Hydraulic Fluids Market Outlook:

Hydraulic Fluids Market size was valued at USD 9.4 billion in 2025 and is expected to reach a significant value of USD 12.8 billion by the end of 2035 with a CAGR of 3.5% over the forecast duration 2026 to 2035. In 2026, the industry size of hydraulic fluids is estimated at USD 9.7 billion.

The global hydraulic fluids market is expected to witness noteworthy growth in the upcoming years, which is fueled by increasing industrialization, expansion in the mining, construction, and manufacturing sectors, and rising demand for efficient fluid power systems across various industries. In this context, the World Bank in 2026 reported that over the past decade, it has funded approximately USD 10 billion in mining projects, with lending in the sector expected to grow from USD 3 billion during FY21-25 to an estimated USD 17 billion in FY26-30. It also stated that global demand for key minerals such as copper, lithium, graphite, nickel, and rare earth elements is projected to nearly double by 2040, requiring more than 500 billion in new mining investment by 2040 and USD 1.7 trillion across mining, processing, and infrastructure by 2050. Hence, this drives the market growth by boosting demand for hydraulic systems and fluids used in mining equipment, construction machinery, and industrial automation.

Furthermore, on the raw materials side, the hydraulic fluids market is dependent on petroleum-based base oils, synthetic esters, and performance-enhancing additives. Besides, the supply continuity is closely associated with crude oil availability, refinery output, and the global chemicals manufacturing ecosystem. In December 2024, the International Energy Agency (IEA) revealed that global oil demand is forecasted to rise from 840 kb/d in 2024 to 1.1 mb/d in 2025, lifting total consumption to 103.9 mb/d, wherein the growth is mainly driven by petrochemical feedstocks while transport fuel demand remains constrained. It underscored that the global oil supply increased to 103.4 mb/d in November 2024, which is supported by recoveries in Libya and Kazakhstan, and is on track to grow by 1.9 mb/d in 2025, led primarily by non-OPEC+ countries, including the U.S., Brazil, Canada, Guyana, and Argentina, hence positively impacting the growth of the hydraulic fluids industry.

OPEC+ and Non-OPEC Crude Oil Production and Spare Capacity Overview (October-November 2024)

|

Group |

October 2024 Supply (mb/d) |

November 2024 Supply (mb/d) |

Spare Capacity (mb/d) |

|

Total OPEC-9 |

21.79 |

21.74 |

5.36 |

|

Total OPEC |

27.03 |

27.21 |

5.41 |

|

Total non-OPEC |

14.06 |

14.19 |

0.46 |

|

Total OPEC+ |

41.09 |

41.40 |

5.87 |

Source: International Energy Agency (IEA)

Key Hydraulic Fluids Market Insights Summary:

Regional Highlights:

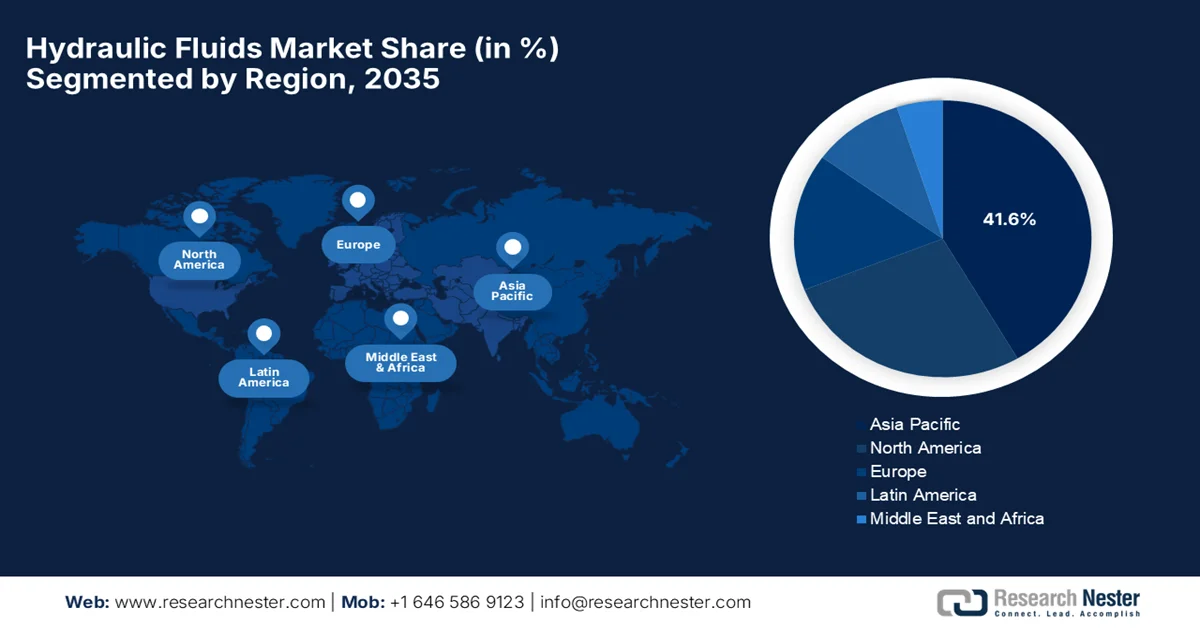

- The Asia Pacific hydraulic fluids market is projected to account for a 41.6% share by 2035, propelled by strong industrialization, infrastructure expansion, and rising demand for heavy equipment

- North America is anticipated to register the fastest growth in the market during 2026–2035 with a CAGR of 4.1%, fueled by increasing industrial activity and infrastructure modernization

Segment Insights:

- In the hydraulic fluids market, the mineral oil segment is forecast to secure a 56.5% share by 2035, owing to its cost efficiency and compatibility with existing equipment

- The construction segment is expected to witness significant share growth by 2035, driven by extensive use of hydraulic systems in heavy machinery and rising infrastructure investments

Key Growth Trends:

- Rapid industrialization

- Industrial automation & mechanization

Major Challenges:

- Environmental regulations and compliance

- Volatility in crude oil prices

Key Players: Exxon Mobil Corporation (U.S.), Chevron Corporation (U.S.), Phillips 66 Company (U.S.), Valvoline Inc. (U.S.), Shell plc (UK), BP plc (UK), TotalEnergies SE (France), FUCHS SE (Germany), Carl Bechem GmbH (Germany), Condat SA (France), Idemitsu Kosan Co., Ltd. (Japan), ENEOS Corporation (Japan), Penrite Oil Company Pty Ltd (Australia), GS Caltex Corporation (South Korea), Indian Oil Corporation Limited (India), Castrol India Limited (India)

Global Hydraulic Fluids Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 9.4 billion

- 2026 Market Size: USD 9.7 billion

- Projected Market Size: USD 12.8 billion by 2035

- Growth Forecasts: 3.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: India, Vietnam, Indonesia, Brazil, Mexico

Last updated on : 19 March, 2026

Hydraulic Fluids Market - Growth Drivers and Challenges

Growth Drivers

- Rapid industrialization: Growth in manufacturing, urbanization, and large infrastructure projects globally results in the increased utilization of heavy machinery such as excavators, loaders, and cranes that rely on hydraulic systems. As stated by the World Bank’s May 2024 article, in 2023, private infrastructure investment in low- and middle-income countries totaled almost USD 86 billion, which supported a broader range of projects across 68 countries and 322 projects, and is considered to be up from 54 countries and 260 projects in 2022. It also mentioned that energy investments tripled, largely in East Asia and the Pacific, with 97% of electricity generation projects being renewable. Among the world’s poorest nations, 26 IDA countries received a total of 53 projects worth USD 4.3 billion, highlighting the expanding deployment of heavy machinery, thus boosting demand in the hydraulic fluids market.

