Next-Generation Digital Cockpit Market Outlook:

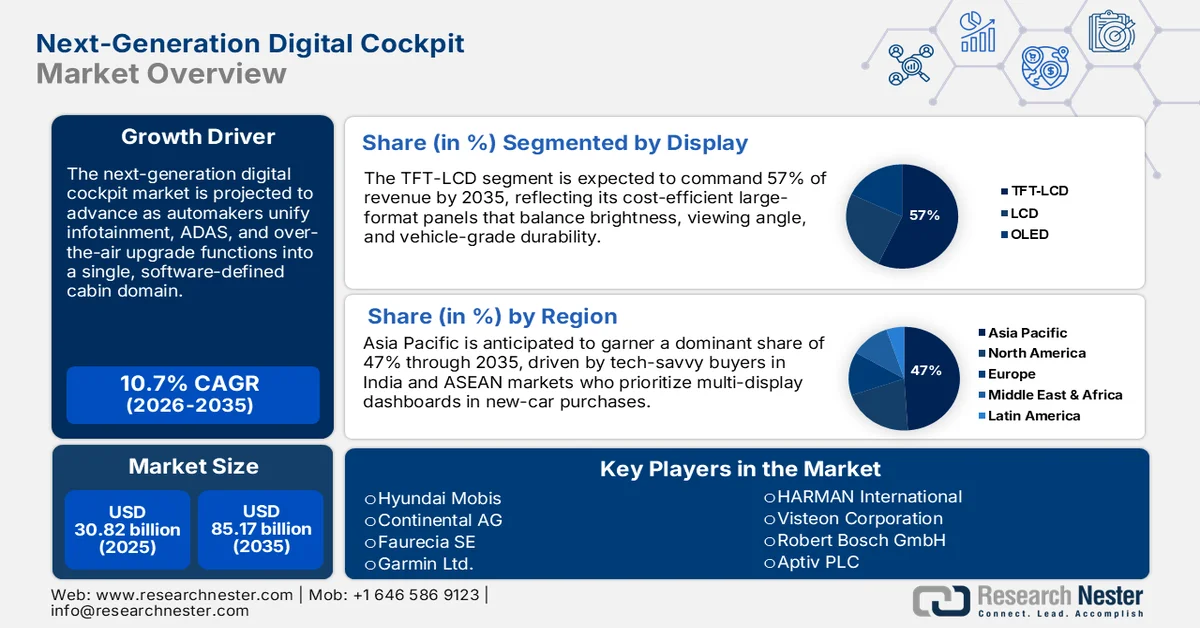

Next-Generation Digital Cockpit Market size was over USD 30.82 billion in 2025 and is projected to reach USD 85.17 billion by 2035, witnessing around 10.7% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of next-generation digital cockpit is evaluated at USD 33.79 billion.

The next-generation digital cockpit market is expanding as automotive manufacturers shift towards software-defined platforms. Car makers pursue smooth infotainment, navigation, and ADAS integration which is driving demand. For instance, NVIDIA launched its DRIVE Thor platform in March 2024, incorporating generative AI along with cockpit functionality onto a single chip. Governments also promote innovation, such as Japan’s Digital Transformation programs, which stimulate innovation in automotive technology. Voice assist, over-the-air software updates, and real-time customization shape cockpit competitiveness. Car makers are more interested in upgradable modularity than in fixed legacy designs. The trend places digital cockpits as strategic differentiators in cars of the future.

User-centric experiences are today central to cockpit design strategy in both the automotive and mobility industries. In November 2023, Visteon and Qualcomm partnered to introduce SmartCore and Snapdragon-enabled immersive digital cockpits. Cloud connections, AI customization, and multi-display technology are transforming dashboards. Sustainability factors also guide materials selection and energy-saving designs. As autonomous and connected vehicle agendas are being made a top national priority, digital cockpits are catapulted to become compliance enablers for regulation. The integration of smart home ecosystems in connected cars is taking shape. Businesses are making significant investments in adaptable architectures to enable cockpit systems across changing EVs as well as AVs.

Key Next-Generation Digital Cockpit Market Insights Summary:

Regional Highlights:

