Integrated Automated Supply Chain Market Outlook:

Integrated Automated Supply Chain Market size was over USD 15.09 billion in 2025 and is anticipated to cross USD 29.13 billion by 2035, growing at more than 6.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of integrated automated supply chain is assessed at USD 16.01 billion.

The market is primarily driven by the adoption of robotics and automation in warehousing and logistics, as the proliferation of automation, robotics, and AI-powered systems is rebuilding the supply chain infrastructure. Technologies such as automated guided vehicles (AGVs), autonomous mobile robots (AMRs), and robotic picking systems enable faster, more accurate warehouse operations. As labor shortages and cost pressures rise, companies are automating material handling, order processing, and inventory management to boost throughput and reduce human error. This technological advancement is more prominent in retail, e-commerce, manufacturing, and third-party logistics.

A recent example illustrating the integration of robotics and automation in warehousing and logistics is Walmart’s strategic partnership with Symbotic. In January 2025, Walmart announced the sale of its Advanced Systems and Robotics business to Symbotic for USD 200 million. Concurrently, Walmart committed to investing USD 520 million in Symbotic’s AI-enabled robotics platform to automate over 400 Accelerated Pickup and Delivery centers (APDs) across its stores. This initiative aims to enhance Walmart’s e-commerce fulfillment capabilities by integrating advanced automation technologies. The deployment of Symbotic’s systems is expected to improve the efficiency and accuracy of online order processing, enabling faster customer pickups and deliveries. This move highlights how retail giants are scaling robotic automation to meet growing customer demand and enable efficient production.

Key Integrated Automated Supply Chain Market Insights Summary:

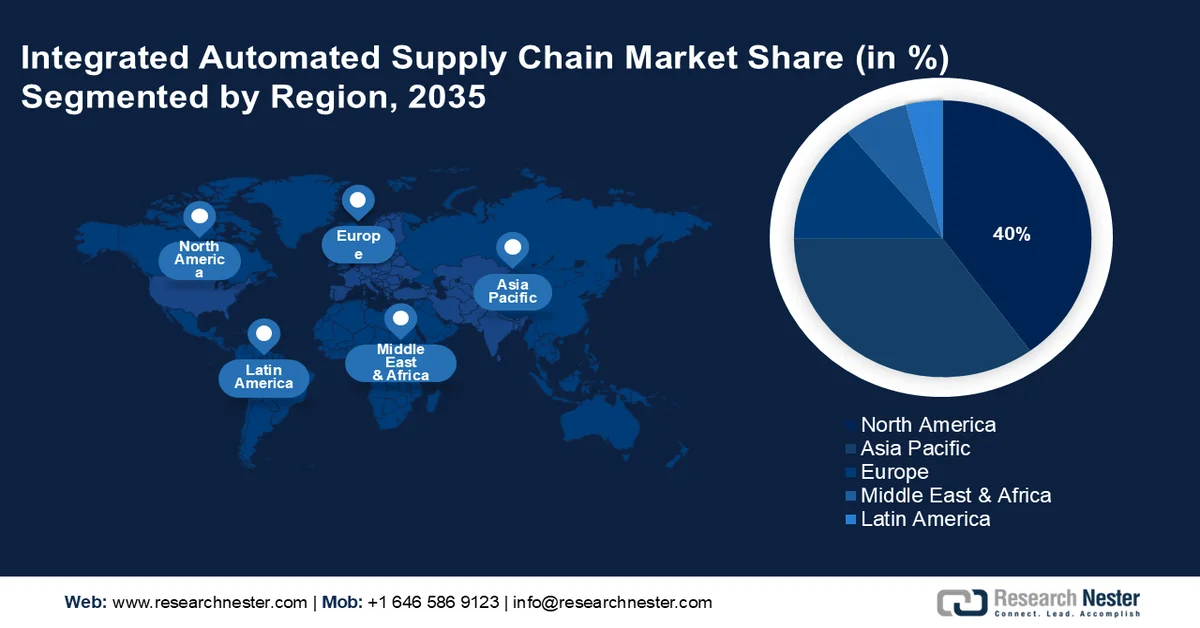

Regional Highlights:

- North America is projected to command over 40% revenue share of the integrated automated supply chain market by 2035, owing to the rapid expansion of e-commerce and rising adoption of automation to manage higher order volumes and labor constraints.

- Asia Pacific is expected to secure a substantial share of the integrated automated supply chain market through 2035, propelled by accelerating technological advancements and strong government support for digital infrastructure and smart manufacturing.

Segment Insights:

- Transportation management segment (TMS) segment is projected to hold over 35% share of the integrated automated supply chain market by 2035, driven by the escalating demand for efficient logistics operations and real-time shipment tracking capabilities.

- Large enterprises segment is anticipated to account for more than 60% revenue share by 2035 in the integrated automated supply chain market, fueled by substantial investments in AI-driven automation, robotics, and cloud-based systems to manage complex global logistics networks.