- Industrial automation & mechanization: Increased adoption of automation in sectors such as manufacturing, mining, and agriculture requires hydraulic systems that depend on quality fluids for efficient power transmission and control. In addition, the adoption of CNC machines, robotics, and automated conveyors increases the demand for heat-resistant hydraulic fluids. According to the official statistics kept forward by the International Federation of Robotics in November 2024, the global adoption of industrial robots in manufacturing has accelerated, with the average robot density doubling from 74 units per 10,000 employees in 2016 to 162 units in 2023. Europe led this adoption with Germany, Sweden, Denmark, and Slovenia among the most automated, whereas Asia Pacific sees strong growth driven by Korea, Singapore, China, and Japan. Meanwhile, North America also continues its automation expansion, in which the U.S. ranks tenth globally, hence denoting a lucrative growth opportunity for the hydraulic fluids market.

Global Robot Density in Manufacturing 2023: Top Countries and Regional Automation Trends

|

Country/Region |

Robot Density (units/10,000 employees, 2023) |

|

South Korea |

1,012 |

|

Singapore |

770 |

|

China |

470 |

|

Germany |

429 |

|

Japan |

419 |

|

U.S. |

295 |

|

European Union Average |

219 |

|

Asia Average |

182 |

|

Global Average |

162 |

Source: IFR

- Automotive sector growth: Expansion in the automotive industry, especially the rise of electric and hybrid vehicles, requires hydraulic fluids for steering, braking, and suspension systems. This factor supports the hydraulic fluids market growth. In this context, the data from IEA in 2025 states that global electric car sales surged past 17 million in 2024, representing over 20% of new car sales, and China led this at nearly half of global sales, and 1 in 10 cars on China’s roads are now electric. Besides, strong growth was also observed in emerging markets in the Asia Pacific and Latin America, whereas Europe and the U.S. maintained steady adoption despite the presence of policy fluctuations. The data states that production and trade expanded globally, with China producing over 70% of EVs and exporting 40% of the world’s electric cars, reflecting the automotive industry’s rapid global expansion and shift toward electrification, hence suitable for bolstering the hydraulic fluids market’s growth.

Top 10 Exporters of Hydraulic Brake Fluids to India in 2024 by Trade Value and Volume

|

Exporter |

Trade Value (USD 1000) |

Quantity (Kg) |

|

Japan |

6,340.06 |

2,589,560 |

|

European Union |

3,175.44 |

1,150,290 |

|

Germany |

2,534.08 |

1,055,550 |

|

Korea, Rep. |

2,059.47 |

896,262 |

|

China |

1,982.21 |

639,282 |

|

U.S. |

837.03 |

197,795 |

|

Malaysia |

659.22 |

50,119 |

|

Thailand |

614.57 |

235,013 |

|

UK |

574.35 |

102,609 |

|

Singapore |

556.08 |

77,818 |

Source: WITS

Challenges

- Environmental regulations and compliance: One of the major restraints for the hydraulic fluids market is the rising number of environmental regulations that are related to lubricant toxicity, biodegradability, and disposal. Both the governments and regulatory bodies across established and emerging nations have imposed strict guidelines on the use of mineral-oil-based hydraulic fluids due to their environmental impact if spilled or not disposed of properly. Most of the industries, such as marine, forestry, and construction, operate in environmentally sensitive areas where fluid leaks can lead to contamination in soil and water resources. As a result, manufacturers need to make investments in the development of biodegradable or environmentally acceptable hydraulic fluids, which in turn necessitates higher research and development costs.

- Volatility in crude oil prices: Hydraulic fluids need to be derived from petroleum-based base oils, which makes the hydraulic fluids market extremely sensitive to fluctuations in crude oil prices. Any changes in crude oil supply, production cuts, or global economic shifts can impact raw material costs for lubricant manufacturers across major nations. Therefore, the rise in oil prices adds pressure to companies, disrupting profit margins since customers in industries such as construction and manufacturing are highly price sensitive. Besides, the frequent price fluctuations make it difficult for suppliers to maintain stable pricing strategies and long-term supply contracts. The existence of these uncertainties in raw material costs can cause disruptions in production planning and reduce overall profitability for manufacturers in this field.

