight, hearing, or regulating heart rhythm. Such advancements reduce phototoxicity risks and enable longer therapeutic windows. Consequently, LEDs become the preferred light source for next-generation clinical optogenetics, reinforcing their dominant revenue share in the market.

Application Segment Analysis

In the optogenetics market, the application segment is led by neuroscience, specifically behavioral and neural circuit mapping. Governor Kathy Hochul in October 2025 announced USD 10 million investment to launch the SUNY Brain Institute will expand neuroscience research infrastructure across multiple SUNY campuses, including Upstate Medical University and Downstate Health Sciences University. This funding supports shared equipment such as optogenetic stimulation systems, fiber-optic recording rigs, and behavioral tracking platforms essential for circuit mapping studies. By enabling researchers to manipulate and record specific neural pathways in awake-behaving animal models, the Institute accelerates research into learning, addiction, and motor disorders. Such state-level investments directly drive demand for optogenetic tools, reinforcing neuroscience as the highest-revenue application segment in the market.

Light Source Segment Analysis

The light source segment is dominated by high-power, multi-wavelength LEDs due to their superior precision, safety, and versatility. Unlike traditional lasers or arc lamps, these LEDs can deliver multiple wavelengths simultaneously, enabling researchers to activate and silence distinct neuronal populations expressing different opsins within the same biological sample. Their low heat emission minimizes tissue damage during chronic in vivo studies, while compact form factors allow integration into wireless and miniaturized headstage systems. Furthermore, multi-wavelength LEDs offer rapid switching between excitation channels, facilitating complex behavioral and circuit-mapping experiments. As optogenetics expands into translational research, these LED systems remain the preferred illumination solution for reliable and reproducible neural control.

Our in-depth analysis of the optogenetics market includes the following segments:

|

Segment |

Subsegments |

|

Product |

|

|

Technology |

|

|

Application |

|

|

End user |

|

|

Light Source |

|

|

Delivery Mode |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Optogenetics Market - Regional Analysis

North America Market Insights

North America is dominating the optogenetics market and is expected to hold the regional revenue share of 42.3% by the end of 2035. The region is driven by sustained federal research funding and a dense concentration of leading neuroscience institutions. The region benefits from well-established core facilities that aggregate equipment procurement, reducing individual lab capital burdens while ensuring high utilization rates for advanced stimulation and imaging systems. Academic and government research priorities increasingly emphasize translational neuropsychiatric and cardiovascular applications, steering demand toward integrated closed-loop platforms that combine optogenetic stimulation with electrophysiological recording. State-level initiatives further expand shared infrastructure across university systems. Additionally, growing collaboration between academic investigators and commercial suppliers accelerates the development of modular, interoperable systems, fostering a competitive yet collaborative ecosystem that reinforces North America's market leadership.

The continued federal investment in neuroscience and vision research is shaping the optogenetics market in the U.S. The Congress.gov May 2023 data, under funding authorized through the 21st Century Cures Act, the U.S. government allocated an additional USD 462 million to advance the Precision Medicine Initiative and the Brain Research Through Advancing Innovative Neurotechnologies (BRAIN) Initiative, accelerating research into neural circuits, brain disorders, and innovative neurotechnology platforms. Additionally, the National Eye Institute (NEI) received approximately USD 896 million in FY2024 funding, supporting retinal disease research and vision restoration programs where optogenetic approaches are increasingly investigated. These government investments strengthen demand for optical stimulation systems, imaging technologies, viral vectors, and specialized neuroscience research services across U.S. academic and research institutions.

