mHealth Market Outlook:

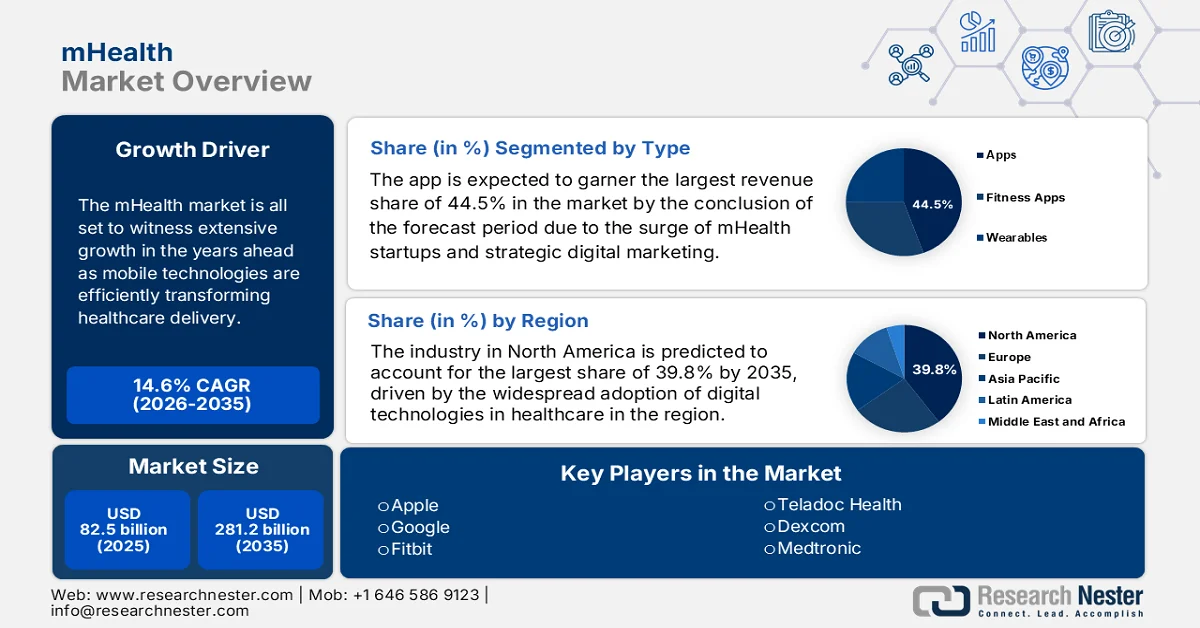

mHealth Market size was valued at USD 82.5 billion in 2025 and is projected to reach USD 281.2 billion by the end of 2035, rising at a CAGR of 14.6% during the forecast period, i.e., 2026-2035. In 2026, the industry size of mHealth is assessed at USD 94.5 billion.

The mobile health (mHealth) market is all set to witness extensive growth in the years ahead as mobile technologies are efficiently transforming healthcare delivery. Increasing adoption of smartphones, wearable devices, and health apps is encouraging a major shift toward remote monitoring. In March 2025, Smile Foundation reported that quality healthcare access in rural India faces certain challenges due to a shortage of medical professionals. In this context, telemedicine and mobile health solutions, i.e., mobile medical units, effectively bridge this gap by delivering remote consultations, monitoring important health metrics, and providing on-site care directly to underserved communities. On the other hand, initiatives such as the Smile Foundation’s Smile on Wheels program are successful models, which combine mobile clinics and telemedicine to expand healthcare access, reduce costs, and improve outcomes for rural populations.

Furthermore, the integration with emerging technologies such as artificial intelligence, cloud computing, and telemedicine is expanding the scope and capabilities of mobile health (mHealth) market solutions. According to the article published by the American Medical Association (AMA) in May 2024, telehealth played a critical role during the COVID-19 public health emergency, which has expanded access to care for rural and underserved populations by allowing patients to receive services from home. The study noticed that 74% of physicians in the year worked in practices offering telehealth, which is nearly three times the share in 2018, highlighting the presence of widespread adoption. Permanent expansion of telehealth, supported by bills such as the CONNECT for Health Act, collectively aims to ensure equitable access, enhance chronic disease management, reduce emergency visits, and integrate hybrid models of care nationwide.