Hydraulic Fluids Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

3.5% |

|

Base Year Market Size (2025) |

USD 9.4 billion |

|

Forecast Year Market Size (2035) |

USD 12.8 billion |

|

Regional Scope |

|

Hydraulic Fluids Market Segmentation:

Base Oil Segment Analysis

The mineral oil is expected to dominate with the largest share of 56.5% in the hydraulic fluids market over the discussed time frame. Their cost efficiency when compared to synthetic or bio-based fluids and compatibility with existing equipment positions the subtype for dominance in this field. In this context, the International Organization of Standardization (ISO) in October 2023 has notified 11158:2023 standard, which sets minimum requirements for mineral-oil-based hydraulic fluids by covering key properties such as anti-wear protection, oxidation stability, and temperature performance for a wide range of hydraulic systems. It is formulated from mineral base stocks with additives; these fluids remain compatible with existing equipment and are widely used in industrial and mobile hydraulic applications. Therefore, this standard solidifies the dominance of mineral oil hydraulic fluids, contributing to wider hydraulic fluids market expansion.

End use Industry Segment Analysis

By the conclusion of the forecast period, construction, which is based on end use industry, is predicted to grow with a considerable share. The extensive use of hydraulic systems in excavators, loaders, bulldozers, and cranes is the main factor behind the sub-segment’s leadership. Infrastructure investment is also a major driver. Based on the data from Press Information Bureau (PIB) in February 2025, India has accelerated its infrastructure development, and the total investment rose to an amount of USD 120 billion in 2023‑24, driven by initiatives such as PM Gati Shakti, Bharatmala Pariyojana, and PMGSY, which enhance connectivity across roads, highways, and logistics networks. Meanwhile, the civil aviation sector has expanded rapidly, wherein the operational airports increased from 74 in 2014 to 157 by 2024, along with the growth in aircraft numbers, hence denoting a huge opportunity for the hydraulic fluids market in the construction sector.

Product Type Segment Analysis

In terms of product type, the anti-wear hydraulic fluids are anticipated to garner a considerable share in the hydraulic fluids market since they protect pumps and components operating under high pressure. AW fluids are best known to reduce friction and component degradation, thereby extending equipment lifespan and lowering maintenance costs, which makes them the highly preferred product type across industrial machinery and mobile hydraulic equipment. On the other hand, the OEM specifications for excavators and mobile cranes encourage AW fluids to comply with extended maintenance intervals and warranty requirements. The fluids also support energy efficiency by reducing hydraulic power losses in high-pressure circuits. Furthermore, several leading manufacturers have benefited from AW fluids in enhancing system reliability and operational uptime.

Our in-depth analysis of the hydraulic fluids market includes the following segments:

|

Segment |

Subsegments |

|

Base Oil |

|

|

End use Industry |

|

|

Product Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Hydraulic Fluids Market - Regional Analysis

APAC Market Insights

The Asia Pacific hydraulic fluids market is projected to be the largest regional market with 41.6% share during the forecasted period. The region’s market is largely driven by strong industrialization, infrastructure expansion, and heavy equipment demand in China and India. In addition, the aspect of agricultural mechanization also raises fluid usage through widespread deployment of tractors and harvesters. In April 2025, the report from the United Nations Industrial Development Organization (UNIDO) stated that the region is progressing in industrial production, energy access, and infrastructure development. The report underscored the need for advanced industrialization, green policies, and Industry 4.0 adoption across middle-income countries such as the Philippines, Malaysia, and Viet Nam. Policymakers and regional organizations stressed coordinated strategies and sustainable industrial growth to drive economic development, hence denoting a positive hydraulic fluids market outlook.

The extensive construction projects and large-scale industrial manufacturing are responsible for driving the hydraulic fluids market in China. There has been a heavy reliance on hydraulic machinery in mining operations and automated factories. Strong domestic production ensures cost efficiency and high-volume availability. In July 2025, the Civil Aviation Administration of China (CAAC) reported that it had granted airworthiness certification for SINOPEC AEH I, which is the first domestically developed fire-resistant aviation phosphate ester hydraulic oil, marking China as the third country globally capable of producing such aviation hydraulic oils. This certification efficiently validates its performance for energy transmission, lubrication, and heat conduction in aircraft hydraulic systems, ensuring operational safety, thus making it suitable for standard market growth.

