Molded Interconnect Devices Market Outlook:

Molded Interconnect Devices Market size was valued at USD 3.1 billion in 2025 and is expected to reach USD 12.1 billion by the end of 2035, growing at around 14.6% CAGR during the forecast period i.e., 2026-2035. In 2026, the industry size of molded interconnect devices is assessed at USD 3.5 billion.

The global molded interconnect devices (MID) market has expanded alongside industrial demand for compact electronic assemblies in transportation, medical equipment, and telecommunications infrastructure. Manufacturing output for the components that combine structural housing with the integrated circuit paths has increased as original equipment manufacturers seek to reduce the part counts and assembly steps. The OEC 2024 data reported that world trade of printed circuit boards reached USD 52.4 billion, indicating sustained industrial reliance on advanced interconnect solutions. The National Institute of Standards and Technology has documented that additive manufacturing processes, including those used for 3D circuit formation adoption, are increasing across U.S. electronics manufacturing, reflecting measurable industry migration toward integrated molding and metallization methods.

Trade Flow of Printed Circuit Boards, 2024

|

Country |

Import (USD billion) |

Export (USD billion) |

|

China |

5.28 |

26 |

|

China Taipei |

4.52 |

4.93 |

|

South Korea |

2.87 |

4.57 |

|

Hong Kong |

8.06 |

1.63 |

|

Vietnam |

4.62 |

2.07 |

Source: OEC 2024

Besides, the federal manufacturing initiatives, Industrie 4.0 programs continue to promote smart factory deployment and machine-to-machine communication infrastructure, driving requirements for smaller and more durable electronic components in industrial environments. According to the International Energy Agency, in May 2025, global electric car sales exceeded 17 million units in 2024, representing more than 20% of total vehicle sales, reinforcing long-term demand for compact sensor modules, radar systems, and power electronics integration. Further, Congress.gov August 2025 in the U.S has expanded broadband and next-generation connectivity investments through the Broadband Equity Access and Deployment Program, which is allocating USD 42.45 billion to communication infrastructure upgrades. This is supporting demand for compact RF components, antennas, and integrated electronic modules used in telecommunications equipment, where MID manufacturing techniques can support reduced size and improved assembly efficiency.

Key Molded Interconnect Devices Market Insights Summary:

Regional Highlights:

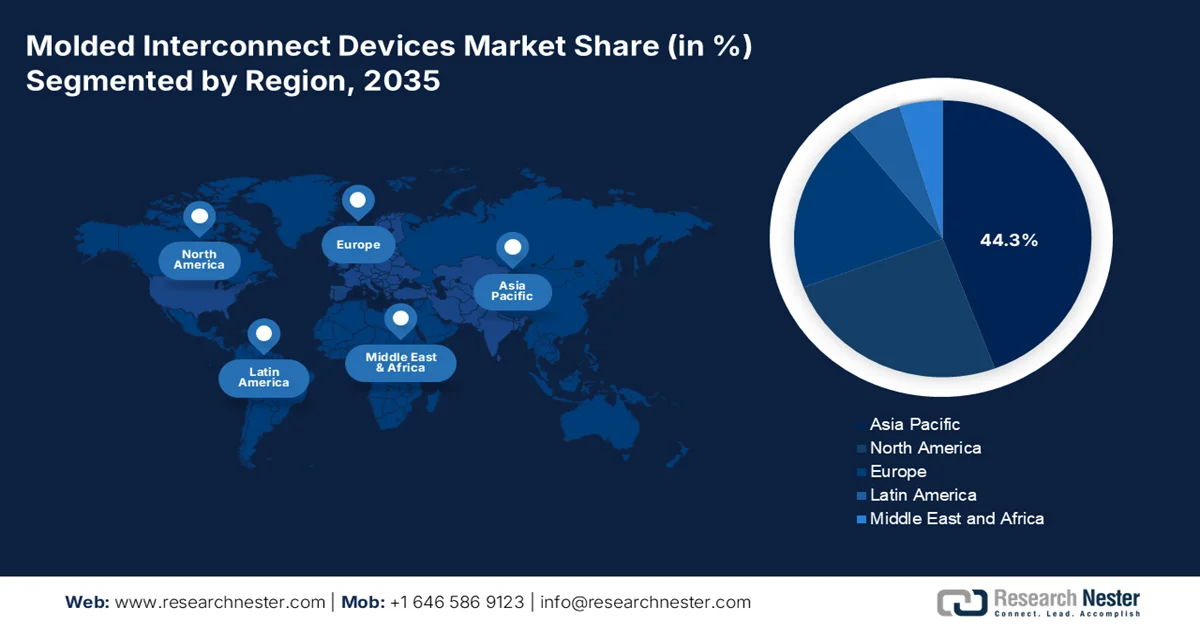

- The Asia Pacific region is anticipated to command 44.3% of the molded interconnect devices market share by 2035, propelled by expanding consumer electronics manufacturing, telecom infrastructure deployment, and automotive production capabilities

- North America is forecast to witness the fastest CAGR of 10.5% during 2026–2035 in the market, fueled by rising adoption of remote cardiac monitoring devices, defense electronics, and automotive sensor applications

Segment Insights:

- The direct OEM supply channel is projected to account for 71.3% of the molded interconnect devices market by 2035, owing to increasing preference among automotive, medical, and consumer electronics manufacturers for direct supplier partnerships ensuring supply chain control and customized integration

- Laser direct structuring is expected to remain the leading technology segment in the market through 2035, stimulated by rising demand for miniaturized wearable electronics, 5G modules, and medical telemetry devices requiring compact and highly reliable 3D circuit integration

Key Growth Trends:

- Rising government spending on medical electronics

- Growth in consumer electronics and wearable devices

Major Challenges:

- High initial capital investment

- Shortage in technical workforce

Key Players: Harting Technologiegruppe (Germany), Molex, LLC (U.S.), TE Connectivity Ltd. (Switzerland), LPKF Laser & Electronics SE (Germany), MacDermid Enthone Industrial Solutions (U.S.), Mitsubishi Engineering-Plastics Corporation (Japan), Selerant Engineering Srl (Italy), Yomura Technologies (Japan), RTP Company (U.S.), Tepro GmbH (Germany), Severity (Sweden), Cicor Group (Switzerland), Sarrel Group (Italy), IMSE GmbH (Germany), LPKF Japan Co., Ltd. (Japan), SelectConnect Technologies (South Korea), MID Solutions (U.S.), SABIC (Saudi Arabia), Amphenol Corporation (U.S.), SENKO (Japan).

Global Molded Interconnect Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.1 billion

- 2026 Market Size: USD 3.5 billion

- Projected Market Size: USD 12.1 billion by 2035

- Growth Forecasts: 14.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (44.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Malaysia, Vietnam, Mexico, Thailand

Last updated on : 14 May, 2026

Molded Interconnect Devices Market - Growth Drivers and Challenges

Growth Drivers

- Rising government spending on medical electronics: Healthcare digitization and the connected medical device deployment are increasing the demand for compact electronic assemblies that support the miniaturized and lightweight designs. The U.S. National Institutes of Health has expanded funding for wearable health monitoring biosensors and digital health technologies through multiple federal research programs. The U.S. Food and Drug Administration (FDA) has also accelerated approvals for connected diagnostic systems and remote patient monitoring devices. MID structures are increasingly used in hearing aids, wearable sensors, surgical instruments, and implantable electronics because they combine conductive pathways and mechanical structures within limited device space.

- Growth in consumer electronics and wearable devices: Government-supported digital transformation programs and rising consumer electronics production are supporting the MID market demand in wearables, audio devices, AR/VR systems, and compact smart devices. According to the International Telecommunication Union, in October 2023, global internet usage exceeded 5.4 billion people, increasing demand for connected electronics and portable communication devices. Governments in APAC, particularly Japan and South Korea, continue investing in electronics manufacturing competitiveness and next-generation digital infrastructure. MID technology enables thinner and lighter product designs while improving antenna integration and internal space utilization, making it increasingly relevant for compact consumer devices. Manufacturers are also using MID structures to reduce assembly complexity and improve product durability.