Key mHealth Market Insights Summary:

Regional Highlights:

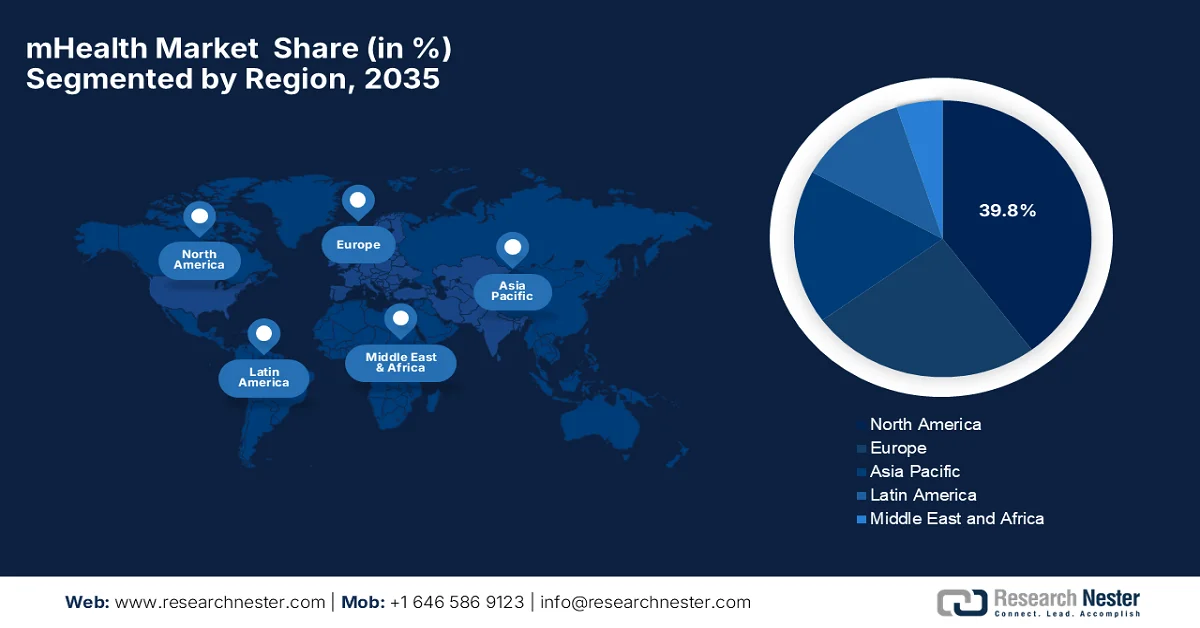

- North America mHealth market is projected to hold a dominant 39.8% revenue share by 2035, reinforced by widespread adoption of digital healthcare technologies and advanced IT and telecommunication infrastructure

- Asia Pacific is anticipated to witness the fastest growth in the market during 2026–2035, fueled by rising smartphone penetration and accelerating digital transformation in healthcare

Segment Insights:

- In the mHealth market, the app segment is forecasted to secure a 44.5% revenue share by 2035, propelled by the surge in mHealth startups and strategic digital marketing initiatives

- The remote monitoring services segment is expected to capture a significant share by 2035, stimulated by the growing geriatric population requiring continuous health monitoring

Key Growth Trends:

- High and growing prevalence of chronic diseases

- Widespread smartphone penetration and connectivity

Major Challenges:

- Data privacy and security

- User engagement and digital literacy

Key Players: Apple Inc. (U.S.), Google LLC (U.S.), Fitbit Inc. (U.S.), Teladoc Health Inc. (U.S.), DexCom Inc. (U.S.), Medtronic plc (U.S.), Koninklijke Philips N.V. (Netherlands), Siemens Healthineers AG (Germany), BioTelemetry Inc. (U.S.), Withings S.A. (France), Omron Healthcare Co., Ltd. (Japan), Sony Group Corporation (Japan), Samsung Electronics Co., Ltd. (South Korea), LG Electronics Inc. (South Korea), ResMed Inc. (Australia), Nabla (France), Amazon One Medical (U.S.), Telstra Health Pty Ltd (Australia), Tata Consultancy Services Limited (India), Practo Technologies Private Limited (India), BookDoc Holdings Sdn Bhd (Malaysia), DoctorOnCall Sdn Bhd (Malaysia)