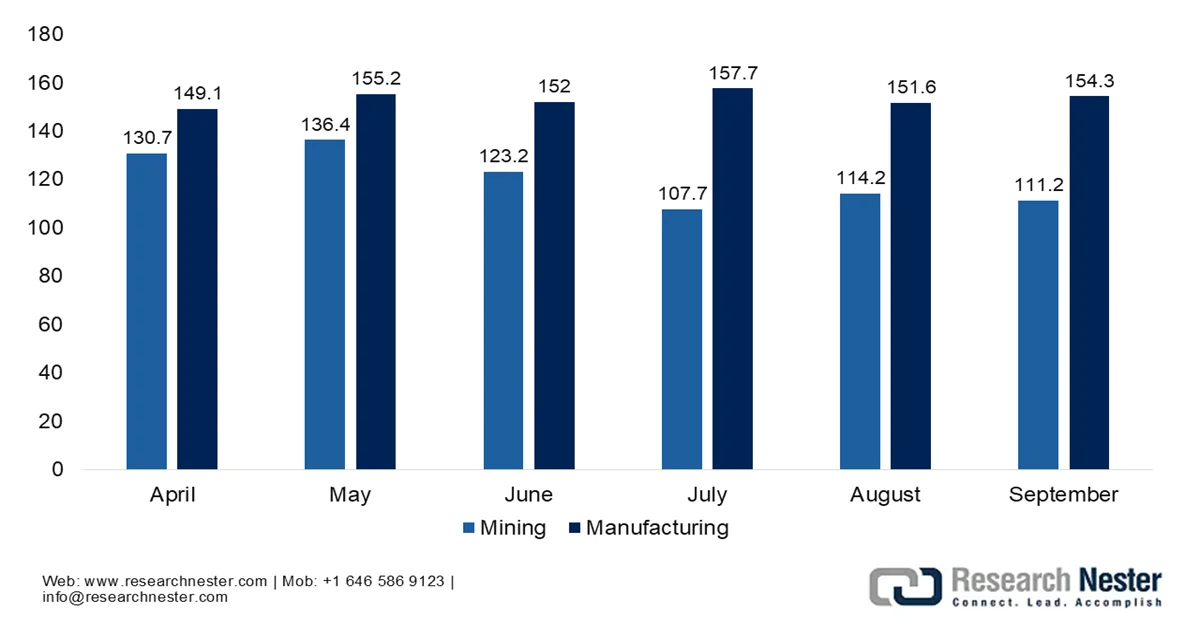

The increasing mechanization of the agriculture sector drives growth in the India hydraulic fluids market. The government pushes for self-reliance through suitable initiatives, and demand for high-performance fluids for construction machinery, automotive assembly lines, and mining equipment continues to rise. In this context, PIB in October 2025 stated that in September 2025, India’s Index of Industrial Production (IIP) grew by 4% year-on-year, which is primarily driven by a 4.8% increase in the manufacturing sector. It also mentioned that key contributors, which included Manufacture of basic metals 12.3%, Electrical equipment 28.7%, and motor vehicles, trailers and semi-trailers 14.6%. Among use-based categories, Infrastructure/Construction Goods increased by 10.5%, Consumer Durables with 10.2%, and Intermediate Goods represented a rise of 5.3% and led the growth, reflecting robust industrial and infrastructure activity.

Monthly Industrial Production Index Trends (Mining & Manufacturing) for 2025-2026

Source: PIB

North America Market Insights

The North America hydraulic fluids market is growing on account of widespread utilization of hydraulic systems in construction, manufacturing, and transportation sectors, with infrastructure upkeep and equipment modernization supporting steady fluid consumption. The strong distribution networks and operational reliability solidify the market stability. Based on the Federal Reserve System reports, which were published in February 2026, in January 2026, U.S. industrial production rose 0.7%, wherein the manufacturing output increasing 0.6% and utilities up 2.1%. The report also mentioned that capacity utilization for the overall industrial sector surpassed almost 76.2%, with manufacturing being at 75.6%, mining at 84.4%, and utilities at 72.9%, which reflects a steady industrial activity. Therefore, the data indicates that there is a continued growth in machinery, construction, and energy-related sectors, thereby supporting consistent demand for hydraulic systems and equipment.