The growing investments in brain health research and neuroscience capacity building is shaping the optogenetics market in Canada. The Government of Canada July 2025 data states that Brain Canada allocated CAD 2.4 million to the Brain Health Care (BHCare) and Support in Aging Training Platform, aimed at developing the next generation of scientists, clinicians, and policy leaders working in brain health. Additionally, CAD 2.1 million was provided to the Brain Health Resources and Integrated Diversity (BRAID) Hub, a national initiative focused on translating evidence-based brain health research into practical tools and educational resources. These investments strengthen Canada's neuroscience research infrastructure, expand skilled talent pools, and support increased utilization of advanced technologies, including optogenetics, across research institutions and collaborative brain health programs.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the optogenetics market. The region is characterized by rapid infrastructure expansion across established research hubs in Japan, South Korea, Australia, and emerging centers in China, India, and Malaysia. Government-backed neuroscience missions and brain research programs are accelerating the installation of core optogenetic facilities at major universities and research institutes. The region shows strong preference for cost-effective, user-friendly LED-based systems over expensive laser configurations, driven by price-sensitive academic budgets. Increasing cross-border collaborations with North American and European institutions are facilitating technology transfer and training. Additionally, pharmaceutical companies in the region are adopting optogenetic platforms for target validation in neurodegenerative and cardiovascular diseases, creating sustained commercial demand beyond traditional academic customers.

The government funding for biotechnology and advanced scientific research continues is fueling the optogenetics market in India. According to the PIB March 2026 data, the Department of Biotechnology (DBT) received an allocation of approximately ₹3,446.64 crore, supporting life sciences, genomics, neurobiology, and translational research programs that contribute to demand for optogenetics-related tools. In addition, the PIB February 2025 data shows that the Government of India has committed ₹20,000 crore to the Anusandhan National Research Foundation (ANRF) to strengthen research and innovation ecosystems across universities and research institutions. These investments are enhancing neuroscience research capacity, laboratory infrastructure, and academic-industry collaboration, creating opportunities for suppliers of optical imaging systems, genetic engineering technologies, and specialized research services.

The sustained government investment in scientific research and brain science initiatives is driving the optogenetics market in China. According to the People’s Republic of China September 2025, the country's research and experimental development (R&D) expenditure reached USD 506.41 billion in 2024, representing continued growth in funding for advanced life sciences, neuroscience, and biomedical technologies. In addition, Chinese Academy of Sciences December 2025 data shows that China's Basic Research Program expenditure increased to approximately RMB 249.7 billion in 2024, reflecting strong government emphasis on fundamental scientific discovery, including brain function and neural circuit research. These investments strengthen the research infrastructure used by universities, institutes, and hospitals, supporting demand for optogenetics-related imaging systems, optical instruments, genetic engineering technologies, and laboratory services across the country's expanding neuroscience research ecosystem.

Europe Market Insights

The optogenetics market in Europe is underpinned by a strong network of publicly funded research consortia and centralized core facilities spanning Germany, the UK, France, and the Nordic countries. Collaborative frameworks such as pan-European neuroscience initiatives promote shared equipment models, reducing per-institution capital expenditure while ensuring high utilization of advanced stimulation and imaging systems. European investigators demonstrate a pronounced emphasis on translational applications, particularly in retinal restoration, cochlear implant optimization, and cardiac arrhythmia modulation. The region's regulatory environment for combination gene-device products encourages early-stage clinical development. Additionally, European suppliers compete strongly in precision optics and fiber-optic components, fostering a robust local manufacturing ecosystem that complements academic demand for modular, interoperable optogenetic platforms.

The strong public investment in biomedical and neuroscience research is driving the optogenetics market in Germany. According to the INSTITUTI GAP November 2024 data, the federal government allocated approximately EUR 25.8 billion for education and research in the 2025 federal budget, supporting scientific infrastructure, life sciences, and advanced medical research programs. In addition, Germany's gross domestic expenditure on research and development is reflecting one of the highest R&D investment levels in Europe. These investments enhance the capabilities of universities, research institutes, and healthcare centers engaged in neuroscience and brain-mapping studies, driving demand for optogenetics-related imaging systems, optical instrumentation, genetic engineering technologies, and specialized laboratory research services.