- Government-led semiconductor manufacturing expansion: The expansion of the CHIPS for the U.S. programs is emerging as a significant growth driver for the molded interconnect devices market because it strengthens domestic semiconductor production, advanced packaging capacity, and next-generation electronics manufacturing. According to the NIST March 2024 data, the U.S. Department of Commerce established two dedicated CHIPS for America offices, including the CHIPS Program Office managing USD 39 billion in manufacturing incentives and the CHIPS Research and Development Office overseeing USD 11 billion for semiconductor R&D initiatives. As semiconductor manufacturers and OEMs increase production of compact sensors, RF modules, and high-density electronic systems, demand for integrated circuit structures compatible with MID manufacturing is expected to rise.

Challenges

- High initial capital investment: The primary barrier to entry in the molded interconnect devices (MID) market is the significant capital expenditure required for specialized LDS lasers injection molding machines with precision tooling and electroless plating lines. For smaller manufacturers, this upfront cost can be prohibitive, especially when compared to traditional PCB assembly lines that leverage more available or multi-purpose equipment. The cost of developing high-precision molds for complex 3D circuit paths is also a major financial hurdle that favors large, established players with deep R&D budgets.

- Shortage in technical workforce: There is a notable global scarcity of engineers and technicians proficient in the interdisciplinary skills required for MID production, which merges polymer science, laser processing, and circuit design. The shortage of skilled labor is a primary constraint on molded interconnect devices (MID) market expansion, potentially limiting the ability of new entrants to scale production and maintain quality standards. Addressing this requires significant investment in specialized training programs and collaboration with technical institutions, which poses a logistical and financial challenge for new MID market entrants.

Molded Interconnect Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

14.6% |

|

Base Year Market Size (2025) |

USD 3.1 billion |

|

Forecast Year Market Size (2035) |

USD 12.1 billion |

|

Regional Scope |

|

Molded Interconnect Devices Market Segmentation:

Sales Channel Segment Analysis

The direct OEM supply channel dominates the molded interconnected devices market and is expected to capture the largest share value of 71.3% by 2035. This dominance is due to the large automotive, medical, and consumer electronics manufacturers preferring direct partnerships with MID component suppliers to ensure design confidentiality, supply chain control, and cost efficiency. The direct OEM contracts enable custom LDS parameters, just-in-time delivery, and joint R&D for application-specific 3D circuits. According to the ACMA July 2025 data, the manufacturing sales via direct B2B channels in the electronic components sector grew by 9.6% YoY, reflecting a broader shift away from third-party distribution. This trend is driven in MID because devices like cardiac telemetry antennas and 5G smartphone modules require tight integration with OEM assembly lines.

Technology Segment Analysis

Laser direct structuring is the dominant technology in the molded interconnected devices market because it enables the creation of high-precision three-dimensional circuit traces directly onto injection-molded thermoplastic components. The process begins with a laser activating specific areas on the molded part, followed by an electroless copper plating step that deposits metal only on the laser-treated regions. This eliminates the need for the masks, tooling changes, or additional assembly steps. LDS is mainly valued for the manufacturing of miniaturized antenna sensor housings and medical telemetry devices, where space is constrained. Its ability to integrate the mechanical and electrical functions into a single molded component reduces the weight, assembly costs, and points of failure. As demand grows for wearable electronics, 5G modules, and ambulatory cardiac monitors, LDS remains the preferred MID technology for its design flexibility, scalability, and repeatability across high-volume production environments.

Process Segment Analysis

The single-shot injection molding combined with the LDS activation process leads the molded interconnected devices market because it simplifies manufacturing by producing a single thermoplastic substrate that is subsequently laser-activated and plated. This process reduces tooling costs compared to the two-shot molding and eliminates the alignment errors between the multiple material layers. It is particularly favored for high-volume production of antenna sensor housings and medical telemetry enclosures. According to the KVI Online March 2023 data, injection molding is expected to expand at 3.5%, with the single-shot methods being more energy efficient than multi-shot alternatives. This efficiency, combined with the lower scrap rates and the faster cycle times positions single-shot + LDS as the process of choice.