The crude oil production capacity is the main fueling factor for the hydraulic fluids market in the U.S. The country is witnessing incremental demand, which is influenced by the resurgence of domestic manufacturing and a strong focus on technological innovation, such as the integration of smart sensors for predictive maintenance. The Energy Information Administration (EIA) stated that between 2020 and 2024, U.S. crude oil and lease condensate production grew by 1.9 million barrels per day, wherein 93% of this growth came from 10 counties in the Permian Basin, Texas, and New Mexico. It also mentioned the top contributors, which were Lea and Eddy counties in New Mexico (1 million b/d) and Martin and Midland in Texas (0.40 million b/d). In addition, these counties averaged 4.8 million b/d in 2024, representing 37% of total U.S. production, hence supporting operations that sustain demand for hydraulic equipment and fluids.

The hydraulic fluids market in Canada is growing at a notable pace, propelled by the country’s vast natural resource sectors, especially mining, automotive, forestry, and oil and gas extraction. The nation's diverse and harsh climate drives a specialized demand for multi-grade and low-viscosity fluids that can maintain performance during extreme winter operations. Based on the country’s government data in 2023, Canada’s hydraulic brake and transmission fluids sector products, which contain less than 70% petroleum oils, saw a total import value of USD 12.38 million, and the top 11 importers accounted for nearly 80% of imports. Major importers in the country are 49 North Lubricants Ltd., based in Alberta, AMSOIL Inc. from Ontario, and Esso Chemical Canada from Alberta, highlighting a concentrated market. Hence, the imports primarily support automotive and industrial applications across multiple provinces.

Europe Market Insights

The increased adoption rates in metal processing and automotive production are responsible for uplifting the hydraulic fluids market in Europe. The region’s stringent environmental regulations are driving demand for high-efficiency and environmentally friendly fluids, whereas the synthetic and bio-based formulations are being preferred to meet sustainability targets. In May 2023, the region’s Ecolabel for lubricants, by the Directorate-General for Environment, set strict environmental criteria to reduce the impact of lubricants on air, water, soil, and biodiversity. Besides, it promotes products that have limited hazardous substances, high performance, and the use of recycled or bio-based materials, thereby supporting sustainable hydraulic fluid adoption in Europe. Furthermore, the ongoing industrial modernization and regulatory compliance solidify the region’s position in global hydraulic fluid demand.

The strong industrial and manufacturing base positions the hydraulic fluids market in Germany for sustained growth in the upcoming years. Premium formulations offering thermal stability, wear protection, low toxicity, and operational efficiency are highly preferred, and ongoing construction projects further support demand. In January 2022, the country’s Federal Environment Agency stated that the Blue Angel Ecolabel for biodegradable lubricants and hydraulic fluids (DE-UZ 178) identifies products with the highest environmental performance within this category. It also stated that the revised criteria incorporate updated scientific understanding of ecotoxicity, degradation behavior, and verification systems for sustainably produced biogenic raw materials. In addition, the update also introduces requirements for post-consumer recycled packaging and reusable alternatives, and harmonizes standards with the region’s Ecolabel for lubricants.

The defense, transportation, and industrial manufacturing sectors are responsible for uplifting the UK hydraulic fluids market. Infrastructure upgrades and consistent use of hydraulic machinery in logistics and public works drive fluid replacement cycles. Import-reliant supply chains and industrial automation result in steady consumption, and ongoing equipment utilization underscores market development. According to the government data, which was published in January 2026, provisional hydrocarbon oil receipts for April to December 2025 reached USD 23.5 billion, which is an increase of USD 0.16 billion when compared with the same period in 2024. Petrol excise duty receipts totaled an amount of USD 9.3 billion, and diesel receipts amounted to USD 14 billion. Overall hydrocarbon oil receipts in 2025 amounted to USD 31.1 billion, indicating continued demand for oil-based fuels and products in the UK.