Key Growth Trends:

- Rising demand for real-time supply chain visibility and analytics

- Federal investments in smart infrastructure and manufacturing modernization

Major Challenges:

- High implementation costs and system integration complexity

- Cybersecurity and data privacy risks

Key Players: Oracle, Temenos, Riskconnect, Experian Information Solution, Inc., Ncontracts, Accenture, Logicmanager, Inc., LogicGate Inc., SAS Institute Inc., CompatibL.

Global Integrated Automated Supply Chain Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 15.09 billion

- 2026 Market Size: USD 16.01 billion

- Projected Market Size: USD 29.13 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: China, India, Singapore, South Korea, Japan

Last updated on : 25 February, 2026

Integrated Automated Supply Chain Market - Growth Drivers and Challenges

Growth Drivers

- Rising demand for real-time supply chain visibility and analytics: One of the most significant growth drivers is the surge in demand for real-time data analytics across end-to-end supply chain operations. Organizations are integrating AI, IoT, and machine learning into supply chain systems to enhance visibility into procurement, production, inventory, and logistics. Real-time analytics helps enterprises to respond faster to market changes, optimize resource allocation, and reduce risks of overstocking or understocking, which is crucial in today’s volatile market conditions.

- Federal investments in smart infrastructure and manufacturing modernization: Government-backed programs that promote smart manufacturing and digital infrastructure upgrades are fueling the adoption of integrated automation. The U.S. Department of Energy Advanced Manufacturing Office (AMO) promotes the deployment of smart manufacturing technologies that integrate digital tools into the supply chain. For instance, in January 2025, the U.S. Department of Energy (DOE) launched a USD 13 million funding opportunity through the State Manufacturing Leadership Program. This program aims to remove barriers preventing small and medium enterprises from adopting innovative, data-driven tools and technologies that strengthen the domestic manufacturing base.

- Rise of Industry 4.0 and digital twin integration: Industry 4.0 principles are accelerating the deployment of automation across the supply chain market. Technologies such as digital twins, i.e., virtual replicas of physical supply chains, allow real-time simulation, monitoring, and optimization of logistics workflows. For instance, in January 2025, KION Group, Accenture, and NVIDIA announced a strategic collaboration aimed at revolutionizing warehouse automation through the integration of artificial intelligence and digital twin technologies. This partnership focuses on creating advanced digital twins to optimize supply chain operations. By leveraging NVIDIA’s Omniverse platform, KION Group can simulate various aspects of warehouse operations such as facility layouts, robot fleet behaviors, and workforce allocation. Moreover, Accenture’s expertise in digital technologies enhances these simulations, enabling real-time analysis and continuous improvement of warehouse performance.

Challenges

- High implementation costs and system integration complexity: Deploying integrated automated systems requires significant capital investment in robotics, AI, IoT, and software infrastructure. Moreover, integrating new automation technologies into existing legacy systems can be technically complex and time-consuming, especially for small and medium enterprises. Many organizations face technical compatibility issues, data silos and workflow disruptions during the transition phase. Thus, the lack of skilled personnel to manage these integrated systems further complicates deployment.

- Cybersecurity and data privacy risks: As automation increases data interconnectivity across the supply chain, the risk of cyber attacks, data breaches, and compliance violations also rises. Cyber threats such as ransomware, system tampering, and industrial espionage can cause several operational disruptions and financial losses. Hence, ensuring robust cybersecurity and adhering to global data privacy regulations remain critical yet challenging tasks for organizations.

Integrated Automated Supply Chain Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 15.09 billion |

|

Forecast Year Market Size (2035) |

USD 29.13 billion |

|

Regional Scope |

|

Integrated Automated Supply Chain Market Segmentation:

Solution Type Segment Analysis

Transportation management segment (TMS) segment is estimated to hold integrated automated supply chain market share of over 35% by the end of 2035, due to the increasing need for efficient logistics and real-time shipment tracking. TMS solutions offer advanced features such as route optimization, freight management, and real-time data analytics, enabling companies to enhance operational efficiency and reduce costs. The rise of e-commerce and global trade has further amplified the demand for robust TMS platforms that can handle complex transportation networks and provide end-to-end visibility. Additionally, the integration of AI and IoT into TMS solutions has improved predictive analytics and real-time decision making, contributing to widespread adoption.

Company Size Segment Analysis

In integrated automated supply chain market, large enterprises segment is set to hold revenue share of more than 60% by 2035. Large enterprises are increasingly adopting integrated automated supply chain solutions to enhance operational efficiency and manage complex logistics networks. Their substantial financial resources enable significant investments in advanced technologies such as robotics, AI-driven analytics, and cloud-based systems. These tools facilitate real-time monitoring and streamlined processes, crucial for handling extensive product lines and global distribution channels. Additionally, the emphasis on cost reduction and improved customer satisfaction drives large organizations to implement automation, ensuring competitiveness in a rapidly evolving market.