Global mHealth Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 82.5 billion

- 2026 Market Size: USD 94.5 billion

- Projected Market Size: USD 281.2 billion by 2035

- Growth Forecasts: 14.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (39.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 23 March, 2026

mHealth Market - Growth Drivers and Challenges

Growth Drivers

- High and growing prevalence of chronic diseases: The rising burden of chronic diseases such as diabetes, cardiovascular diseases, respiratory illnesses, obesity, and hypertension requires ongoing monitoring and management. This can be met with mHealth solutions, and this long‑term care need is a major driver for the mHealth market. According to the WHO November 2024 reports, the diabetes cases surged from 200 million three decades ago to 830 million in 2022, wherein the prevalence is rising faster in low- and middle-income countries. In 2021, diabetes directly caused 1.6 million deaths, while kidney disease due to diabetes added another 530,000 deaths, and high blood glucose contributed to 11% of cardiovascular deaths. The report highlights that globally, 14% of adults aged above 18 had diabetes in 2022, and over 95% of cases were type 2 diabetes, underscoring a huge growth potential for the mobile health (mHealth) market.

Global Diabetes Statistics 2025: Prevalence, Growth, and Key Factors

|

Statistic |

Value |

|

Adult population (20–79 years) living with diabetes |

11.1% (1 in 9 adults) |

|

Adults are unaware they have diabetes. |

Over 4 in 10 |

|

Projected adults with diabetes by 2050 |

1 in 8 adults (853 million) |

|

Increase in diabetes prevalence by 2050 |

46% |

|

Percentage with type 2 diabetes |

Over 90% |

|

Adults living with diabetes in 2024 |

589 million |

|

Adults living in low- and middle-income countries |

81% |

|

Adults with undiagnosed diabetes |

252 million |

Source: IDF

- Widespread smartphone penetration and connectivity: The higher adoption rates of smartphones efficiently expand access to mobile health apps and services, thereby pushing mHealth adoption in both developed and emerging mobile health (mHealth) markets. Improved digital literacy also supports this trend. In April 2023, the data from the World Economic Forum stated that as of 2022, there were more than 8.5 billion mobile phone subscriptions worldwide, surpassing the global population of 7.9 billion. Besides, the report underscored that more than 5.4 billion people in 2023 have at least one mobile subscription, highlighting the ubiquity of mobile connectivity. Therefore, this rapid growth reflects the transformative impact of mobile technology on global communication and digital access, thereby positively impacting the growth of the mobile health (mHealth) market.

- Demand for remote patient monitoring and telehealth: There has been a critical need to monitor patients outside clinical settings, which fuels demand for remote monitoring tools, virtual consultations, telemedicine platforms, as well as connected wearables. In September 2025, the study from the Telehealth Organization revealed that the global telemedicine mobile health (mHealth) market is projected to grow from a valuation of USD 146.9 billion in 2025 to a total of USD 251.5 billion by the end of 2030, reflecting a CAGR of 11.3%. The article also highlighted that remote monitoring, AI-based tools, and evolving insurance coverage are key drivers that are deliberately enhancing chronic disease management and behavioral health care. This growth highlights encouraging opportunities for clinicians to adopt best practices, leverage technology, and align with global trends in digital healthcare, hence benefiting the overall mHealth market.

Challenges

- Data privacy and security: Data privacy and security are considered to be major challenges in the mobile health (mHealth) market. Mobile health apps, wearable devices, and remote monitoring platforms collect sensitive personal information from users, which includes biometric data, medical history, and lifestyle habits. Therefore, any breaches or unauthorized access can impact patient confidentiality and result in heavy fines under laws such as HIPAA in the U.S. and GDPR in Europe. In this context, ensuring proper storage, encrypted data transmission, and robust authentication across multiple devices is considered to be complex, especially when integrating third-party applications. Therefore, companies operating in this field need to balance data accessibility for healthcare providers with stringent privacy protections.