Our in-depth analysis of the molded interconnect devices (MID) market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Process |

|

|

Material |

|

|

Application |

|

|

End use Industry |

|

|

Component |

|

|

Sales Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Molded Interconnect Devices Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating the MID market and is expected to hold the regional revenue share of 44.3% during the forecast period in the molded interconnect devices market. The region is driven by the concentration of consumer electronics manufacturing, telecommunications infrastructure deployment, and automotive production. China leads in volume, integrating MID antennas directly into the smartphone housing, laptop hinges and wearable devices to reduce the assembly steps and weight. Japan contributes via precision manufacturing for automotive sensors and medical telemetry components using its advanced injection molding and laser structuring capabilities. India and Malaysia are emerging as the cost-competitive production hubs for contract manufacturers serving global electronics brands. The growth is further supported by the government initiatives promoting domestic electronics manufacturing and foreign direct investment in specialty material compounding and LDS equipment installation across the region.

Active growth in semiconductor manufacturing, electric vehicle production, and electronics exports is shaping the molded interconnect devices (MID) market in China. According to the Our China Story October 2024 data, the nation produced more than 9.49 million new energy vehicles, strengthening demand for compact electronic systems used in battery management, sensors, and vehicle connectivity applications. The OEC 2024 data reported that integrated circuit exports exceeded USD 171 billion, reflecting sustained expansion in advanced electronics manufacturing and interconnect technologies. Moreover, the National Bureau of Statistics of China stated that high-technology manufacturing investment increased during 2024, supported by national industrial modernization policies. These trends are stimulating the adoption of lightweight and integrated circuitry solutions compatible with MID manufacturing across automotive, telecommunications, and industrial automation sectors.

Japan molded interconnect devices (MID) market is experiencing a strong growth and reached USD 120.40 million in 2025, and is expected to reach USD 144.00 million by the end of 2026. Moreover, the MID market is estimated to reach USD 468.00 million by 2035, escalating at a CAGR of 14% during the assessed period. The nation is driven by the rising semiconductor and AI-related investments. According to the NHK World April 2026 data, Japan’s industry ministry announced plans to provide Rapidus with an additional USD 4 billion for semiconductor research and development. The Japanese government also plans to invest more than USD 62.8 billion in semiconductors and AI by fiscal 2030 to strengthen domestic chip production capacity. These initiatives are stimulating the demand for compact and high-density electronic integration technologies supporting MID adoption across automotive electronics, telecommunications equipment, industrial automation, and advanced computing applications in Japan.

North America Market Insights

The North America is projected to be the fastest-growing region in the molded interconnect devices (MID) market, expanding at a CAGR of 10.5% during the assessment period, 2026 to 2035. The MID market is defined by steady demand from the medical device, defense, and automotive electronics sectors. The U.S. leads in the adoption of remote cardiac monitoring devices and smart munitions fuzing systems, where reliability under harsh conditions is critical. Canada contributes via its automotive supply chain, producing MID-based sensors and lighting modules for electric vehicle platforms. The regional MID market benefits from a mature ecosystem of LDS equipment suppliers, specialty material compounders, and contract manufacturers with defense and medical certifications.

The rising federal investment in advanced electronics manufacturing, aerospace systems, and connected infrastructure is shaping the molded interconnected devices market in the U.S. According to the U.S. Department of Commerce, August 2024 data, the government has announced more than USD 30 billion in proposed semiconductor manufacturing awards under the CHIPS Act to strengthen domestic electronics production capacity, supporting demand for compact circuit integration technologies used in MID-based assemblies. The Federal Aviation Administration reported that commercial aerospace manufacturing shipments in the U.S. increase the requirements for lightweight and space-efficient electronic systems in avionics and communication modules. Additionally, the TMF 2023 data stated that federal agencies invested over USD 100 billion annually in information technology modernization and digital infrastructure programs, accelerating the deployment of compact networking and communication electronics compatible with MID manufacturing techniques.