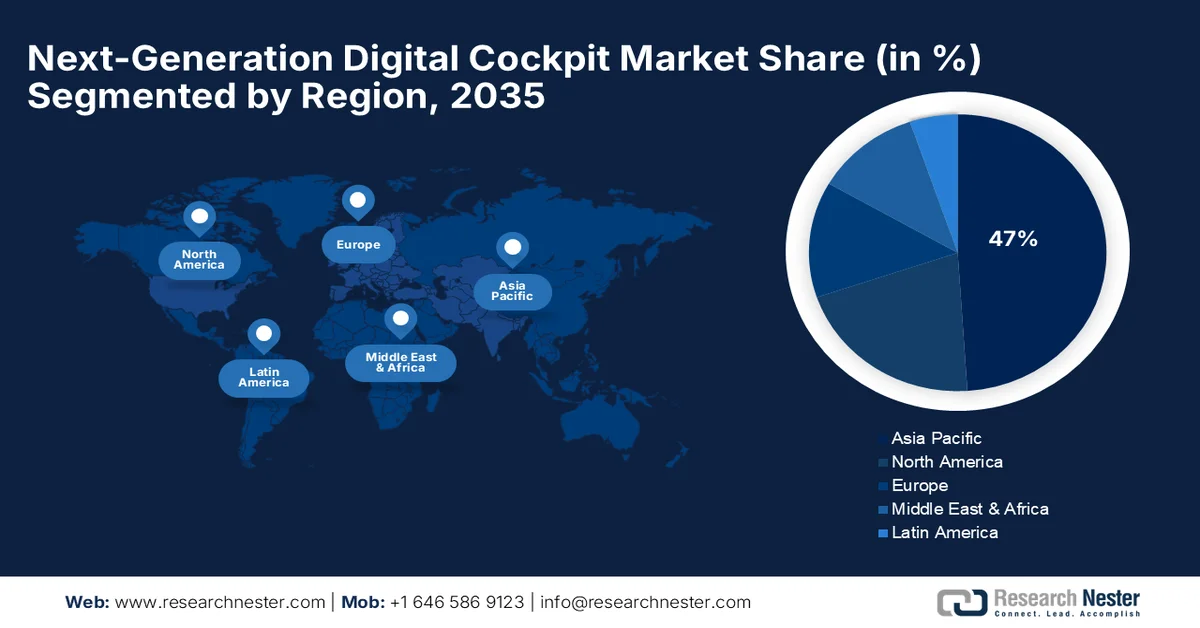

- Asia Pacific is forecast to secure over 47% revenue share of the next-generation digital cockpit market by 2035, impelled by surging EV sales volumes across China and India alongside rapid AI and 5G cockpit integration.

- North America is projected to witness growth exceeding 10% through 2035 in the next-generation digital cockpit market, stimulated by increasing integration of AI-enabled infotainment, cloud services, and advanced driver-assist technologies.

Segment Insights:

- TFT-LCD segment is projected to command over 57% share of the next-generation digital cockpit market by 2035, propelled by its cost efficiency, superior display clarity, and adaptability to evolving touchscreen innovations.

- Passenger vehicles segment is anticipated to account for nearly 77% revenue share by 2035 in the next-generation digital cockpit market, driven by accelerating consumer demand for premium in-vehicle digital experiences and expanding EV adoption.

Key Growth Trends:

- Rise of software-defined vehicles and OTA integration

- Combining AI with generative intelligence in in-vehicle experiences

Major Challenges:

- Data privacy and security issues in connected cockpits

- Complicated hardware-software integration impacts commercialization

Key Players: Hyundai, General Motors, Volkswagen, Li Auto, Ford, Tesla, Porsche, Audi, Jaguar, Mercedes Benz, Chrysler, BMW.

Global Next-Generation Digital Cockpit Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 30.82 billion

- 2026 Market Size: USD 33.79 billion

- Projected Market Size: USD 85.17 billion by 2035

- Growth Forecasts: 10.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (47% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, South Korea

- Emerging Countries: China, India, Japan, South Korea, Thailand

Last updated on : 25 February, 2026

Next-Generation Digital Cockpit Market - Growth Drivers and Challenges

Growth Drivers

- Rise of software-defined vehicles and OTA integration: Automakers are designing cars more like digital platforms that need dynamic cockpit over-the-air updates. Marelli joined forces with Sibros in January 2023 to integrate OTA solutions into its Mind-Xp Cockpit Domain Controller. OTA functionality makes cockpit investments future-proof through real-time feature upgrades. Constant software updating enables security patches, infotainment enhancement, and dynamic UI customization. Recall costs are saved, as well as customer loyalty, by OEMs through OTA-enabled cockpits. OTA is also instrumental in keeping regulatory compliance in data-centric ecosystems in check. Digital cockpit evolution comes hand in hand with the increasing software-defined vehicle structures.

- Combining AI with generative intelligence in in-vehicle experiences: AI is revolutionizing how drivers interact with cockpit interfaces, from customization to predictive diagnosis. In March 2025, Qualcomm and Visteon reimagined intelligent cockpits through the power of generative AI to maximize user experience. Autonomous driving dashboards, mood-sensitive UIs, and real-time voice assistants come to the forefront. Seamless multimodal operation across touch, gesture, and voice input becomes a reality through AI. Predictive diagnosis and health checks are more and more a part of digital cockpits. Consumers demand smartphone-like, intuitive, personalized experiences. As cars become personal digital environments, cockpit transformation through AI goes into overdrive.