- User engagement and digital literacy: This is yet another burden for the mHealth market since the aspects of user engagement and digital literacy significantly influence the effectiveness of mHealth solutions. Most of the patients, especially older adults or individuals in rural and underserved regions, find it challenging to use smartphone navigation, app interfaces, or wearable device management. These lower rates of digital literacy can result in reduced utility of remote monitoring and telehealth programs. On the other hand, high engagement is essential for chronic disease management, medication usage, and wellness tracking. To address this, educating patients and caregivers, along with ongoing support, is crucial, thus driving consistent usage and driving higher adoption rates in the mobile health technologies.

mHealth Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

14.6% |

|

Base Year Market Size (2025) |

USD 82.5 billion |

|

Forecast Year Market Size (2035) |

USD 281.2 billion |

|

Regional Scope |

|

mHealth Market Segmentation:

Type Segment Analysis

In terms of type, the app is expected to garner the largest revenue share of 44.5% in the mHealth market by the conclusion of the forecast period. The dominance of the segment is largely attributable to the surge of mHealth startups and strategic digital marketing. In addition, the mHealth apps can positively influence health outcomes by enabling efficient storage and management of health information, ultimately enhancing patient care. For instance, in April 2024, the Union Health Ministry of India launched the myCGHS iOS app, thereby giving CGHS beneficiaries easy access to healthcare services and electronic health records. It is developed by NIC teams, and this particular app enables appointment booking, lab report access, medicine history, claim status, and locating nearby wellness centers and hospitals, hence denoting a wider segment scope.

Service Segment Analysis

The remote monitoring services, which are a part of the service segment, are anticipated to capture a significant revenue share in the mobile health (mHealth) market by the end of 2035. The growth of the segment is highly driven by the global geriatric population, as older adults are more susceptible to chronic conditions and require regular health monitoring. Based on the officially reported data in November 2025, the UK government and NHS are rolling out new digital technologies to deliver faster, more convenient care at home, freeing up to 500,000 appointments annually. Remote monitoring through the NHS App will allow patients to share health data such as blood pressure and oxygen levels directly with specialists, reducing hospital visits and easing staff workload. It also mentioned that a world-first trial will support motor neurone disease patients with remote breathing care, along with pilots in ENT, gastroenterology, respiratory medicine, urology, and cardiology.

Application Segment Analysis

In the application segment, the healthcare apps subtype is anticipated to grow with a considerable revenue share in the mobile health (mHealth) market during the discussed timeframe. The segment’s growth is largely driven by the rising demand from both patients and providers for streamlined, real‑time care management. In this context, Samsung Health in February 2026 launched the find care feature in partnership with PharmEasy and Tata 1mg, which allows users to order medicines, book diagnostic tests, and consult doctors online directly within the app. This particular integration eliminates the need to switch between multiple apps while enhancing accessibility and convenience for users. Hence, with such continued innovations from the leading pioneers, the segment is expected to grow exponentially in the upcoming years.

Our in-depth analysis of the mHealth market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Service |

|

|

Application |

|

|

Format |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

mHealth Market - Regional Analysis

North America Market Insights

North America mobile health (mHealth) market is expected to garner the largest revenue share of 39.8% during the forecast period. The region’s leadership is efficiently driven by widespread adoption of digital technologies in healthcare, advanced IT and telecommunication infrastructure, and high internet and smartphone penetration. In February 2026, the American Hospital Association reported that CMS has announced the launch of its Medicare app library, allowing beneficiaries access to a wide range of digital health tools under its Health Technology Ecosystem framework. It underscored that these apps will focus on eliminating manual check-in forms, providing AI-powered assistants, and supporting diabetes and obesity management, hence, strengthening digital care options for Medicare patients. Furthermore, the active investments by numerous market players in digital marketing, coupled with increasing healthcare expenditures, significantly fuel the expansion of the mHealth market in the region.

The U.S. mHealth market is undergoing a significant transformation, which is driven by the widespread adoption of wearable devices, shifting the healthcare landscape toward remote, patient-centered care. This growth is efficiently fueled by the presence of major technology giants and healthcare providers, which are heavily investing in integrated ecosystems that sync medical data in real-time, supported by favorable regulatory updates and expanded reimbursement policies for remote monitoring. In October 2023, Cedars-Sinai announced the launch of Cedars-Sinai Connect, which is a mobile app offering 24/7 urgent care and same-day primary care appointments. It is developed in partnership with K Health, and the app uses AI to streamline intake, reduce clinician workload, and provide patients with quick access to expert care, hence positively influencing the market’s expansion and exposure.