Key Hydraulic Fluids Market Players:

- Exxon Mobil Corporation (U.S.)

- Chevron Corporation (U.S.)

- Phillips 66 Company (U.S.)

- Valvoline Inc. (U.S.)

- Shell plc (UK)

- BP plc (UK)

- TotalEnergies SE (France)

- FUCHS SE (Germany)

- Carl Bechem GmbH (Germany)

- Condat SA (France)

- Idemitsu Kosan Co., Ltd. (Japan)

- ENEOS Corporation (Japan)

- Penrite Oil Company Pty Ltd (Australia)

- GS Caltex Corporation (South Korea)

- Indian Oil Corporation Limited (India)

- Castrol India Limited (India)

- Petronas Lubricants International (Malaysia)

- Sinopec Lubricant Company (China)

- LUKOIL Lubricants Company (Russia)

- HydraForce (U.S.)

- Lubrizol (U.S.)

- ContiTech (Germany)

- Eastman Chemical Company (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ExxonMobil Corporation is one of the leading players in this sector, which offers a wide range of mineral-based and synthetic hydraulic oils through its Mobil industrial lubricants portfolio. The company benefits from a strong presence in North America and the Asia Pacific through its integrated refining, additive technology, and global distribution network.

- Shell plc is yet another dominant company in the hydraulic fluids market, which is supported by its large lubricant manufacturing capacity and global supply chain across many countries. The company’s strategy is mainly focused on innovation in high-efficiency hydraulic fluids, which also includes biodegradable formulations and fire-resistant variants.

- Chevron Corporation is considered to be the central player in the hydraulic fluids sector through its Chevron Lubricants division. The company offers mineral and synthetic hydraulic oils, which are especially designed for high-pressure industrial equipment and mobile hydraulic systems.

- BP plc participates in the hydraulic fluids market primarily through its Castrol Industrial division, which produces the well-known Castrol Hyspin hydraulic fluid series. The company is primarily concentrated on high-performance fluids, which are designed for mobile hydraulics, industrial manufacturing systems, and heavy equipment operating in extreme conditions.

- TotalEnergies SE is also a key competitor in the hydraulic fluids industry, which is offering a systematic portfolio of industrial lubricants for sectors such as mining, construction, energy, and manufacturing. The firm makes investments in digital monitoring solutions that efficiently track lubricant degradation and equipment performance, thereby enabling predictive maintenance and longer service intervals.

Below is the list of some prominent players operating in the global hydraulic fluids market:

Major oil and chemical companies across different nations dominate the hydraulic fluids market due to their global refining capacity and established distribution networks. Companies such as Exxon Mobil Corporation, Chevron Corporation, and Shell plc are maintaining stronger positions in this field owing to their extensive lubricant portfolios as well as stronger OEM partnerships. Pioneers are opting for distinct strategies such as R&D investment in synthetic and acquisitions to expand specialty lubricant portfolios, and regional manufacturing expansion to strengthen supply chains in high-growth economies. In August 2024, PMC Hydraulics Group, which is backed by Dacke Industri, notified that it had acquired the remaining shares of Hydroquip Hydraulics in Bangalore to strengthen its footprint in India. Hydroquip is a leading distributor of Kawasaki and SUN hydraulic components, thus denoting a positive outlook for standard market growth.

Corporate Landscape of the Hydraulic Fluids Market:

Recent Developments

- In February 2026, HydraForce reported that it had partnered with Elevāt to deliver intelligent electro-hydraulic solutions that integrate hydraulics, electronics, and AI-based digital services for OEMs.

- In October 2025, Lubrizol introduced AH933ZF, which is a zinc-free hydraulic additive especially designed to deliver strong performance while reducing environmental impact. It offers improved hydraulic efficiency, making it suitable for industries such as mining, forestry, marine, and construction.

- In August 2025, ContiTech inaugurated its new USD 90 million hydraulics manufacturing facility in Mexico, spanning 900,000 sq. ft. The plant produces high-performance hydraulic hoses for industrial and mobile applications across construction, agriculture, mining, and energy sectors.

- Report ID: 4889

- Published Date: Mar 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.