The increased government support for mental health and neuroscience research is driving the optogenetics market in the UK. In May 2026, the Government of UK launched the Mental Health Mission (MHG) with an investment of up to £50 million over five years, funded by the Office for Life Sciences and delivered by the Medical Research Council (MRC). The program aims to advance precision psychiatry by supporting experts in mental health data, genomics, multiomics, digital technologies, and clinical research. In addition, the initiative emphasizes the development of sustainable research infrastructure and industry partnerships. These investments strengthen the UK's neuroscience ecosystem, creating demand for advanced research tools, including optogenetics platforms used to investigate neural mechanisms underlying mental health conditions.

Key Optogenetics Market Players:

- Bruker Corporation (U.S.)

- Thorlabs, Inc. (U.S.)

- Coherent, Inc. (U.S.)

- Addgene (U.S.)

- Prizmatix (Israel)

- Ray Therapeutics (U.S.)

- Nanoscope Therapeutics Inc. (U.S.)

- AviadoBio Ltd. (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Bruker Corporation is leading in the optogenetics market leverages its expertise in advanced imaging and microscopy systems to provide integrated optogenetic solutions. The company offers multimodal platforms combining two-photon microscopy with optogenetic stimulation, enabling real-time neural activity manipulation and observation at cellular resolution.

- Thorlabs, Inc. is a prominent player in the optogenetics market, specializing in modular photonic tools and light delivery systems. The company offers a comprehensive portfolio including high-power LEDs, patch cables, rotary joints, and beam splitters tailored for optogenetic stimulation.

- Coherent, Inc. has established a strong presence in the optogenetics market through its advanced laser diode and fiber-coupled light source technologies. The company’s optogenetic-dedicated lasers offer precise wavelength control, high output stability, and low noise, essential for activating specific opsins in vivo.

- Addgene is dominating in the optogenetics market and occupies a unique and crucial niche as a nonprofit global repository for plasmid reagents. It distributes thousands of optogenetic constructs—including channelrhodopsins, halorhodopsins, and genetically encoded calcium indicators—directly to researchers at low cost.

- Prizmatix is a specialized innovator in the optogenetics market, known for its high-power, multi-wavelength LED systems and fiber-coupled light sources. The company’s flagship products, such as the Ultra-Long Working Distance LED and the OptiLED line, provide precise, collimated light for simultaneous stimulation of multiple opsins.

Here is a list of key players operating in the global optogenetics market:

The optogenetics market is highly consolidated, led by North America firms due to advanced R&D and high procedural volumes. Key players focus on strategic initiatives such as product innovation, geographic expansion into Asia-Pacific, and regulatory approvals. Mergers and acquisitions are common to enhance portfolio diversification and distribution networks. For example, in March 2024 Zylox-Tonbridge announced a new strategic partnership with Avinger. Europe and Japan companies compete through precision engineering and cost-effective solutions, while emerging players from India and South Korea target niche segments. Intense rivalry drives technological integration, including image-guided devices and disposable catheters for peripheral and coronary applications.

Corporate Landscape of the Optogenetics Market:

Recent Developments

- In January 2026, Ray Therapeutics, a clinical-stage biotechnology company developing optogenetic gene therapies for vision restoration, announced the company’s lead program, RTx-015, is currently being evaluated in a Phase 1 clinical trial to treat retinitis pigmentosa (RP).

- In December 2025, Nanoscope Therapeutics Inc. announced that Dr. Jordi Monés and Dr. Allen C. Ho will present Phase 2b/3 RESTORE and Long-Term-Follow-Up REMAIN study results at the FLORetina-ICOOR 2025 Congress, at the Fortezza da Basso in Florence, Italy.

- In October 2025, AviadoBio Ltd. and UgeneX Therapeutics announced an exclusive option and license agreement for the development and commercialization of UGX-202, an investigational, AAV-based gene therapy in clinical development for patients with retinitis pigmentosa (RP), with a second undisclosed indication entering the clinic by year-end.

- Report ID: 8624

- Published Date: Jun 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Optogenetics Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.