Our in-depth analysis of the global market includes the following segments:

|

Solution Type |

|

|

Company Size |

|

|

Deployment Model |

|

|

Industry Vertical |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Integrated Automated Supply Chain Market - Regional Analysis

North America Market Insights

North America in integrated automated supply chain market is predicted to hold over 40% revenue share by the end of 2035, due to the rapid expansion of e-commerce. The surge in online shopping has compelled companies to adopt advanced automation technologies to efficiently manage increased order volumes and meet consumer expectations for swift deliveries. This trend is particularly evident in the U.S., where e-commerce sales reached USD 291.6 billion in the second quarter of 2024, reflecting a 1.3% increase from the previous quarter. In addition, companies are increasingly adopting automation to address labor shortages and rising wages while also improving accuracy and lowering costs.

The integrated automated supply chain market in the U.S. is rising speedily as enterprises prioritize supply chain resilience following recent global disruptions. A major growth driver is the increasing investments in warehouse and distribution center automation to streamline domestic logistics. For instance, in August 2024, Walmart announced the opening of five new automated distribution centers, each averaging 700,000 square feet. These centers utilize advanced storage facilities and robotic arms to customize pallets for individual stores, aiming to enhance efficiency in stocking its 4,600 U.S. stores and support the growth of its grocery delivery services. Manufacturers in the U.S. are leveraging automation to localize production and reduce dependency on international supply chains. This shift toward nearshoring, backed by smart technologies, is fueling demand for fully integrated and automated supply chain systems.

The integrated automated supply chain market in Canada is growing steadily, driven by substantial investments from major retailers and advancements in automation technologies. For instance, in January 2025, Walmart Canada announced a significant investment of USD 6.5 billion to expand its store network and enhance supply chain infrastructure, including the modernization of distribution centers, with five new supercenters in Ontario and Alberta by 2027 and a new Vaughan Distribution Centre in Spring 2025. Additionally, companies such as Metro are implementing automation to transform their supply chains aiming to improve efficiency and scalability. These developments reveal Canada’s commitment to enhancing supply chain resilience and competitiveness through integrated automation.

Asia Pacific Market Insights

Asia Pacific is anticipated to garner a significant market share during the forecast period due to rapid technological advancements and increasing e-commerce activities. China and South Korea are the leading countries leveraging innovations in artificial intelligence, IoT, and robotics to enhance supply chain efficiency and resilience. Government initiatives promoting digital infrastructure and smart manufacturing further bolster this expansion, positioning the region as a leader in supply chain automation.

China’s integrated automated supply chain market is advancing rapidly fueled by its strategic push towards Made in China 2025 and digital Silk Road Initiatives. The country is embedding AI and blockchain into logistics to optimize customs clearance and cross-border trade. Major tech firms such as JD.com are deploying fully automated warehouses powered by drones and autonomous vehicles. These innovations enhance supply chain agility and support China’s dominance in global manufacturing.

South Korea integrated automated supply chain market is advancing rapidly driven by significant advancements in Industry 4.0 technologies and government initiatives. The government has committed approximately USD 160 trillion under the Korean New Deal to enhance digital infrastructure, focusing on AI, IoT, and smart factories aiming to automate the manufacturing sector by 2025. These efforts help South Korea to lead in supply chain automation and digital transformation.

Integrated Automated Supply Chain Market Players:

- Siemens

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- KION GROUP AG

- KNAPP AG

- TGW Logistics Group

- WITRON Logistik

- Informatik GmbH

- EXOTEC Solutions SAS

- AutoStore AS

- Westfalia Technologies Inc

The top companies dominating the integrated automated supply chain market include Siemens, SAP, and Honeywell known for their end-to-end digital solutions and industrial automation systems. Amazon and Alibaba also play major roles with their highly automated fulfillment networks and AI driven logistics platforms. In addition, companies such as Zebra Technologies, and Dematic are shaping the space with advanced robotics and real time tracking innovations. Here are some leading players in the market:

Recent Developments

- In March 2025, Tompkins Solutions, a company that specializes in supply chain consulting and automation, and MSI Automate, a top provider of warehouse automation solutions, announced a merger of their respective companies. This move brings their strengths together to offer complete warehouse automation services. The new company will provide services such as supply chain consulting, equipment and system setup, support, and software for managing and controlling warehouses.

- In March 2025, FORTNA, a logistics automation and software company, partnered with Hai Robotics, a leader in warehouse automation. This partnership adds Hai Robotics’ HaiPick systems, automated tools for picking and storing items, to FORTNA’s lineup. The newest version, HaiPick Climb, will help FORTNA improve how customers store, pick, and ship their products.

- Report ID: 7567

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.