A major shift toward patient-centric care and the integration of virtual services into provincial healthcare systems is the main driving factor for the mobile health (mHealth) market in Canada. Growth is largely driven by the government's backing and supportive regulatory frameworks in the country. In February 2026, the Government of Canada introduced Bill S-5, the Connected Care for Canadians Act, with a main goal to modernize health data sharing and build a more connected healthcare system. The article also underscored that 29% of providers securely share patient information outside their offices, whereas others are still relying on fax machines. This particular legislation will mandate common digital health standards, ensuring the secure exchange of medical records across systems while respecting privacy laws. Furthermore, the Act aims to improve patient safety, support AI-based innovations, and strengthen the country’s healthcare efficiency as well as competitiveness.

APAC Market Insights

The mHealth market in the Asia Pacific is expected to grow at the fastest rate during the forecast period. The region’s pace of progress is highly supported by high smartphone penetration and a massive push toward digital transformation in healthcare. Government initiatives aimed at improving rural medical access, particularly in countries such as China, India, and Japan, are driving the adoption of telemedicine and remote monitoring platforms. According to the article published by the Organization for Economic Co-operation and Development in November 2024, due to the COVID-19 pandemic, there are life expectancy gaps of more than 10 years between countries and inequalities in terms of child mortality. Besides, mental health burdens are also high, wherein disorders and self-harm account for almost a quarter of disability years, underscoring the urgent need for investment in equitable, regularly accessible services to achieve long-term recovery and progress.

The domestic internet giants and online hospitals play a central role in reshaping the mobile health (mHealth) market in China. These factors help in addressing any imbalances in terms of medical resource distribution between urban and rural areas. The country’s market is gradually making a shift toward integrated digital platforms that offer everything from AI-assisted screenings to virtual consultations and chronic disease management for a rapidly aging population. In this context, the NIH article published in May 2025 states that a study on telemedicine in China utilized 25,499 online reviews from major platforms, and the research analyzes user perceptions of service quality through a hybrid deep-learning framework combining Servqual and CNN-BiLSTM models. The findings show that users have an increased prioritization of service quality, particularly the professional competence of doctors, as a key factor influencing satisfaction and health outcomes. Overall, the study highlights the prominence of telemedicine in enabling accessible and consumer-centered healthcare services.

The mHealth market in India is undergoing a profound transformation, effectively fueled by the government's Ayushman Bharat Digital Mission, which aims to create a unified digital health infrastructure across the country. The ecosystem in the country represents a startup landscape that is focused on AI-based diagnostics, virtual consultations, and pharmacy delivery services. The article published by the Press Information Bureau (PIB) disclosed that as of February 2024, more than 566.7 million Ayushman Bharat Health Accounts have been created, and over 348.9 million health records have been digitally linked. This particular initiative connects patients, healthcare professionals, and health facilities through platforms such as the ABHA App and Aarogya Setu. In addition, the mission enables digital health records and digital connectivity, thereby improving healthcare accessibility across the country’s vast geography.

Europe Market Insights

A supportive regulatory environment and a strong emphasis on data privacy are responsible for uplifting the overall mobile health (mHealth) market in Europe. Growth in the region is largely propelled by a shift toward value-based healthcare and the increasing integration of digital tools into national health systems. The region’s aging population drives high demand for remote patient monitoring and telemedicine solutions. In October 2024, the WHO reported that telehealth has rapidly expanded across the region, wherein 40 countries have adopted national or integrated digital health strategies. The report underscores that Norway stands out as a leader in terms of teleradiology for more than 30 years and advancing telemedicine and telepsychiatry, supported by innovations such as AI-based diagnostics and platforms such as eMeistring. Further, Norway’s trials show both improved patient safety and concerns over cost-effectiveness, highlighting the need for sustainable strategies aligned with the WHO’s 2023-2030 digital health action plan.

The higher consumer adoption of wearable devices, health apps, and digital fitness tools is driving the mHealth market in Germany. The fast-track system for digital health applications in the country has positioned it as a predominant leader in terms of incorporating mobile tools into a statutory health insurance framework, ensuring that digital treatments for conditions such as anxiety, diabetes, and sleep disorders are reimbursed. As per the NIH February 2024 article, the digital health companion, which is an mHealth app developed in the country for statutory health insurance users, targets physical activity, nutrition, and stress management. Besides, its development emphasized user participation through usability testing, including the think-aloud method, identifying 103 usability issues, and achieving a system usability scale score of 82/100. Therefore, the study highlights that user-centered design and early engagement are highly essential for long-term adoption and effectiveness of preventive mHealth applications.