Increasing investments in electric vehicle manufacturing and advanced industrial production are shaping the molded interconnect devices market in Canada. In April 2024, Honda Motor Co. announced plans to establish a comprehensive EV value chain in Ontario with an investment of approximately USD 15 billion, including EV assembly and battery manufacturing facilities. The project is expected to increase demand for compact electronic architectures used in sensors, battery-management systems, and communication modules, where MID technologies support space-efficient integration. Moreover, the Government of Canada's October 2024 report indicates that the manufacturing revenues increased from USD 22.3 billion in 2022 to USD 27.0 billion in 2023, representing 21.2% annual growth. Further, the total manufacturing revenues reached USD 28.1 billion in 2023, highlighting a continued growth in the advanced manufacturing activity that supports the adoption of integrated electronic components across automotive and industrial sectors.

Total Revenues in Manufacturing vs. Non-Manufacturing Activity, 2020-2023

|

Type of Output |

2020 |

2021 |

2022 |

2023 |

% change 2022 - 2023 |

|

Manufacturing revenues |

USD 20.9B |

USD 19.8B |

USD 22.3B |

USD 27.0B |

21.2 |

|

Other revenues |

USD 1.3B |

USD 822.7M |

USD 1.1B |

USD 1.1B |

-8.6 |

|

Total revenues |

USD 22.1B |

USD 20.6B |

USD 23.4B |

USD 28.1B |

19.8 |

Source: Government of Canada October 2024

Europe Market Insights

Strength in automotive engineering industrial automation and medical device manufacturing is shaping the medical interconnect devices market in Europe. Germany serves as the primary hub home to several MID technology pioneers and LDS equipment manufacturers. Europe automakers utilize MID for the steering wheel controls lighting modules and the sensor housings valuing the technology's ability to reduce wiring harness complexity and improve vibration resistance. The industrial sector adopts MID for the robotic grippers and smart factory sensors where compact integrated electronics provide the reliability in harsh production environments. Medical device firms in Switzerland Italy and the UK leverage MID for the miniaturized hearing aids drug delivery systems and surgical instruments. Europe places strong emphasis on sustainable manufacturing processes, with multiple collaborative research initiatives focused on the recyclable LDS grade polymers and reduced metal additive usage.

Rising semiconductor investments and strong electronics export activity are fueling the growth in the molded interconnect devices (MID) market in Germany. According to the European Commission, December 2025 data, the European Commission approved USD 672.8 million in Germany state aid to support the establishment of new semiconductor manufacturing facilities in Dresden and Erfurt, including USD 534.6 million for GlobalFoundries and USD 138.2 million for X-FAB. These projects are aligned with the European Chips Act and are expected to strengthen regional production of advanced electronic components and integrated circuitry. On the other hand, the OEC 2024 data indicates that Germany exported USD 939 million worth of printed circuit boards globally, reflecting the country’s strong position in electronics manufacturing and interconnect technologies. These data show increasing demand for electronic integration solutions supporting MID adoption in various sectors.

The molded interconnect devices market in the UK is expanding due to increasing government support for semiconductor development, aerospace electronics, and electric mobility manufacturing. According to the UK government's May 2023 data, the government introduced a National Semiconductor Strategy backed by up to USD 1.33 billion in funding over the next decade to strengthen domestic semiconductor design and advanced electronics capabilities. The UK Parliament May 2025 data indicates that the UK manufacturers produced more than 775,000 motor vehicles in 2023, supporting the demand for the integrated electronic modules used in EV systems, lighting, and driver assistance technologies. Moreover, the UK Civil Aviation Authority reported continued growth in aerospace and avionics activity, increasing procurement of lightweight and compact electronic systems. These developments are supporting wider adoption of MID technologies in the UK.

Key Molded Interconnect Devices Market Players:

- Harting Technologiegruppe (Germany)

- Molex, LLC (U.S.)