- Expanding collaborations between technology majors and auto manufacturers: Strategic partnerships are accelerating innovation in cockpit ecosystems in digital space. In November 2023, Amazon reached a partnership agreement with Hyundai to incorporate Alexa and AWS cloud services in Hyundai cockpit platforms. Cross-industry partnerships combine automaking with technology know-how in areas such as AI, cloud, and edge computing. These partnerships enable end-to-end connected environments in areas such as entertainment, navigation, and smart home controls. Such joint development also shortens time-to-market for new cockpit solutions. Entrance by technology players continues to fuel feature upgrades and app-store-like experiences. Competitive intensity forces OEMs to differentiate through smarter, richer cockpit environments.

Challenges

- Data privacy and security issues in connected cockpits: With cockpits being made into centers of sensitive data, cybersecurity threats worsen. Driver safety and data abuse are threatened by unauthorized access to cockpit tools. Regulatory agencies increasingly require strong compliance with data protection in vehicles. Vehicle networks and over-the-air update mechanisms have to be secured by OEMs. Constant threats demand end-to-end encryption, intrusion detection, and patch management. Businesses have to invest heavily in multi-layered cybersecurity solutions to maintain consumer trust.

- Complicated hardware-software integration impacts commercialization: Achieving harmony between high-end hardware and adaptable, updatable software poses a challenge for cockpit suppliers. The integration of AI, high-end computing, and multi-display setups in real-world applications remains a challenge. Ensuring high-level performance across legacy and next-gen platforms calls for vast testing. Regulatory variability across worldwide markets hinders standardization across markets. Slow validation processes hamper new cockpit launches. Powerful virtual testing environments are essential to cutting time-to-market while ensuring high performance levels along with high levels of safety standards.

Next-Generation Digital Cockpit Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

10.7% |

|

Base Year Market Size (2025) |

USD 30.82 billion |

|

Forecast Year Market Size (2035) |

USD 85.17 billion |

|

Regional Scope |

|

Next-Generation Digital Cockpit Market Segmentation:

Display Segment Analysis

TFT-LCD segment is estimated to hold next-generation digital cockpit market share of more than 57% by 2035, as it is preferred for its relative price, clarity, and longevity. SmartThings Pro and other new display technologies were revealed by Samsung in June 2023, emphasizing TFT-LCD benefits in vehicle applications. These displays have high brightness, responsiveness, and power efficiency, along with competitive costs. TFT-LCDs are highly used by OEMs in mid-tier to high-end models. Continued sensitivity improvements in touchscreen capabilities, along with increasing color vividness, contribute to extending market longevity. TFT-LCDs accommodate changeable dashboard configurations, which are essential in flexible cockpit designs. The segment has a maturing supply chain, as well as continuing to benefit from innovation.

Vehicle Type Segment Analysis

In next-generation digital cockpit market, passenger vehicles segment is set to account for revenue share of around 77% by 2035, reflecting overall digitization trends in consumer mobility. In January 2024, Hyundai Mobis chose BlackBerry QNX to power its next-generation digital cockpit platform, aimed primarily at passenger cars. Premium in-vehicle experiences are driven by increased consumer demand, driving cockpit innovation. Urbanization patterns and EV uptake fuel compact and mid-size passenger cars' penetration of digital cockpits. Strong uptake of infotainment, navigation, and AI-enabled safety components drives demand. Passenger vehicle platforms are more scalable to deliver cockpit software upgrades, as well as feature additions. The integration of autonomous driving in the future is expected to further spur growth.

Our in-depth analysis of the global next-generation digital cockpit market includes the following segments:

|

Equipment Type |

|

|

Display |

|

|

Vehicle Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Next-Generation Digital Cockpit Market - Regional Analysis

APAC Market Insights

Asia Pacific next-generation digital cockpit market is anticipated to dominate revenue share of over 47% by 2035, driven by dramatic EV sales volumes in China and India. In March 2025, ECARX made cockpit supply commitments to Volkswagen, deepening its reach in China’s thriving motor industry. OEMs aggressively adopt AI, cloud, and 5G in cockpit ecosystems. Middle-class customers who are on the rise demand luxury experiences, driving feature pervasiveness. EV affordability drives in China and India make digital cockpits a key to differentiation. Policy environments favor V2X connectivity and autonomous technology pilot programs. Regional vendor hubs make cockpit components more affordable and scalable.

Domestic technology players collaborate with automakers to expedite cockpit innovation in China. Leapmotor adopted Qualcomm’s Snapdragon Cockpit Platform in March 2024, focusing on AI and immersive experiences. Chinese OEMs such as XPeng, NIO, and BYD aggressively introduce multi-screen, AI-infused interiors. Government-imposed requirements for V2X enablement drive cockpit upgrades as an indirect catalyst. Competition in EVs accelerates smart UI, digital dashboard, and personalization of infotainment development. Public sector smart city development provides real-world deployment opportunities for next-gen cockpit solutions. China’s leadership dictates that cockpit hardware-software standards have a profound impact on worldwide automotive trends.