The mHealth market in the UK is witnessing extensive growth, which is primarily shaped by the digital transformation strategies from the country’s government. Growth is also fueled by a high level of digital literacy among the population and a clear regulatory roadmap that ensures clinical safety and efficacy. In July 2025, the country’s government launched a 10-year health plan, which will transform the NHS App into a complete digital front door, enabling patients to book and manage appointments, access medicines, self-refer to specialist services, and connect wearable health data with AI-based advice. This particular plan introduces a single patient record by consolidating medical histories securely and improving care coordination, saving the NHS an estimated USD 246 million over three years. Features such as My NHS GP, My Medicines, My Children, and My Vaccines will provide personalized health management, hence positively impacting the mHealth market’s growth and exposure.

Key mHealth Market Players:

- Apple Inc. (U.S.)

- Google LLC (U.S.)

- Fitbit Inc. (U.S.)

- Teladoc Health Inc. (U.S.)

- DexCom Inc. (U.S.)

- Medtronic plc (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- BioTelemetry Inc. (U.S.)

- Withings S.A. (France)

- Omron Healthcare Co., Ltd. (Japan)

- Sony Group Corporation (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- LG Electronics Inc. (South Korea)

- ResMed Inc. (Australia)

- Nabla (France)

- Amazon One Medical (U.S.)

- Telstra Health Pty Ltd (Australia)

- Tata Consultancy Services Limited (India)

- Practo Technologies Private Limited (India)

- BookDoc Holdings Sdn Bhd (Malaysia)

- DoctorOnCall Sdn Bhd (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Apple leads the entire consumer-facing mHealth sector through its Apple Watch, iPhone, and Health app ecosystem, which integrates fitness tracking, heart monitoring, sleep analysis, and research participation. The company is highly focused on partnerships with leading hospitals and AI-based insights, which are giving it a strategic edge in this sector.

- Google benefits from its vast technology ecosystem, which includes Google Fit, Wear OS, and AI analytics, with a prime focus on enhancing personal health tracking and digital wellness. Strategic initiatives adopted by the company include AI-based predictive health insights and the integration of mHealth capabilities into its Android ecosystem to expand global reach.

- Fitbit is now under Google and is identified as a pioneer in wearable fitness and health tracking devices, including heart rate, sleep, activity, and stress monitoring. The brand is highly focused on user engagement, personalized coaching, and integration with health platforms.

- Teladoc Health is a prominent player in terms of telemedicine and remote patient monitoring, which is offering virtual care, chronic condition management, and AI-assisted consultations. The company’s platforms efficiently integrate mHealth apps, wearable data, and electronic health records to provide personalized care.

- Dexcom specializes in terms of continuous glucose monitoring systems for diabetes management. Its mHealth solutions combine wearable sensors with mobile apps to provide glucose tracking, alerts, and data sharing with healthcare providers.

Below is the list of some prominent players operating in the global mobile health (mHealth) market:

The mHealth market is a cluster of global technology giants, healthcare device manufacturers, and digital health startups. Leading companies such as Apple, Google, and Samsung Electronics leverage strong consumer ecosystems and wearable technologies with the main goal of expanding digital health capabilities. Healthcare giants such as Philips, Medtronic, and Omron Healthcare are highly focused on remote patient monitoring and connected medical devices. Meanwhile, telehealth providers such as Teladoc Health and regional platforms such as Practo concentrate on virtual care services. In this context, in January 2026, OpenAI announced ChatGPT Health, which is a dedicated experience especially designed to securely integrate personal health information with ChatGPT’s intelligence. It allows users to connect medical records and wellness apps for more personalized insights, by maintaining strict privacy protections with separate storage and encryption.

Corporate Landscape of the mobile health (mHealth) Market:

Recent Developments

- In February 2026, M Health Fairview selected the unified Ambient AI Assistant and Dictation platform from Nabla for system-wide deployment across its hospitals and clinics. The AI tool captures clinician-patient conversations within the Epic EHR and automatically generates structured clinical documentation.

- In January 2026, Amazon One Medical announced the launch of the health AI assistant in the One Medical app, which will offer 24/7 personalized guidance based on patients’ medical records, lab results, and medications while maintaining HIPAA-compliant security.

- In February 2025, Apple announced the launch of the Apple Health Study through the Apple Research app to explore how devices such as iPhone, Apple Watch, and AirPods can help improve physical and mental health monitoring.

- Report ID: 4256

- Published Date: Mar 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.