- TE Connectivity Ltd. (Switzerland)

- LPKF Laser & Electronics SE (Germany)

- MacDermid Enthone Industrial Solutions (U.S.)

- Mitsubishi Engineering-Plastics Corporation (Japan)

- Selerant Engineering Srl (Italy)

- Yomura Technologies (Japan)

- RTP Company (U.S.)

- Tepro GmbH (Germany)

- Severity (Sweden)

- Cicor Group (Switzerland)

- Sarrel Group (Italy)

- IMSE GmbH (Germany)

- LPKF Japan Co., Ltd. (Japan)

- SelectConnect Technologies (South Korea)

- MID Solutions (U.S.)

- SABIC (Saudi Arabia)

- Amphenol Corporation (U.S.)

- SENKO (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Harting Technologiegruppe is a dominant player in the molded interconnect devices (MID) market, using its expertise in industrial connectivity to miniaturize and integrate electronic functions into the 3D molded components. The company utilizes the advanced Laser Direct Structuring to produce the rugged MID market solutions for automotive, medical, and industrial automation sectors.

- Molex LLC drives innovation in the molded interconnect devices (MID) market by combining its deep expertise in high-speed connectors with 3D molded electronics for compact and lightweight applications. The company has pioneered MID-based antenna systems and sensor housings for smartphones, wearables, and automotive LiDAR.

- TE Connectivity Ltd. is a global leader in the molded interconnect devices (MID) market, focusing on harsh environment applications such as medical devices, aerospace, and electric vehicles. The company utilizes MID technology to create miniaturized multifunctional components that replace traditional printed circuit boards. In 2025, the company made sales of USD 6,552 million in APAC.

- LPKF Laser & Electronics SE is a critical enabler of the molded interconnect devices market, providing the laser direct structuring equipment and process know-how used by most MID manufacturers worldwide. The company’s LDS lasers selectively activate conductive paths on injection-molded plastics, allowing for rapid prototyping and high-volume production of 3D circuits. In 2024, the company made a revenue of USD 122.9 million.

- MacDermid Enthone Industrial Solutions is a key materials supplier in the molded interconnect devices (MID) market, specializing in electroless copper and nickel-plating chemistries for LDS and two-shot molding processes. Their proprietary metallization systems enable high-adhesion fine-line circuitry on a wide range of thermoplastic substrates used in mobile cardiac telemetry, hearing aids, and automotive sensors.

Here is a list of key players operating in the global molded interconnect devices (MID) market:

The molded interconnect devices market is moderately consolidated, with key players from Europe, Japan, and the U.S. leading due to the advanced laser direct structuring technology. Strategic initiatives include capacity expansions, partnerships with automotive and medical device OEMs, and investments in 3D molded electronics. For example, in August 2025, Amphenol Corporation acquired Trexon. Asian manufacturers are gaining ground via cost-competitive solutions and increased R&D in the miniaturized antennas for 5G and IoT. Mergers and acquisitions are common as firms seek to integrate the full-service offerings from material sourcing to injection molding. Sustainability is emerging as a focus with companies developing recyclable LDS substrates.

Corporate Landscape of the Molded Interconnect Devices (MID) Market:

Recent Developments

- In February 2026, Molex introduced Impress Co-Packaged Copper Solutions, a compression-based on-substrate connector and mating cable assembly that delivers near ASIC connectivity at 224Gbps PAM‑4 and beyond. Its compact, durable socket simplifies maintenance and future-proofs high-density AI and hyperscale data center architectures.

- In November 2024, TEMPE, the National Institute of Standards and Technology, part of the U.S. Department of Commerce, announced that it plans to award as much as USD 100 million to Arizona State University and Deca Technologies for the SHIELD USA initiative.

- In March 2024, SENKO, a pioneering force in Co-Packaged Optical Communication, continues its journey toward global leadership in optical interconnects. This marks a significant milestone as the company launches a ground-breaking innovation: a detachable version of its cutting-edge high-density Metallic PIC Connector (MPC).

- Report ID: 5506

- Published Date: May 14, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.