India next-generation digital cockpit market in electronics grows along with urbanization and electrification waves. Panasonic’s growth through Virtual SkipGen in AWS Marketplace in March 2025 demonstrates India’s increased demand for cockpit system simulation. Domestic OEMs such as Tata Motors and Mahindra make connected cockpit features a mandated option in EV launches. FAME-II and PLI schemes drive indirect acceptance of digital components. Middle-class aspirations fuel infotainment system improvements in lower segments as well. Telematics-integrated cockpits are adopted by fleet operators to enhance operational efficiency. Affordability combined with smart technology defines India’s cockpit innovation strategy.

North America Market Insights

North America next-generation digital cockpit market is likely to observe growth of more than 10% through 2035. U.S. OEMs are focusing on integrating drive assist, cloud services, and smooth infotainment solutions. For instance, in January 2025, CES featured significant advancements in AI-enabled digital cockpits through platforms such as Qualcomm Snapdragon and NVIDIA DRIVE Thor. Federal regulatory initiatives for cybersecurity in connected cars facilitate secure cockpit developments. Demand for smart, personalized mobility experiences from customers propels further cockpit complexity. The EV craze fosters further demand for next-generation digital interfaces. Strategic collaborations between tech companies and automakers drive quick cockpit ecosystem development.

The U.S. holds leadership positions in cockpit software innovation, led by tech companies and electric vehicle (EV) centric automakers. In January 2024, Hyundai and Amazon announced a partnership integrating Alexa into U.S.-market-oriented models, featuring smart cockpit capabilities. Tesla, Rivian, and Ford are leading in AI-infused cockpit offerings. Vehicle architectures defined by software quicken scalable cockpit implementation. Furthermore, consumer demand for hassle-free smartphone integration into cars continues to be a leading growth driver. Industry regulatory directions focusing on data privacy and protection are in tune with cockpit system design. Flexible finance schemes, along with subscription cockpit upgrades, are set to become popular in the U.S. markets.

Canada next-generation digital cockpit market gains from expanding EV penetration as well as connected vehicle programs. Aptiv’s USD 45 million investment in its Chennai (exporting globally) base in February 2025 testifies to the intensifying demand for North American cockpit technology. Canada’s ZEV mandates complement further cockpit system uptake, optimized for electrification. OEMs are designing cockpits specifically for extreme weather operability. Public and fleet’s electrification policies promote smarter dashboards along with remote system diagnosis. Data interoperability standards in Canada promote ecosystem cooperation. Rising consumer focus on tech-enhanced interiors supports market growth in premium and mainstream segments.

Next-Generation Digital Cockpit Market Players:

- Hyundai Mobis

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Continental AG

- Faurecia SE

- Garmin Ltd.

- HARMAN International

- Visteon Corporation

- Robert Bosch GmbH

- Aptiv PLC

- DXC Technology Company

The next-generation digital cockpit market is highly competitive, fueled by innovation at all hardware, software, and connectivity levels. Continental AG, Denso Corporation, Faurecia SE, Garmin Ltd., HARMAN International, Hyundai Mobis, Panasonic Corporation, Pioneer Corporation, Visteon Corporation, Robert Bosch GmbH, Aptiv PLC, and DXC Technology Company are top players in this space. Suppliers are focused on developing modular architectures, AI-enabled customization, and cloud-enabled upgradability. Strategic partnerships among tech companies and OEMs are becoming more essential to ensure differentiation in cockpit solutions.

Garmin and Qualcomm introduced a new Snapdragon Cockpit Elite-enabled solution in April 2025, featuring rich graphics, AI, and smooth infotainment integration. The move strengthens the trend towards immersive, connected, and smart cockpit experiences in the industry. Collaborations like Hyundai-Samsung SmartThings and Unity-Mazda indicate the growing power of non-automotive players in shaping developments in HMI. Innovation in digital cockpits remains at the core of automakers' differentiation strategies. Technology integration, regulatory adherence, and consumer-centric design ensure cockpit disruption continues in the sector.

Here are some leading players in the next-generation digital cockpit market:

Recent Developments

- In April 2025, DXC Technology partnered with Ferrari to develop the driver Human-Machine Interface (HMI) for next-generation vehicles. The collaboration focuses on creating intuitive and personalized cockpit experiences through advanced software engineering and design.

- In March 2025, ECARX announced plans to provide digital cockpit solutions to Volkswagen Brazil and Skoda, expanding its presence in the global automotive market. The partnership includes integrating ECARX's Antora 1000 platform, featuring voice recognition and navigation services.

- Report ID: 7573

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.